T.G.I.F.F.

The Quotedian - Vol V, Issue 95

“I have experienced failure as a politician and for that very reason, I am ready to give everything for Japan.”

— Shinzo Abe

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

Is it just me or are you also thinking T.G.I.F.F.? In reality, markets gave us some kind of breather this week, with (US) stocks up for a fourth consecutive day yesterday. But so many moving pieces continue to keep us constantly on our toes. No wonder daughter number #2 eventually gave up on ballet…

As mentioned and observable in the Dashboard, global stocks had a strong up day yesterday, and the bottom-building that started mid-June is slowly morphing into one of the dreaded bear market rallies, with the potential of sucking everybody back in on the long side just at the wrong time. The S&P 500 needs only to close eight point or so higher to put a pattern of higher highs and higher lows into place:

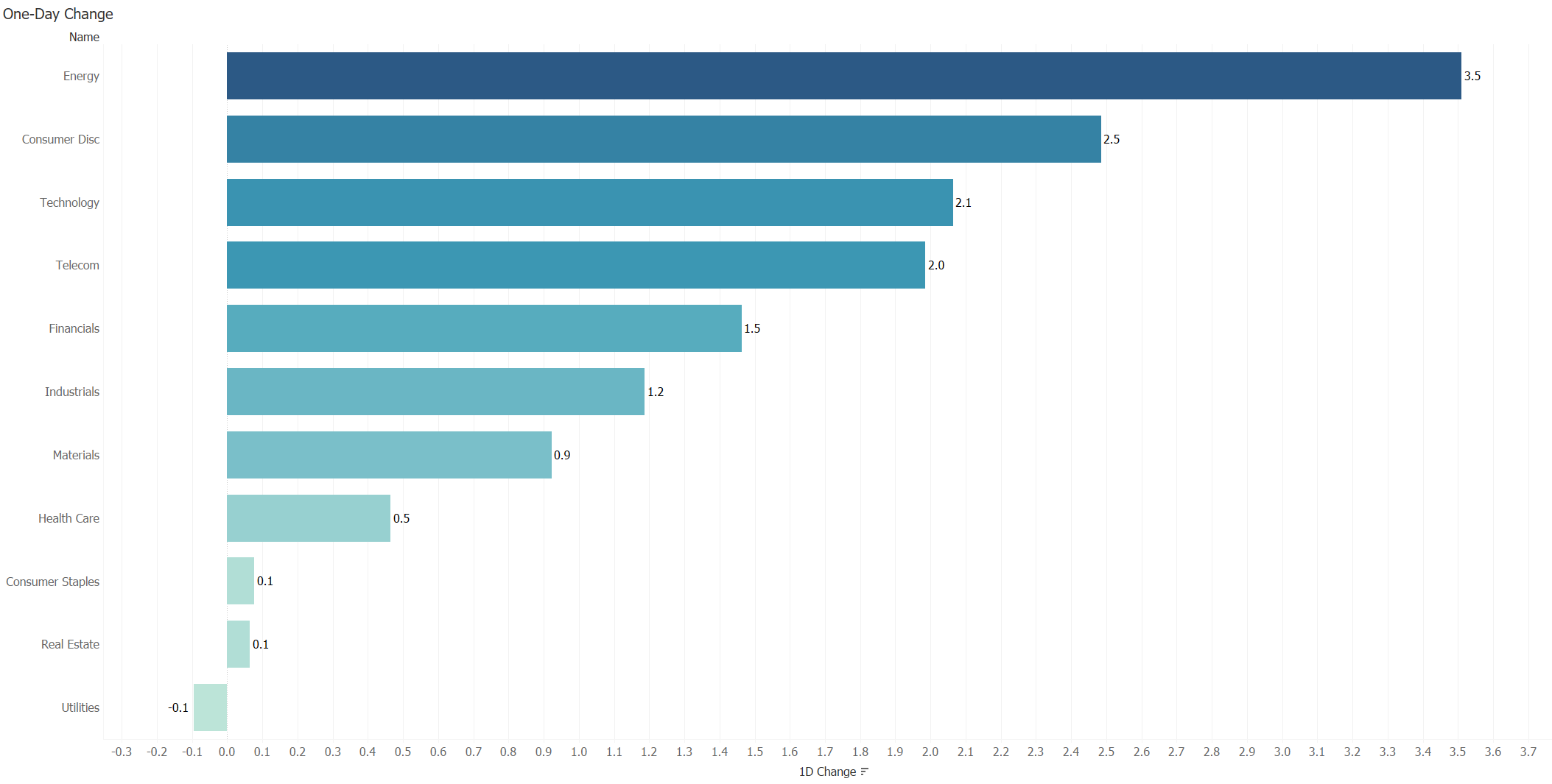

Breadth was broad with four stocks up for every stock down and in terms of sector performance, bar Utility stocks, all sectors ended the day higher:

Semiconductor stocks were up four and a half per cent as measured by the Philadelphia Semiconductor Index (aka SOX ), after Samsung’s earnings surprised to the upside:

European stocks also bounced, and looking at the monthly chart, they are bouncing right about at a crucial level:

Staying in Europe for a moment, please allow me to insert a (for this space) atypical corporate observation:

This week the French government announced that it was nationalizing EDF (Electricite de France), buying out public shareholders at EUR9.00 per share. After having sold the company to the same public shareholders in 2005 at EUR32.00:

This is how France’s EDF adventure compares over the period where the company was available to the public to the CAC-40 and the MSCI World:

As if not bad enough, consider this: EDF is one of the global leaders in nuclear energy; arguably the cleanest, most efficient source of energy available nowadays. As the formidable Louis Gave at Gavekal put it in a recent note (paraphrasing):

“Putting it all together, it is not surprising (…) but it is depressing, for it illustrates it illustrates the predicament of large companies (…) because of decades of terrible policies. Moreover, EDF’s nationalization is a reminder to investors that the victims of the unfolding energy crisis are only just starting to emerge.

Anyway, not sure where this rant came from, let’s continue with market observations…

Asian markets are flashing green this morning, though the Nikkei in Japan gave back most of its early gains after news broke that the country’s ex-Prime Minister Shinzo Abe had been shot in the chest during a campaign speech.

European index futures are flat, whilst their US counterparts are printing a small red though as I type.

Bonds were under pressure yesterday, as yields continued to climb again, with the US 10-year yield for example briefly moving above the three per cent handle again:

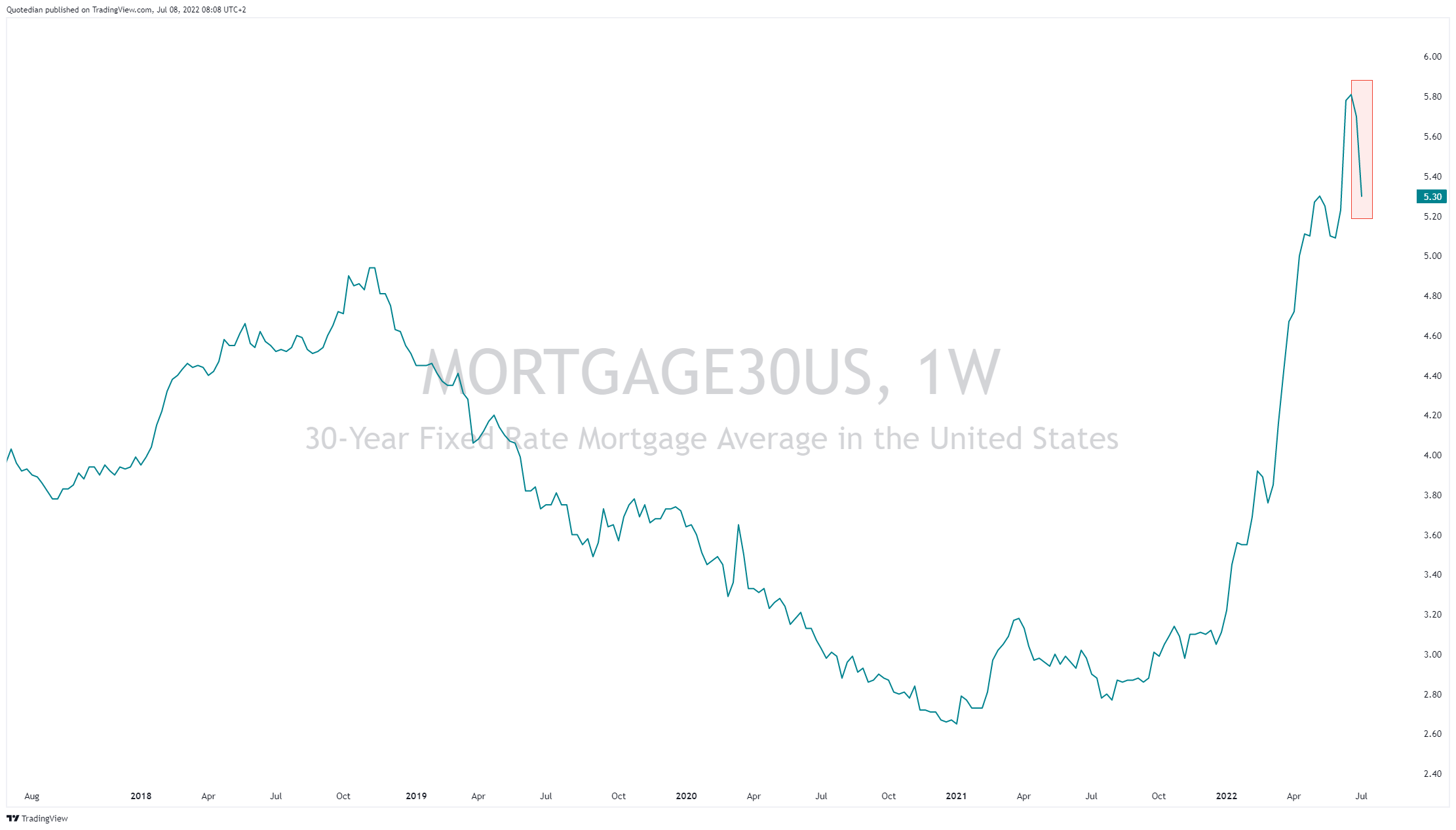

One more noteworthy observation from yesterday, is the steep correction in the 30-year mortgage rate (US):

That could provide some relief to the embattled homebuilders:

Let’s move on into currency, where the British Pound was of some focus yesterday, as Boris Johnson finally gave in - kind of … Anyway, the GBP jumped, though more so versus the Euro than versus the USD:

With the Euro of course suffering its own on the path the parity versus the USD:

Finally, in the commodity complex Gold got hammered over the past two sessions (basically since I mentioned how remarkably it had held up … Doh!). I think the current levels are very interesting for a) either a direct entry or b) some put selling with a strike of 1,700 for example (though ‘yield’ is only about 10% p.a.):

Way over my quota (once again) already, let’s start wrapping up today’s Quotedian…

Two events will dominate the agenda today. For one, all (investors’) eyes will be on the release of the June non-farm payroll (NFP) number at 14:30 CET. Too good a number, stocks down and vice versa, but I am sure that the BLS (short for Bureau of Labour Statistics or alternative BuLlSh.t) will be able to bake the right number. Secondly, I could imagine that the G20 meeting of Foreign Ministers including Russia’s Lavrov could be, well, tense …

Bon week-end les amis!

CHART OF THE DAY

Market analogies are always amusing, though mostly they fail. But still, difficult not to relish the one comparing the 2000-2002 Dot.com bubble burst with the ARK innovation ETF burst of recent times:

If all goes to plan (ha ha ha), the current rebound has some leg, before the next “throwing in the towel”.

LIKES N’ UNLIKES

I have decided to replace the previously ad-hoc updated portfolio section, with a less implicit and more regular like/dislike section for two reasons:

It’s less implicit

It’s more regular

:-P

On with the likes/disliked, most of them of tactical nature (weeks to months):

China equity (FXI)

Biotech (XBI); trailing stop now at $66

Energy stocks (XLE); 1/2 of position size

** NEW ** Long some Gold (direct or via short puts)

India equity (PIN)

Agree with this new section? Then thanks for clicking the Like button towards the bottom of the mail. Prefer to leave a comment? Perfect:

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance