Carry On

The Quotedian - Vol VI, Issue 50 | Powered by NPB Neue Privat Bank AG

“Leadership is not about the leader, it's about the ship”

— Simon Sinek

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

After last week’s back-to-back-to-back losing session for stocks as measured by the S&P 500, for a whooping loss of a bit more than one percent, today was a pretty quiet session with a positive drift. The S&P’s intraday chart quickly gives away what a day of nothingness it was:

But even so, breadth was very decent with 3 stocks up for every stock down and seven out of the eleven economic sectors closing higher, leaving us with following heatmap:

It is actually pretty attention amazing how the leading stocks of this year saw retreats in yesterday's session. But what is even more stunning, is that despite AAPL, GOOGL, AMZN, TSLA, MSFT and NVDA down on the day, the Nasdaq 100 still managed to squeeze out an 90% breadth day.

So, what’s going on? Some profit taking finally settling in? Or maybe rotation as the investors prepare for the next upleg.

As a matter of fact, that rotation argument sound pretty, well, eh, “sound”, as the Russell 2000 (small cap stocks) have been on a tear recently:

Not only are they up close the 10% in about a month, but also did they add 1.6% today after a 1.2% rally already on Friday. Watch this space …

Finally, as last comment to yesterday’s US equity session, one of the more worrying components was probably a 5% rally in non-profitable tech stocks (yes, Goldman Sachs has an index on that). This provides a sense of animal spirits and FOMO being heavily at work:

Asian stocks this morning are up across the entire region, with the largest gains registered in Honk Kong, Taiwan and Australia.

European equity futures point towards a very decent opening for cash markets, whilst US futures are hovering in positive territory too.

Other asset classes are quickly discussed, as hardly anything was going on.

Bond yields came down a little, probably not least to a nearly disinflationary inflation (what a mouthful) reading in China,

and a drop in the Manheim Used Car index in the US, which points to further inflation slowdown:

Here’s the 10-Year US treasury yield chart:

The yield downside was more limited in Europe:

Finally, the EUR/USD has been moving higher as is close to negate a potential shoulder-head-shoulder reversal pattern we had discussed on several occasions. That would be VERY bullish for this currency pair:

At the same time, a top in the US Dollar - Japanese Yen cross rate could also be in place,

which could finally push the US Dollar Index (DXY) below 101 and have medium- to long-term bearish implications for the greenback:

Time to hit the send button, but first …

In conclusion, Monday was quiet, but is this just the calm before the storm?

After all, the NATO meeting is kicking off today (Tuesday), and albeit the latest news (Monday night 22:30) is that Turkey agreed to the inclusion of Sweden (hours before it was rumoured that a Sweden inclusion would be tied to a Turkey EU inclusion), things can still change quickly.

Then on Wednesday, we get the most lagging the Fed´s favourite inflation indicator - The CPI

Thursday the US PPI number is due and without time to breath earnings season kicks off on Friday with some of the major banks reporting (JPMorgan, Citi, Wells Fargo, others).

Banks, next to tech stocks, are the major market segments to keep your eyeballs on this earnings season. Both could potentially lead to a market reversal, or paradoxically, an upside acceleration.

Have a great Tuesday,

André

CHART OF THE DAY

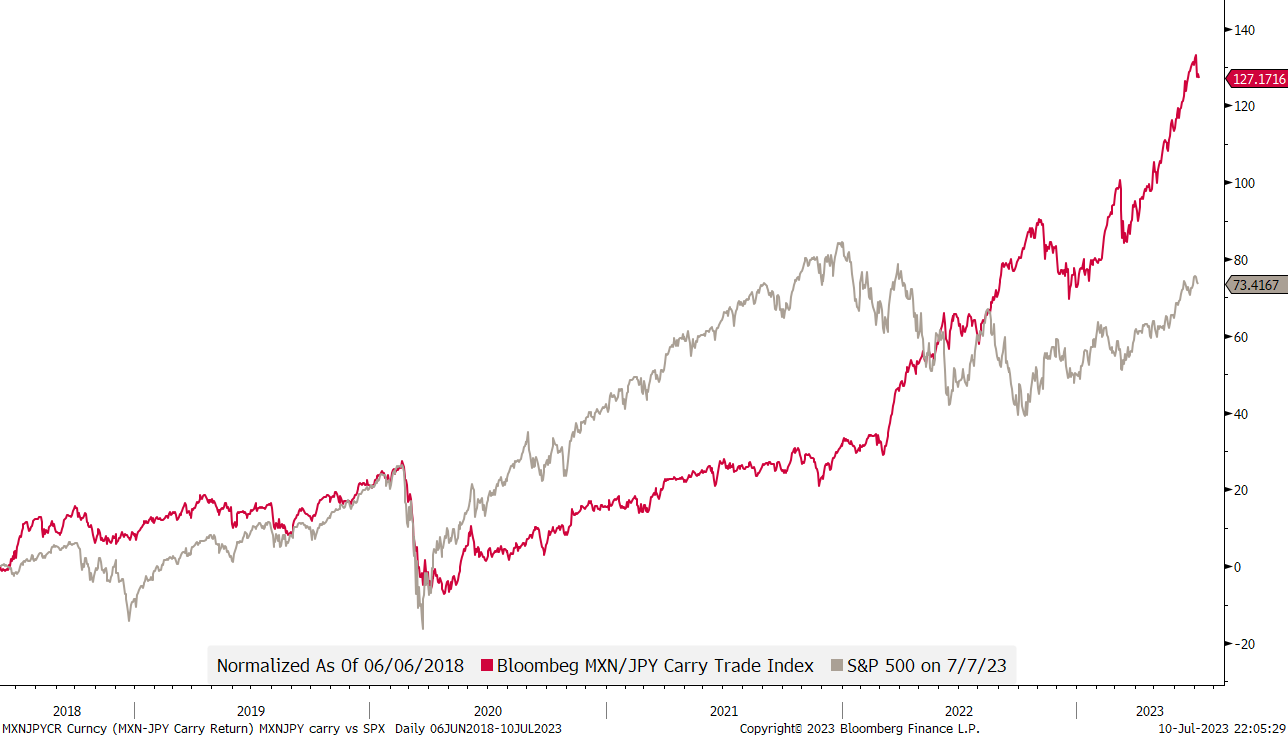

So, what is today’s mystery title “Carry On” referring to then?

What if I tell you that there’s a (relatively) simple strategy that nearly doubled the return of the S&P 500 over the past five years?

Don’t believe me? There you go:

A carry-trade strategy (in which money is borrowed cheaply in yen and then parked in pesos, where it can accumulate at higher Mexican interest rates) involving the Mexican Peso and the Japanese Yen would have more than double your money in five years, with not necessarily more volatility (risk) and, arguably, uncorrelated to equity strategies.

So, all we need to know now, is whether we should carry on with the carry trade or whether it is too late. Stay tuned …

Thanks for reading The Quotedian! Subscribe for free to receive new posts the moment they are published.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance