Rejection

The Quotedian - Vol V, Issue 108

"In investing it is never wrong to change your mind. It is only wrong to change your mind and do nothing about it."

— Seth Klarman

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

Without further ado, let’s dive right into yesterday’s market observations …

Global stock markets retreated yesterday, and for now, the S&P 500 as the benchmark for anything equity, respected the “final” resistance we had identified yesterday in the form of the 200-day moving average and the downward sloping longer-term trendline:

As the following few graphs/stats will show, market internals were relatively weak, but keep in mind that volumes were, in typical late August fashion, also low, so anything should be taken with a grain of salt.

The intraday chart of the S&P 500 mini futures contracts shows that stocks sold off throughout most of the session until they found some footing just before and right after the release of the June FOMC meeting minutes, which were leaning to the dovish side. Though stocks continued to deflate shortly after again:

Only one sector in the S&P managed to eke out a gain on the day:

Breadth was weak, with close to four stocks falling for every stock advancing higher, which is also pretty clearly visible in yesterday’s market heat map:

We haven’t looked at the European equity chart for a few issues now, so let’s do that:

In a nutshell, similar to the US equity chart, but weaker. Specifically, the SXXP has neither quite reached its 200-day moving average, but maybe more importantly and unlike its US counterpart, as not (yet?) exceeded the 50% retracement from the January to June sell-off.

Just before we turn to bonds, let’s have a quick look at one of the few markets with a GREEN UP arrow under the long-term column: Japan!

Really quite the bullish chart, with a run-up to the January highs likely, unless other global markets fall completely out of bed. But definitely worth the relative play versus other, weaker markets (Europe?). Finally, all this Yen weakness is good for something …

Moving into fixed income markets, there was some divergence between the slope of European curves versus the one in the US. Whilst the former flattened after the highest inflation rating in 40 years in the UK, the latter steepened somewhat for the first time in a while as the rally in 10-year yields outpaced the one in shorter-term yields on the back of the dovish FOMC minutes.

And let me commit some chart crime here (i.e. using two different scales for comparison and ‘proof’ of correlation), by showing how high yield bonds (HYG) have not been confirming the equity (SPY) rally as per late:

In currency markets little new observations to be had, except that it was a good day for the US Dollar, but also a very quiet (i.e. low volatility) session:

So, as there is nothing to see here …

… let’s move to our final observations for today in the commodity space.

Gold had a bad-hair day yesterday and continues to give back some of its latest rally attempt from key support levels. However, as long as the price stays above $1,740 per ounce, that attempt remains valid:

Oil (Brent) has found some kind of a footing after an (oil price bullish) US inventory report yesterday. Though the overall picture remains weak, with the price below its 6-months trading range AND below its 200-day moving average:

Time to hit the send button. Enjoy that Thursday of yours!

— André

CHART OF THE DAY

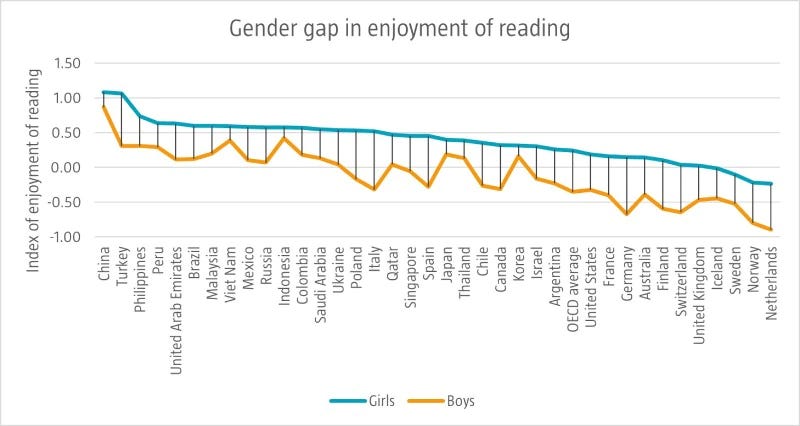

Actually, today’s COTD, should be titled “Shameful Chart of the Month”. Put together by the fine folks at Robeco, it illustrates the ‘Joy of Reading’ amongst boys and girls in different countries. I will leave you with Robeco’s comments and their chart, but not without adding my observation, that the more (supposedly) ‘developed’ a country is, the less we seem to read…Shame on us!

In all countries and economies, girls reported much greater enjoyment of reading than boys, according to the OECD’s Program for International Student Assessment (PISA). The largest gender gap in enjoyment of reading was observed in Germany, Hungary and Italy, and the smallest in Indonesia and South Korea. On average, both boys and girls reported significantly less enjoyment of reading across OECD countries in 2018 than their counterparts in 2009. In the 2018 PISA study, girls outperformed boys in reading by almost 30 score points. Boys however, outperform girls in mathematics, but by a much smaller margin.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance