Nothing Burger

The Quotedian - Vol VI, Issue 24 | Powered by NPB Neue Privat Bank AG

“The history of markets is one of overreaction in both directions.”

— Peter L. Bernstein

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

A shorter note today on what is a surprisingly busy Friday …

First of all, I missed to give you the results from Wednesday’s poll in yesterday’s Quotedian. Hence, here it is now:

The majority of those who voted (which is the minority of members on this list - shame on you), continue to be bearish.

This serves as a perfect segue into today’s Blitz market review, as yesterday’s session was clearly a small win for the bears.

The good old Quotedian, now powered by Neue Privat Bank AG

NPB Neue Privat Bank AG is a reliable partner for all aspects of asset management and investment advice, be it in our dealings with discerning private clients, independent asset managers or institutional investors.

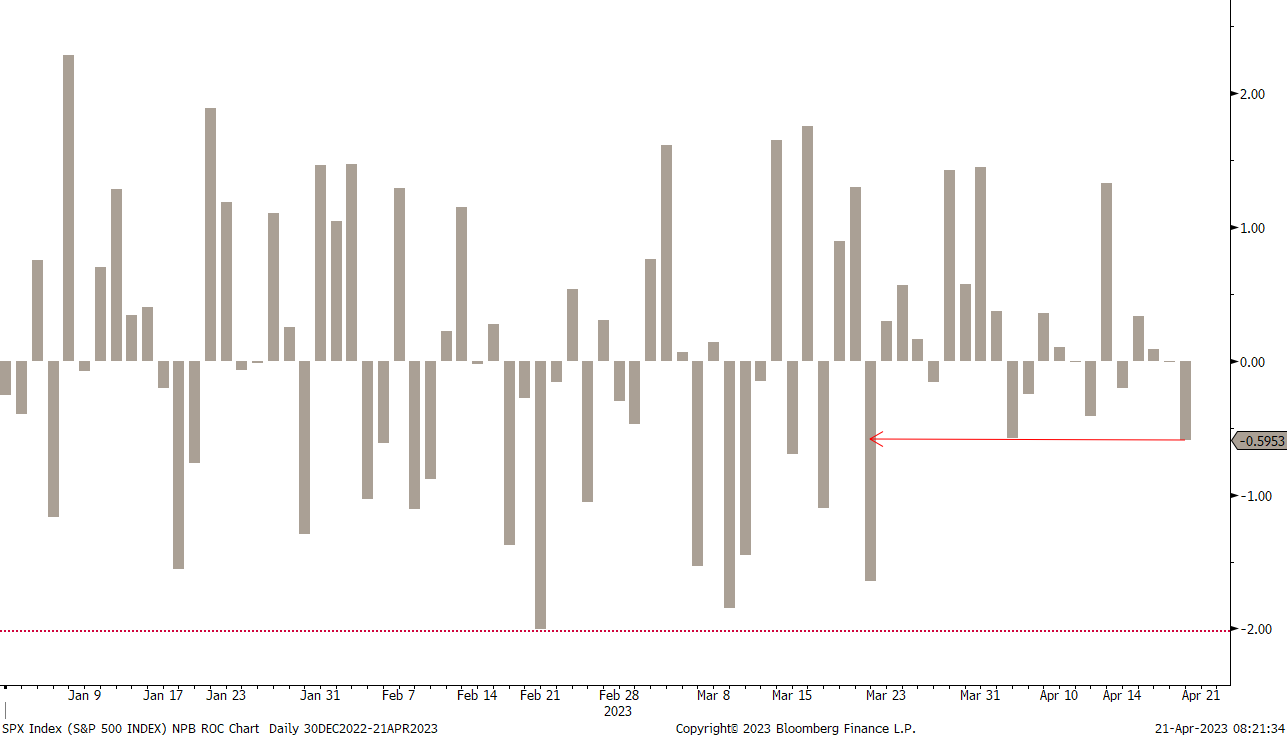

Whilst the S&P dropped less than 1% it was still the biggest drop in about a month:

And under the hood breadth was also pretty weak, with two stocks falling for every stock up and only one sector out of eleven showing a positive daily return:

Going even more granular, some stocks took a big one day hit, with opinion-splitter Tesla leading to the downside with an ten percent drop after their earnings release:

Of course, this was not the only thing that blew up in Elon Musk’s face yesterday:

But TSLA was not alone, as AT&T and Seagate Technologies (STX) dropped by about to the same extent.

Asian equity markets are then taking a similarly prudent approach this morning, with most regional indices retreating somewhere between a half and one and a half percent.

European index futures indicate a flattish opening of cash markets at 09:00 CET.

Turning to fixed income, bond yields softened across the board, maybe on the back higher than expected initial jobless AND continuing claims. We will remember that employment is the last inflationary bastion remaining. Whilst most of the yield curve saw a small softening, there was quite a dramatic collapse at the very short end (1M T-Bills):

That’s a 36 bp drop on the day (and ‘only’ 36bp because it recovered into the close), but actually it is down from close to 5% at the beginning of the month to 3.50ish currently.

Not sure this chart is worth anything, but interestingly enough the 10y-1m yield curve (bottom clip) is now positively sloping again, which is not the case for the 10y-3m:

Nothing to report back from the currency front, except if you consider cryptos as currencies, in which case Bitcoin has given back all of its gains since early April:

On the commodity side of matter, it is worth highlighting that black gold is about to close its OPEC surprise-gap window, surely disappointing many oil bulls:

That’s all for today -time to hit the send button!

Have a great weekend!

André

CHART OF THE DAY

The chart below shows the price ‘action’ of the NASDAQ since late March. Or maybe we should replace the word action with chomp, for this big, fat nothing burger:

Thanks for reading The Quotedian! Subscribe for free to receive new posts the moment they are published.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance