Summer Break!

Vol IX, Issue 26 | A NPB Original

“The mind should be allowed some relaxation, that it may return to its work all the better for the rest.”

— Seneca

Not a TL;DR, but a short note that this is the last Quotedian before a hopefully well-deserved summer break. We should be back around mid-August, depending on markets and/or Trump’s social media feed …

This week, as promised in our previous Quotedian (“The Show Must Go On”), the Quotedian will look at some of the highlights out of NPB’s Q3 2026 outlook, which has been freshly published this morning.

You can find the full documents in the pressroom on our website:

Or, have a look at the executive summary in our video here:

But, in any case, all the fun is in the charts, of which I will share my favourite ones below - please enjoy and if you enjoy, please like!

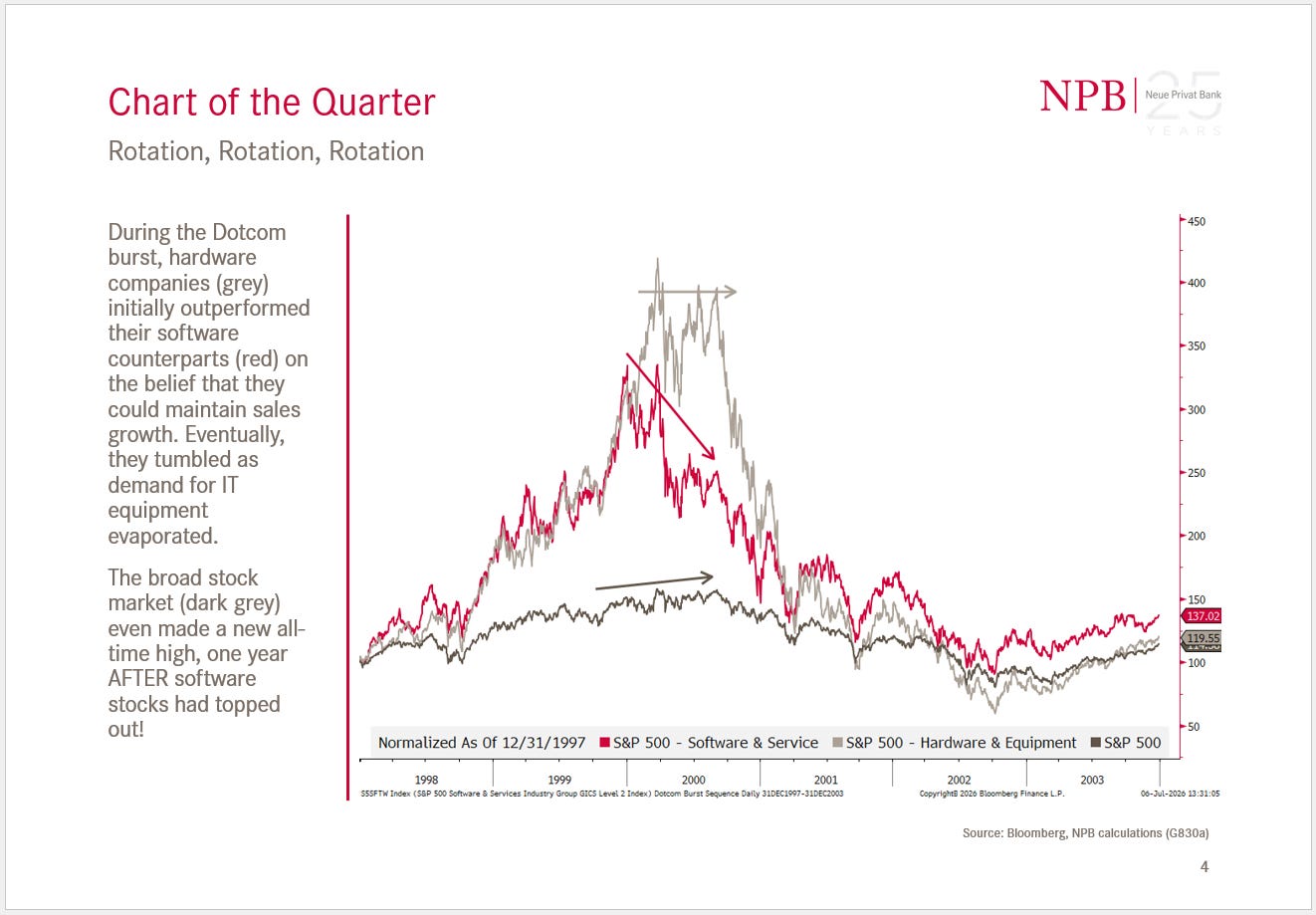

Let’s start with the chart of the quarter, which set as a reminder that back in 2000, software stocks topped out several months before hardware stocks did, and nearly a year before the overall market (S&P) rolled over:

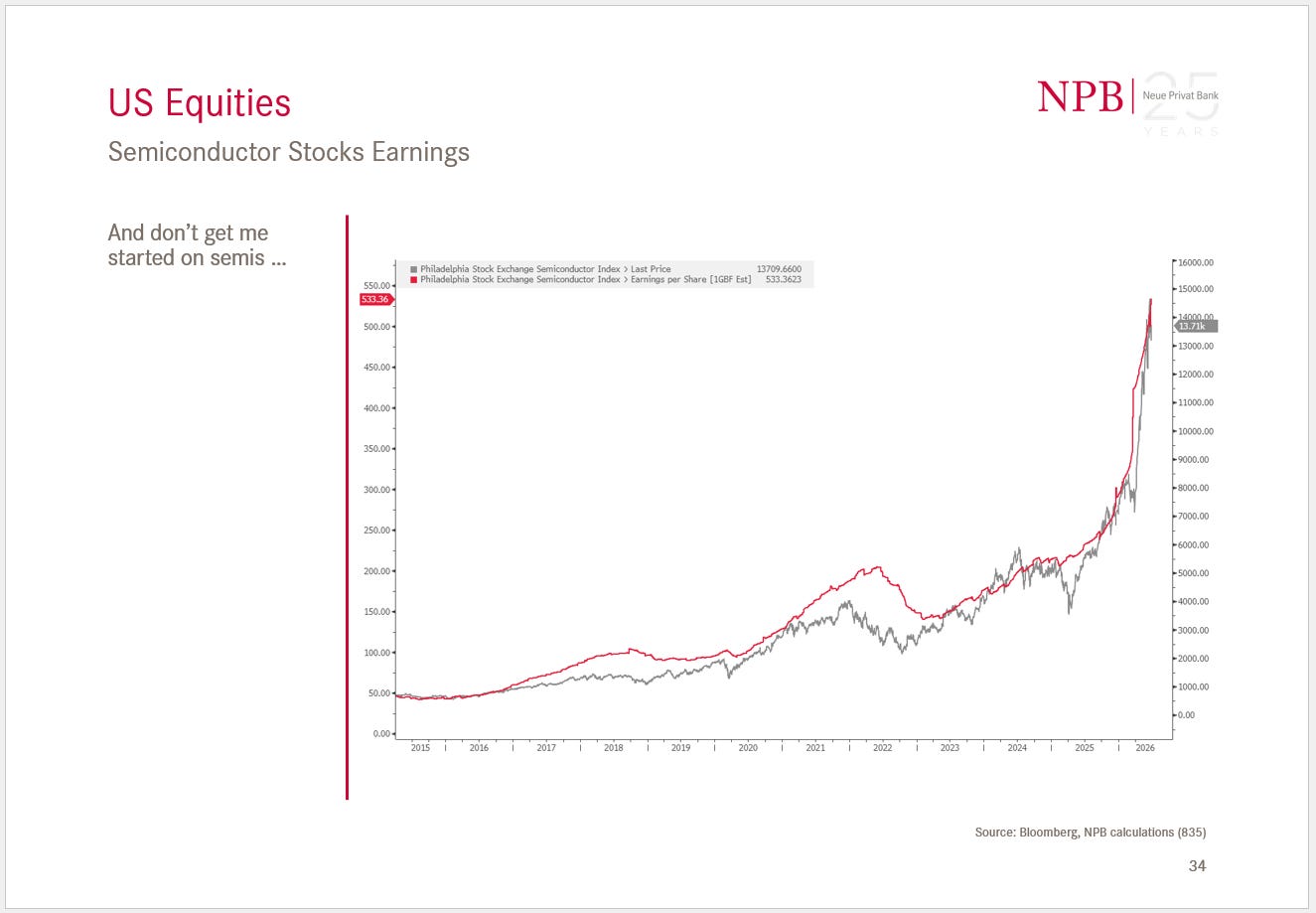

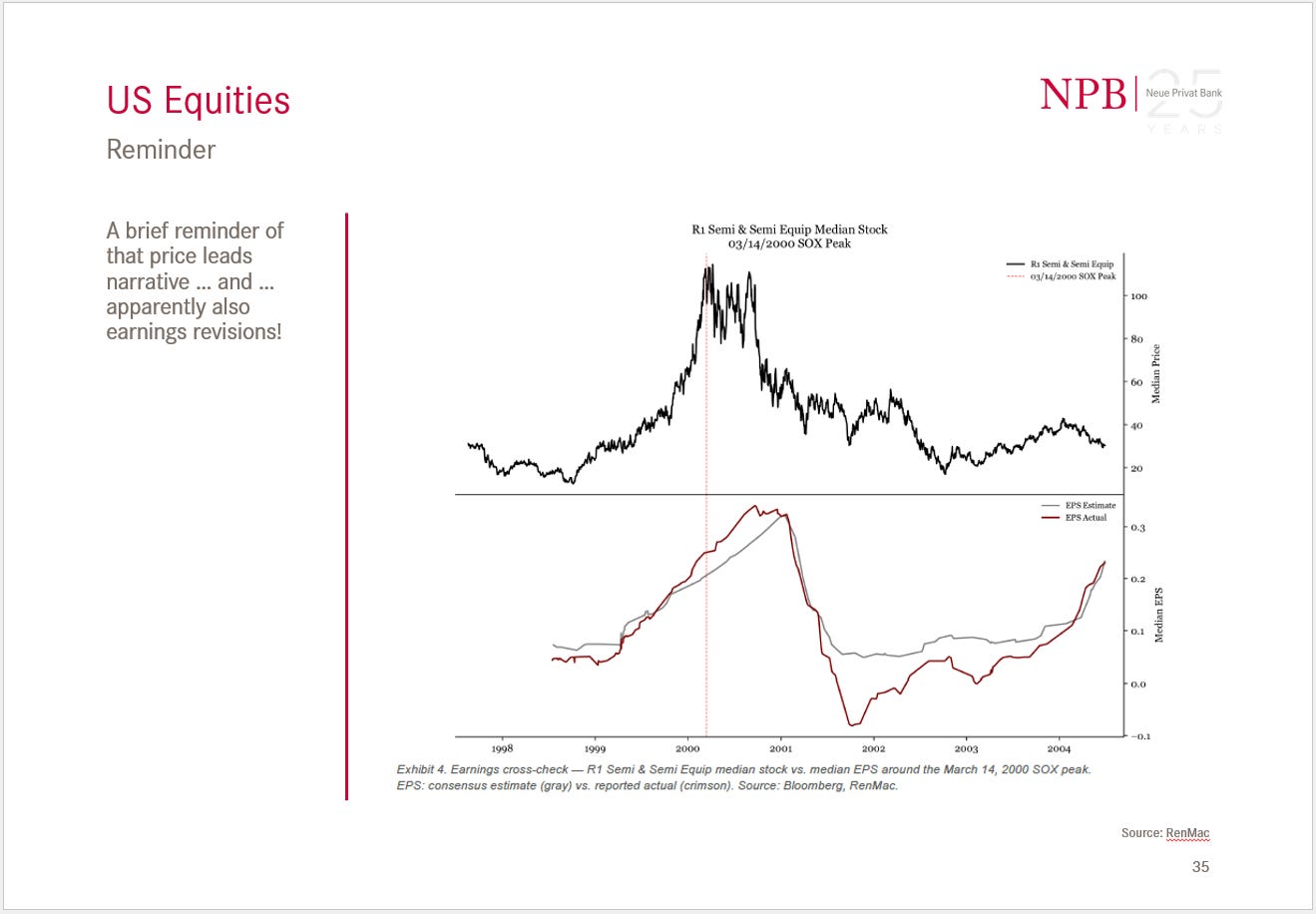

Very similar, given the current sky-high earnings expectations on semiconductor stocks for example,

it should not never be forgotten that actual and forward earnings tipped lower months (!) after stocks had turned lower:

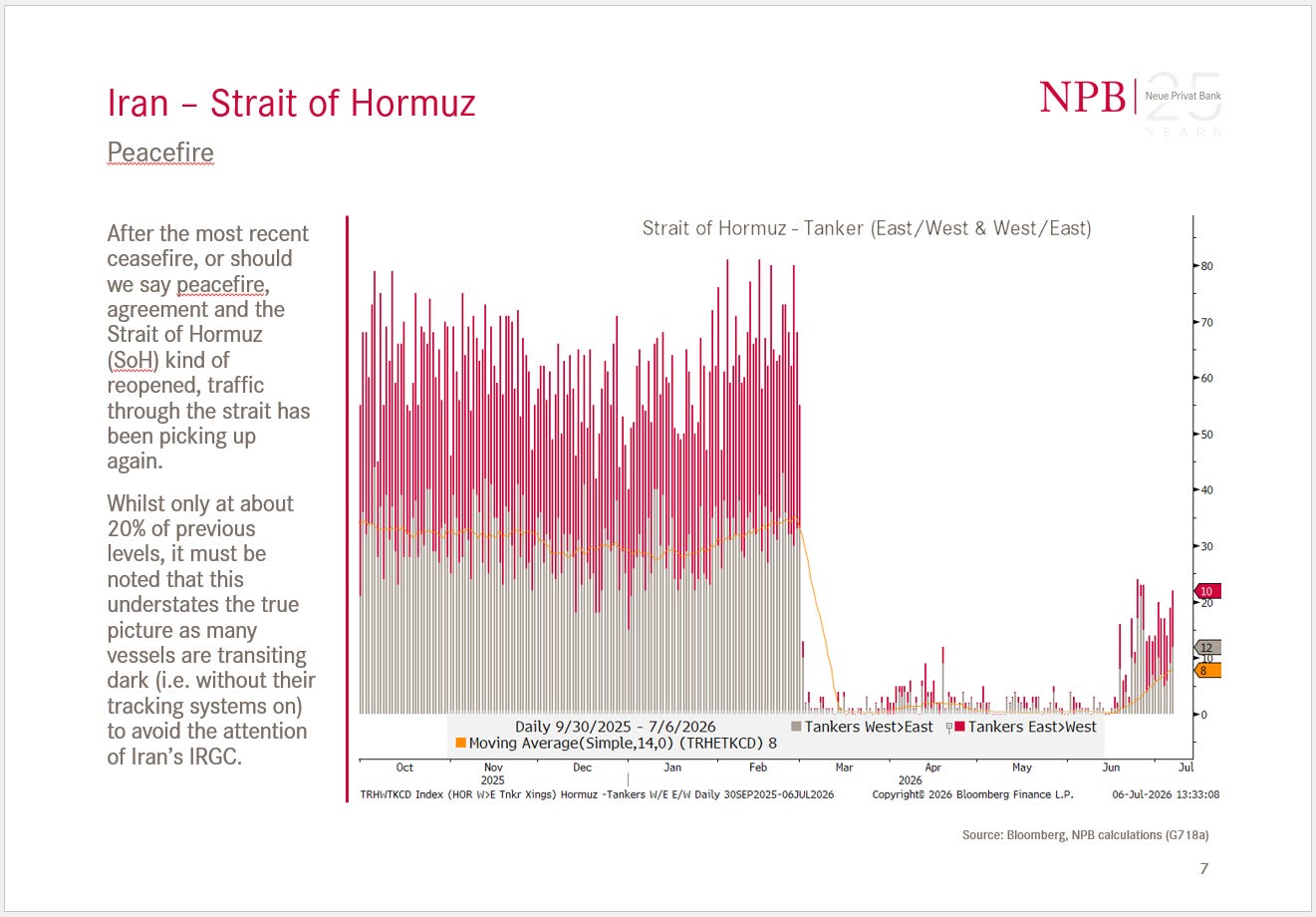

The Strait of Hormuz (SoH) and its on-off-on-off re-opeing is of course also a topic discussed:

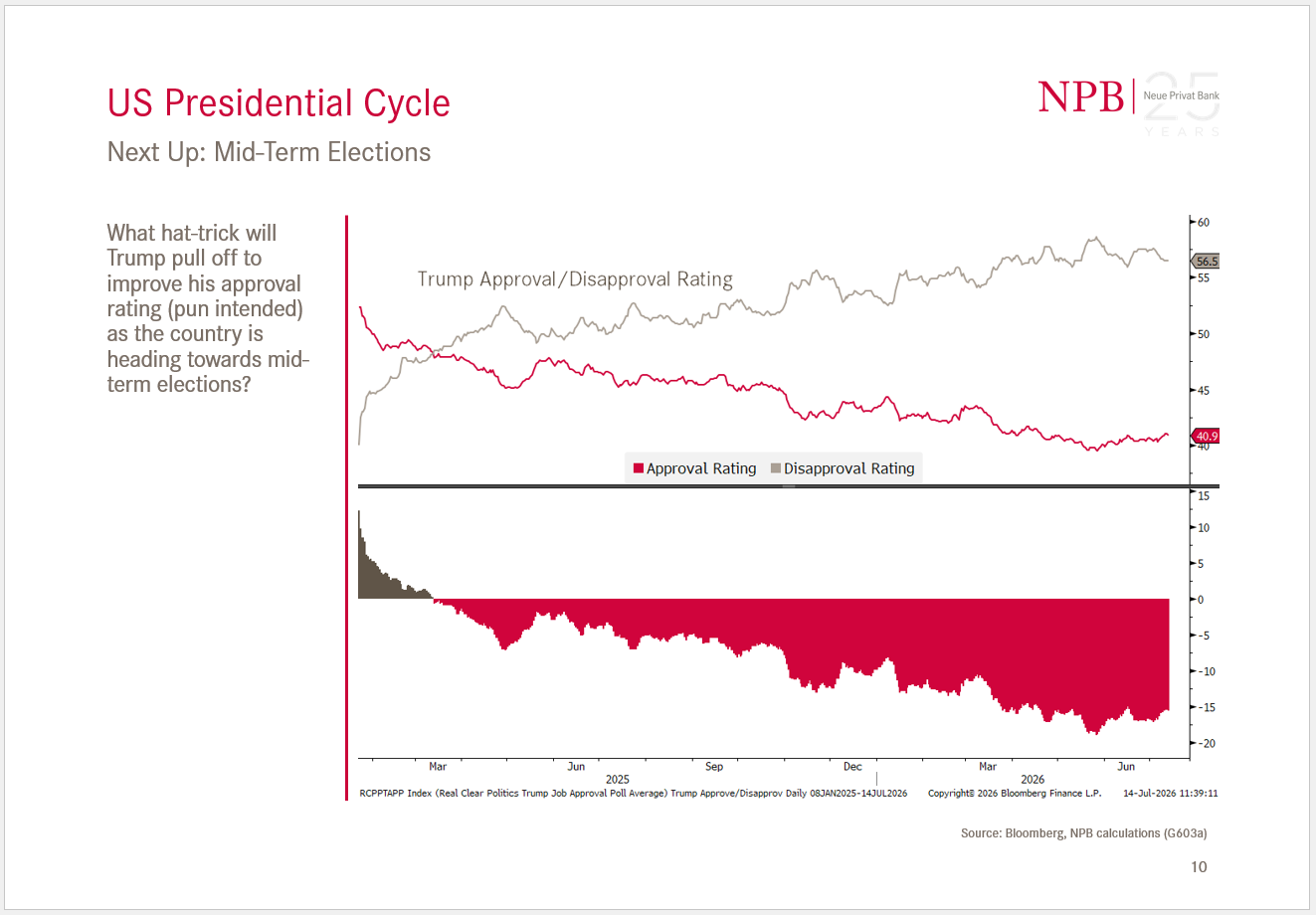

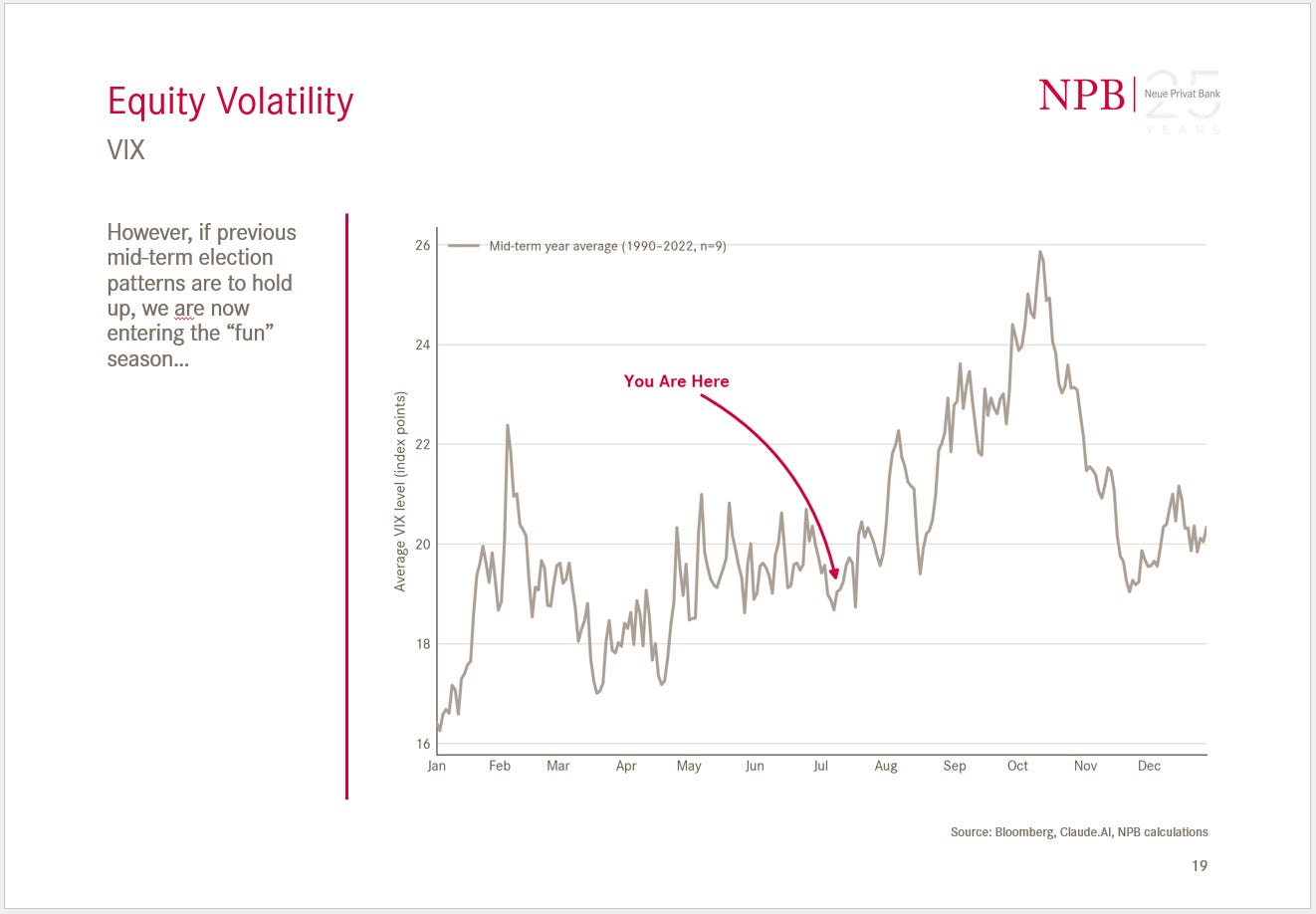

As is the upcoming US midterm election:

where the ‘hot’ season is about to start:

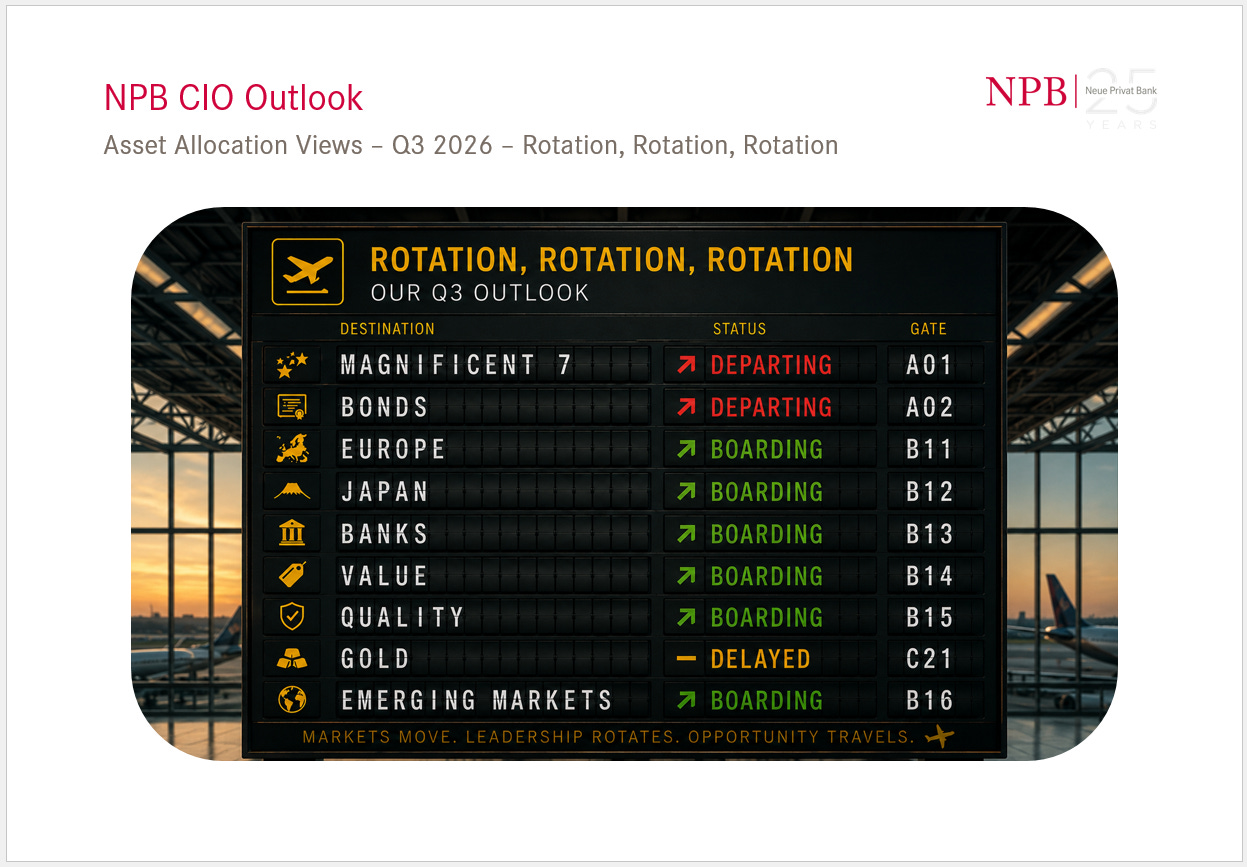

The main theme, also used as ‘hook’ for the entire Q3 Outlook, is an expected rotation taking place amongst asset classes but especially amongst equities:

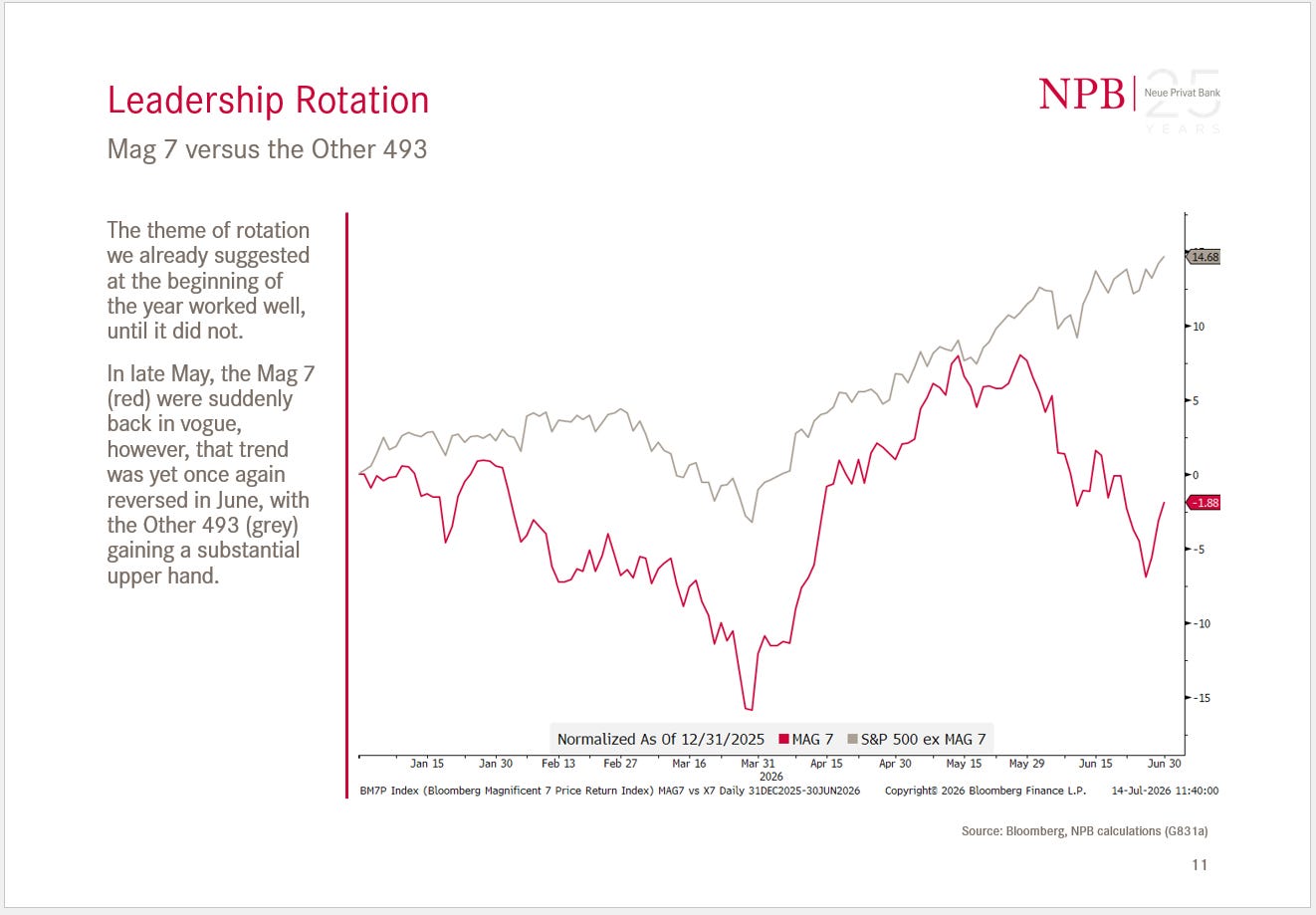

One rotation we have been observing for example is the one from ‘The Mag 7’ into ‘The other 493’:

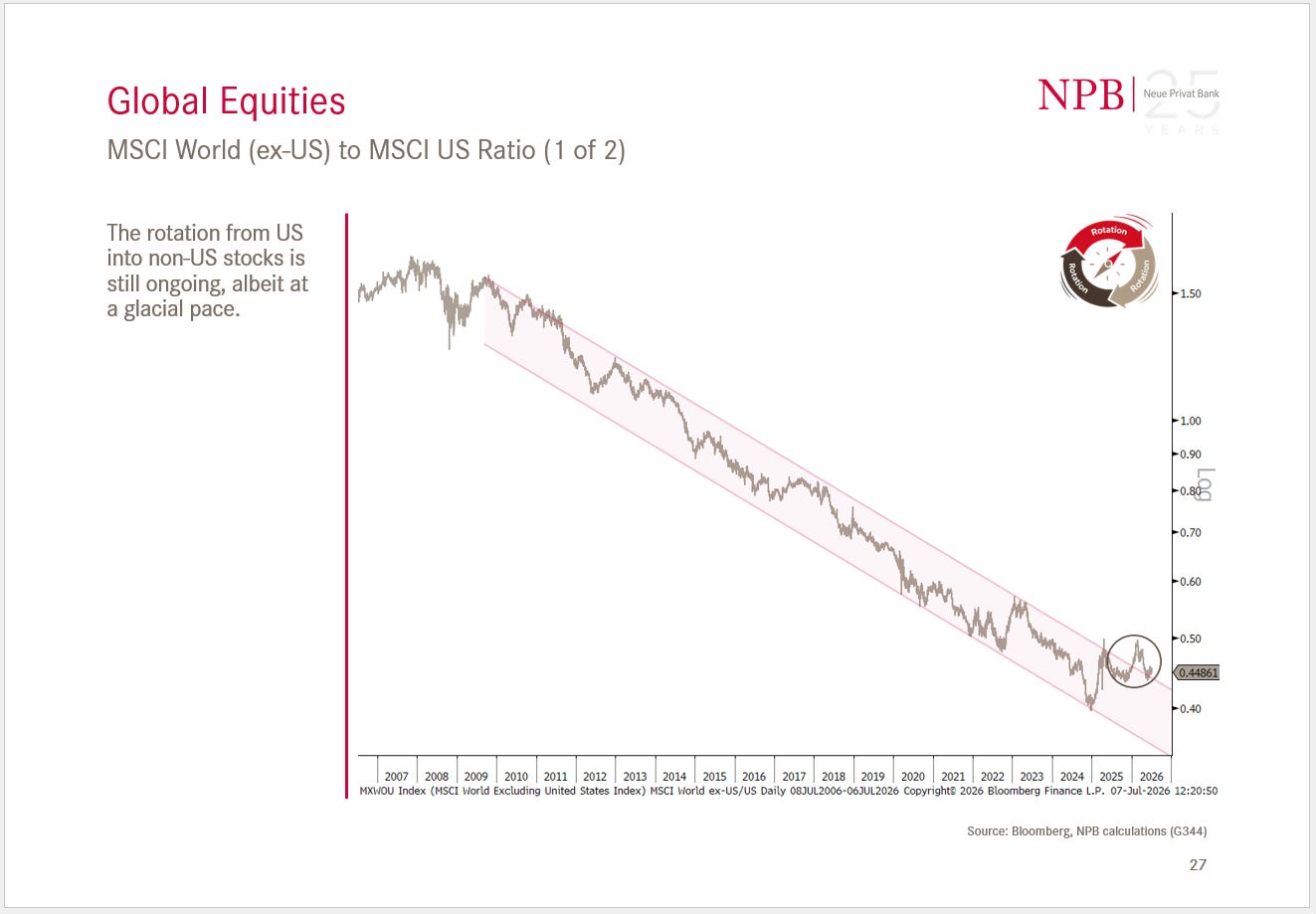

Other areas we are observing for possible further rotation is for example the one from US to Rest of the World stocks:

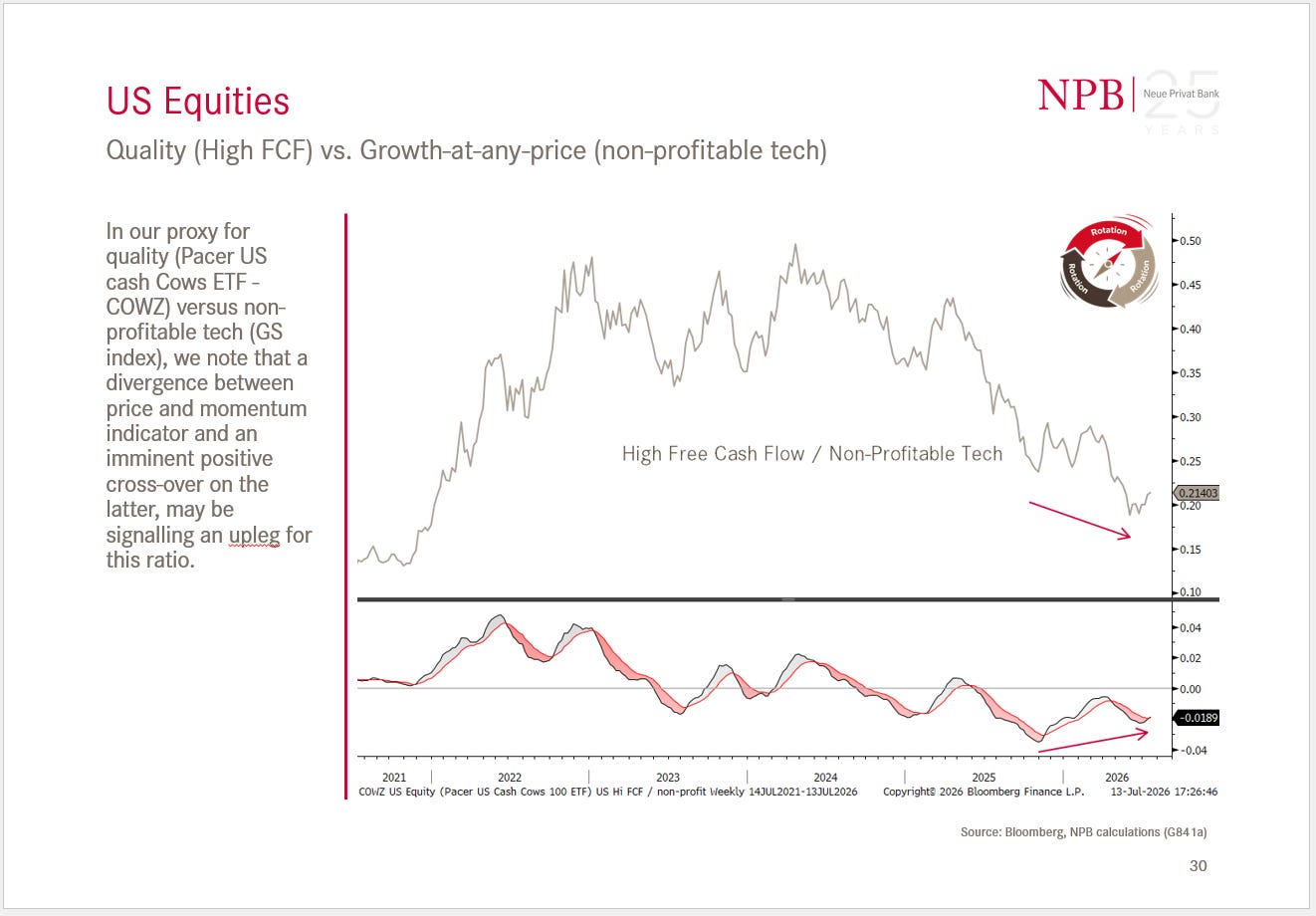

Or, the possible rotation from high-growth, non-profitable tech stocks into safer, high-free cash flow producing companies:

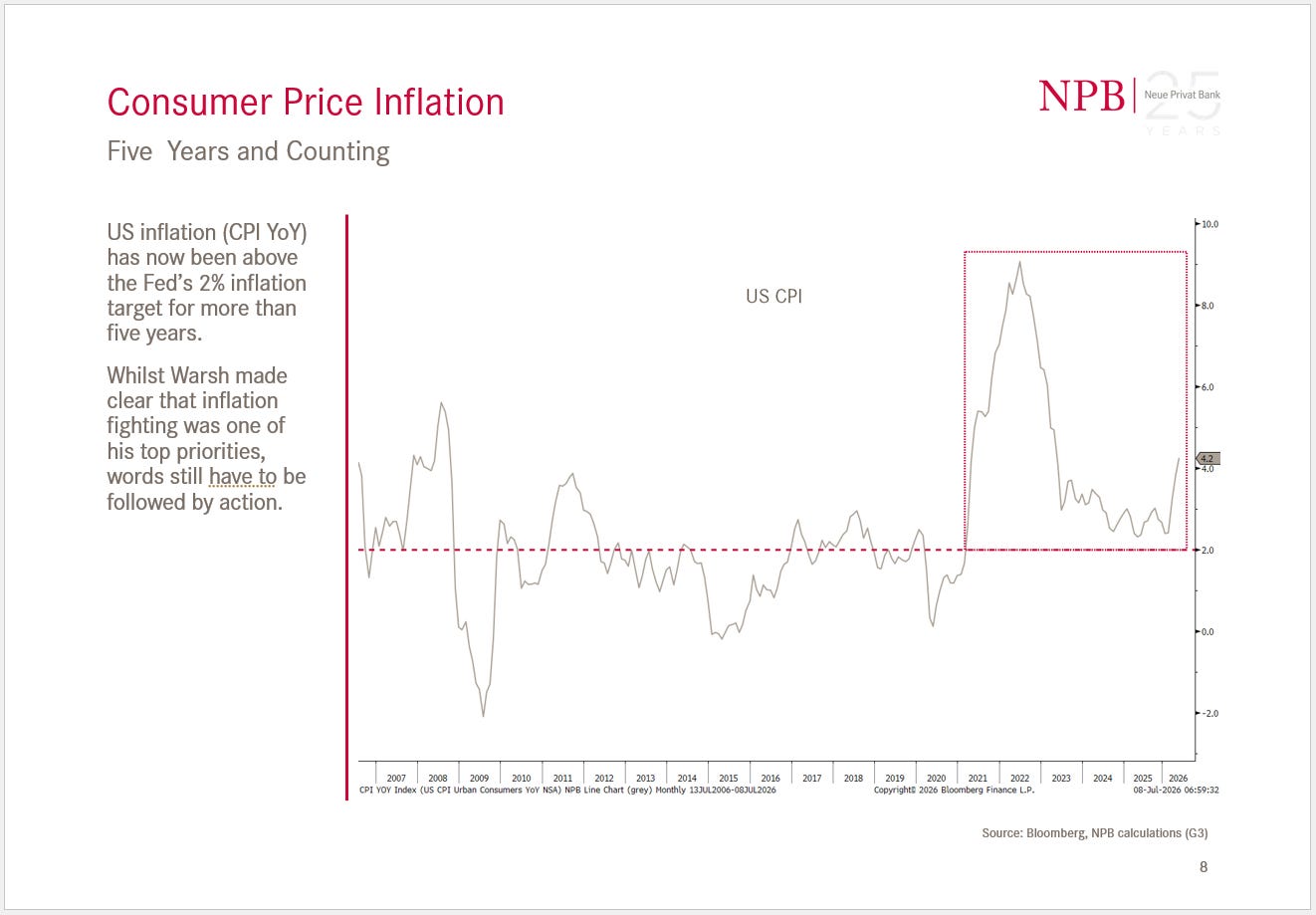

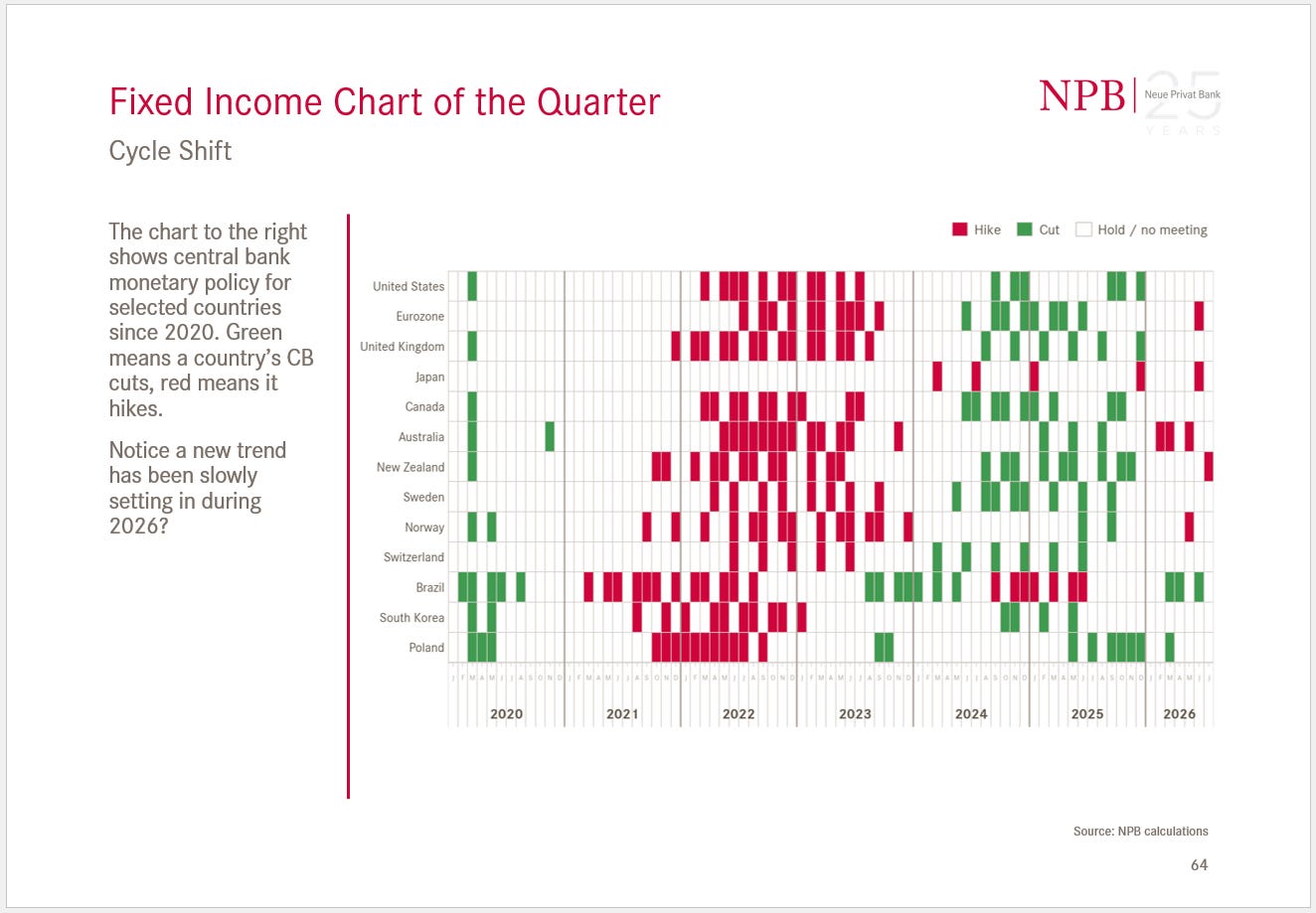

In the fixed income space, we note that the Fed has been allowing CPI to run above its own two percent target for nearly six years now:

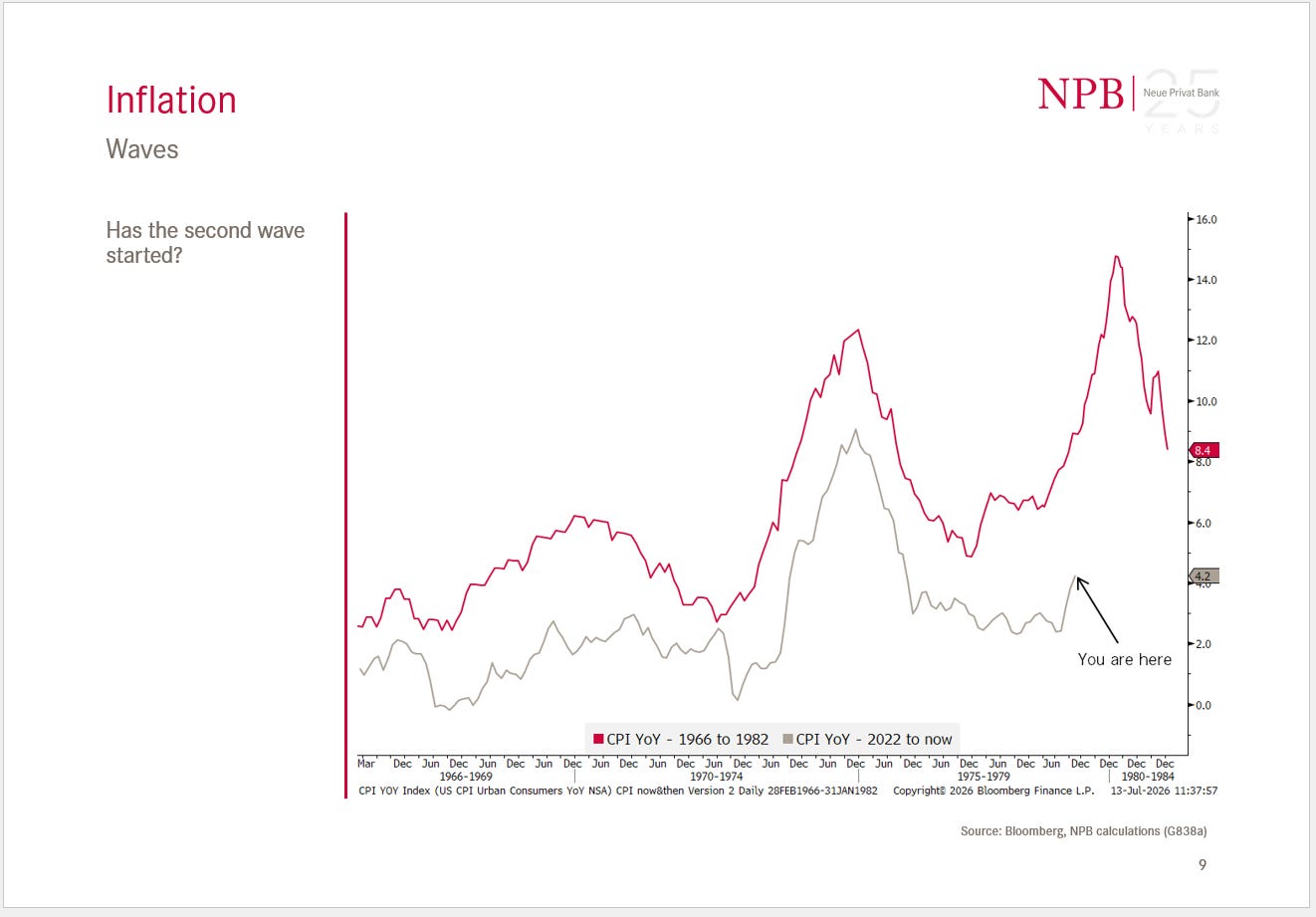

And the danger of a second inflationary wave being clear and present (despite yesterday’s lower-than-expected reading):

Newly wed Fed president Warsh insists on his inflation-fighting message, which other countries seem to be already applying:

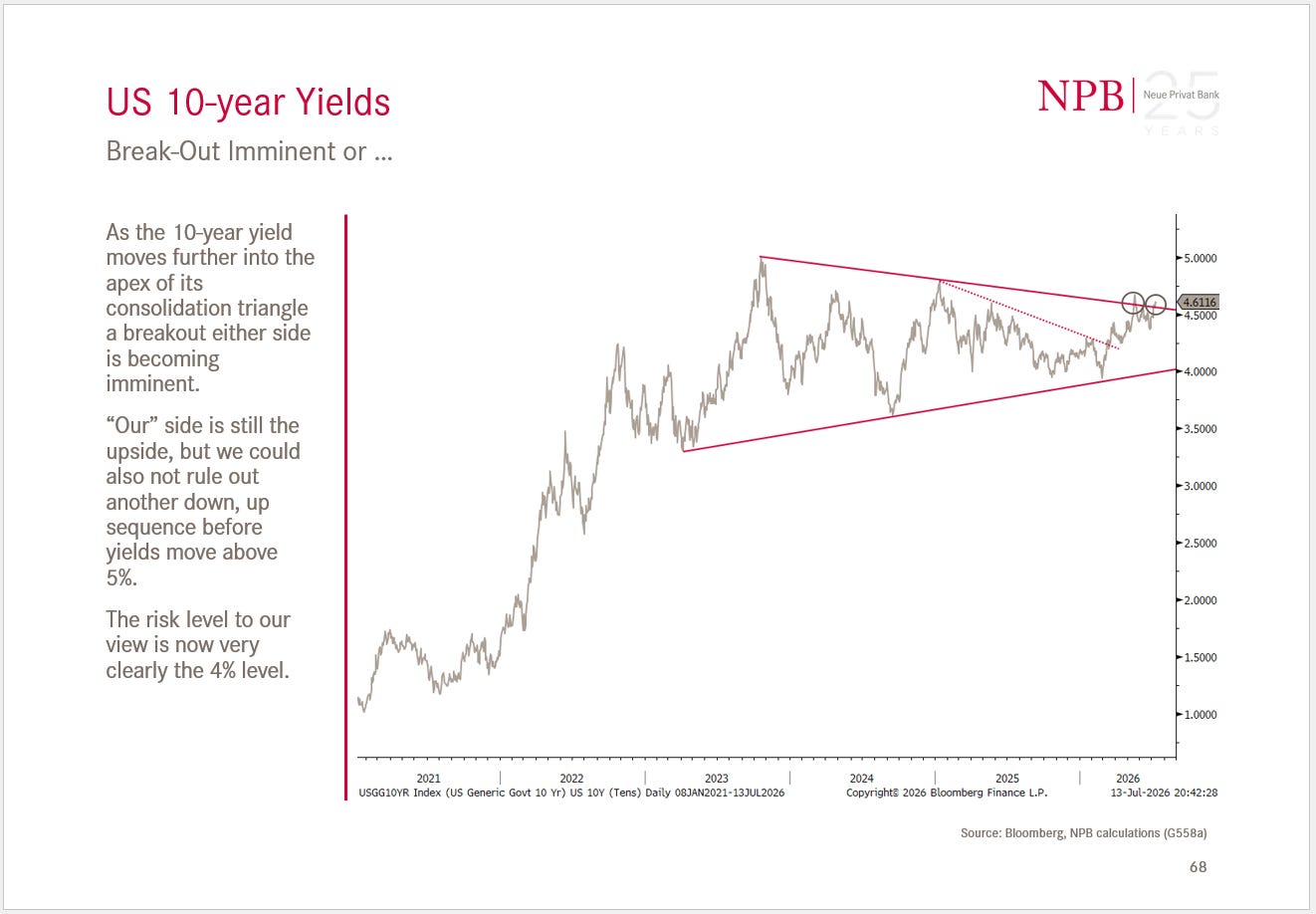

We further look at longer-term bond yields, noting that US 10-year Treasuries are pushing hard on the upper resistance level:

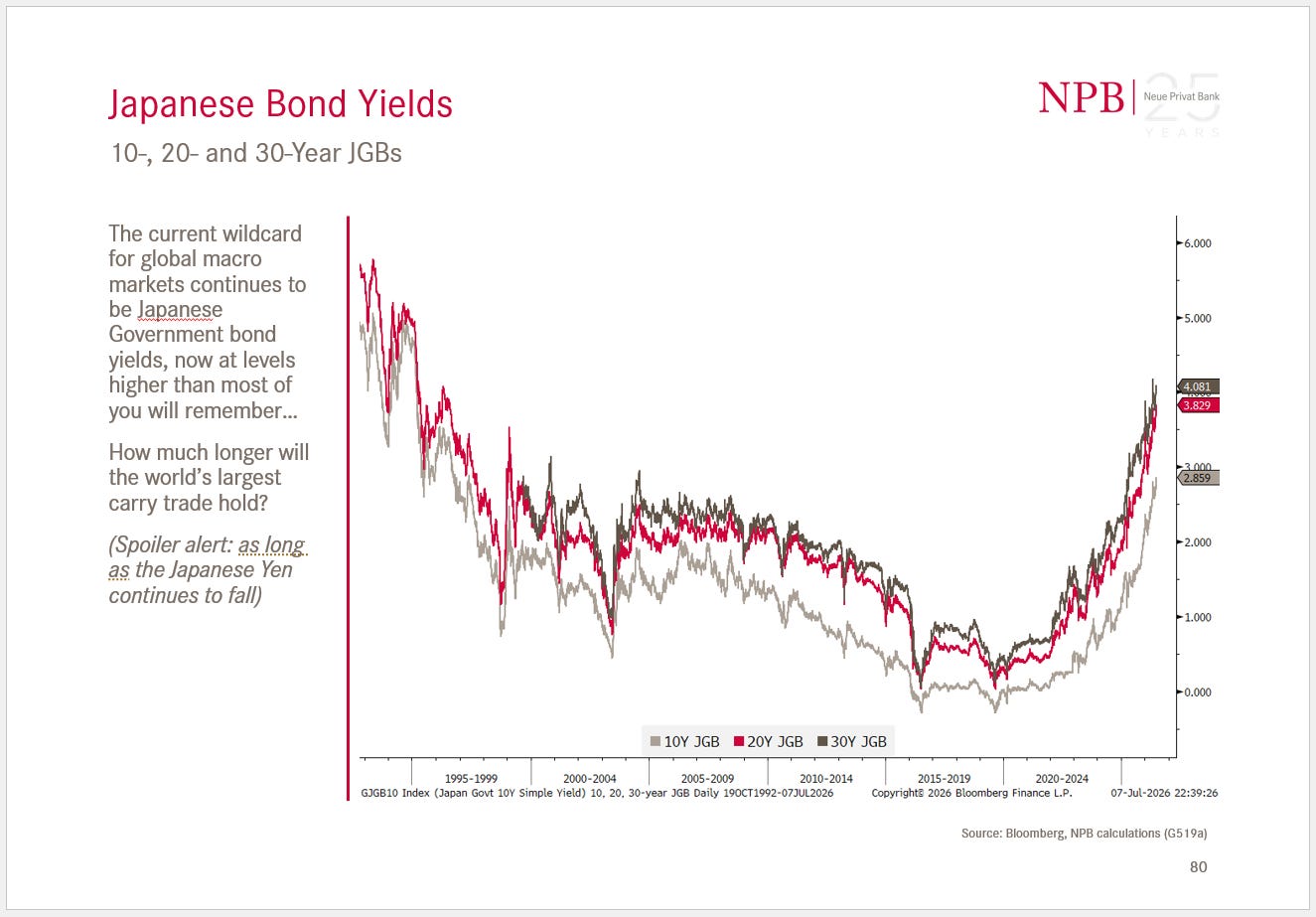

And then there are of course the JGBs …

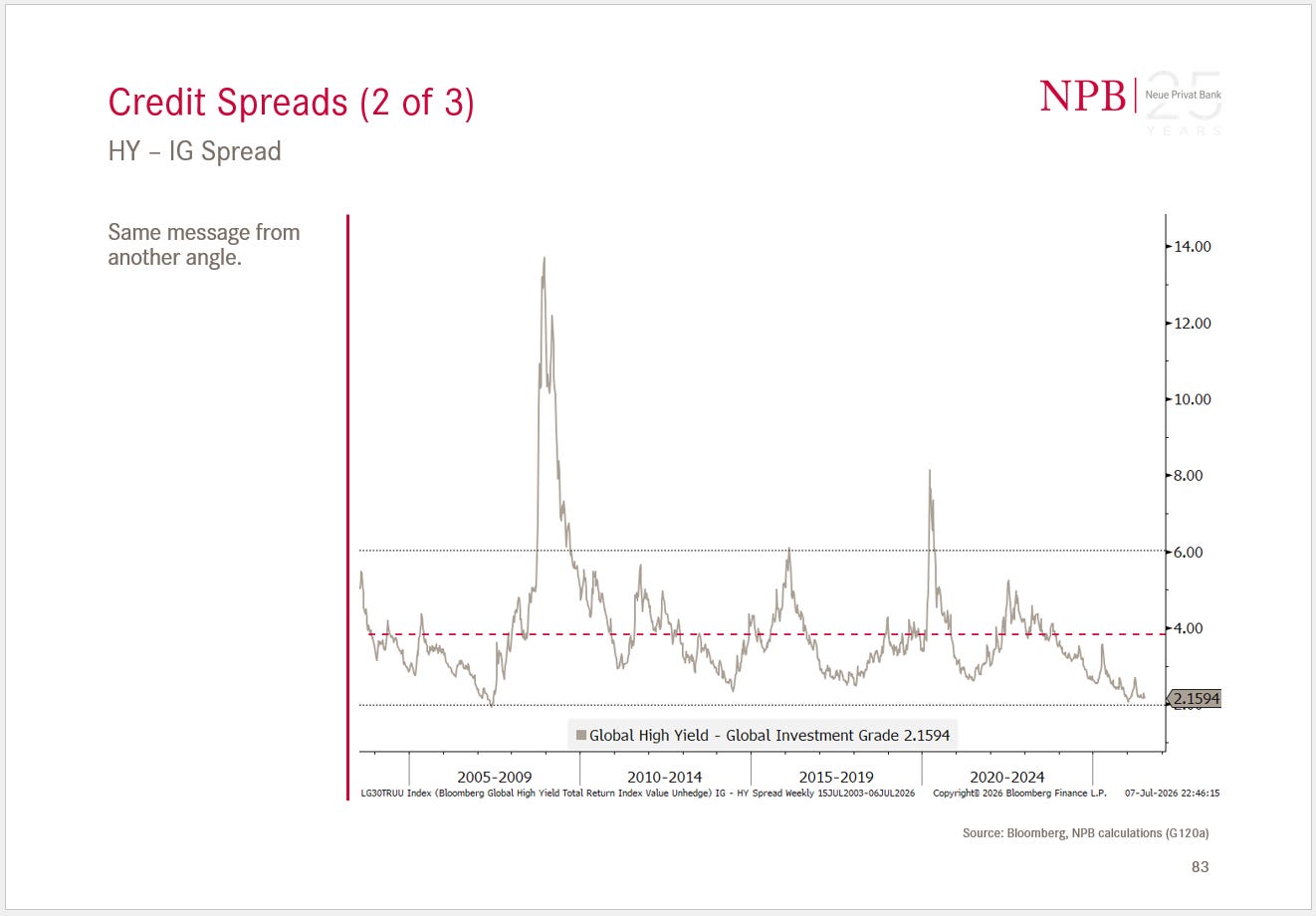

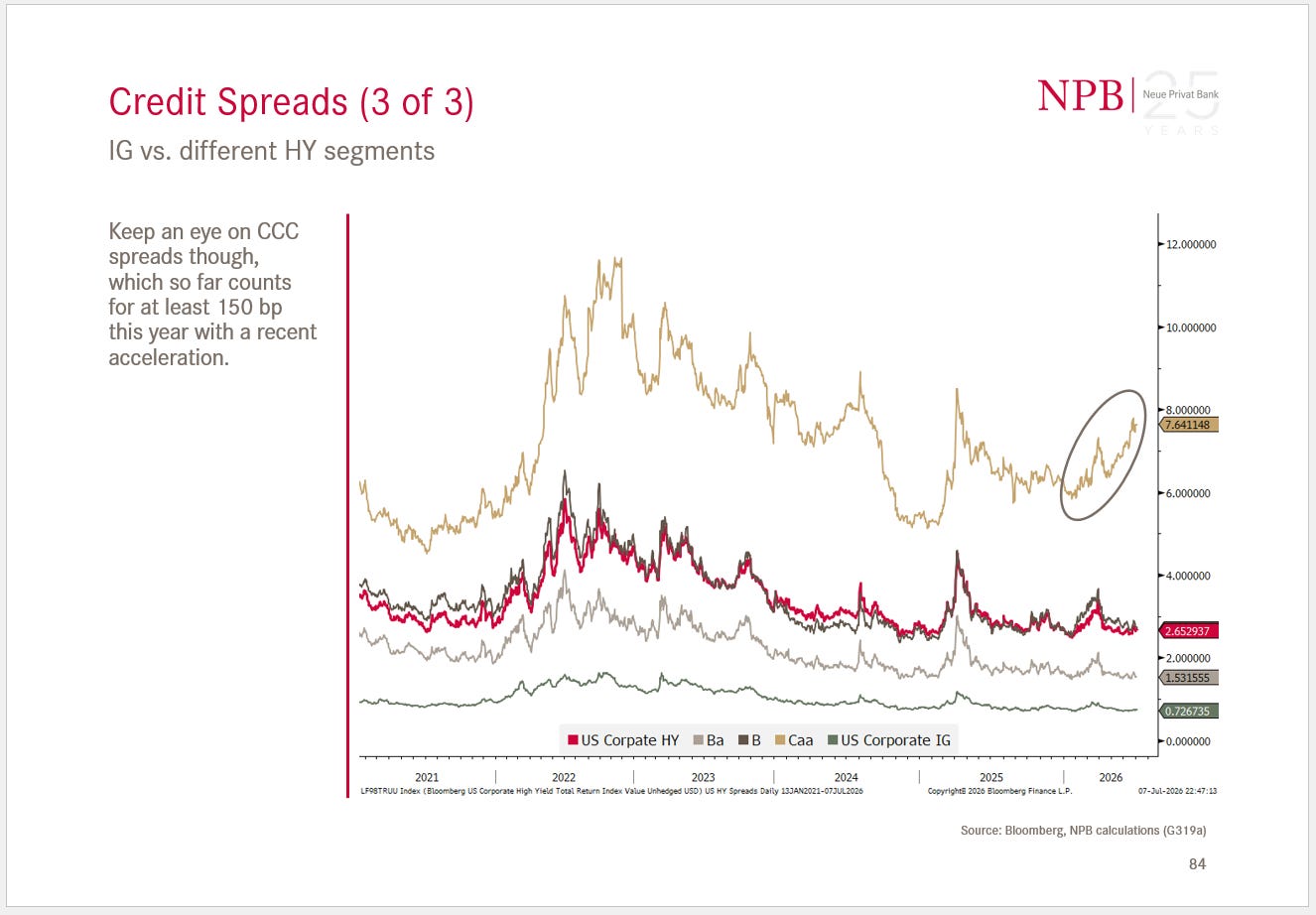

We highlight the tightness of credit spreads …

but also mark the widening of the CCC-segment as “to be observed”:

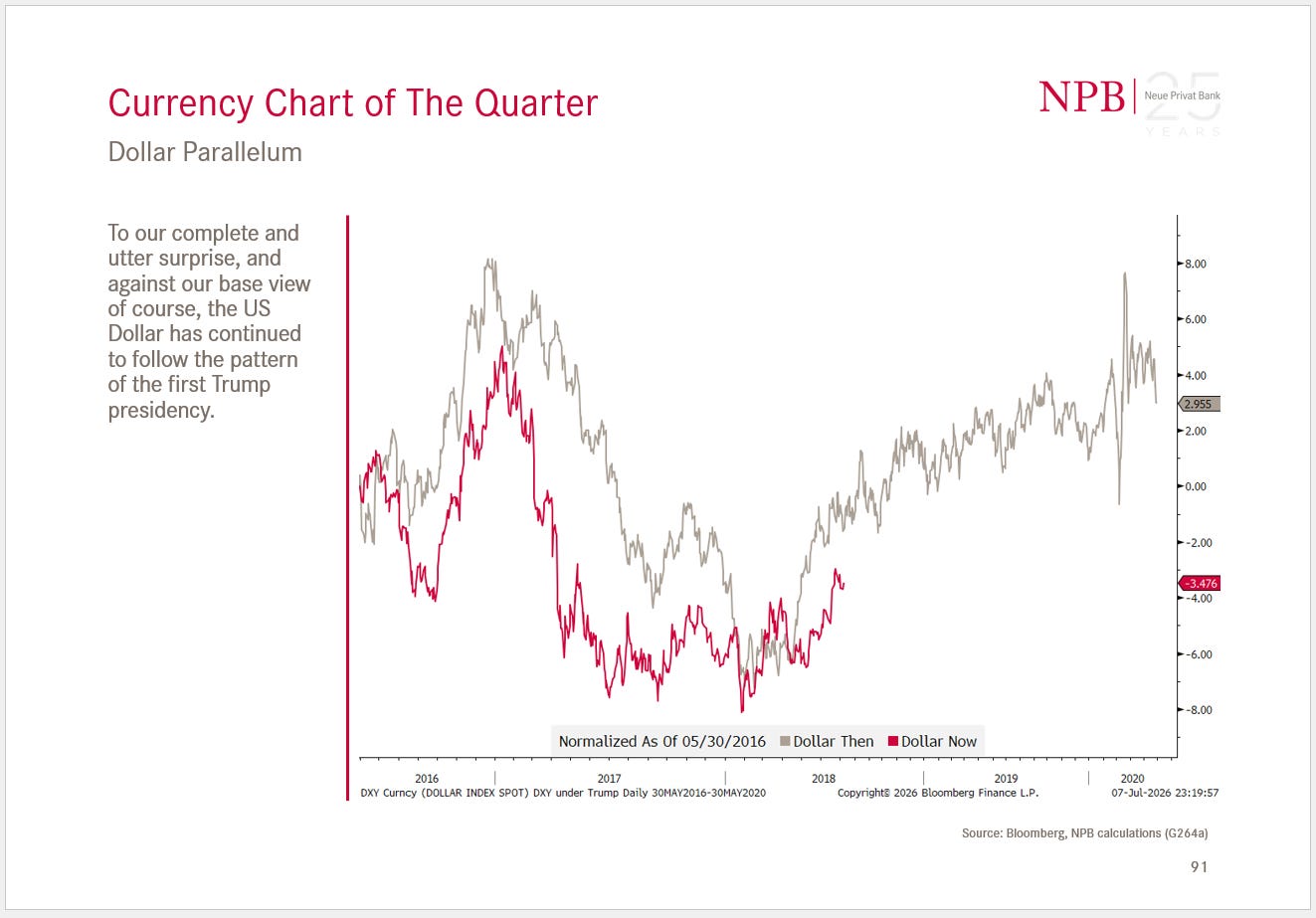

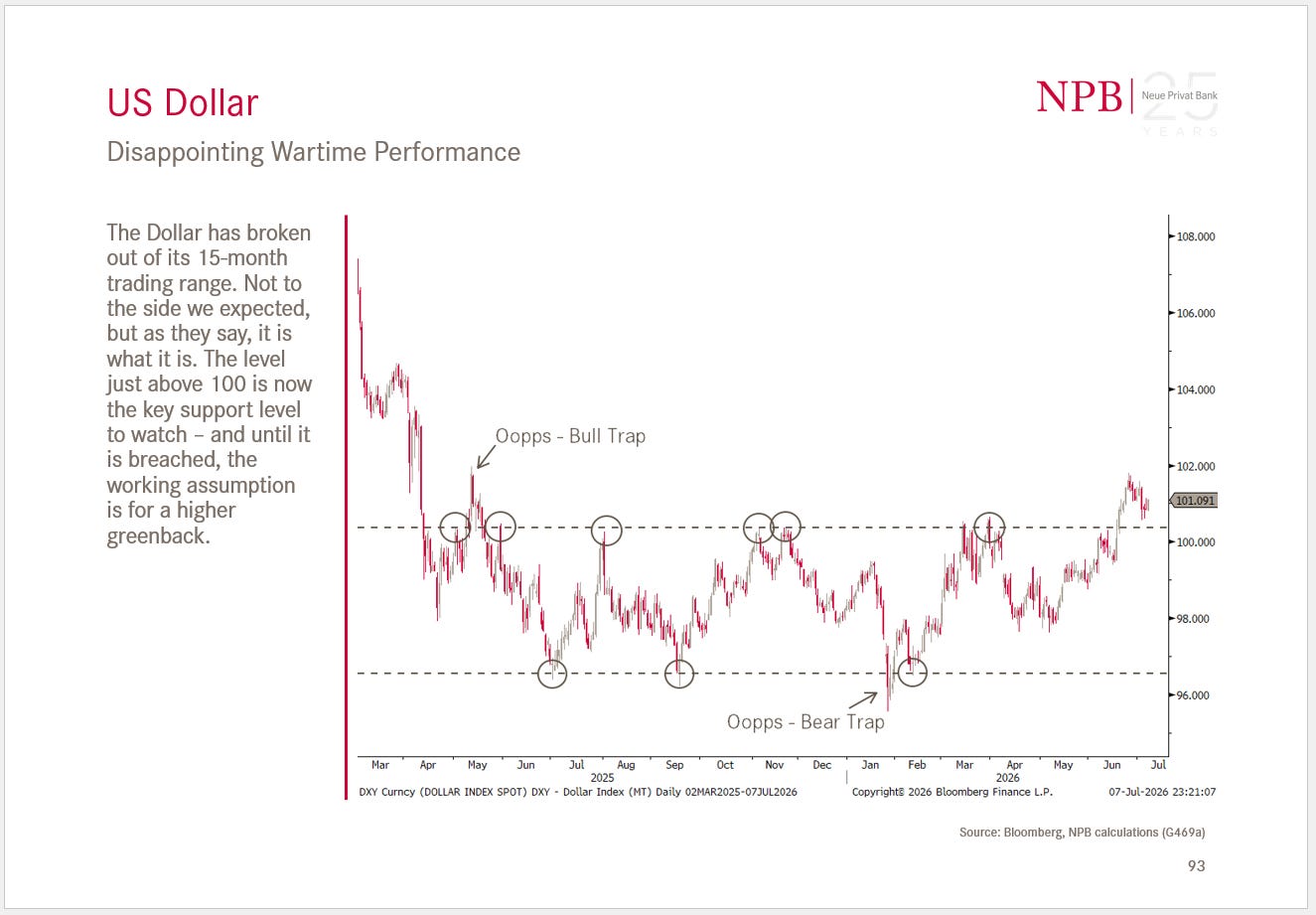

In the magic realm of currency markets we cannot stop being stunned about the US Dollar correlation between Trump’s first He(grey) and his second term (red):

Hence, we had to admit that our negative outlook for the US Dollar is wrong has been paused:

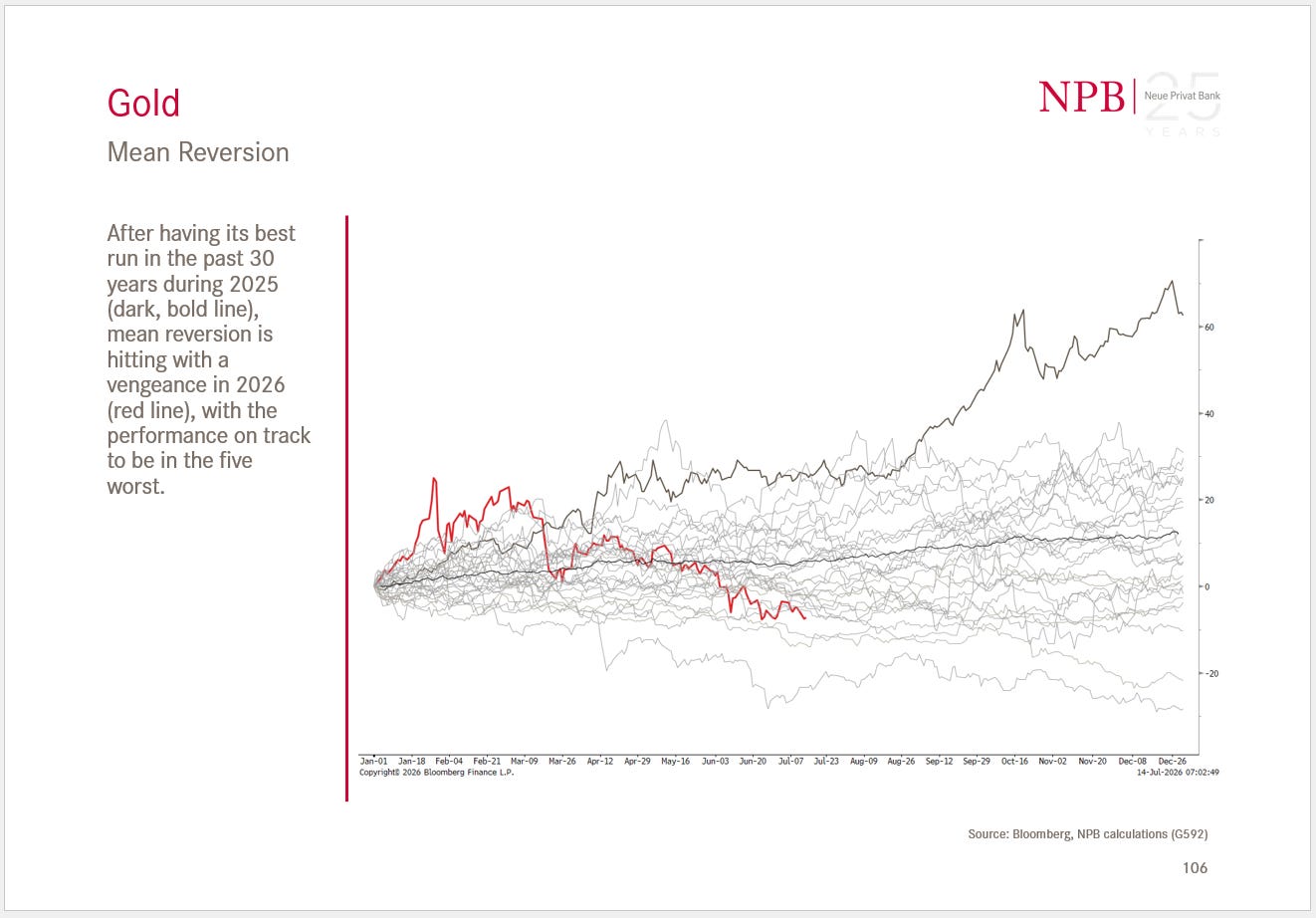

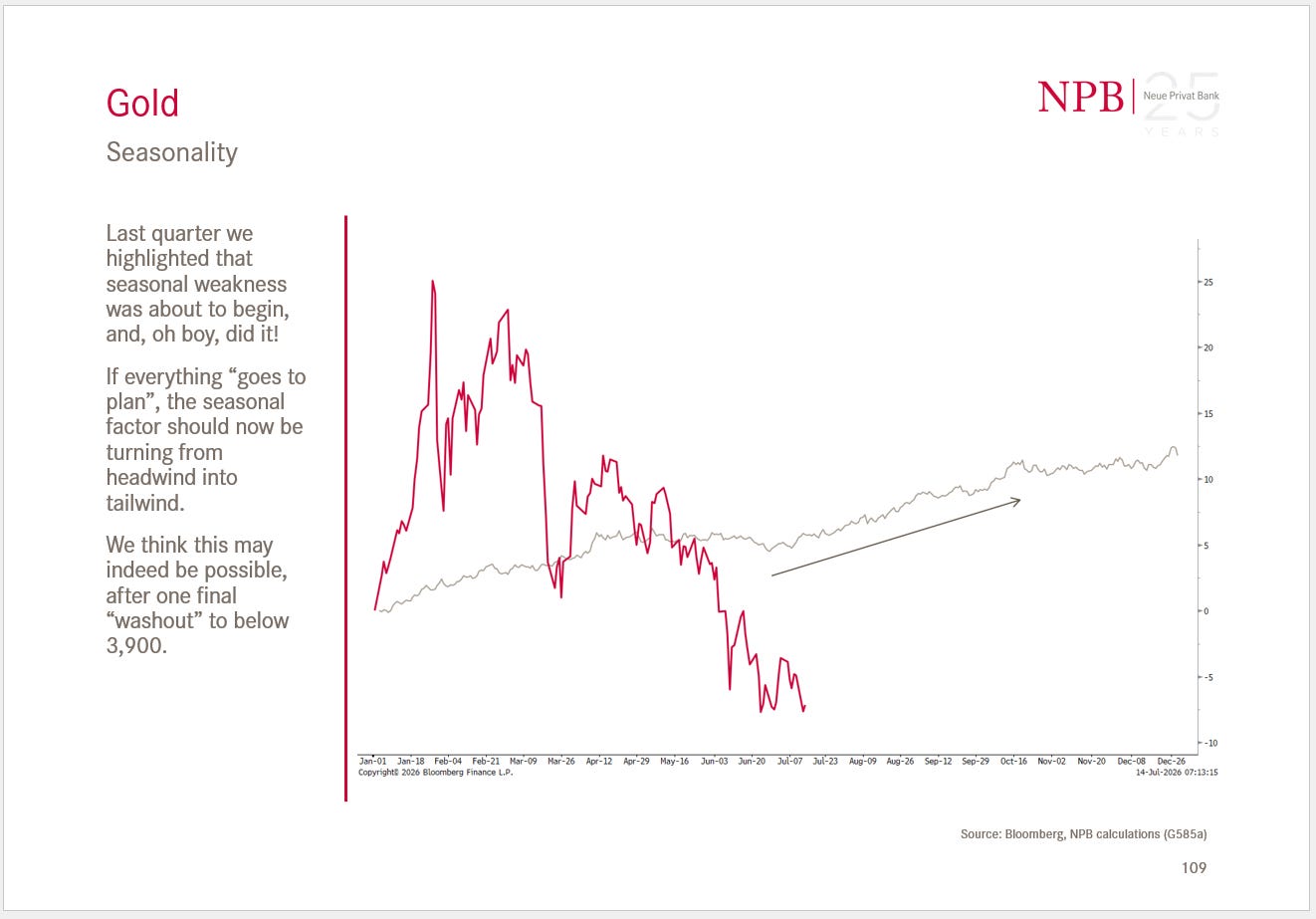

And finally, in the commodity section, we discuss the bursting of the gold bubble,

but also how seasonal tailwinds may lead to a short- to medium-term recovery rally:

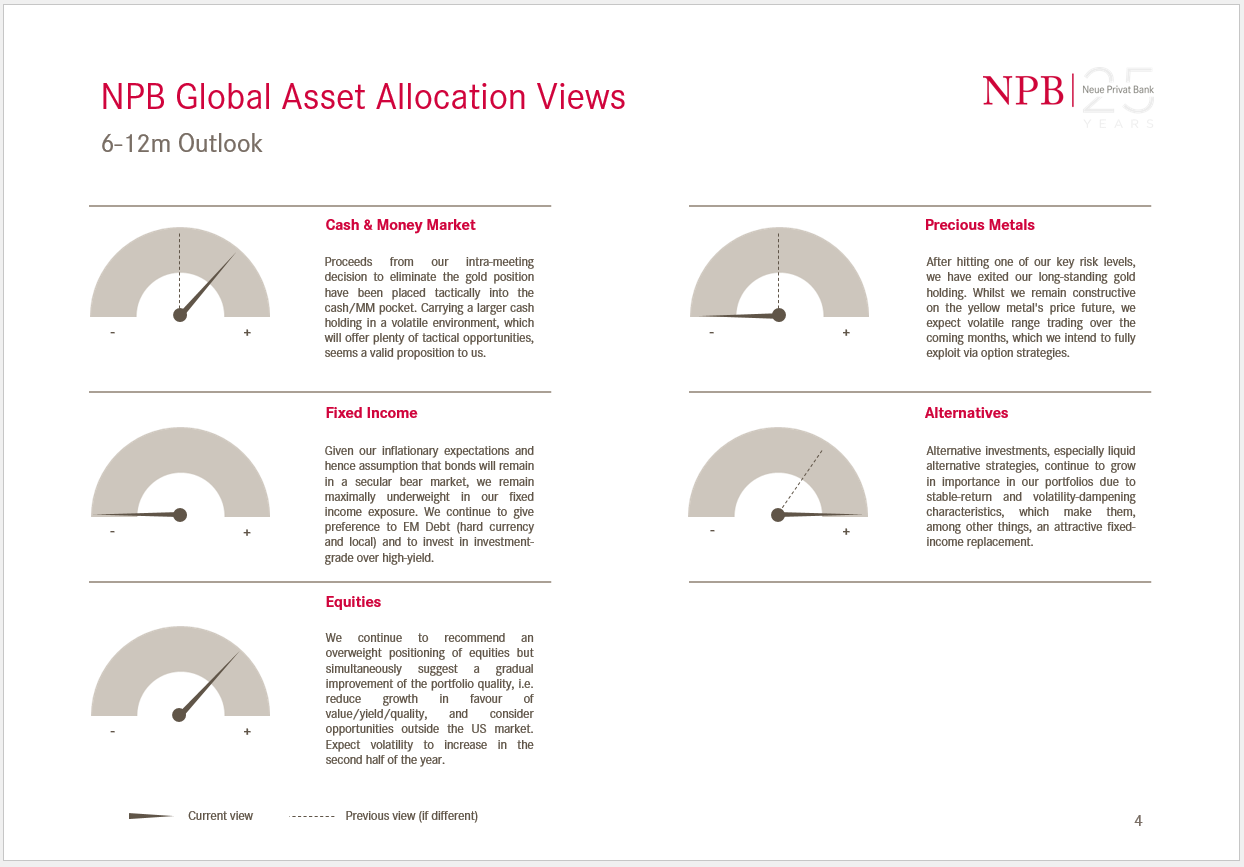

What better way then to present you with the (top-level) asset allocation decisions to square the circle?

So, as they say: “That’s all folks!”. Make sure to enjoy your summer, make sure to keep updated via our sister-publication The Quotedian - Daily Edition (aka QuiCQ) but above all:

Make sure that the trend will be with you!

André

“Time you enjoy wasting is not wasted time.”

— Marthe Troly-Curtin,

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG