Damage-Control Reports, All Stations!

Vol IX, Issue 11 | Simplicity is the Ultimate Sophistication

“Risk — risk is our business. That’s what this starship is all about.”

— Captain Kirk

As an analyst friend posted on X:

"This is more of a Gulf War than the first two Gulf Wars were Gulf Wars."

He's right. Desert Storm and the 2003 invasion were land wars that happened to be near the Gulf. This one is the Gulf — the strait blocked, the waterway weaponised, Gulf states under direct fire, and every barrel that used to transit Hormuz now missing from the global supply chain. A bit more than two weeks in, it's time for a full damage-control report across all macro stations on the USS Enterprise HSS Quotedian.

Stock prices have been surprisingly resilient given the danger of a global recession

Many major indices continue to trade above their 200-day moving averages

Energy-price sensitive markets such as India have been hit harder

Bonds failed to function as safe haven, but are rather discounting higher inflation via higher yields

Credit spreads are widening, but unlikely war-induced instead rather provoked by fallout from the private credit sector

The US Dollar has strengthened against all other major currencies.

Oil continues to trade in backwardation, hence expressing the view of a relatively short-lived conflict in the Middle East

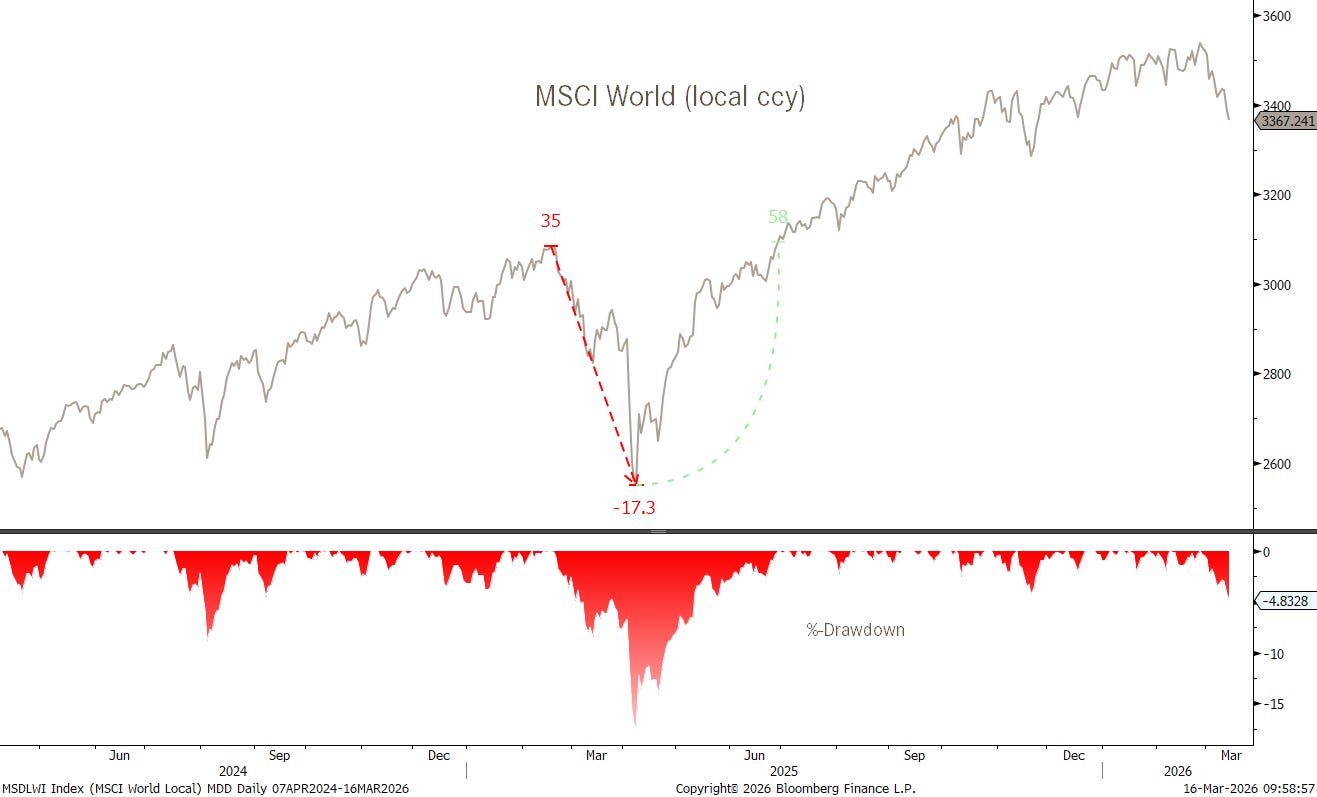

Global stocks (MSCI World) have started correction following the onset of the Iran war,

but at less than five percent drawdown so far and prices still above the 200-day moving average (see black line above), the ‘correction’ has been a walk in the park so far:

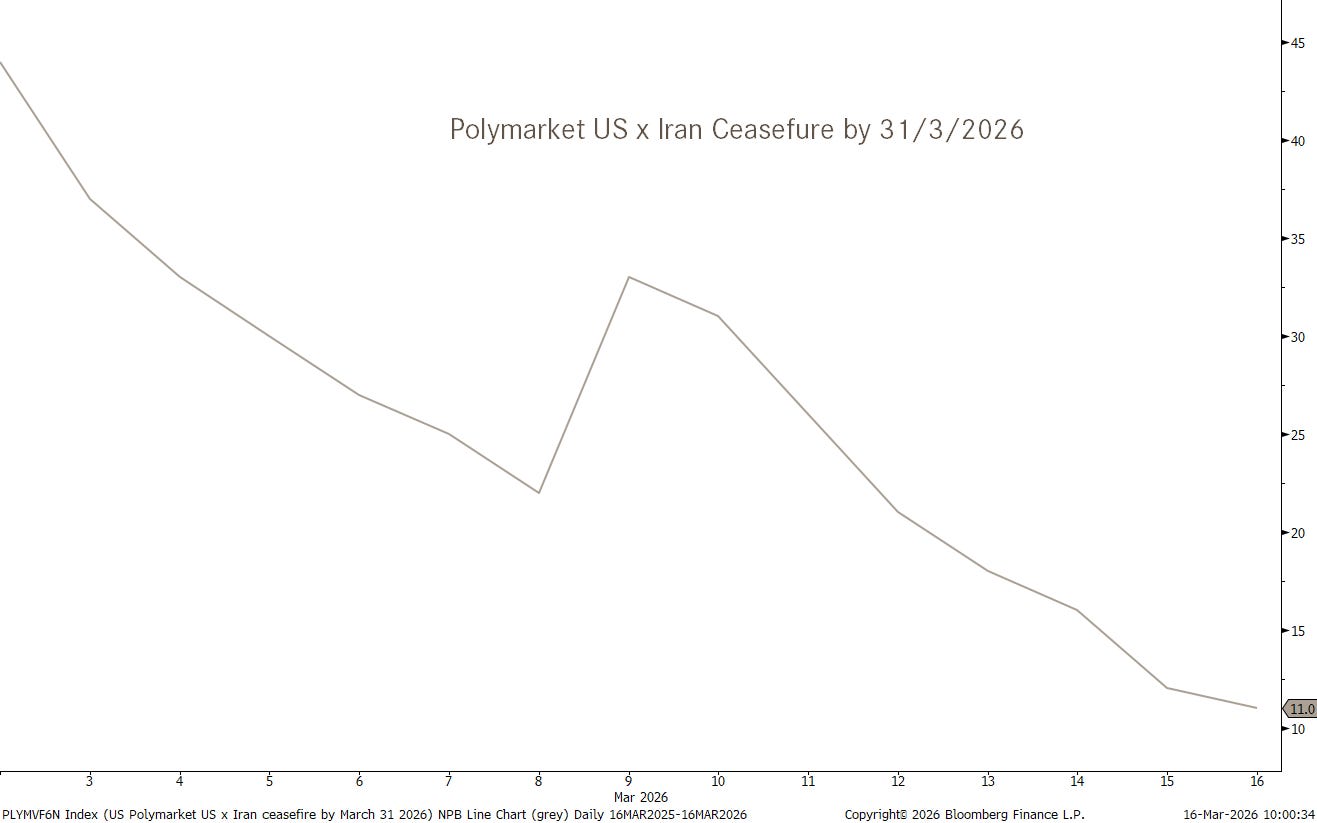

Are investors then betting on the war being over soon? Not on betting markets:

