Potpourri

The Quotedian - Vol VII, Issue 18 | Powered by NPB Neue Privat Bank AG

"Life is a tragedy when seen in close-up, but a comedy in long-shot."

- Charlie Chaplin

Today’s Quotedian will be a short, random walk down the asset classes alley. Just a simple, ad-hoc potpourri of market observations ahead of our end-of-the-month issue due next weekend.

Believe markets are a random walk? They are not. Speak to us.

Contact us at ahuwiler@npb-bank.ch

Let’s get down and dirty then …

On the surface, European equity markets are trading flattish to slightly positive today, given the absence of any guidance from US markets, which are closed for Memorial Day. The broad STOXX Europe 600 index is up 0.25% about two hours before session close:

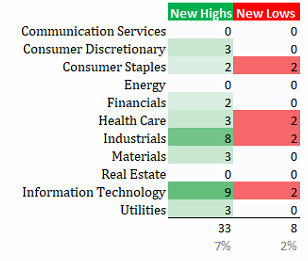

Looking under the hood though, we realize that today’s strength is much … well … stronger than the index itself would reveal, i.e. 33 stocks are hitting a new 52-week high today, versus only fours stocks trading at a new 52-week low:

With over half of those stocks being industrials, go figure how the European economic recovery is fairing …

And in case you are wondering what names are included in those 33, here you go:

In the US, where stocks recovered on Friday from a slump the previous day,

we got a similar new 52-high versus new 52-week low ratio:

Interested to see those names too? Hit the like button and then send me an email (ahuwiler@npb-bank.ch)

The Nasdaq recovered close to one percent on Friday after Thursday’s slump and the chart “smells” like new all-time highs will be reached this week:

Of course was NVDA the big winner, as it gained another $345 billion of market cap during the week:

In case you wondered, only 19 companies in the S&P have a market cap in excess of those $345 billion that NVDA added in ONE WEEK:

Here’s another random observation for the galleries - remove any sharp objects nearby …

We agree that the Nasdaq must have been one of the best performing indices over the past decade or so, right? Well, here’s the chart of the Nasdaq (NDX) expressed in Bitcoins:

Over in Asia, Indian equities (BSE 500) are hitting new all-time highs in the last week before the election window closes (June 1):

Japan’s Nikkei index looks slightly trendless at the moment:

And Chinese stocks trading in Honk Kong (HSCEI) are seemingly also trying to end their short-term consolidation:

Ok, time for some useless fun sector charts!

Let’s start with the US discretionary consumer sector, which in relative terms is hitting a 10-year low:

So, what are the main constituents of the sector? These are the top weights in XLY:

And these are the main detractors this year:

But keep in mind, it is a relative performance chart, the absolute chart of XLY does not look as nasty:

Performance of Transportation stocks (IYT - iShares US Transportation ETF) is a bit more worrisome in that context:

A breakdown below key support (dash line) and 200-day moving average (black line) would be anything else but constructive.

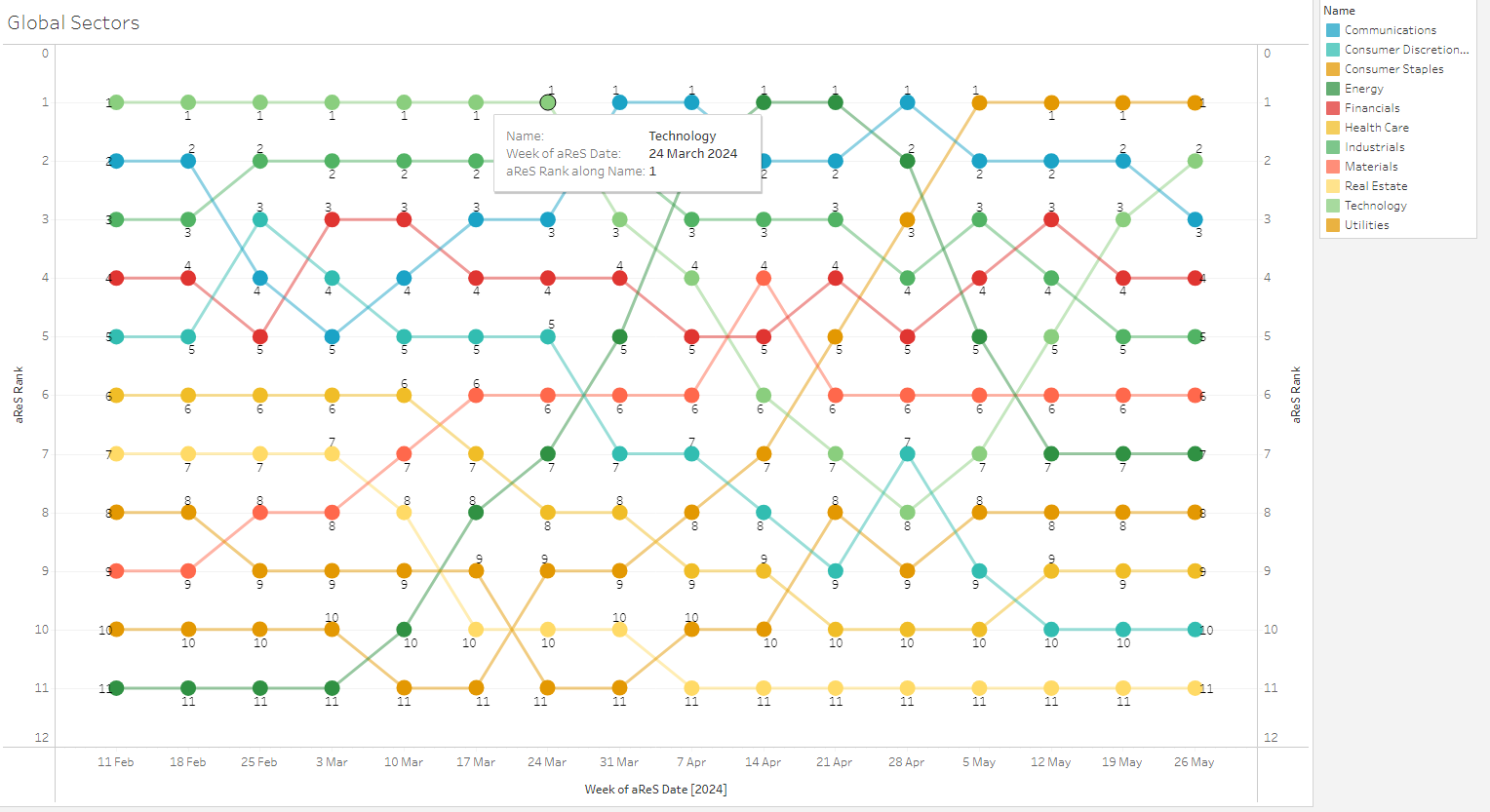

So, which sectors are going up then?

Our proprietary aReS model suggests to overweight utilities, technology, communications and financials and to stay away from real estate, consumer discretionary and health care:

Bloomberg’s RRG (Relative Rotation Graph) model agrees more or less with that ranking:

Last week not only brought us smokin’ hot NVDA quarterly earnings, but also a tad to hot PMI readings:

The far right column was last month’s reading, the circled column was the number reported on Thurday and the column to the left of that was expectation.

As you can easily see, the numbers came in well above the previous month and expectation, which was a bit too much for the bond market to handle. Expectations for a rate cuts by end of 2024 fell further from 2 to 1.5,

and bond yields rallied,

sending bond prices lower:

From a technical analysis point of view, the triple rejection at resistance (black dashed), downward sloping trendline (red dots) and 200-day moving average (black line) does not bode well at all (all circled). Stay strongly underweight for now, as outlined in our latest quarterly outlook.

In Europe in the meantime, the ECB insist on cutting rates in June, which is now nearly fully baked into futures markets:

Nevertheless, did 10-year Bund yields also jump last week:

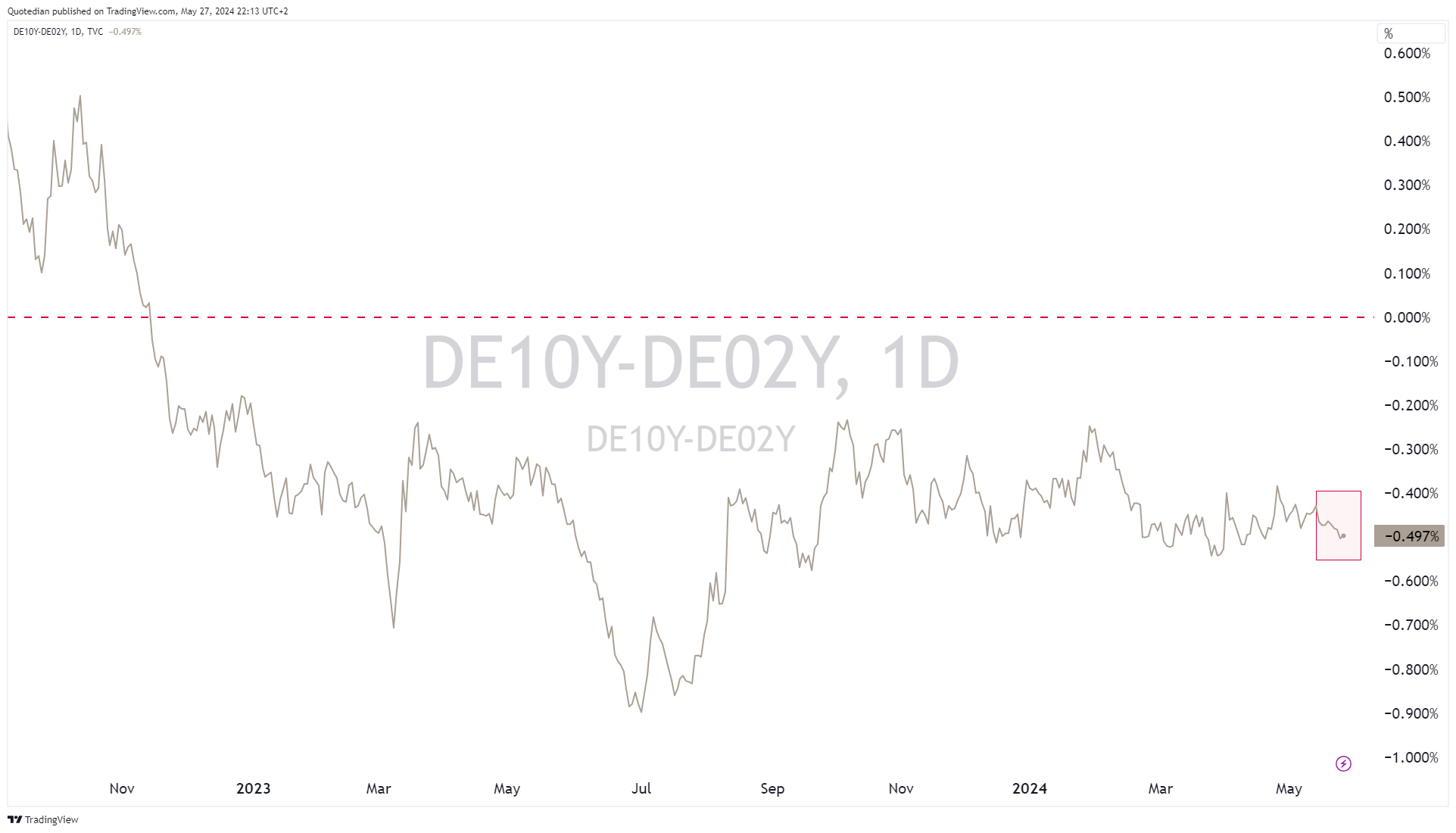

This caused the yield curve (10y-2y) to slip further back into inverted territory:

Indian bond holders must have been on a tear with yields collapsing 25 bp in short span of time:

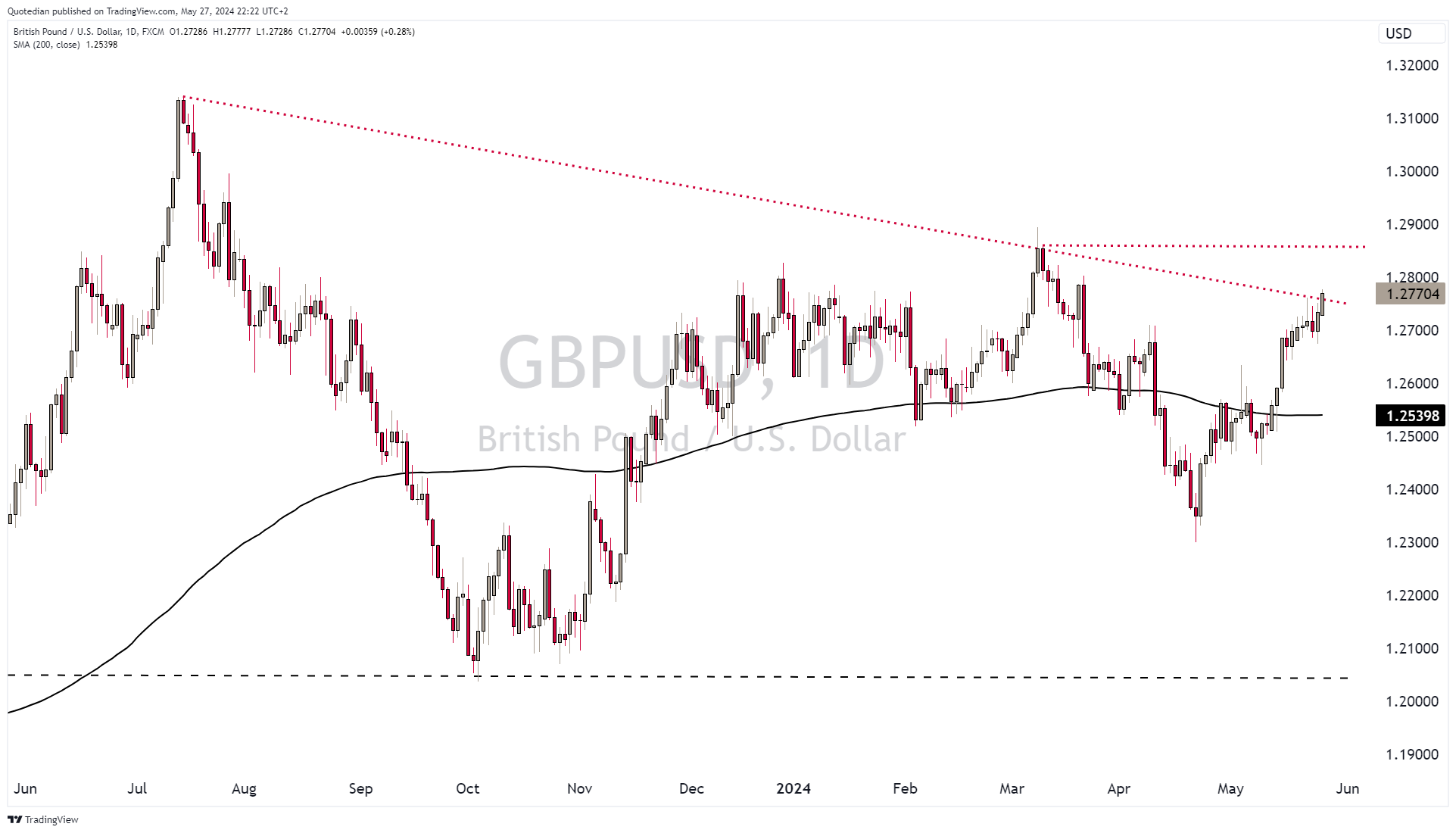

In currency markets, the GPB has been rallying versus the USD,

and the EUR,

since the announcement of general elections to be held on July 4th.

A strange choice of a date, maybe that why the Sterling is celebrating government change already now….

The EUR/USD cross-rate …. well, never mind …

The USD/JPY cross is also looking similar indecisive:

Much more action to be had in cryptocurrencies, where Bitcoin for example seems ready to move higher again:

But the real action has been in Ethereum, as rumours of a ETF on this cryptocurrency are sending the XET higher:

But over the past twelve months, Solana has been the true winner:

Finally, in the commodity space precious metals continue to attract most attention. Gold has corrected about a hundred bugs, but the chart does not feel bearish at all:

Price behaviour in Silver,

is indicating that we might be at the start of one of those crazy period of price spikes:

Are you long already?

Platinum is always a bit slower to react, and hence offers a nice “defensive” way to play the wave:

Ok, time for Quid Pro Quo: I hit the send button and you hit the like button. Deal? Deal!

Here’s one last one for the gallery of useless pair trades …

The Invesco Solar ETF, which tracks securities in the solar energy industry and with the catchy ticker TAN,

is trying to start a new outperformance cycle versus dirty, dirty fossil fuel oils (proxied via XLE):

Breaking above the 200-day moving average (black line) would confirm this long/short idea.

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance