Pirate Credit II - My, My, Here We Go Again

Vol IX, Issue 09 | Simplicity is the Ultimate Sophistication

“We don’t have red flags. In point of fact we don’t have yellow flags. We actually have largely green flags.”

— Marc Lipschultz, co-CEO of Blue Owl on an earnings call (Feburar 26)

The second instalment of “Pirate Credit” is being rolled out in financial markets

Equities are range stuck, but all over the place

Invested in Tech? You may have done very well … or not!

Bond yields are still range stuck, but “high noon” is moving closer

Cryptocurrencies are on the verge of breaking down again

The Oil price is slave to Polymarket bets, Gold is ready to move higher again and copper mining stock may be leading physical prices higher

This week’s title and theme should actually have been, well, title and theme of the Quotedian two weeks ago, but impending changes to the newsletter and a tight agenda (in combination also known as: “dog ate my homework”) kept me from publishing the following paragraphs earlier. Though given the size of the potential fall-out, we may be still in the early moments of this particular crisis.

But to get us starting, let me circle you back to today’s quote of the day first and then push you back through the tunnel of time of financial hysteria history:

“We don’t have red flags. In point of fact we don’t have yellow flags. We actually have largely green flags.”

— Marc Lipschultz, co-CEO of Blue Owl on an earnings call (Feburar 26)

Does that not sound awfully a lot like:

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

— Chuck Prince, CEO Citigroup (July 2007)

or

"We don't see any pressure on our liquidity, let alone a liquidity crisis."

Alan Schwartz, CEO of Bear Stearns (March 2008)

or even

"We will get through this."

— Dick Fuld, CEO Lehman Brothers (August 2008)

You get my point.

Five months ago, in early October 2025, I wrote a lengthy piece on what I thought (and still think) has the potential of becoming a crisis with a massive fall-out. Titled, “Pirate Credit”, (click here to read it again) it analysed the (nearly) first warning signs of a crisis befalling the private credit sector.

That October newsletter also carries a very, very, very basic primer (and some links) on private credit, but for a fantastic introduction, explanation and more, I would refer you to the article just published by my friend Cédric Kohler at Seneko, titled “Give me a Pound of Flesh”, which is less gory than you initial think:

Though we are probably still in stage one of the five investment grief stages, evidence is now accelerating. Keeping our “Pirate Credit” style:

Anyway, why am I bringing this all up again?

Well, this was one of the headlines last week:

So, come again: no red and no yellow flags, just green, right??

And here’s where the virtue of that one of very few quotes you actually really need to remember comes in:

“Price leads narrative”

Source: 37-years of hands-on market experience

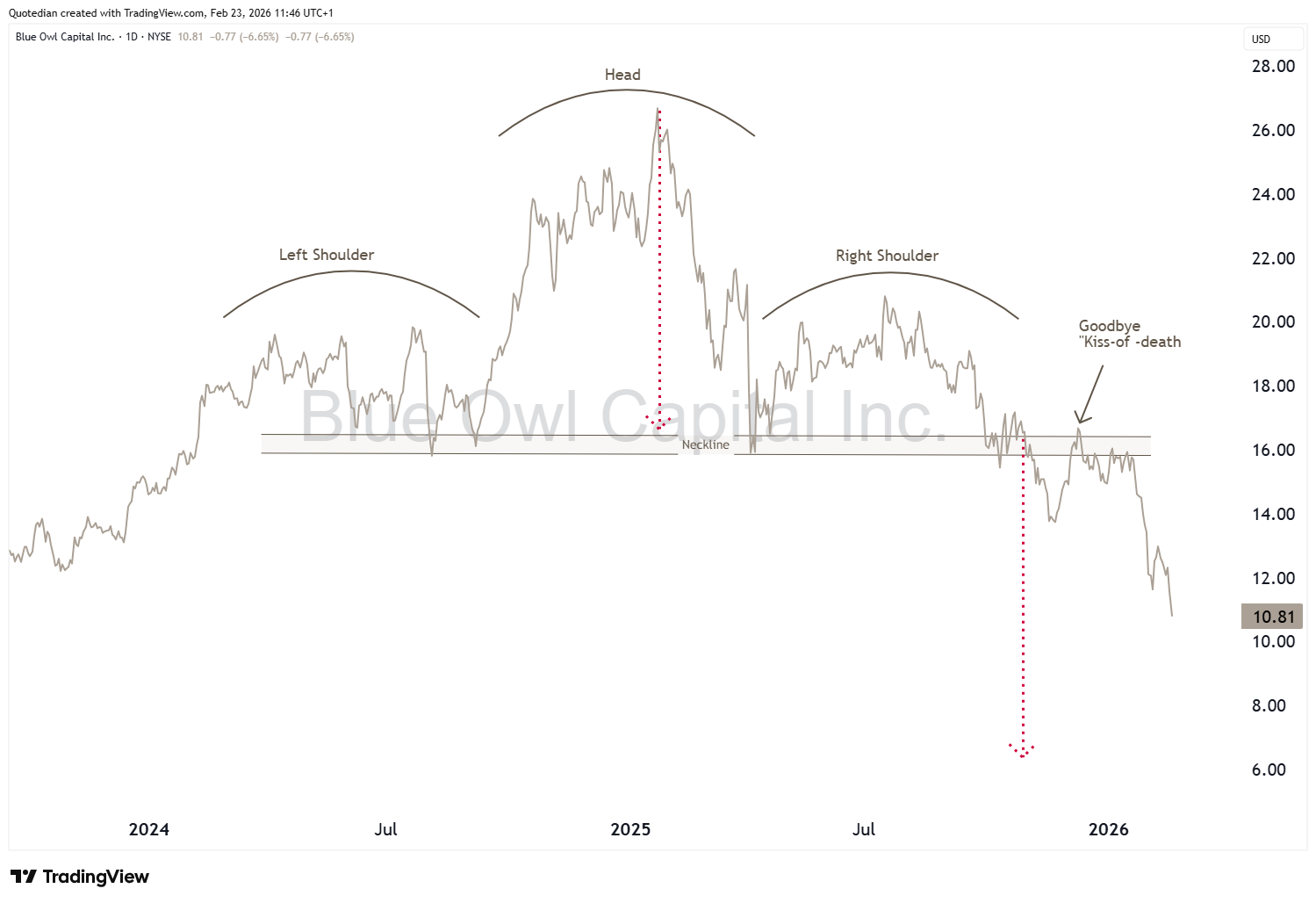

Already back in October, Part I of the “Pirate Credit” Saga was premiered, shares of Blue Owl were already down 50%+ peak to low:

Since then shares are now down 60%, which does not sound like an awful lot more, but as investment maths would have it, any bottom-fisher or bargain-hunter buying a fifty percent pullback back in October would now be down over 30%:

And you know what, simple, rule-based technical analysis (shoulder-head-shoulder pattern), would indicate that the (low) price target may carry a six-handle:

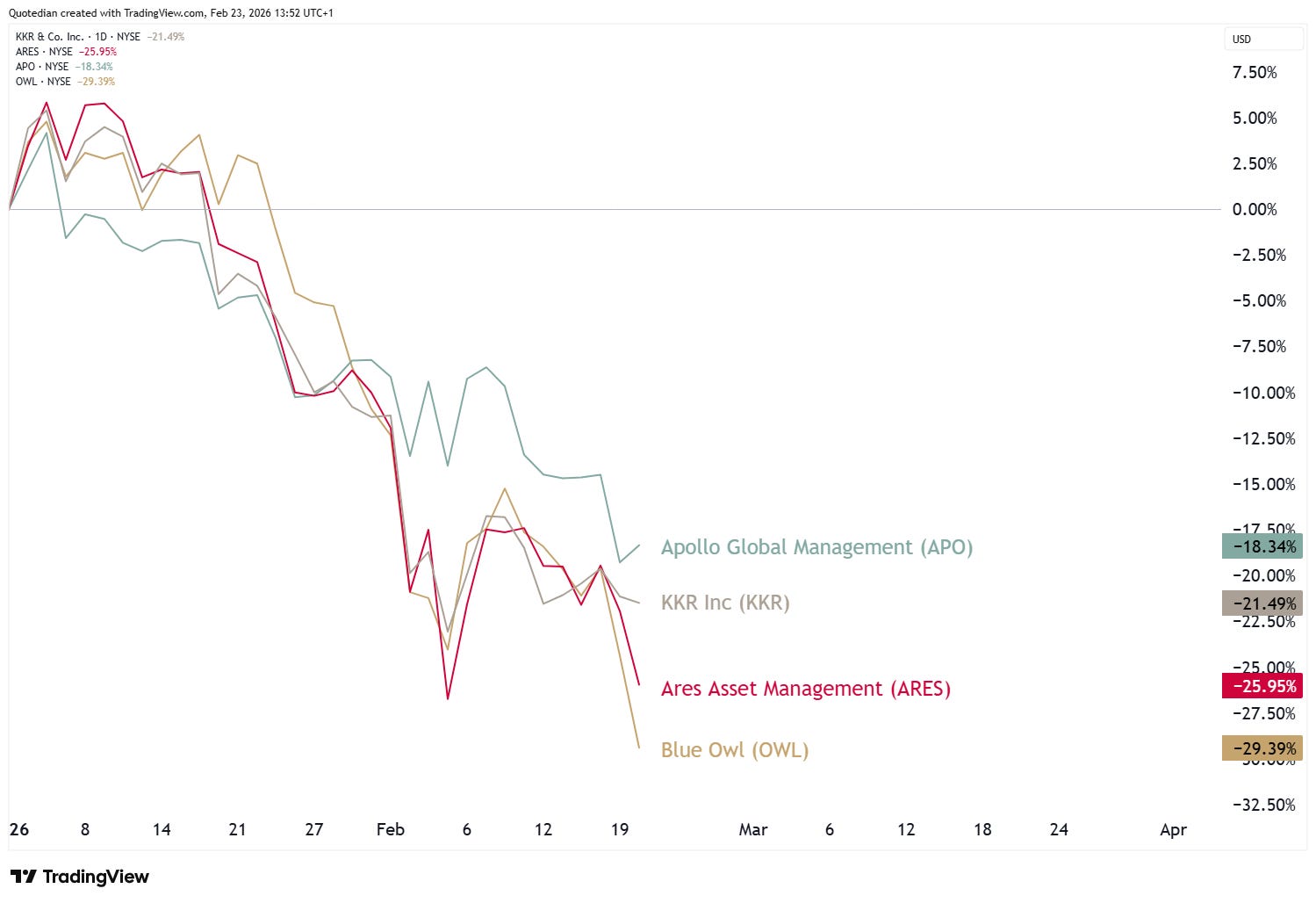

But, of course, did the headlines surrounding Blue Owl (OWL) last week not remain confined to OWL, but spread across to other similarly listed private credit and private equity, both closely (and lethally) connected outlets. The following year-to-date performances are just a refined selection of some of the larger players in this space:

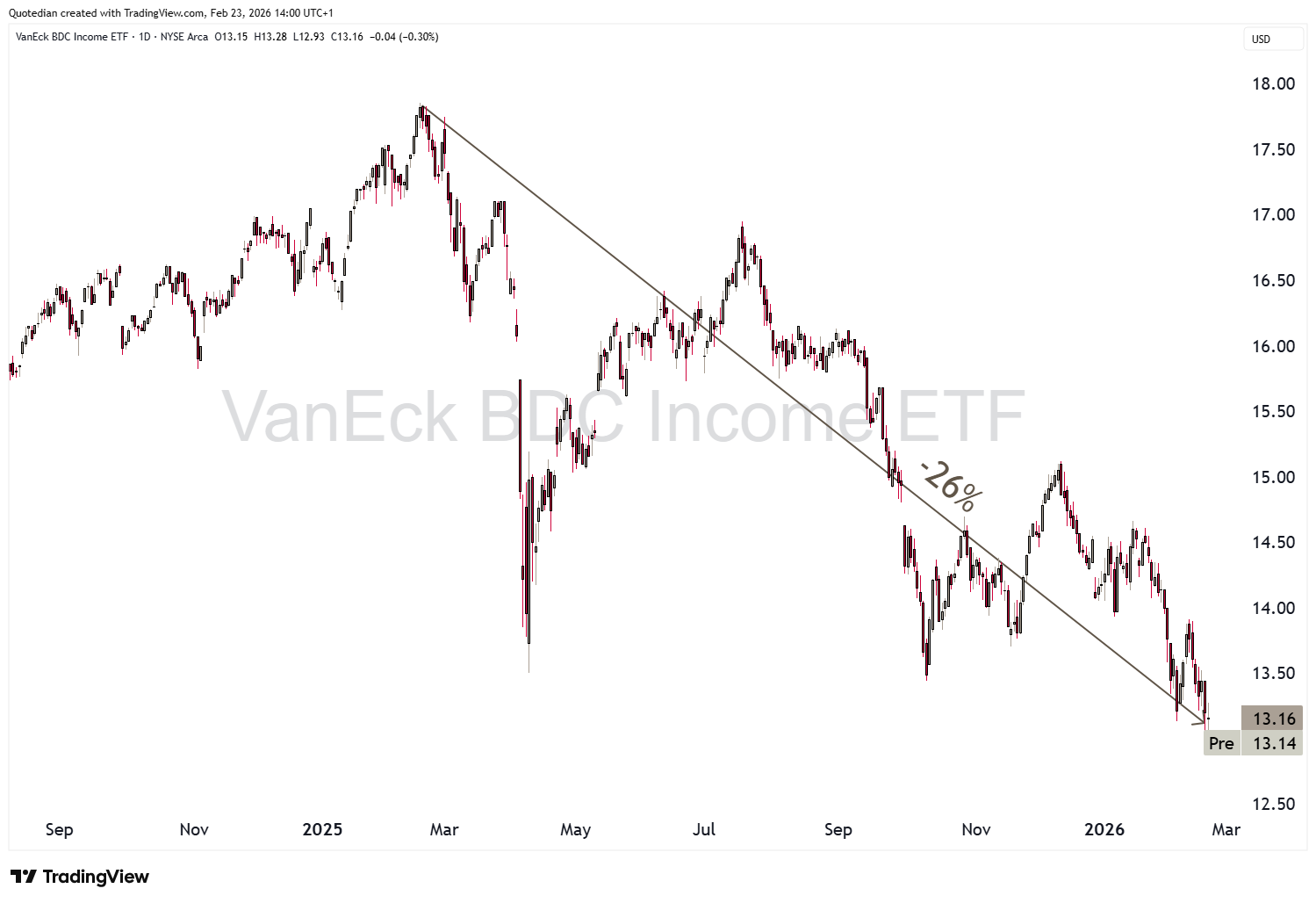

And here is the chart of the VanEck BDC Income ETF that I DID show back in October and the is highly correlated with the fortunes of the private credit sector:

And here’s the update of that chart:

In conclusion, and zooming out on this some chart,

you could rightfully ask whether it is time to try and catch that falling knife at current levels. IMHO and FWIW, this is something I would not touch 10-yards pole, given the immense opportunity set out there and the high risk associated to this market segment, which after all, carries TWO OF THE MOST IMPORTANT market risks in existance:

Too much dumb money running after a dumb idea (after all, private credit is covenant lite credit)

andA classical duration mismatch, where quarterly redemptions are promised on five to ten year duration loans. (Ask SVB for their recent experience on duration mismatch…)

Let me finish then with the question that is probably burning on your lips (or at least should be):

Where is the regulator on all of this?

My blunt answer:

What regulator?

The FT’s Alphaville slightly more eloquent reply on the same:

ONWARDS …

Equity markets had a largely ‘boring’ week last week, with US markets regaining nearly all of the previous week’s losses and European markets building further on gains.

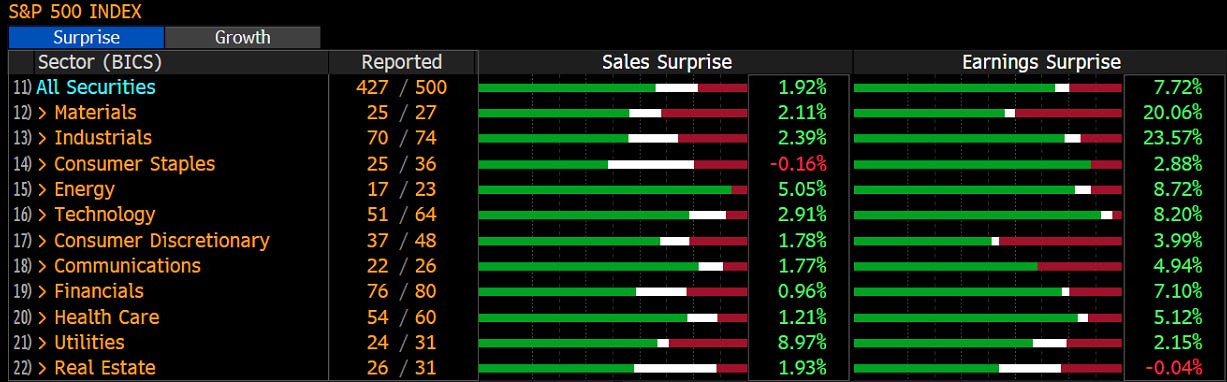

On one hand side, newsflow (private credit, Iran, tariff back-and-forth, etc.) are exerting downside pressure on stocks, whilst earnings

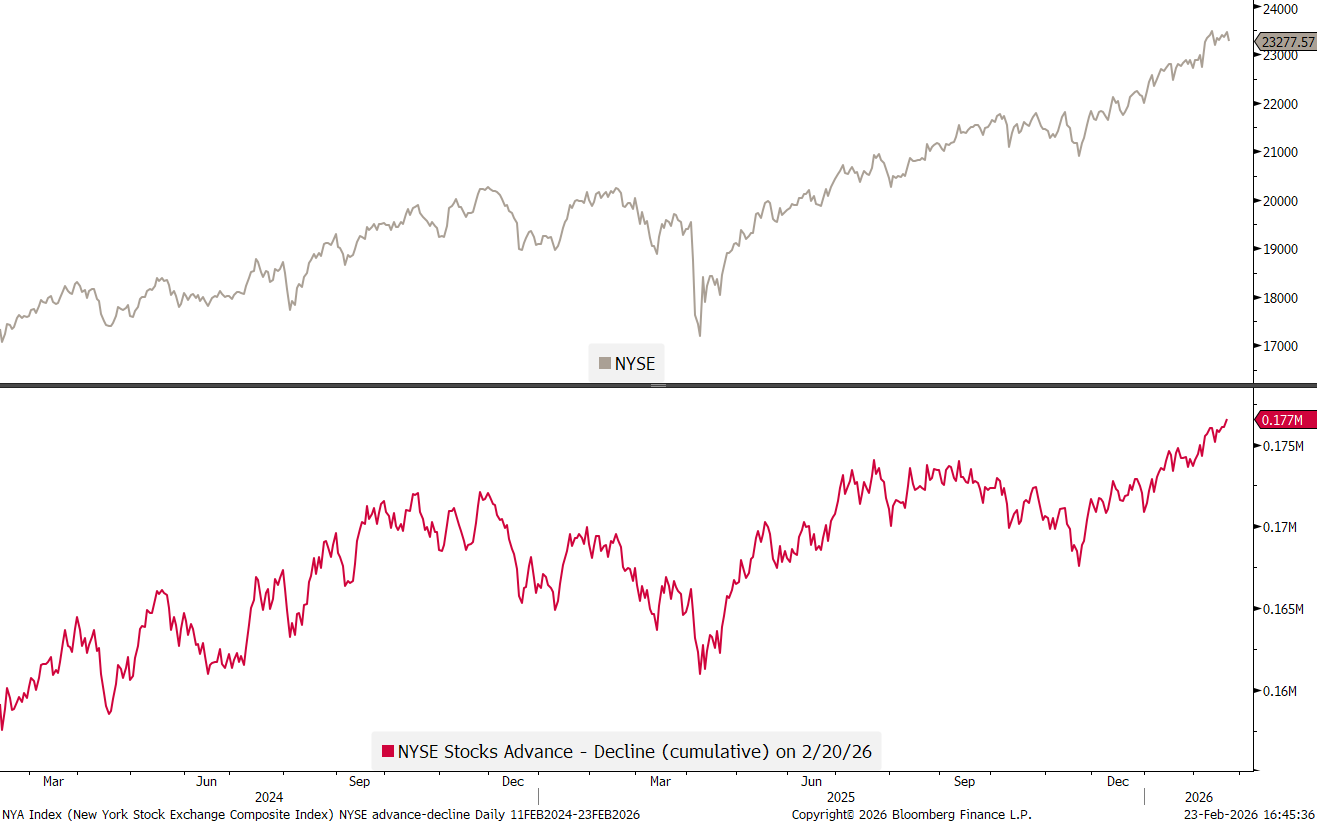

continue to be supportive and market breadth also remains constructive:

It is maybe therefore that the almighty S&P 500 continues to be stuck in that 200-points range:

And also maybe it is why the dispersion on the index is so bi-polar (aka barbell) this year. Take this graph from the fine folks at Bespoke Investment Group, which shows that whilst the index is up just about one percent year-to-date, only one-in-five stocks is up or down less than 5%, with a big majority showing much wider outcomes:

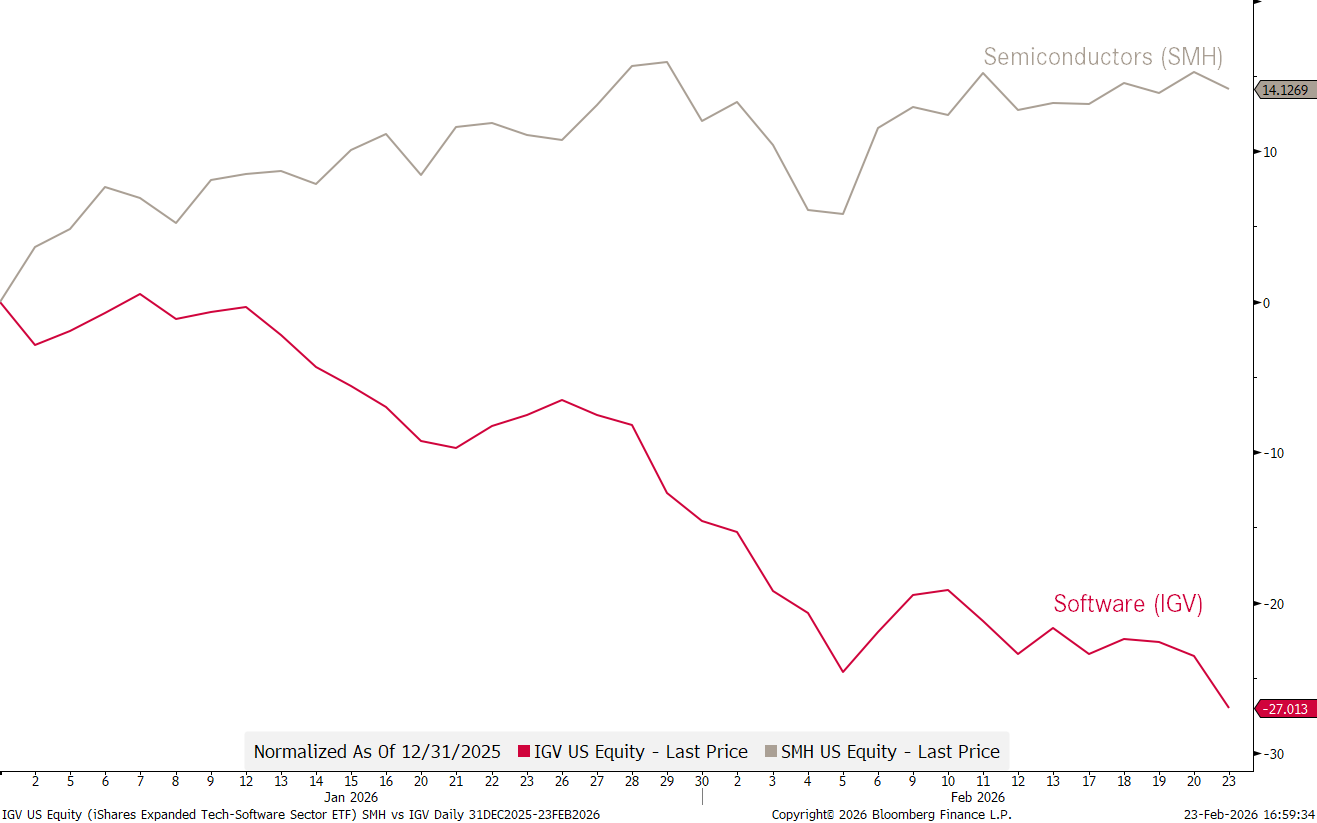

But probably the widest and most stunning dispersion between up and down comes out of the SAME(!) sector. Here’s the performance difference between semiconductor (SMH) and software (IGV) stocks on a year-to-date basis:

That’s 41% performance difference just year-to-date!!!

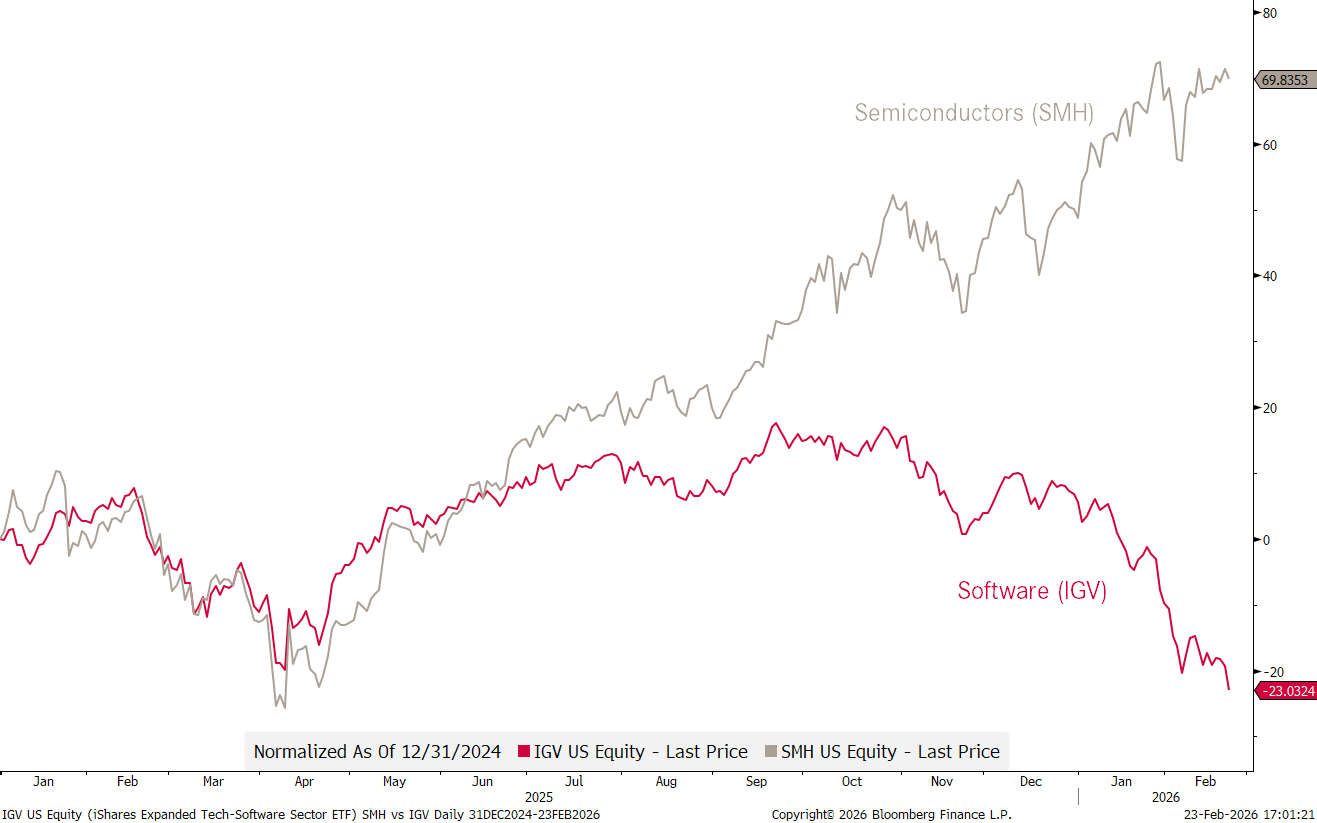

Zooming out to go back one more year:

Make that 93%(!) of performance delta in less than 14 months … WOW!

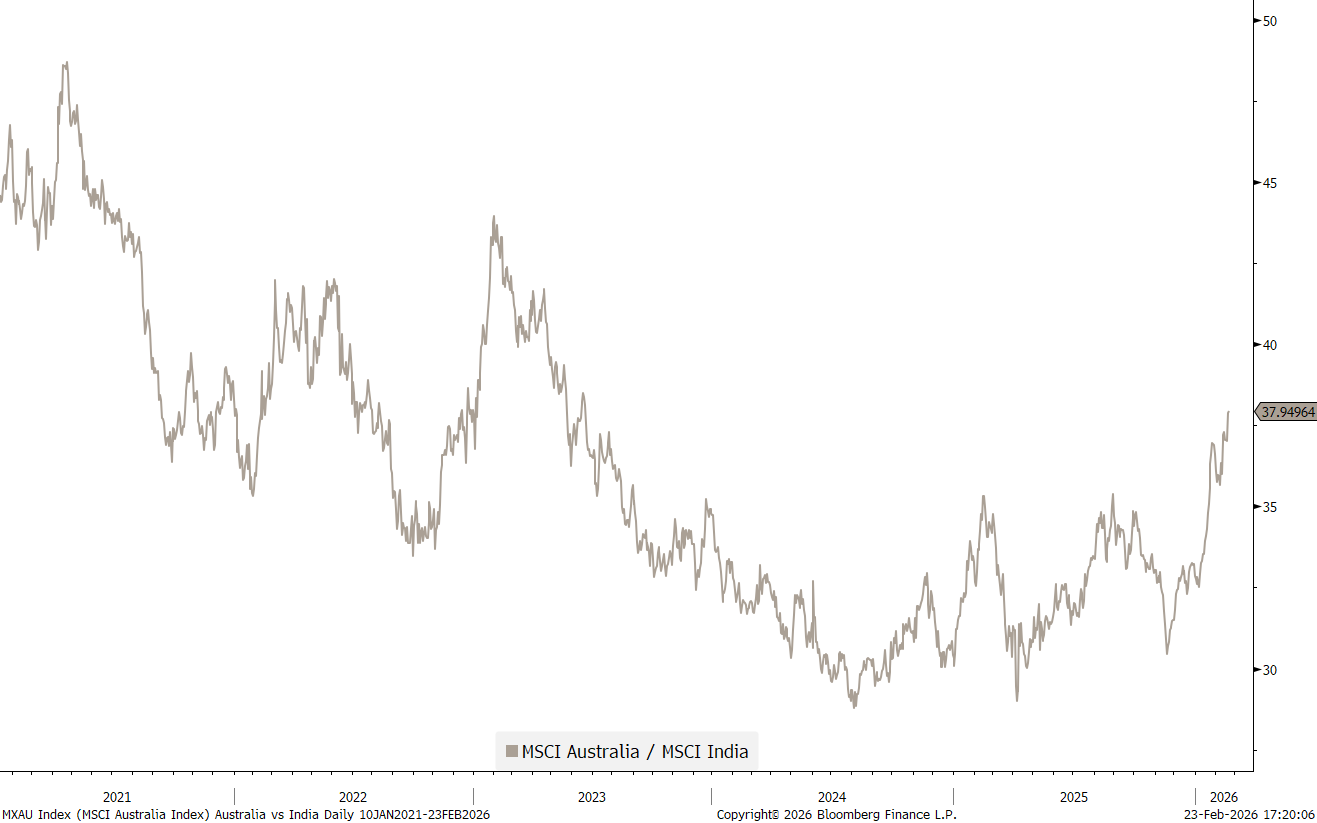

To finish off the equity part, here’s a country pair trade you should implement if you believe the impact of AI on sectors such as software and services and the “age of empire” both continue. Long Australia, short India:

In bond/rates markets, just two observations:

First, the yield on the Tens continues to adhere to our consolidation triangle established many moons ago:

As mentioned on several occasions, we expect a resolution out of the triangle in Q2 of this year. Which direction? No forecasting here, just patiently waiting and then ready to follow the outcome, whatever it is.

The second observation goes to credit spreads, which (so far) largely fail to show any nervousness regarding the deteriorating situation in private credit markets:

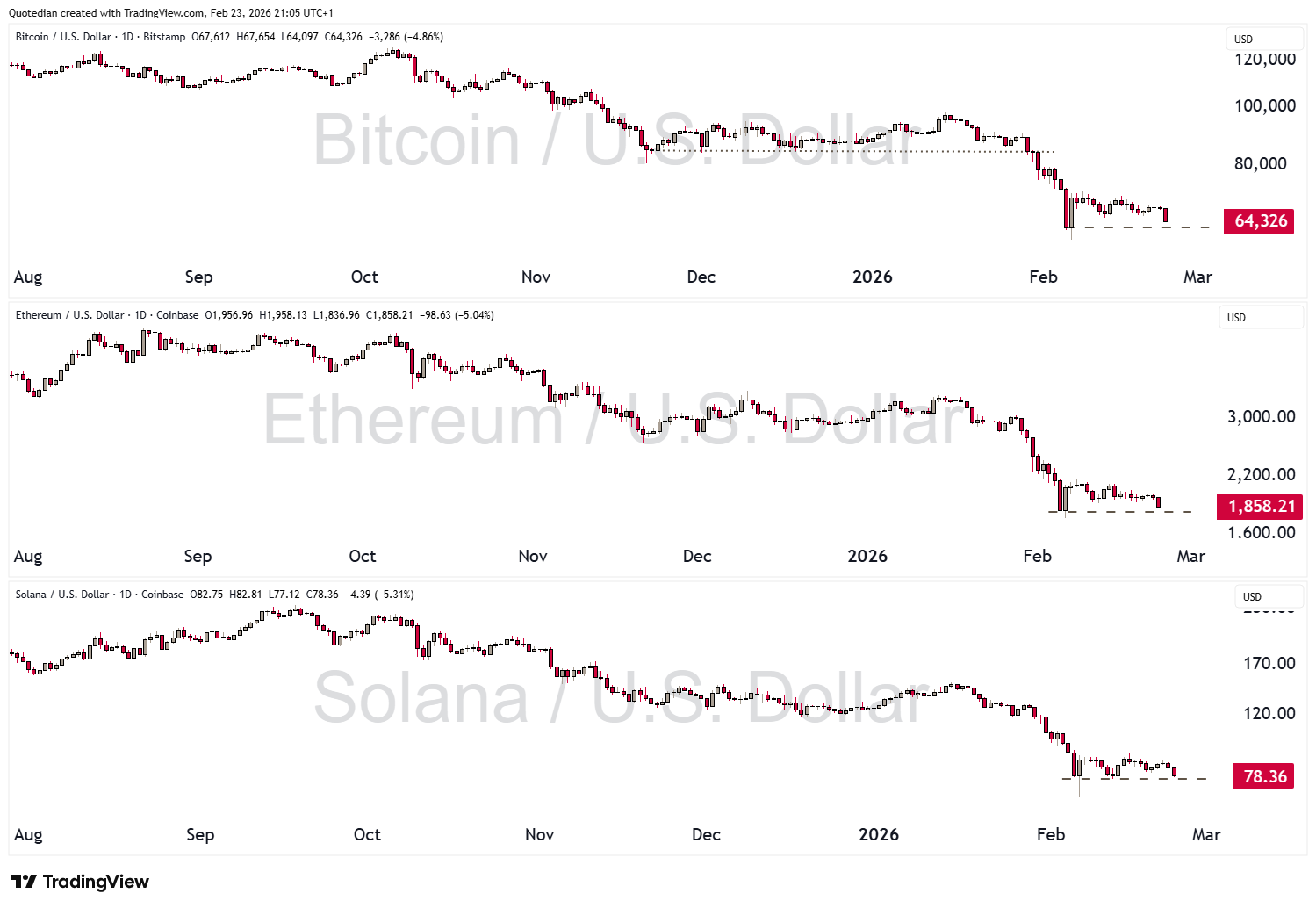

We will skip the currency section this week, only highlighting that in cryptocurrency-wonderland all three larger cryptos (Bitcoin, Ethereum and Solana) seem ready to attack key support levels again:

Having hopelessly overrun on time with regards on writing this week’s Quotedian, let me add just three more charts, all related to commodities.

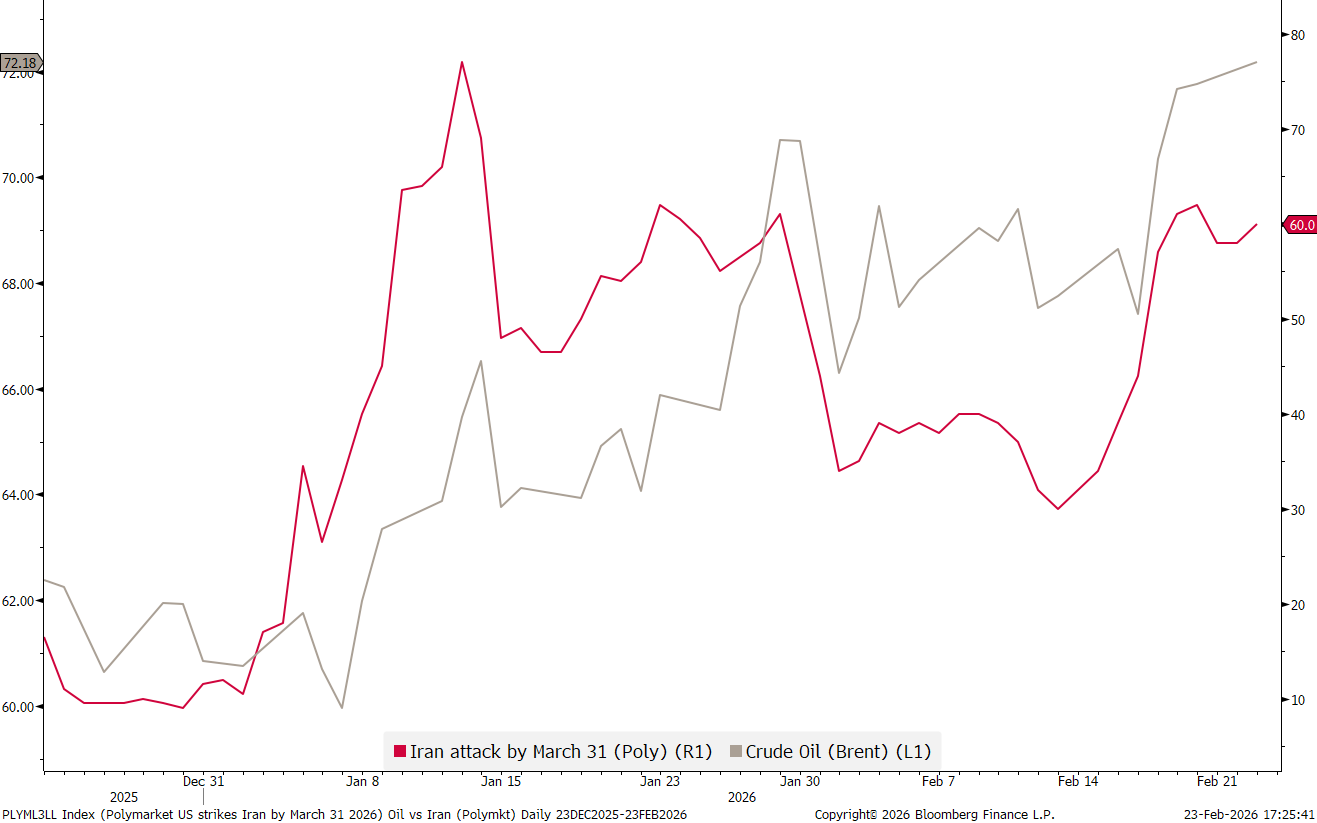

The first chart shows the correlation between Polymarket bets that the US will attack Iran before March 31st (red) and the price of Brent (grey):

Not really a surprise there - but still important market implications. Will it be: “buy the rumour, sell the fact” with the selling commencing once an attack really happens? We may not need to wait until the end of March to find out, as chances for an ‘intervention’ are not slim once Trump’s “State-of-the-Union” address (Tuesday) and India PM’s Modi visit to Israel (Friday) is over …

The second chart may kind of confirm that just forementioned thesis:

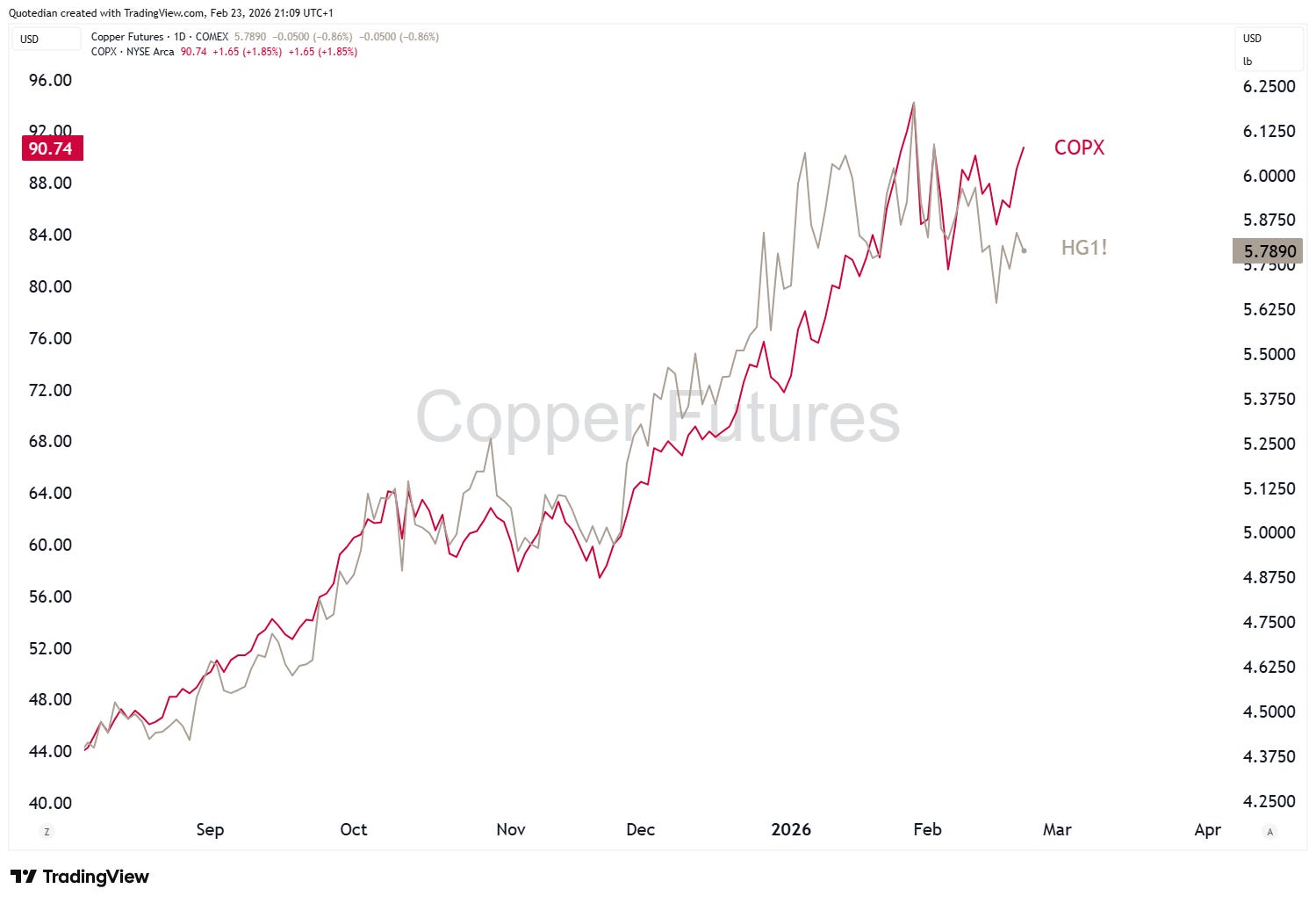

And finally, our third chart argues that Copper Mining stocks (COPX ETF - red line) may be leading the Copper Futures prices (grey line) higher:

Investment thoughts:

Do NOT catch that falling private credit knife

Wait for breakout in S&P 500 for clearer directions, though over the intermediate term path of least resistance continues to the upside

Similarly, remain duration neutral with your fixed income exposure, but maybe seek to improve the credit quality if necessary

Stay away from cryptos right now

Buy copper stocks on a set-back, buy gold/gold stocks on a break out

That’s all for this week - with a bit of luck our brand new Quotedian - Daily Edition (letter formerly known as The QuiCQ) should be out tomorrow Wednesday. Sign up below if you have not done yet so:

In the meantime: May the Trend be With You!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG

Who would have thought that a 15-20% IRR was difficult to obtain with simple loans?😱😱