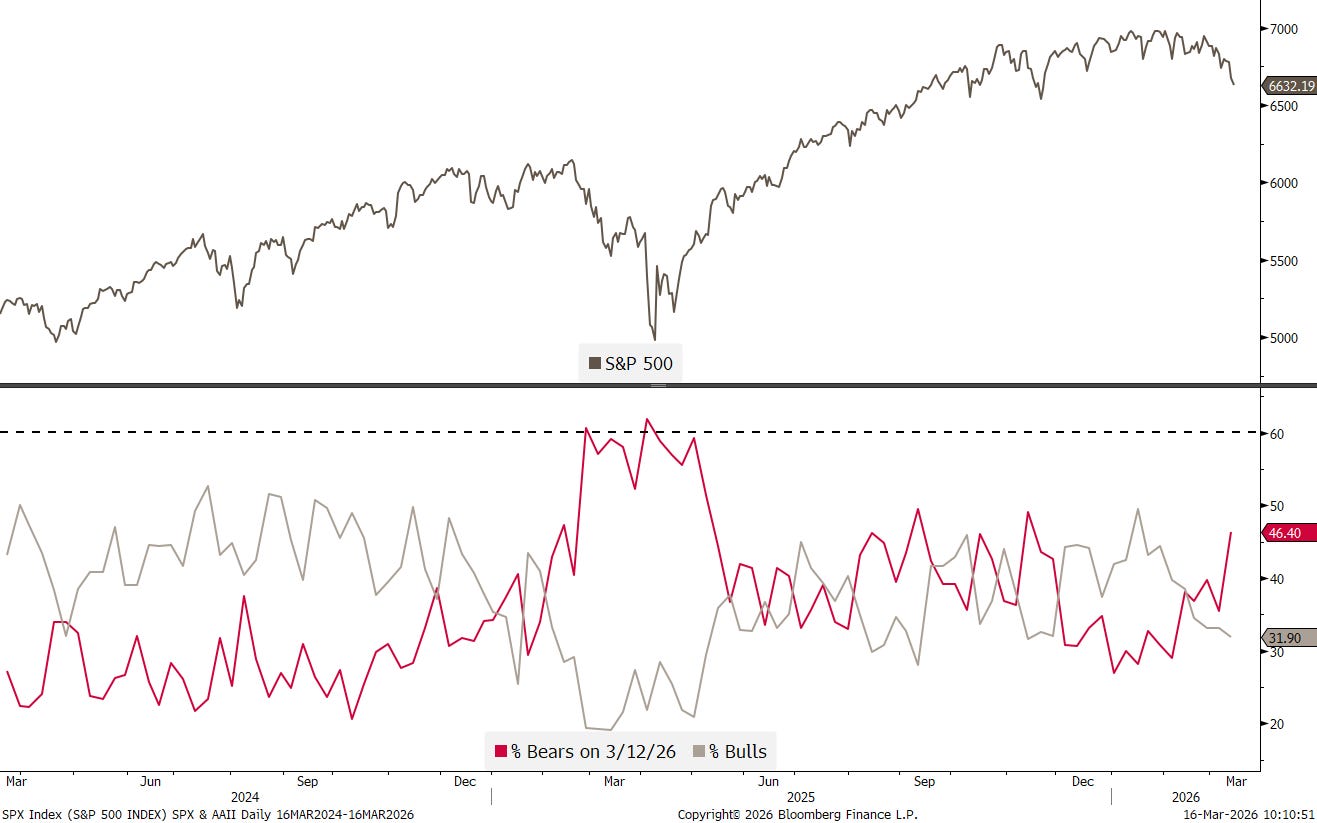

The ‘mood’ amongst investors has turned sour, with the AAII bears hitting nearly 50%,

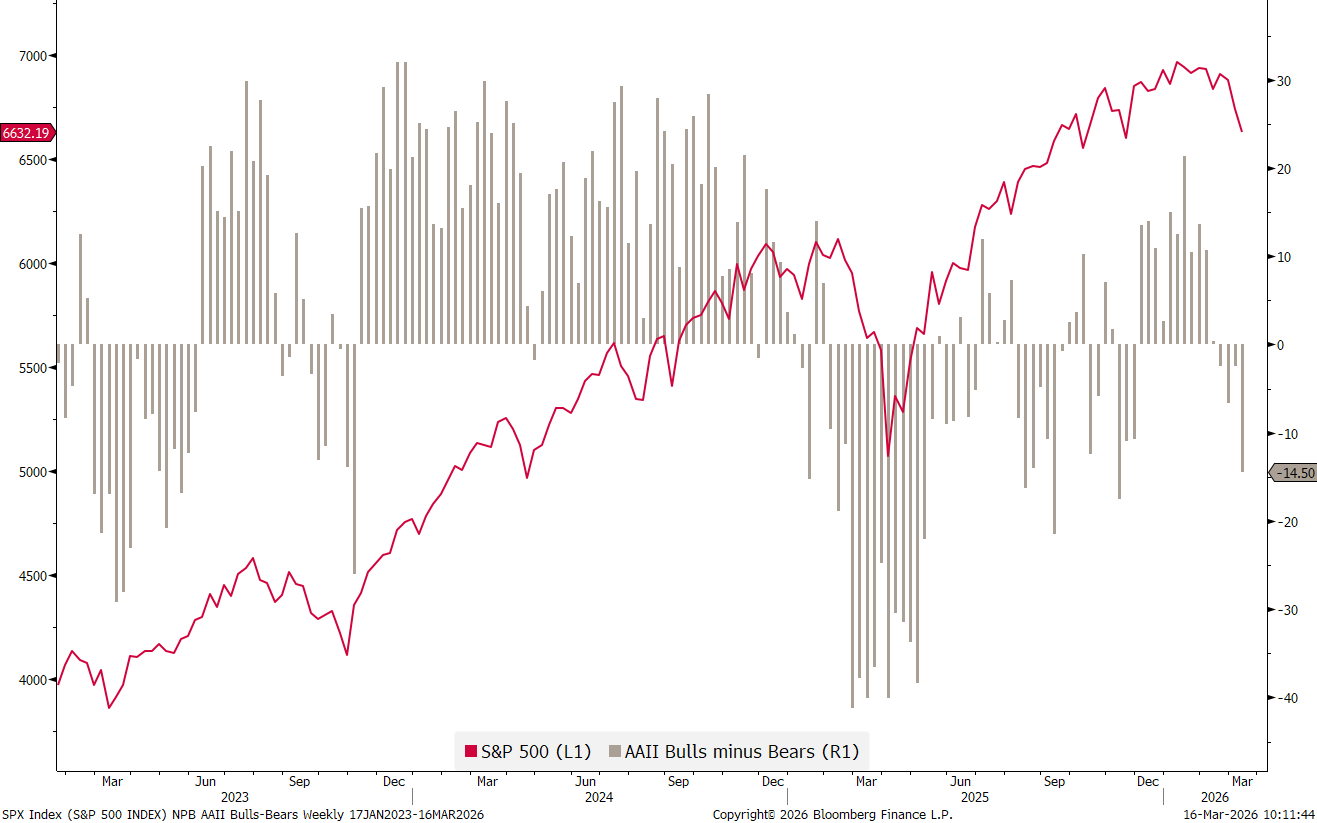

and the bull/bear ratio hitting its lowest level since November last year:

At less than four percent, the drawdown in the S&P 500 since the onset of the war has been very benign, and it could be argued the nearly six-month old 6,600-7,000 range is still intact:

Though we need to watch that supporting 6,600 200-day moving average line over the next few sessions. A break would definitely not be constructive.

Similarly, the Nasdaq, down even only two percent over the past two weeks, is also hovering just above its 200-day moving average:

The more energy-price sensitive European market (SXXP) is down well over six percent over the past two weeks, but ALSO still trades above its 200-day moving average:

Germany’s (a Eurozone country with the arguably worst energy strategies …ever!) stock market, is trading well below its 200-day moving average, but just above key support:

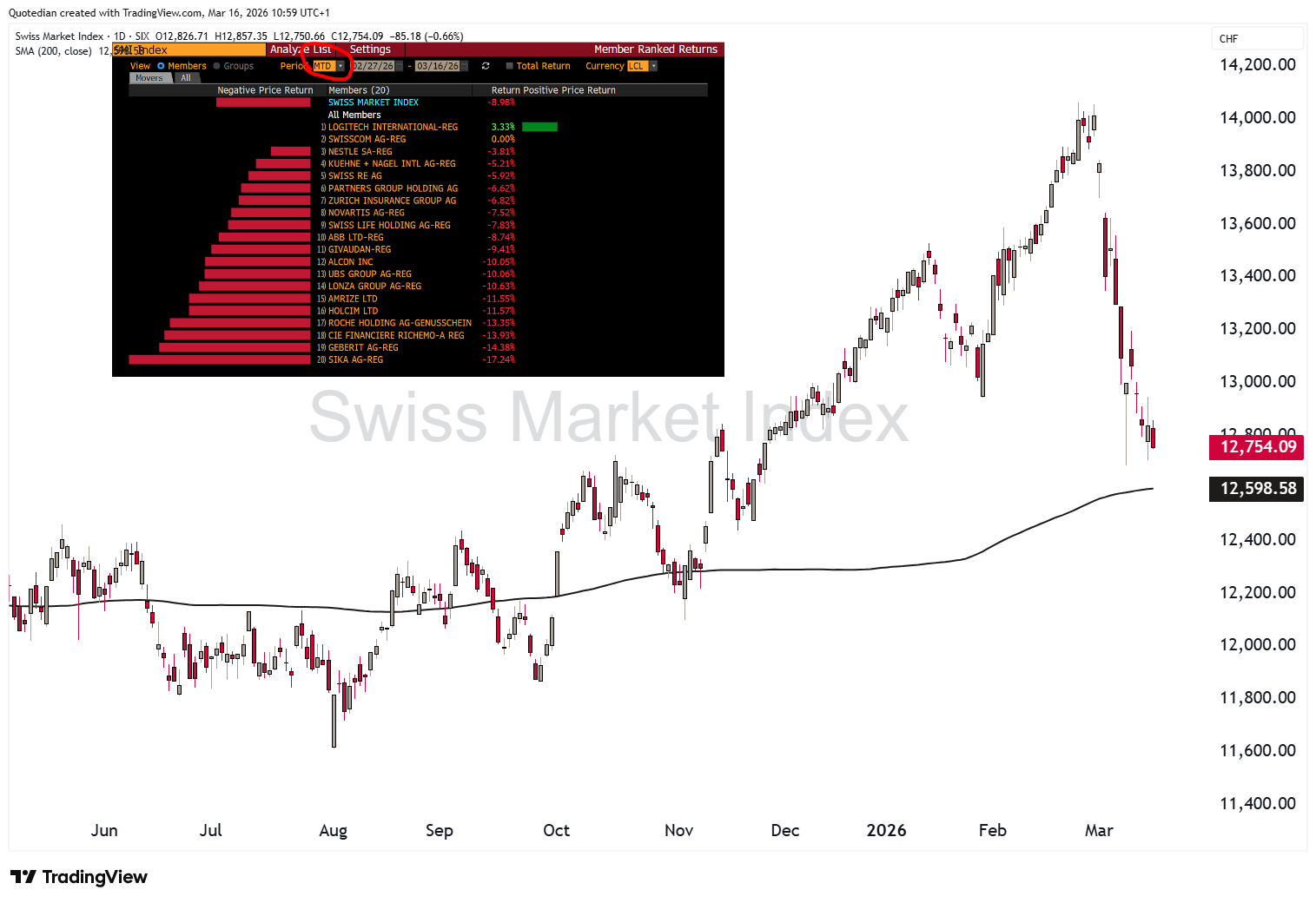

Switzerland’s SMI, usually a bit more of a safe haven thanks to its defensive pharmaceutical and consumer staples stocks, has been hard hit (-9%) since the outset of the war:

Turning to Asia, one of the worst performing markets has been the Indian stock market, with the Nifty 50 down over twelve percent since early February and down eight percent since the outbreak of war in the Middle East:

Not only is the Indian market very exposed to energy prices and the flow of oil through the Strait of Hormuz (SoH), but early sellers have been citing its sensitivity to the roll-out of AI agents (Claude et al.) too.

Our call at the beginning of this year to relatively underweight the Indian equity market within a portfolio’s emerging market exposure continues to look very timely:

Another, supposedly also very oil-price sensitive market, China, has barely budged:

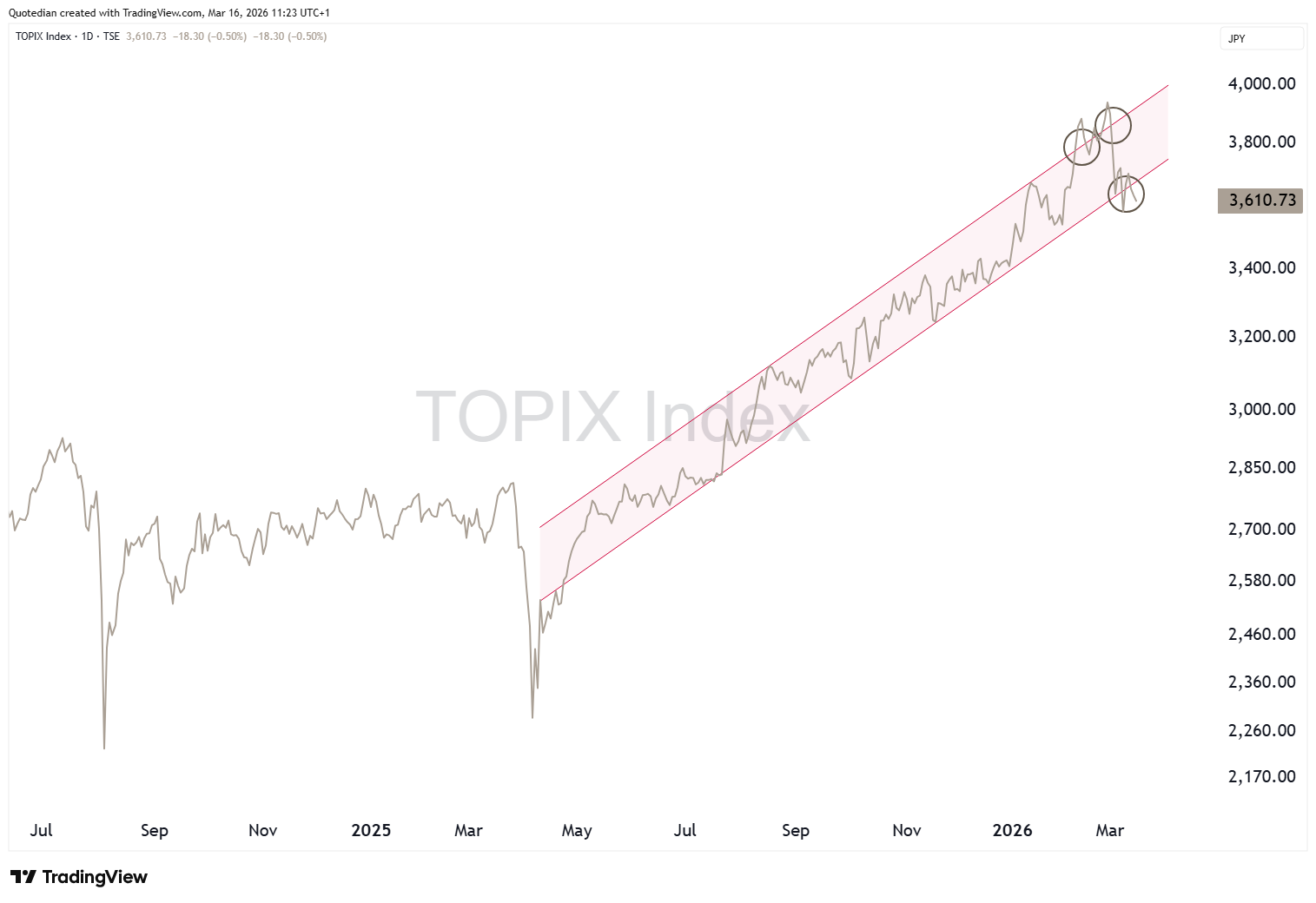

Japan’s TOPIX has corrected, but to the extent what I would call a healthy breather in an ongoing secular uptrend. Here’s the long-term picture:

And here a close-up:

Some Middle Eastern markets have for obvious reasons suffered. Here’s Dubai’s DFM index:

Though Saudi Arabia’s Tadawul Index has been very resilient and is actually slightly higher than at the end of February:

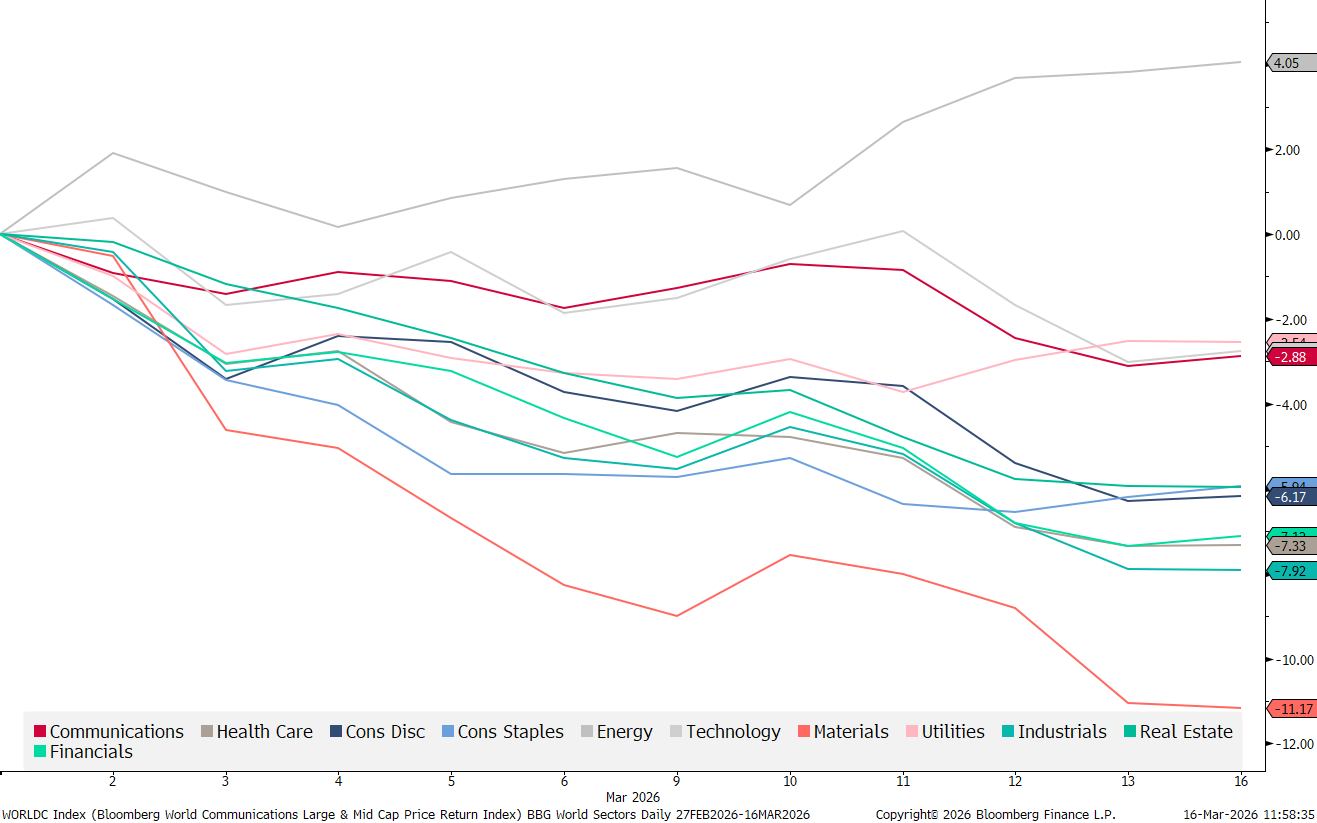

Since the beginning of the month, not surprisingly Energy stocks have seen the best performance in terms of sector comparison, whilst Material stocks have been laggards:

The latter is probably more due to a technical correction in Gold-, Silver- and other mining stocks after a massive rally over the past twelve months, more than a war-induced sell-off:

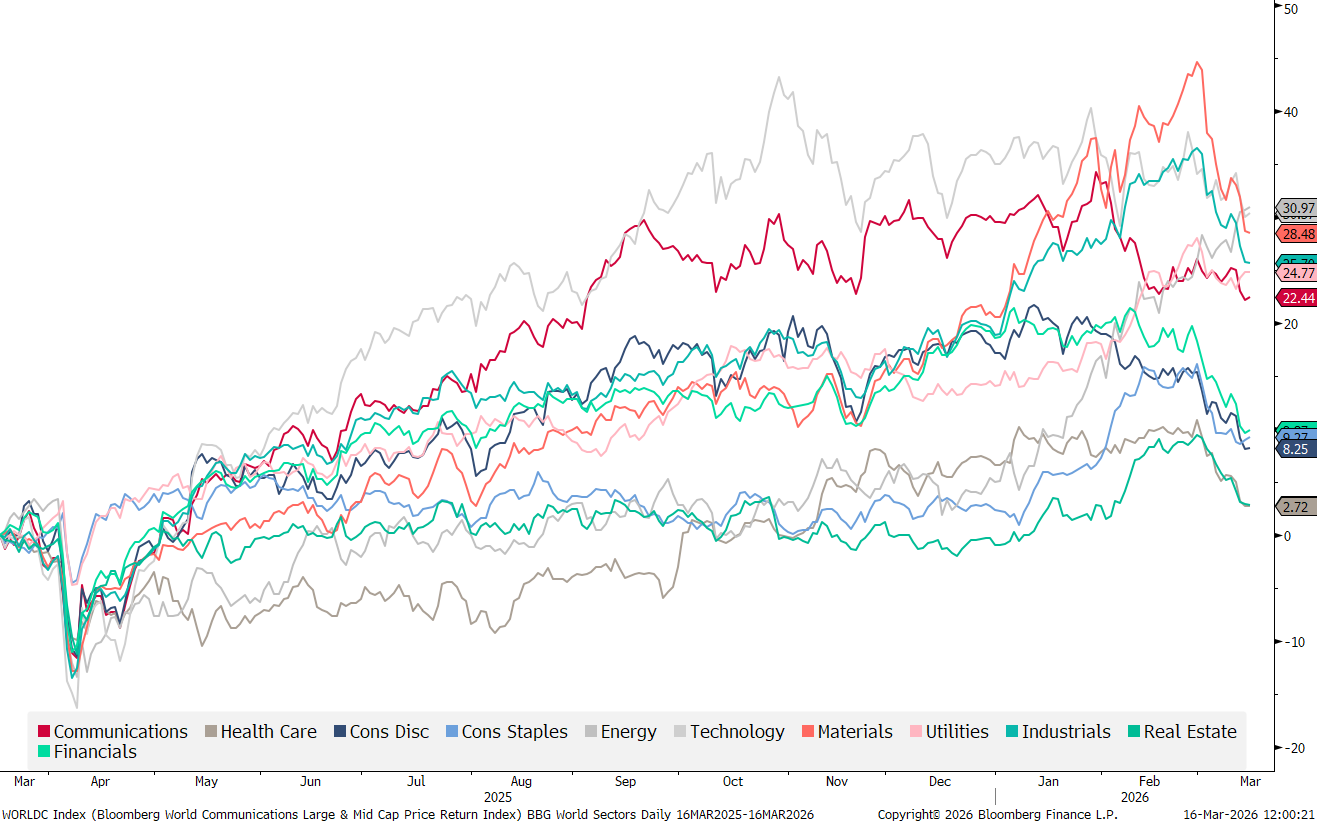

Back in March of 2000, Richard Bernstein, then at Merrill Lynch, had a research report out titled “Attention Venture Capitalists: Leave Silicon Valley for West Texas”. That was a very timely call to rotate out of tech stocks into energy stocks:

Are we there again? With the market cap weight of tech stocks at 32% and that of Energy stocks at less than 4%, that definitely could be an interesting trade…

Ok, so the damage report out of the equity corner reads something like “Down, but not out”.

Let’s turn over to bond markets now, to see how strongly the hull has been impacted.

In theory, (US Treasury) bonds should rally as the ultimate safe haven investment when a war breaks out. In practice, they haven’t:

Looking at the same market (10Y UST) in terms of yield, we saw an initial yield drop (bond market rally), which reversed the same day though, indicating that bond investors are positioning themselves for a stagflationary environment:

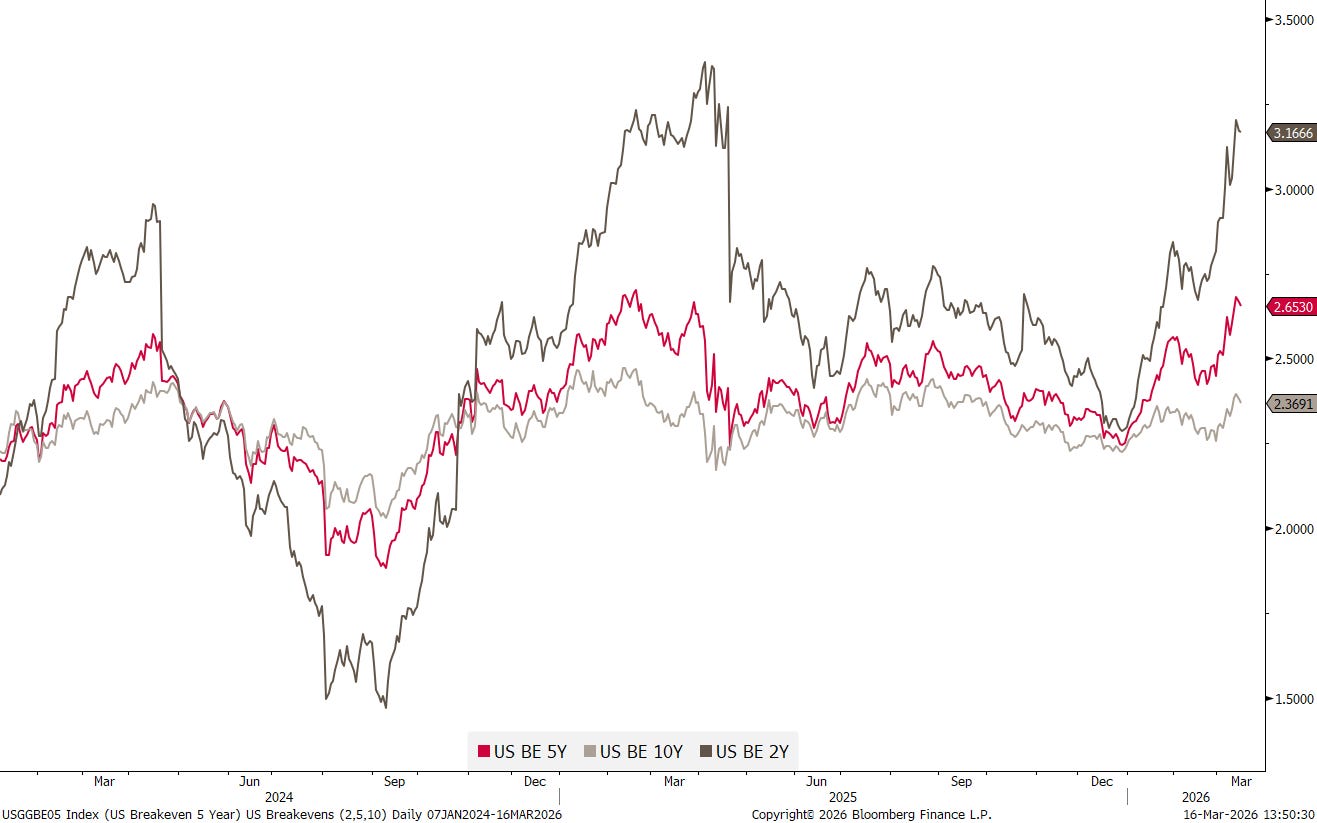

In sync with rising bond yields have inflation expectations (via Breakevens below) also been rising,

and expectations of further FOMC rate cuts vanishing:

Though maybe one cut is not enough, especially if the war drags on and the price shock on the oil/gasoline side continues with black gold trading above USD100. Yes, it is inflationary for prices, but also recessionary for the economy.

The Fed is likely to find itself between a Rock and a Hard Place very soon…

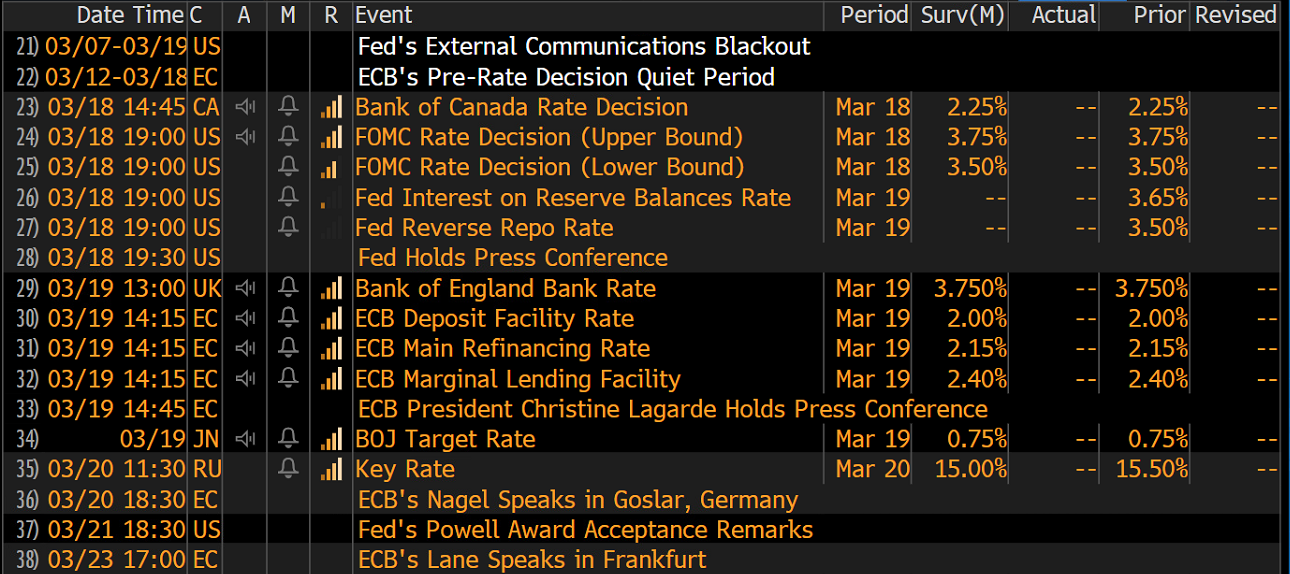

And talking of the US Fed, the FOMC is not the only central bank committee convening this week to discuss rates:

The ECB may also be soon looking at an economy at the brink of a recession.

German 10-year yields nearly touched the 3% landmark last week:

Let’s see what the message from the ECB will be next Thursday …

And by the way, here’s some tin-foil hat conspiracy for the nutters out there … or well-thought-of exit-strategy timing by the Fed's Powell and the ECB's Lagarde

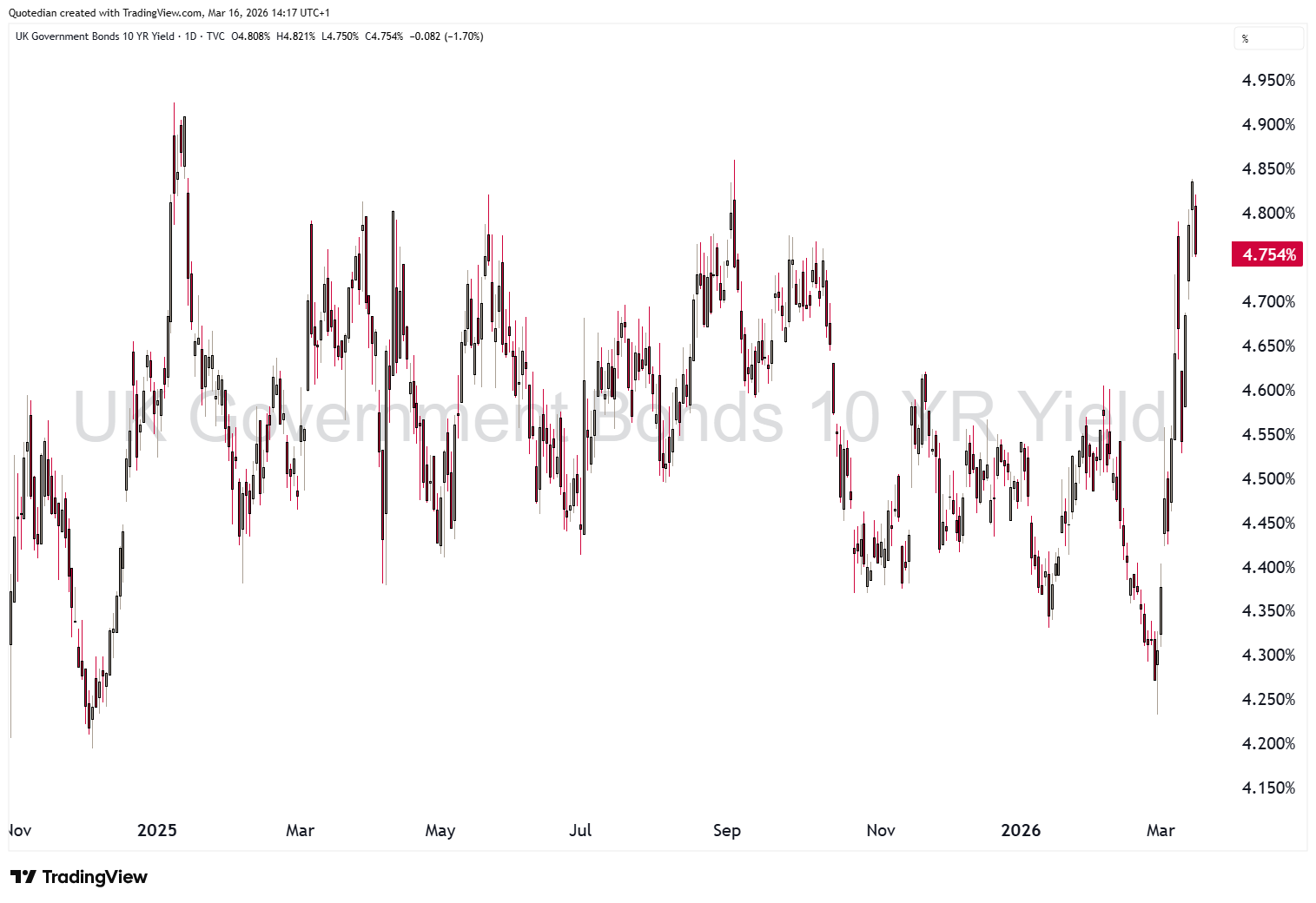

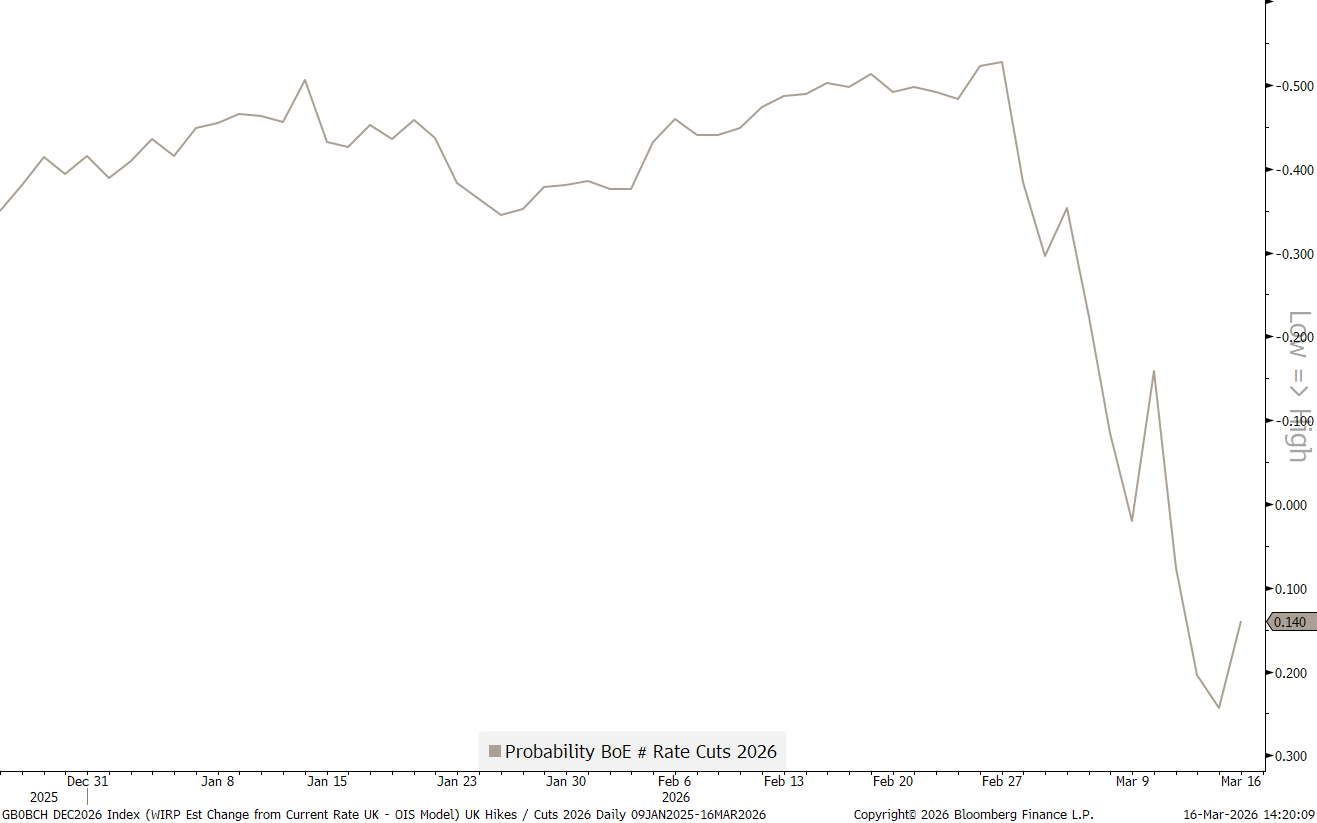

Another bond market seeing its rates going (nearly) through the roof, was the UK Gilt market. At 4.85% it hit a level not seen since September and January of last year:

Here, a rate cut that had been fully baked in for this week,

had to be fully “baked out” again:

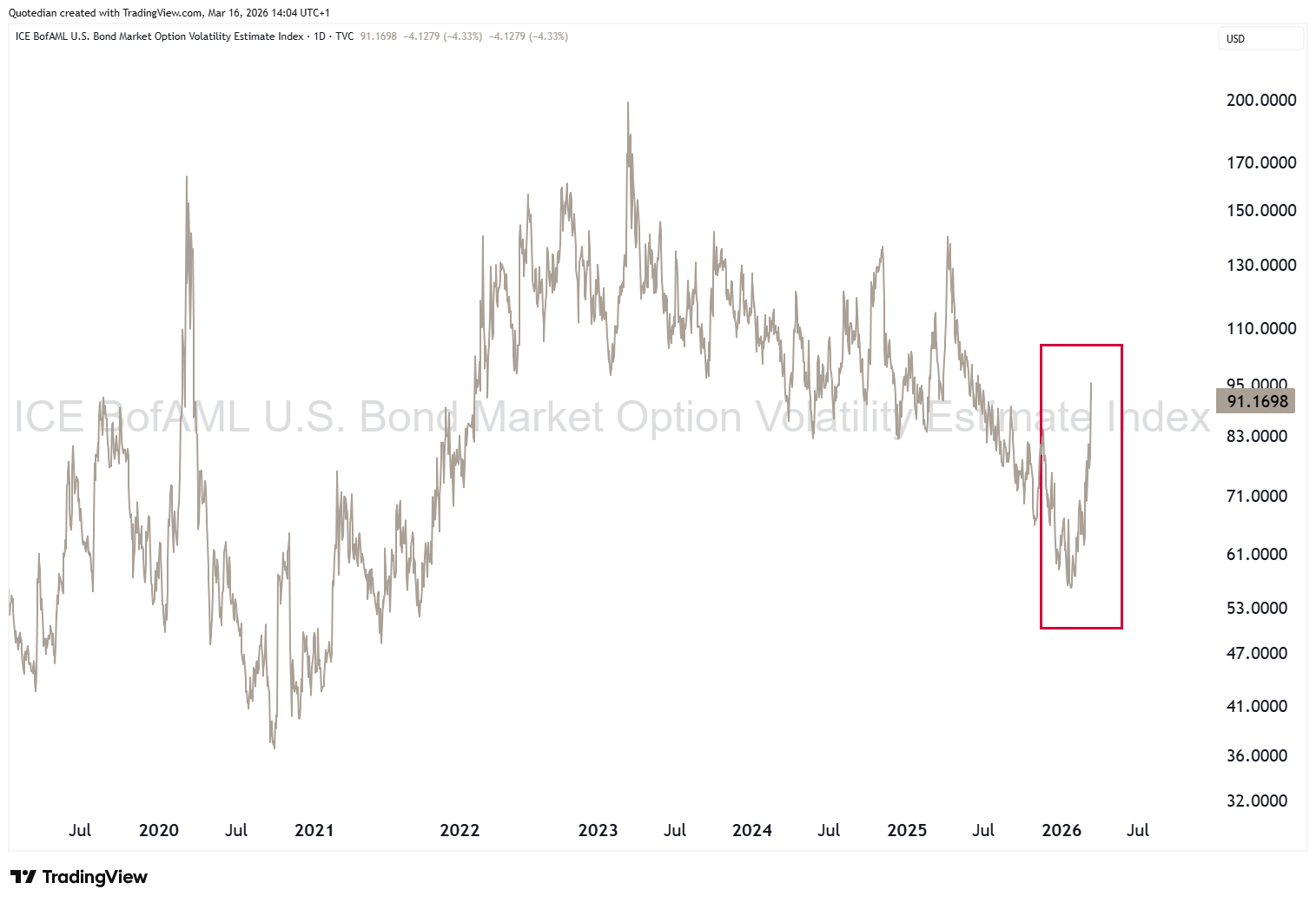

Given all of the above, it is no wonder that bond volatility (below measured via the MOVE index as proxy for Global treasury markets), has seen one of its steepest accelerations since the early COVID days:

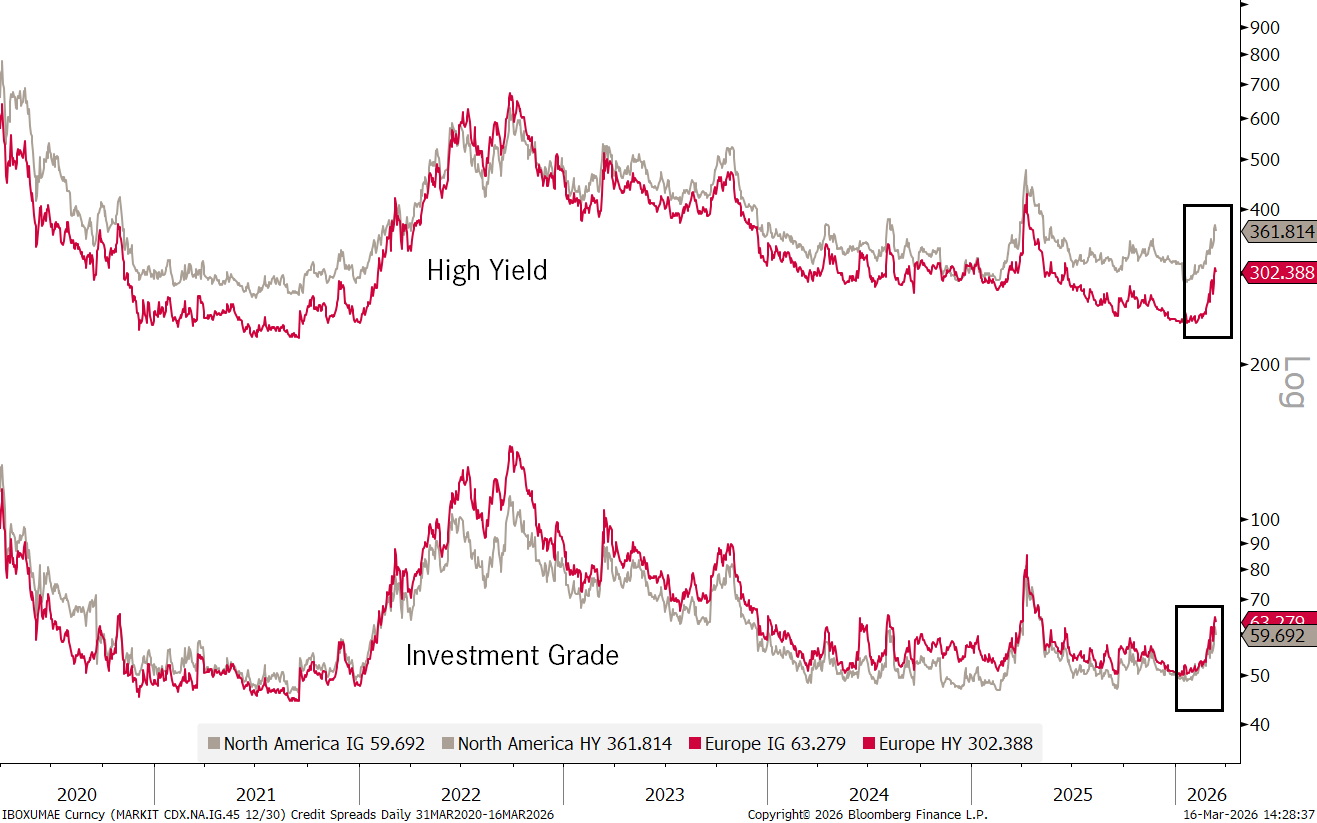

So much excitement in bonds markets and we even haven’t spoken credit risk yet, where the private credit fallout finally seems to be feeding into spreads:

Looking at (US) high yield sectors, we note the largest widening has taken place in technology spreads:

This of course fits well with the “AI is eating the software world”-narrative …

OK, damage control on the bond station is done - quite a few fires are still burning here.

Next up, currency markets!

Since the start of the Israel/US attacks on Iran, the Greenback has strengthened against all other major currencies:

Though the US Dollar Index continues to trade below 100.00 and on Friday was rejected at THE major resistance point:

Similarly, has the Euro bounced off major support just below 1.14:

The USD/JPY cross is back to a level (160) where the BoJ/MoF has intervened (at least verbally) on two occasions already:

Hence, no big disasters in the corridors of the currency wing of our HSS Quotedian …

Last up, health check for the commodity sector!

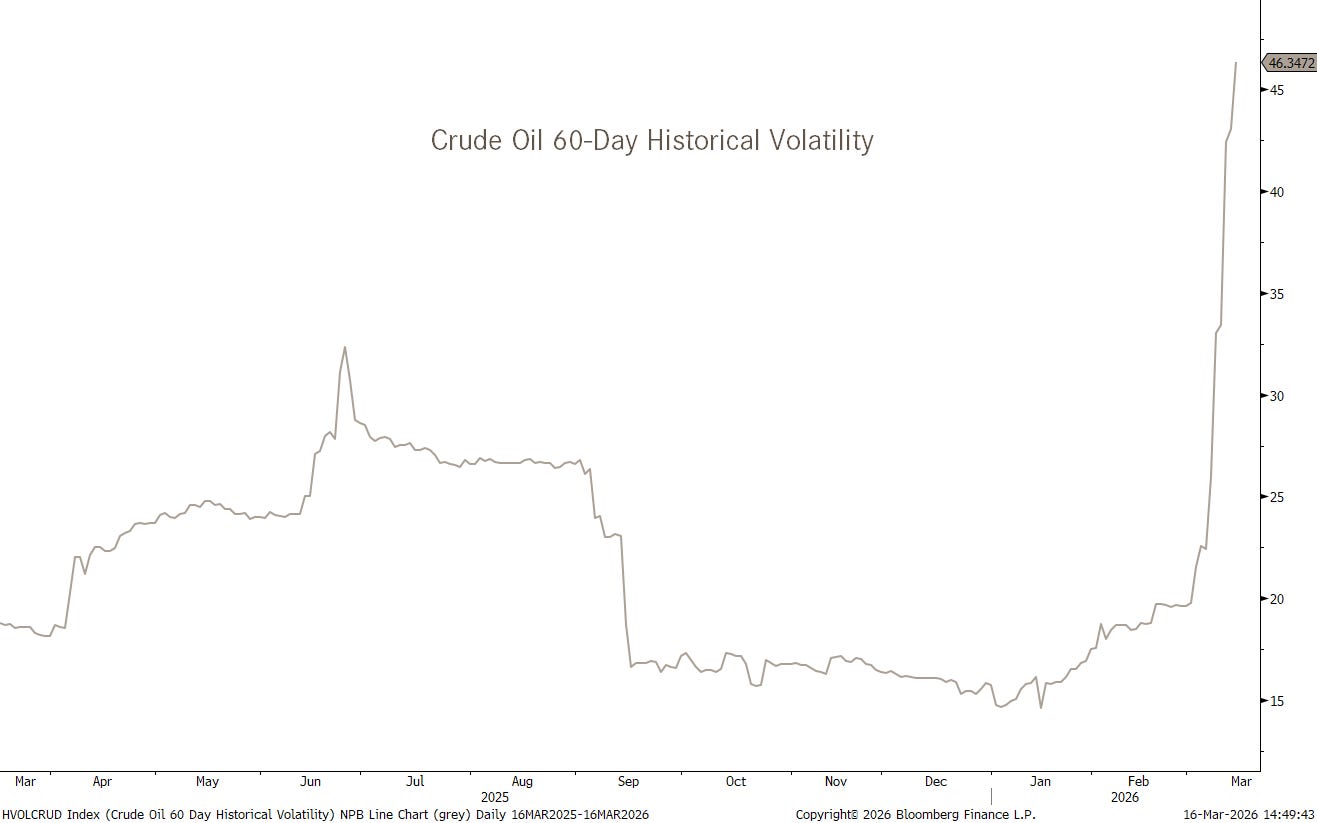

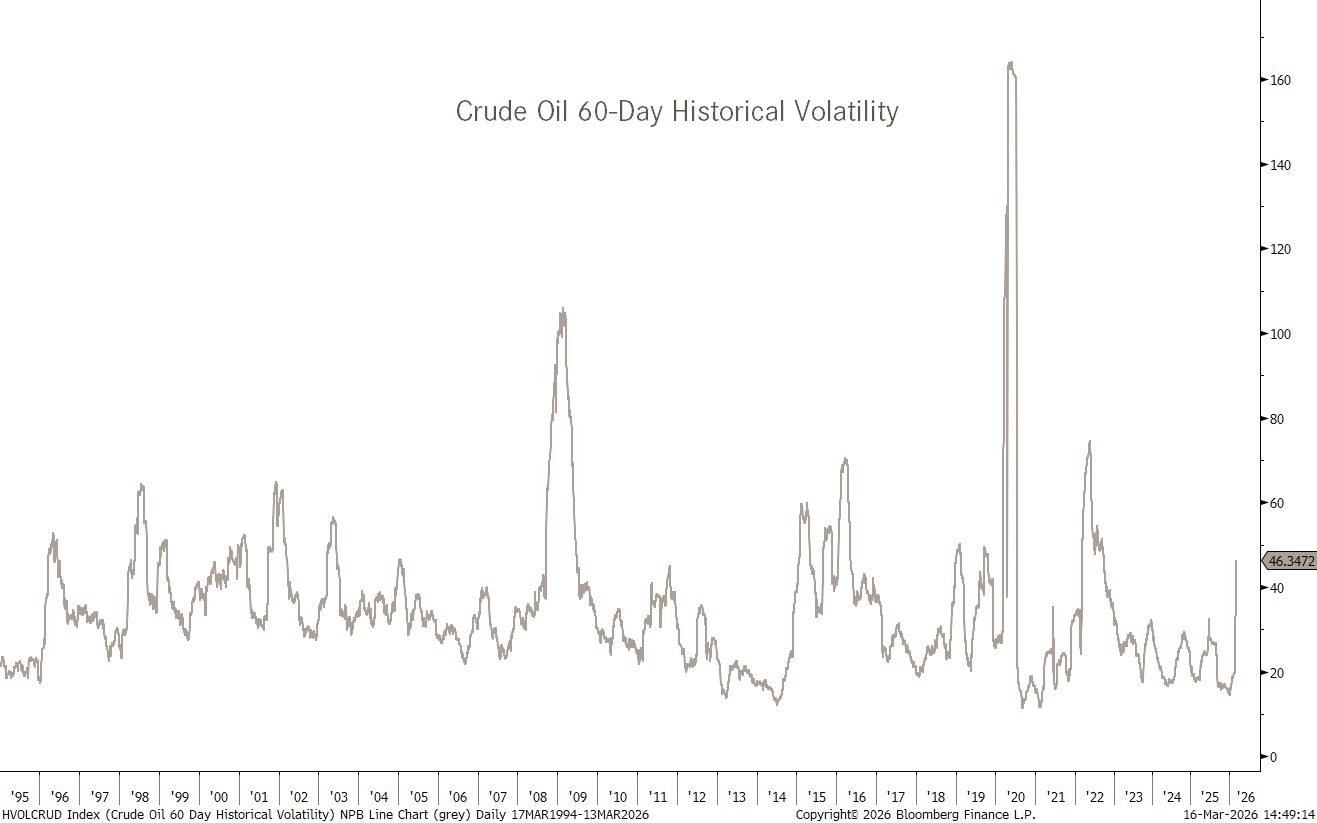

Crude oil volatility has exploded,

but we have seen worse!

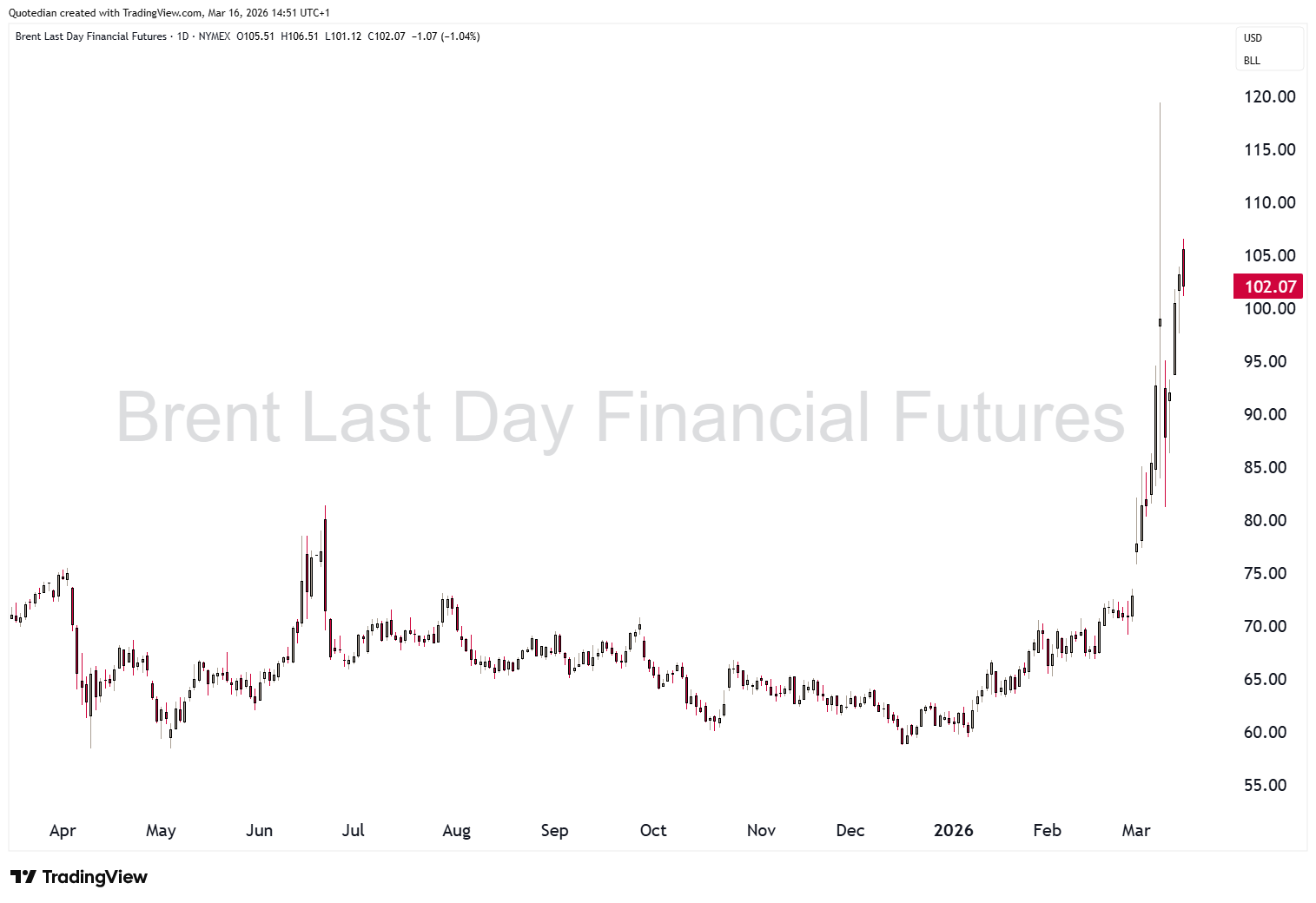

I am pretty sure that Trump & Co’s game plan did NOT foresee the price of a barrel of crude remaining above USD100 for several days:

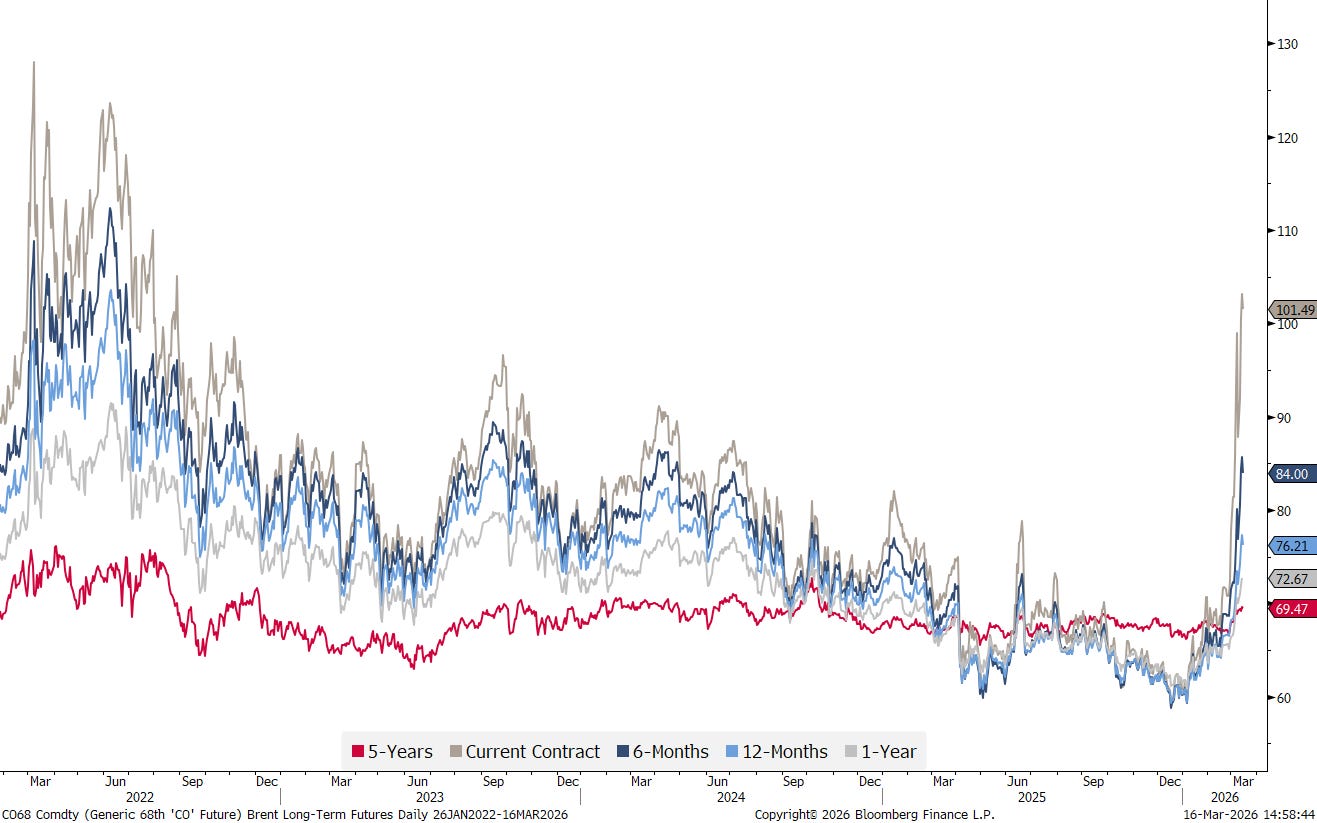

Oil price futures continue to be in strong backwardation (i.e. future prices are lower than near months prices). Is the market too relaxed about the war in the Middle East?

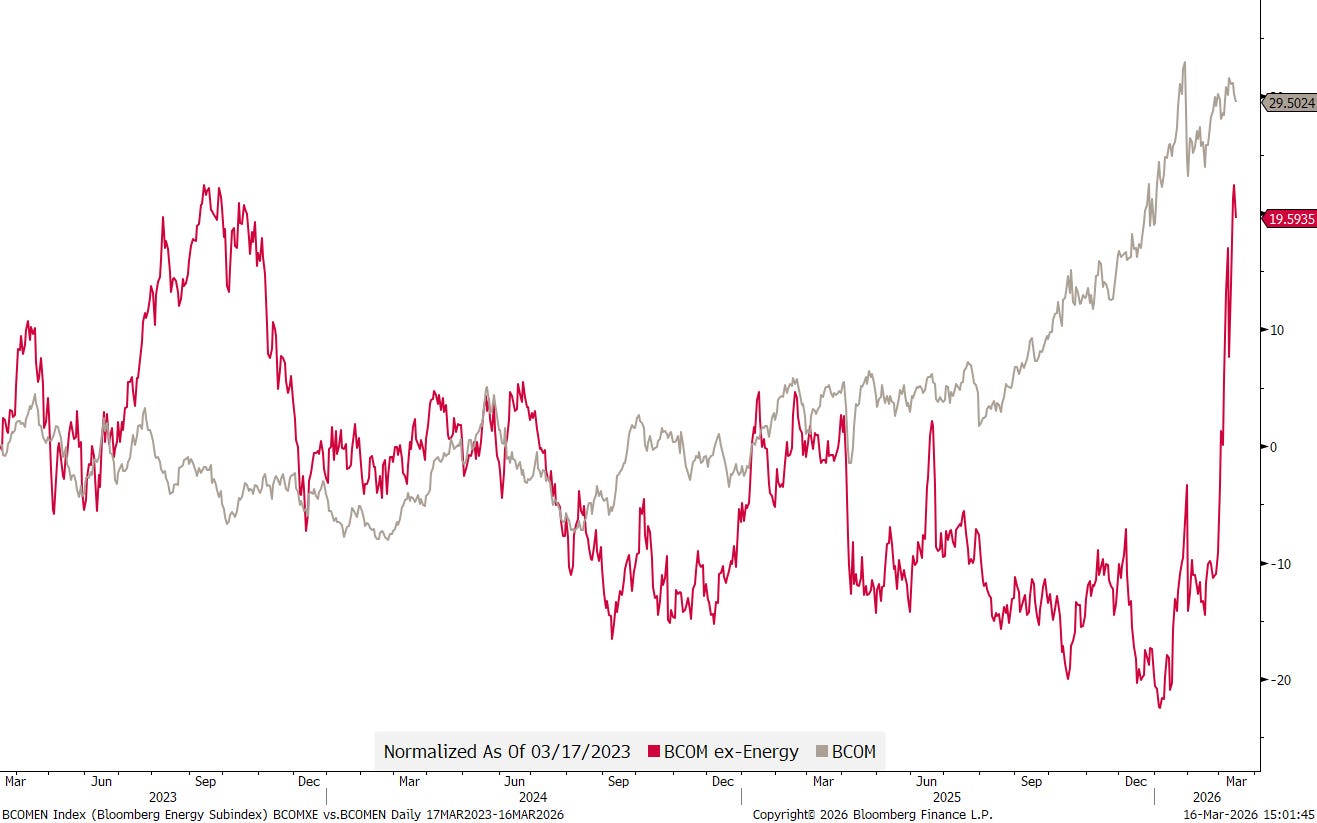

It is ‘funny’ to observe that in the past we said the oil price is usually the last mover in the commodity space, and for reasons we did not know back then, we now suddenly have that last mover joining the rally:

The precious metals space has seen a bit of a profit taking since the onset of the war or as they say: “Never let a good crisis go to waste” (and talk it as an excuse to book profits).

Here’s Gold:

It is also true for Gold that trees do not grow into the sky and hence the price of gold is waiting patiently for its 200-day moving average to catch up.

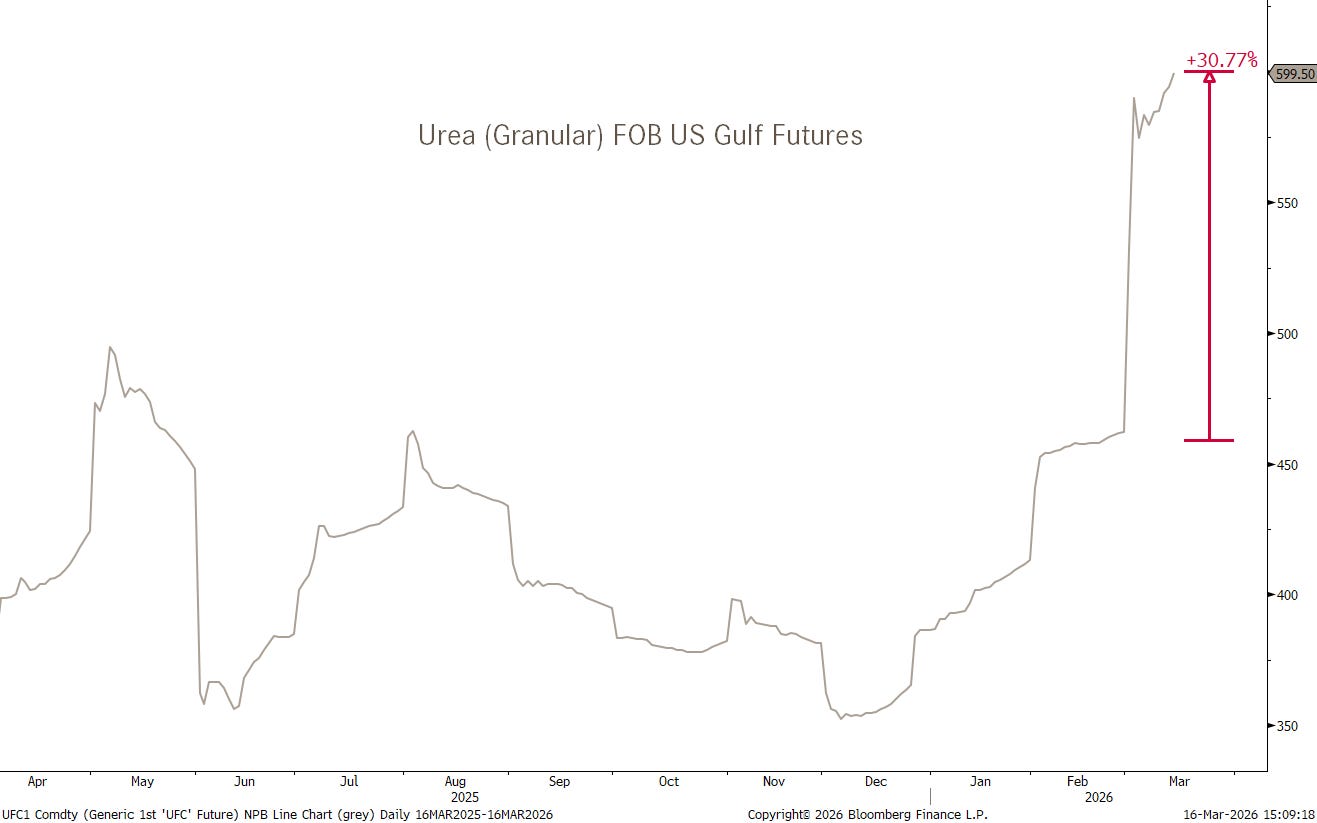

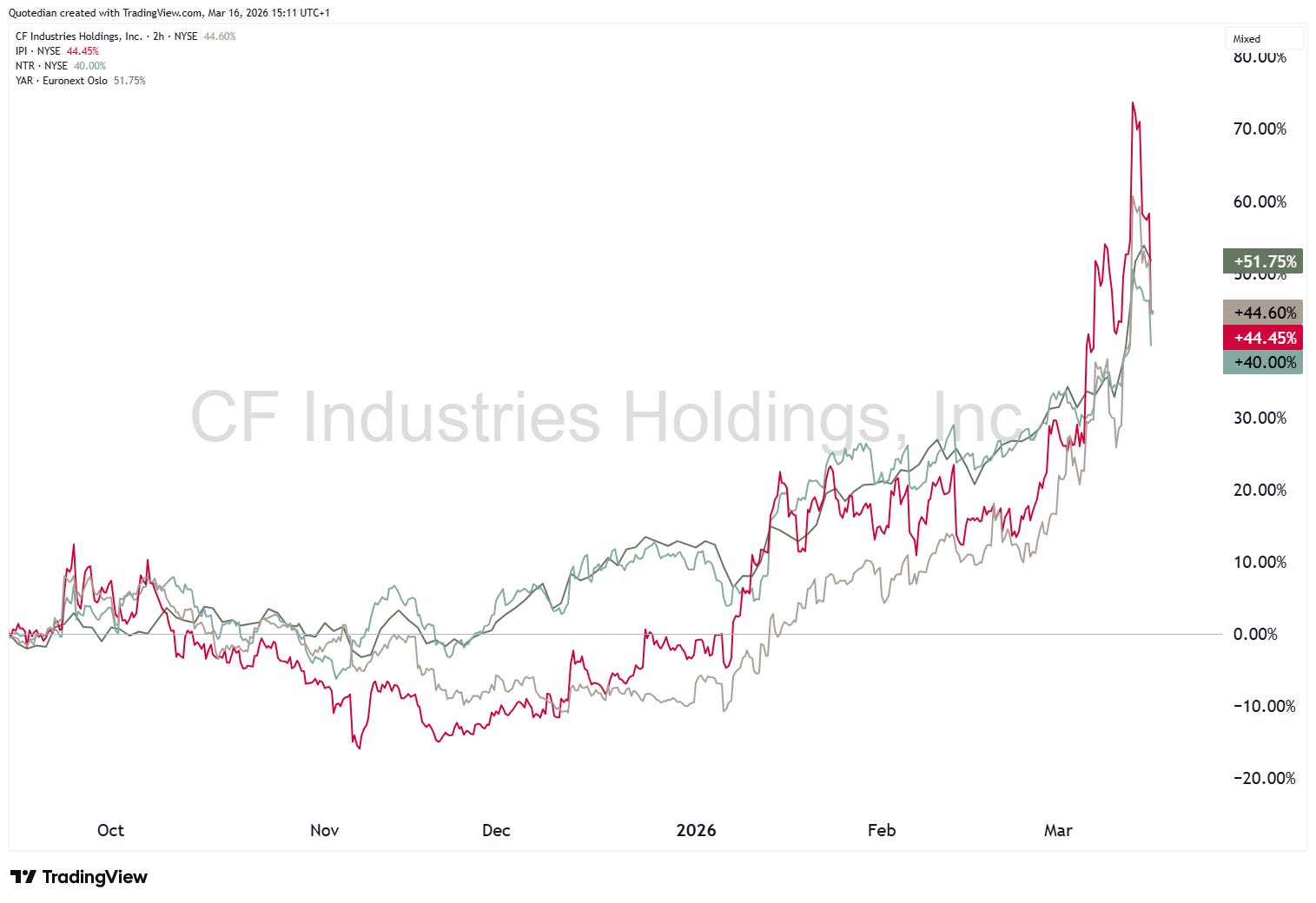

One commodity usually less discussed but currently of utmost importance are fertilizers. Those have been shooting up recently, as energy costs to produce them have shot higher too:

I have written about this last week (click here) and I remain bullish on fertilizer stocks, such as CF Industries (CF), Intrepid Potash (IPI), Nutrien (NTR) and Yara (YAR):

Markets have been shaken across the entire macro landscape, but stand to fight another day, with the damage so far contained. Stocks are trying to shrug off the worries from the war, but may be ignoring the second order effect of global recession, which is partly being expressed in bond yields. Keep a sharp eye on credit spreads for further fallout/contagion from the private credit space. Central bank messages this week will be interesting to observe.

That’s all for this week - May the Trend be with You!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG