One currency to rule them all

The Quotedian - Vol V, Issue 97

“The USD is our currency but your problem”

— John Connolly, Secretary of State, 1971

Get your daily market deliberations delivered directly to your inbox. Subscribe to The Quotedian here:

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

As today’s title and QOTD suggest, it was the currency market tail that waged the market dog yesterday, with the cleanest dirty shirt, the US Dollar, dominating the macro landscape. We get back to currency markets further down, but it was that in combination with some profit-taking after last week’s strong performance that sent equity markets lower in yesterday’s session.

The S&P closed down around one per cent, with about three stocks down for every stock up and only one (Utilities) out of the eleven economic sectors ending up on the day:

However, one little ray of hope for equity bulls was to be found in the volume (turnover) numbers, which saw one of its lowest readings since the current market ‘rally’ started in mid-June.

The corporate news landscape was dominated by the ensuing battle between Twitter (-11.3%) and Elon Musk, a downgrade by a popular analyst of Meta (-4.7%), whilst in Europe the drama around German utility company Uniper (-14.4%) continues to unfold.

This morning Asian equity markets are largely a see of red and Western equity index futures are also pointing to a lower opening of cash markets later today.

In bond markets, Treasuries and German government bonds both saw some safe-haven buying on the back of weaker equity markets, pushing yields lower from their Friday highs. The US 10-year yield dropped below the three per cent handle again, but remains within our defined range (see chart), on which we swore the oath :-) to only take an aggressive duration bet if violated on either side:

Credit spreads continue to trade wide meanwhile, continuing to fail confirming the equity rally of past weeks. Though admittedly, they seem to have largely at least paused the widening process:

Which brings us back to currency market, where the Euro was 5 pibs away from hitting parity a few moments ago:

Of course, we readers of The Quotedian, have been talking about this happening for weeks now (or at least since the German trade deficit showed a negative reading for the first time since 1991 early this month). Of course is this old news now and the focus should be on how much lower it can go. But that will be an analysis for tomorrow or Thursday - as an immediate measure, I will close our EUR dislike (aka short) position as we hit parity throughout the day today.

The other currency pair momentarily under close scrutinity is of course the USD/JPY, where the Bank of Japan’s continued insistence on a 0.25% ceiling on the 10-year JGB is creating havoc for the Yen. This morning, the country’s PPI (9.2%) in Japan came in above expectations AND the previous month’s reading, which should only put further pressure on the currency. 140, here we come? Here’s a longer-term chart of the currency pair:

The “best” argument against a further raising greenback is positioning, which is becoming somewhat extreme among speculators (lower clip, blue line) and could lead to a painful (temporary?) unwind at some stage:

And finally, moving into the commodity complex, we observe a lot of red flashing also this morning, with the correction dominated by the recession-sensitive energy and industrial metals sub-categories:

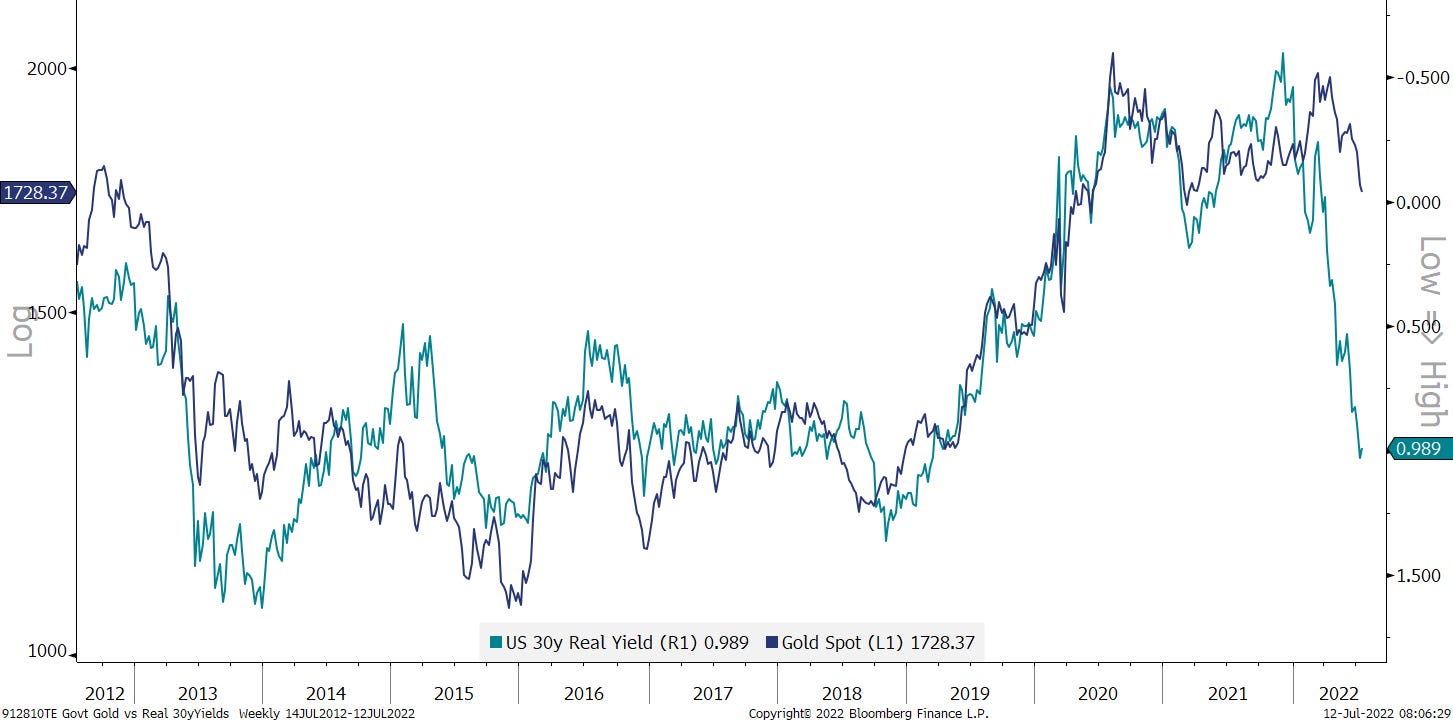

Gold still seems at interesting accumulation levels, though it seems a lot of patience will be needed for the upside to eventually develop:

Also, don’t miss today’s COTD in order to curb your gold enthusiasm…

Ok, time to hit the send button. There is little on the economic agenda today and Pepsico kind of kicks off earning season, being the first large US company reporting their quarterly results at noon (CET) today.

CHART OF THE DAY

Even though there is a bit of chart crime going on below (two different y-axes), the correlation between real yields (inverted) and Gold are undeniable. This would suggest that our accumulation idea may be somewhat premature still. Stay tuned..

LIKES N’ UNLIKES

Likes and Dislikes are not investment recommendations!

Long China equity (FXI) / short India equity (PIN)

Biotech (XBI); trailing stop now at $66

Energy stocks (XLE); 1/2 usual position size

Long some Gold (direct or via short puts)

Euro(closing position below parity)

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance