Oxymoron

The Quotedian - Vol VI, Issue 25 | Powered by NPB Neue Privat Bank AG

“I am a deeply superficial person.”

— Andy Warhol

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

I just love that word: “OXYMORON”. Don’t you too? So many cool oxymoron examples are to be had:

accurate estimate

alone together

awfully good

grow smaller

or even … jumbo shrimp!

Some people are walking oxymorons, but let’s not go there …

And then sometimes we see oxymorons in financial markets, though some people prefer to call them conundrums. But we’ll stick with oxymoron and one such “oxymoron” can be found in financial markets as I type.

The chatter regarding the US debt ceiling (hhhmmm, ‘debt ceiling’ is that a oxymoron too in the case of the US?) is increasing and some parts of the market are starting to show some nervousness.

Here are the 1- and 5-year Credit Default Swap (CDS) rates for the US for example:

It is still relatively cheap to ensure, but in case of the 1-year CDS it has reached about double the level of previously stressful periods!

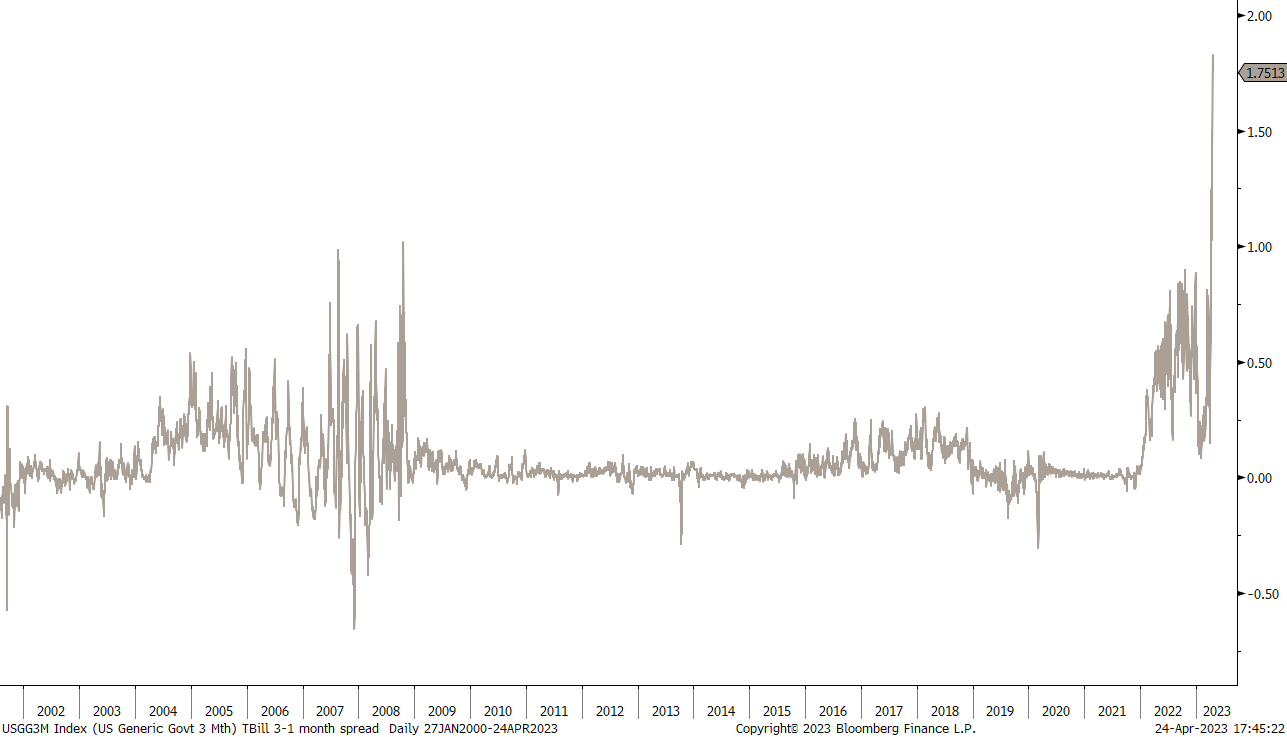

Or look at the spread between three- and one-month treasury bills blowing out:

Obviously, some investors are getting very nervous regarding a possible stalemate in negotiations regarding the debt ceiling between the donkey and the elephants.

And then there are equity investors…. here’s the VIX:

Complete absence of even the slightest level of fear, with the VIX at a close to a 2-year low.

Now let me put that oxymoron together into one chart for you:

Maybe equity investors have come to the conclusion that stocks will go up as bond investors flee treasury bills in case of an increased possibility of a default? Maybe an S&P 500 earnings yield of 4.97% is the new risk free rate?

Maybe …

And off we go with our usual review of Monday’s session …

The good old Quotedian, now powered by Neue Privat Bank AG

NPB Neue Privat Bank AG is a reliable partner for all aspects of asset management and investment advice, be it in our dealings with discerning private clients, independent asset managers or institutional investors.

Starting with equities, it was yet again an extremely quiet session, where investors do not seem to give a monkey’s about earnings, debt ceiling and other worries, but rather exhibit a certain level of FOMO on a possible rally as the Fed will hike 25 bp next week and then announce they are finished hiking … oh well, good luck with that.

With the S&P 500 close to unchanged on the day, six out of eleven sectors ended higher and the advance-to-decline ratio was 3:2, leaving us with the following non-descriptive heatmap:

Over the coming two weeks, close to 350 companies out of the 500 in the S&P are reporting their earnings, which is equal to about 67% of market cap. An especially strong focus will be on the big tech names, as they have done most of the lifting in the current rally. For proof, here’s the S&P 500 market-cap weight index versus the equal-weight version:

In corporate news, maybe to mention that LVMH hit the $500 billion market cap level yesterday,

IMHO, the first European company to do so (any objections?).

Also, Bed Bath & Beyond (finally) went into chapter eleven:

And shares of regional lender First Republic Bank dropped initially 22% after-hours, as the bank reported a $72 billion drop in deposits during Q1.

Little happening on the fixed-income front, where the Fed has (thankfully!) moved into their quiet-period ahead of next week’s FOMC meeting.

A move above 50 in last week’s S&P Global US Manufacturing PMI failed to worry market on a continuingly hawkish Fed:

10-year rates dropped off a little over the past few sessions,

Little to report back from FX and Commodity markets, which is good as time has come to hit the send button.

More tomorrow, take care.

André

CHART OF THE DAY

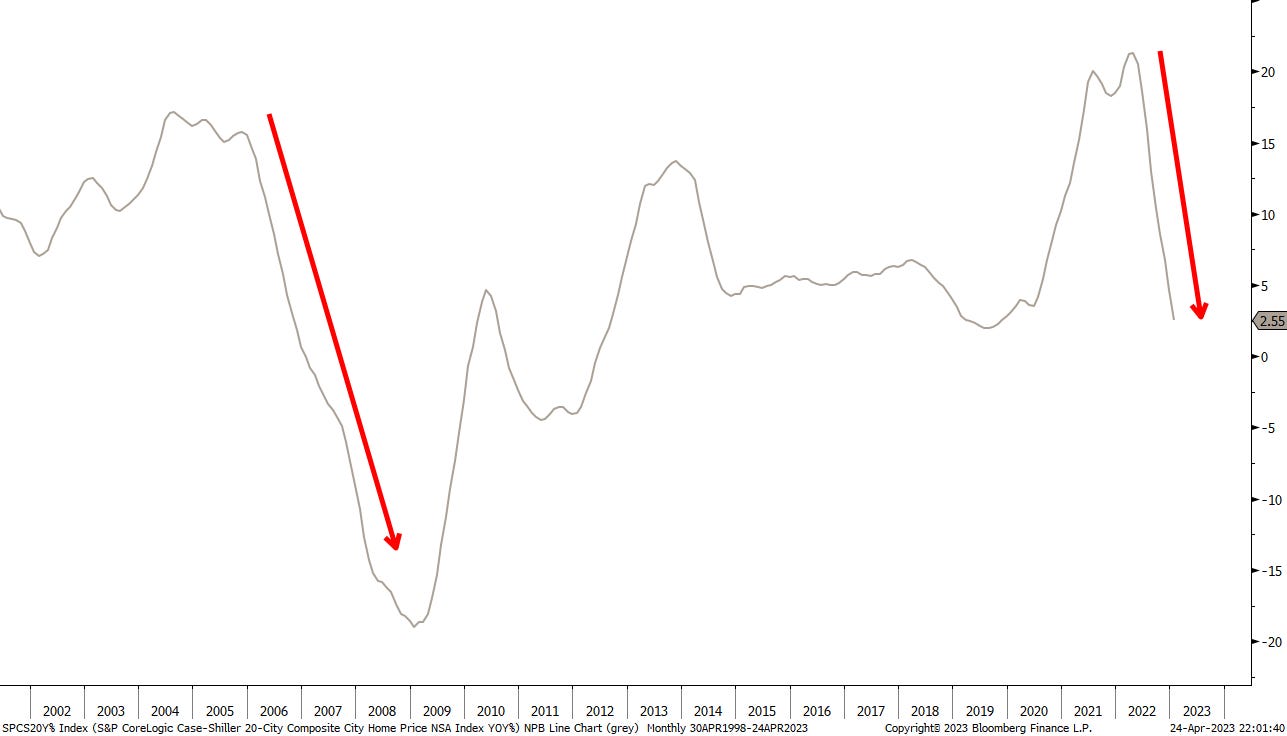

We started today’s missive talking about oxymorons. Here’s another example of opposing contradictions (is that a double-negative?).

House prices in the US have seen their biggest retreat since the GFC some 15 years ago as measured by the S&P CoreLogic Case-Shiller 20-City Composite City Home Price Index (what a mouthful):

So, what does this mean for the share prices of home-building companies?

Correct, closing in on new all-time highs of course!

Stay tuned ...

Thanks for reading The Quotedian! Subscribe for free to receive new posts the moment they are published.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance