The Spice Must Flow

Vol IX, Issue 15 | Simplicity is the Ultimate Sophistication

“The Spice must flow.”

— The Spacing Guild, Dune Universe

In Frank Herbert’s 1965 sci-fi classic Dune, the entire galactic empire runs on a single substance: a spice called melange, found on exactly one desert planet, Arrakis. The spice lets the Guild Navigators fold space and travel between stars. No spice, no travel. No travel, no trade. No trade, no empire. Hence the book’s most quoted line, repeated like a mantra by everyone from emperors to smugglers: “The spice must flow.”

Now squint a little. Replace Arrakis with the Persian Gulf, melange with crude and LNG, and the Spacing Guild’s monopoly with a 21-mile-wide strait flanked by a bruised and bothered Iran — and welcome to 2026. Roughly a fifth of the world’s oil and a quarter of seaborne LNG squeeze through the Strait of Hormuz every single day. Close it, choke it, or merely threaten it, and the cascade is brutal: energy → nitrogen fertilizer (no natural gas, no Haber-Bosch) → food. As we’ve been banging the drum in these pages: you can’t print molecules. And you certainly can’t reroute them around a closed chokepoint with a press release.

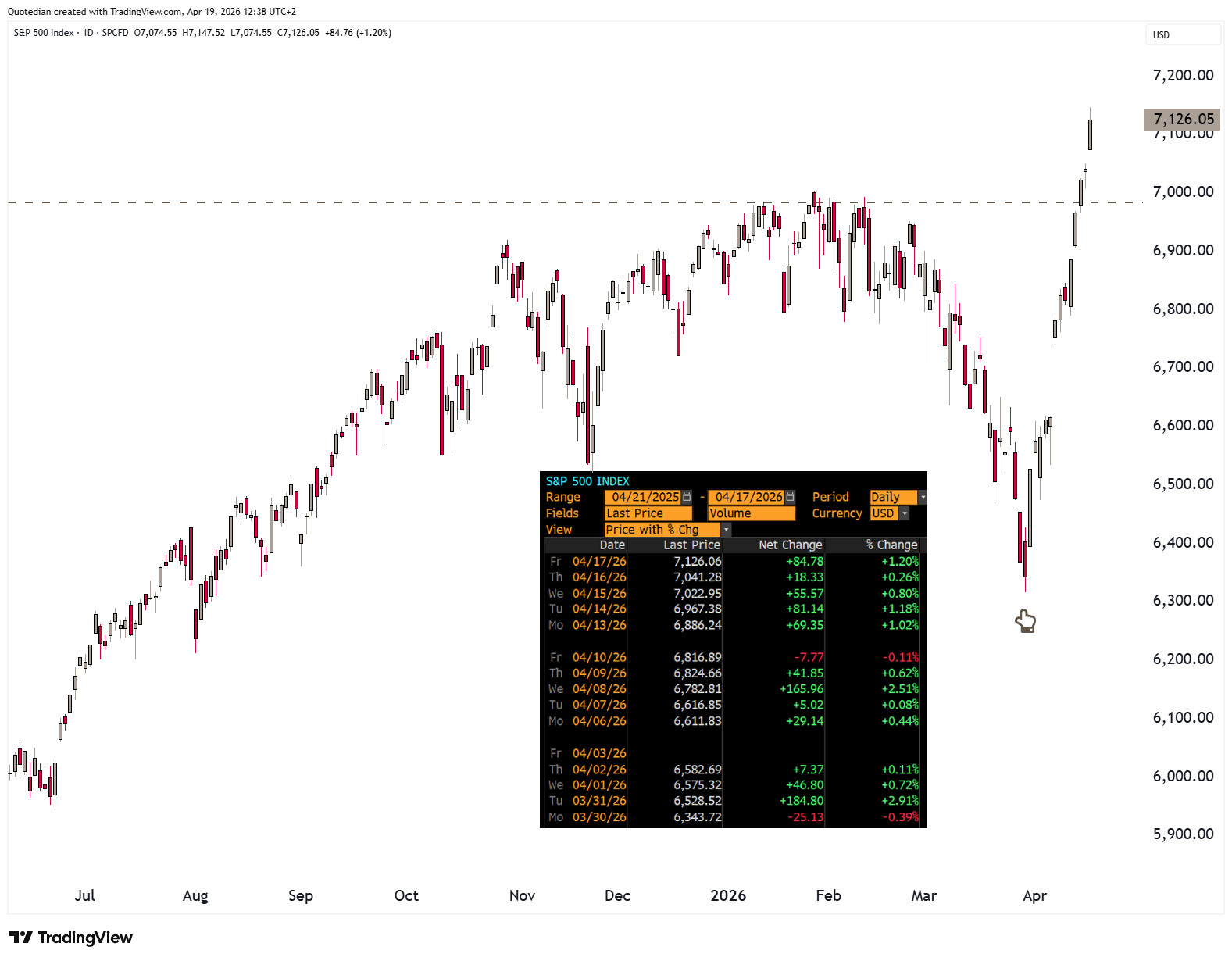

News on Friday that the SoH is fully open again,

made markets continue their mad hatter rally of the past two weeks. But between having some doubt about the quality of the rally and new headlines flowing over the weekend, such as this

or this

can the rally continue from here.

Let’s have a look …

The S&P 500 bottomed on March 30, and really never looked back!

Whatever happened to “stocks take the stairsteps up, and the elevator down”. Quite the reverse is true on the above chart!

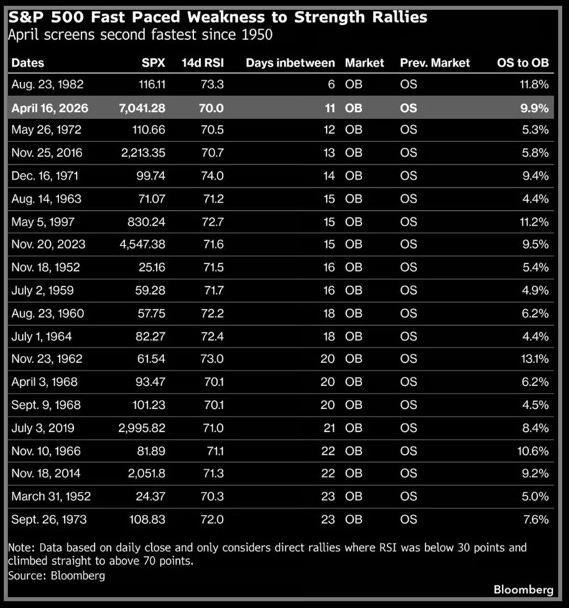

As a matter of fact, according to the following table from Bloomberg, this was the second fastest recovery (from RSI <30 oversold to RSI >70 overbought) since 1950:

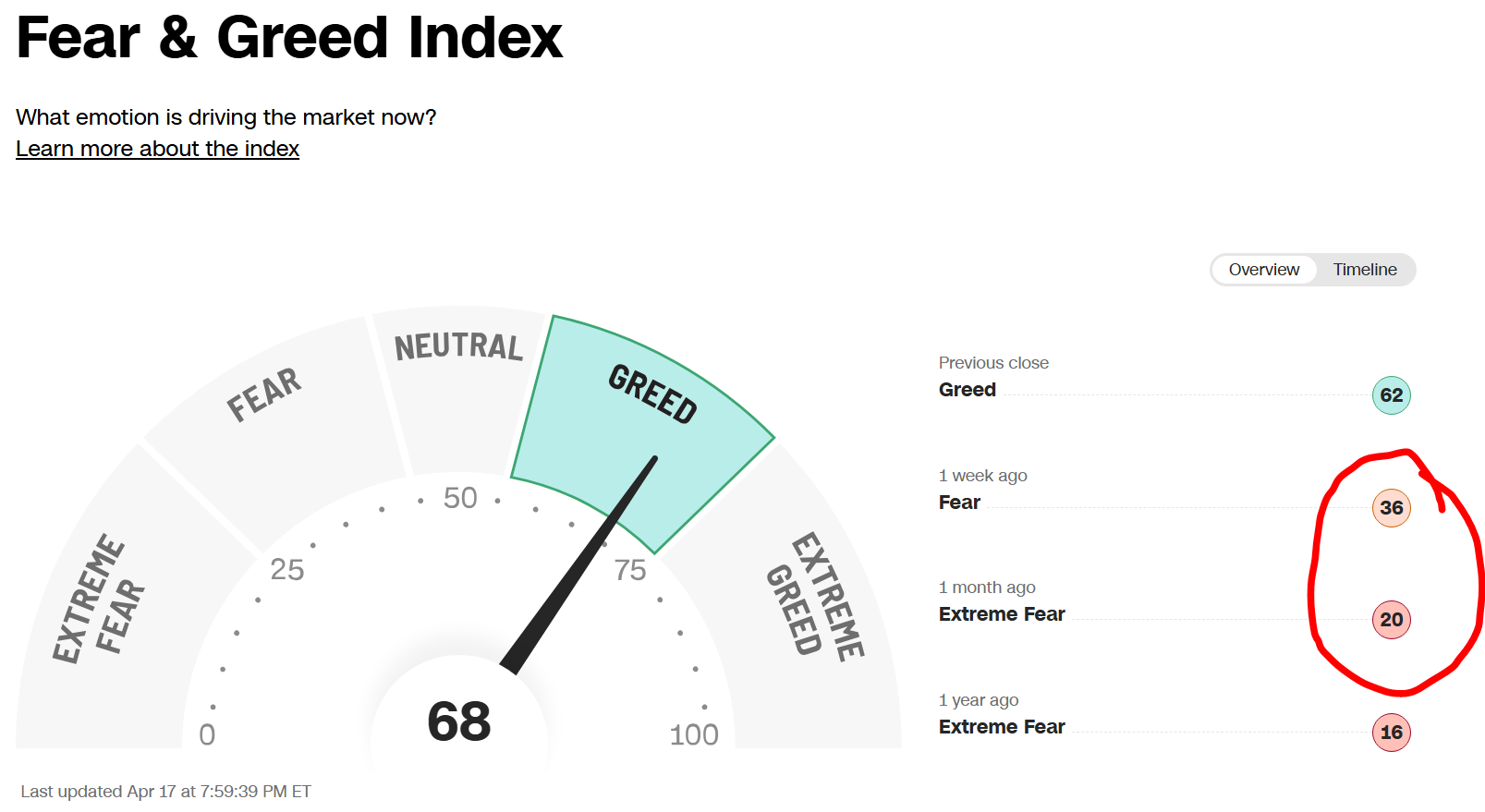

Similarly, CNN’s Greed and Fear indicator moved from Extreme Fear/Fear to Greed in a record short time:

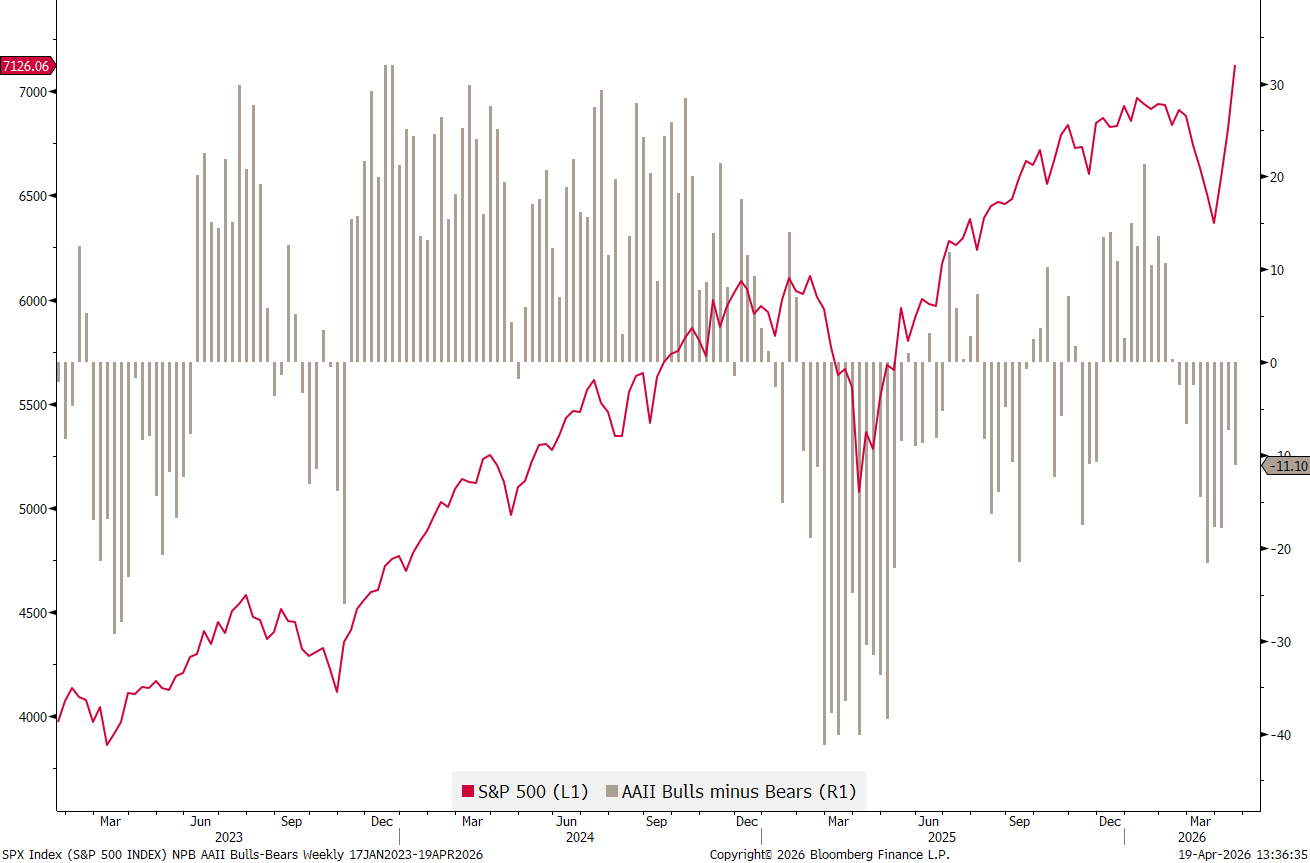

Albeit the AAII Bull/Bear survey was still in net negative territory last week, but given the strong rally on Thursday and Friday (the indicator is published on Thursday pre-market opening) it has probably also moved into net positive territory in the meantime:

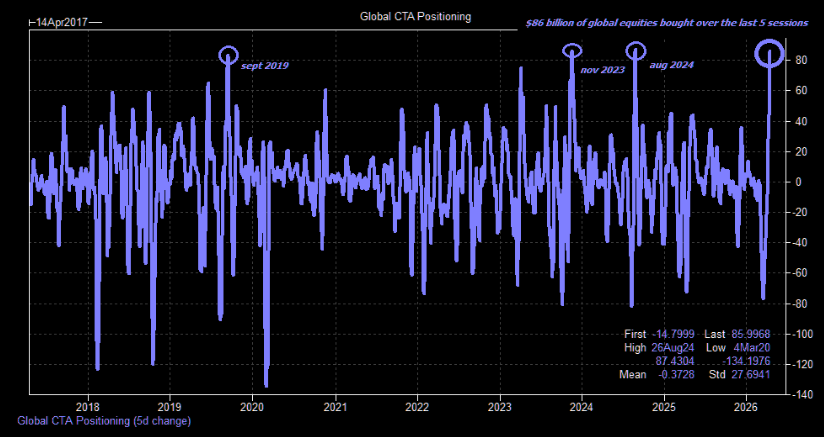

Clearly, a short squeeze has taken place, with CTA’s (trend followers) buying $86bn of global equities according to Goldman Sachs (GS), top 5 all-time!

GS models another ~$70bn of buying over the next 5 sessions (assuming a flat tape).

We increased equity exposure to our managed portfolios a few weeks ago, as economic-sensitive indices such as the Dow Jones Transportation index,

or the Philadelphia Semiconductor index,

hit new ATHs already on April 8th.

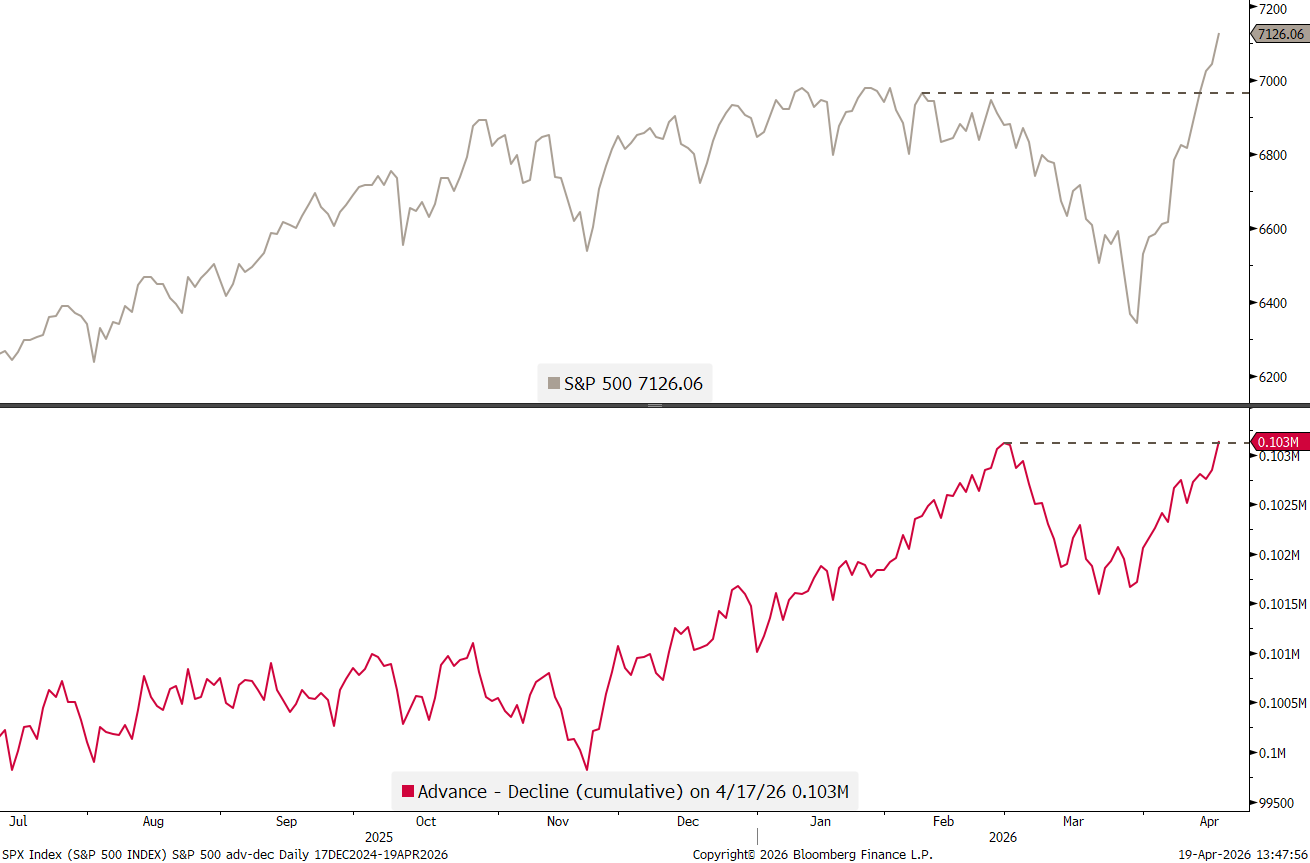

So, what’s not to like about this rally then? For starter, breadth has been ok-ish, but in contrast to the underlying index (S&P500 below) failed to reach a new all-time high, creating a possible negative divergence to the index:

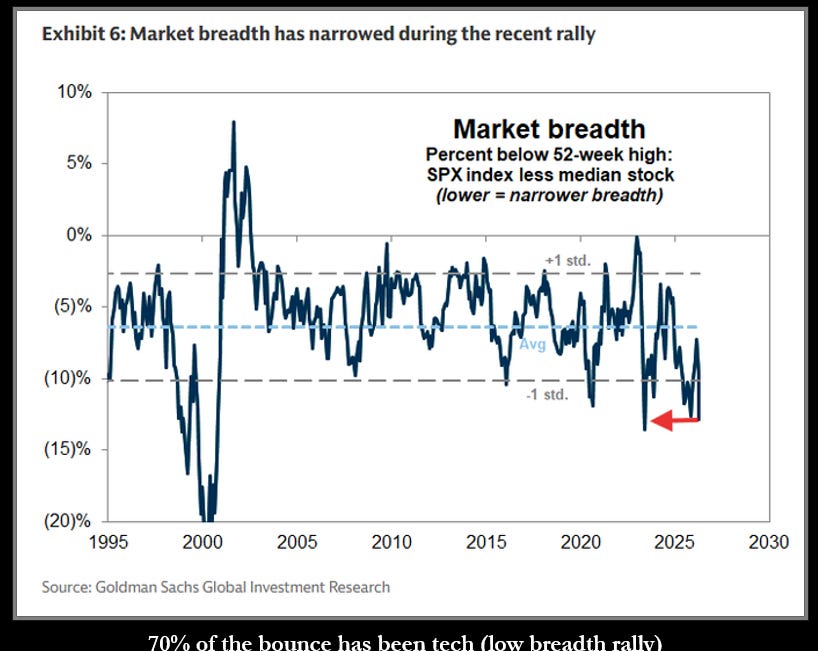

Here’s another measurement showing that breadth has not been great in this recent rally:

And then there are these signs, which may be less important from a tactical point of view, but increasingly bolster our suspicion that an end to the 17-year bull market (in the US) may be coming to a halt.

Exhibit 1 - IPOs

I firmly believe that the market top will be in on T+1 after the SpaceX IPO, which should be somewhere between June and July. But in the meantime, evidence mounts:

Exhibit 2 - AI craze

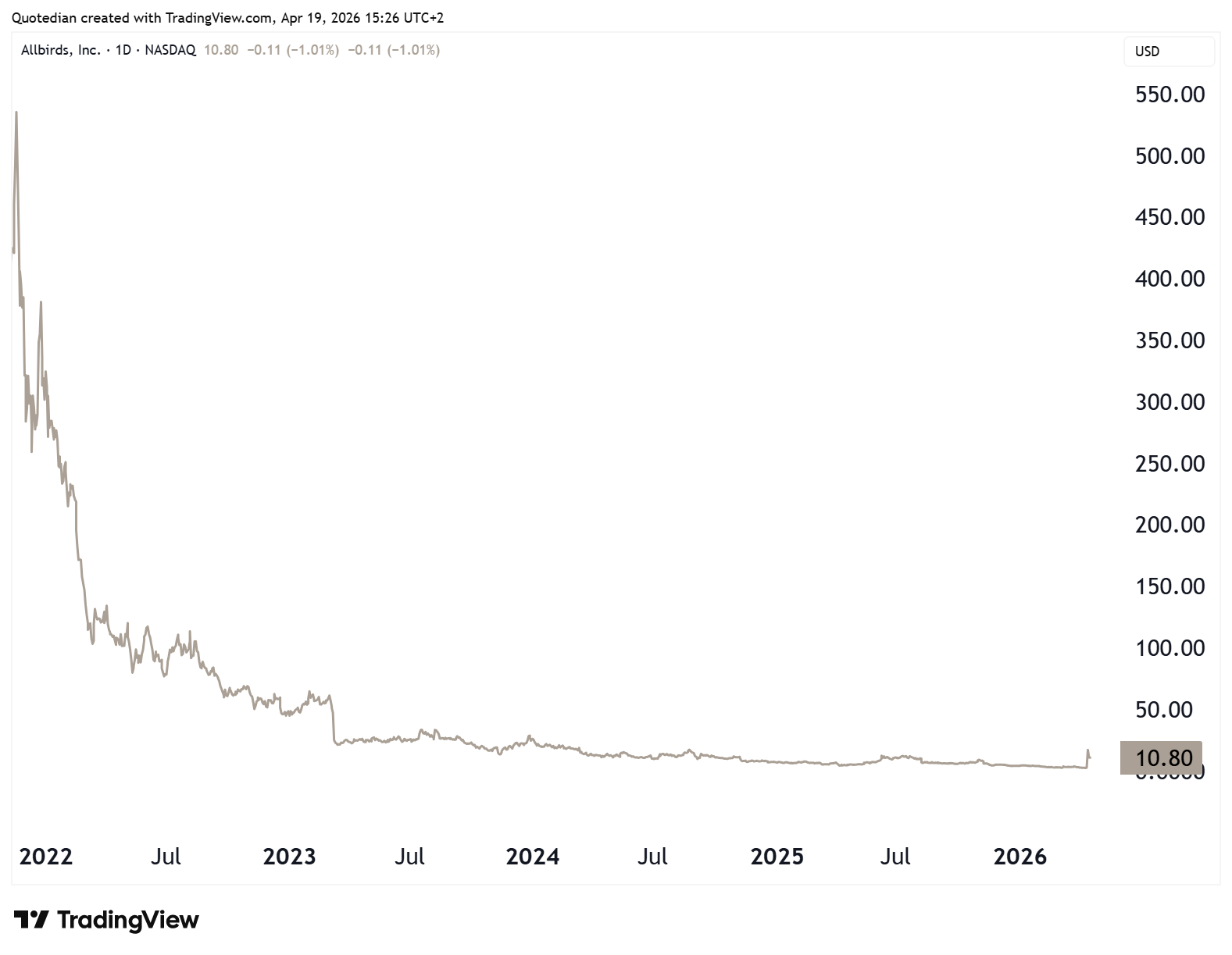

Last week, a woolen-shoe making company, Allbirds, announced that they will sell all of their core-business, supposedly including sheep et al. (week Dad-joke, I know), to re-focus on AI GPU-leasing, rebranded as NewBird AI. This is what the share price did:

Of course, the company is desperate to do anything, having seen its share price drop 99% since its IPO in 2021:

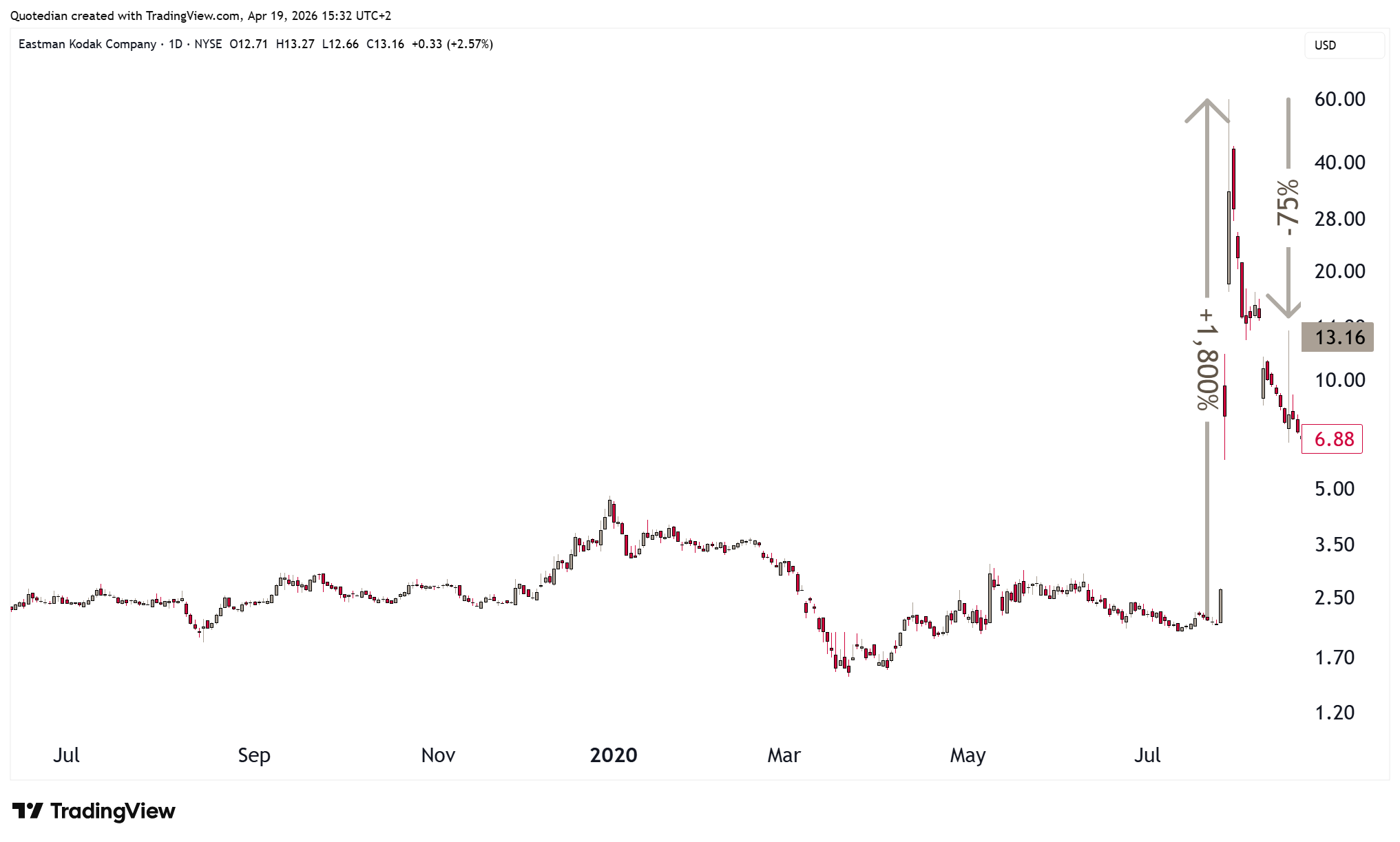

But for now, this ‘move’ reminds me a lot of Kodak’s, a once Nifty-Fifty company, intent to relaunch their glory days by refocusing their business on crypto-bla-bla-bla back in 2020:

In any case, signs of speculative fervour are plentiful and whilst we continue to slightly overweight allocation to equities, we continue to have an eye on that exit door and continue to position less ‘beta’.

In markets outside the US, the recovery in European markets has also been impressive, albeit the SXXP has not yet reached a new ATH*:

* Regional differences apply.

For example, whilst Germany’s Dax still needs to rally 3% to reach a new ATH,

Spain’s IBEX is only about a quarter of a percentage point away from reaching that feat:

And Italy’s FTSE MIB index is even already three percent above the previous ATH:

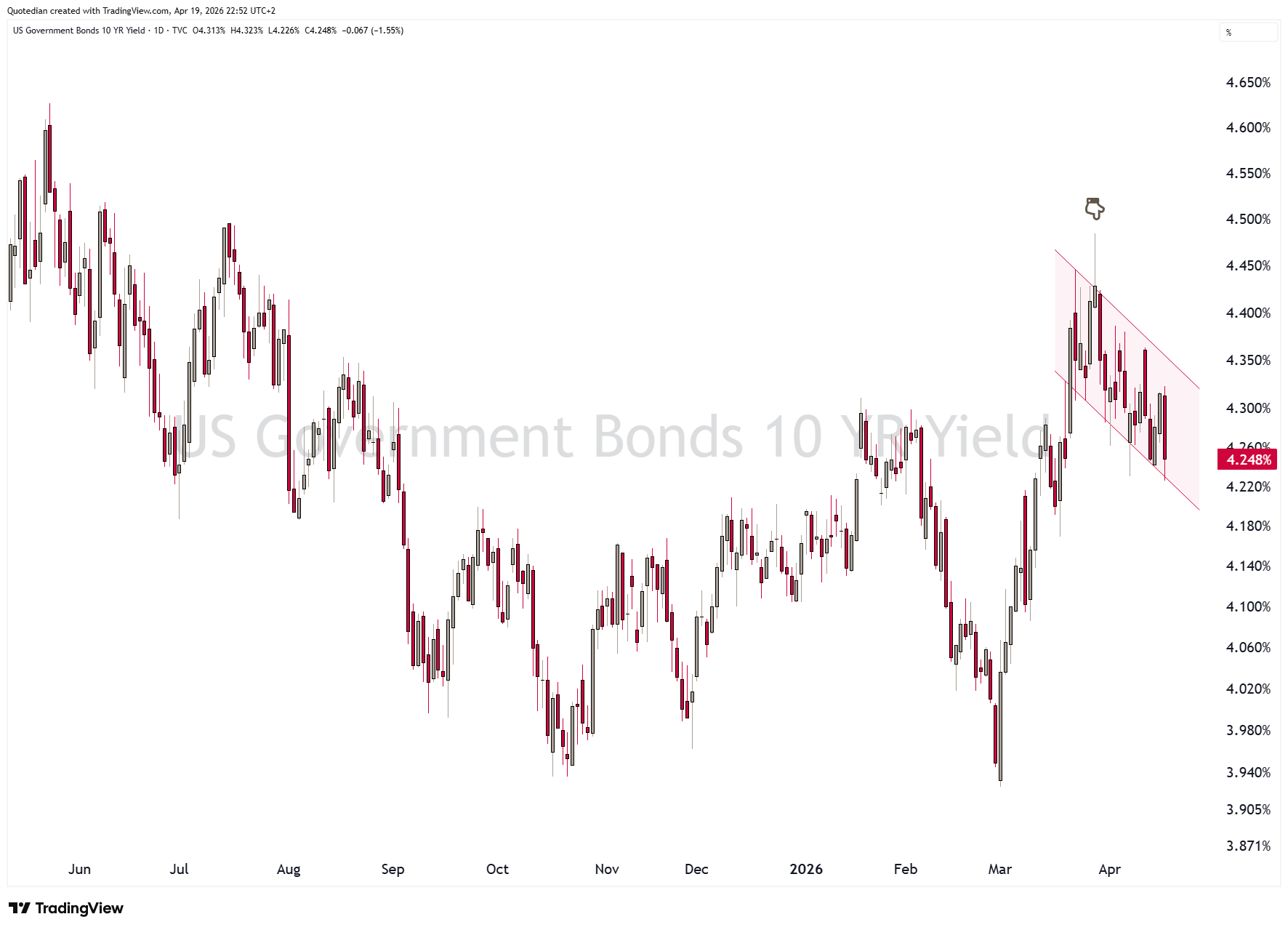

Moving over to fixed income markets, I find it intriguing, given the rally in equities how bond yields have resisted to move meaningfully lower:

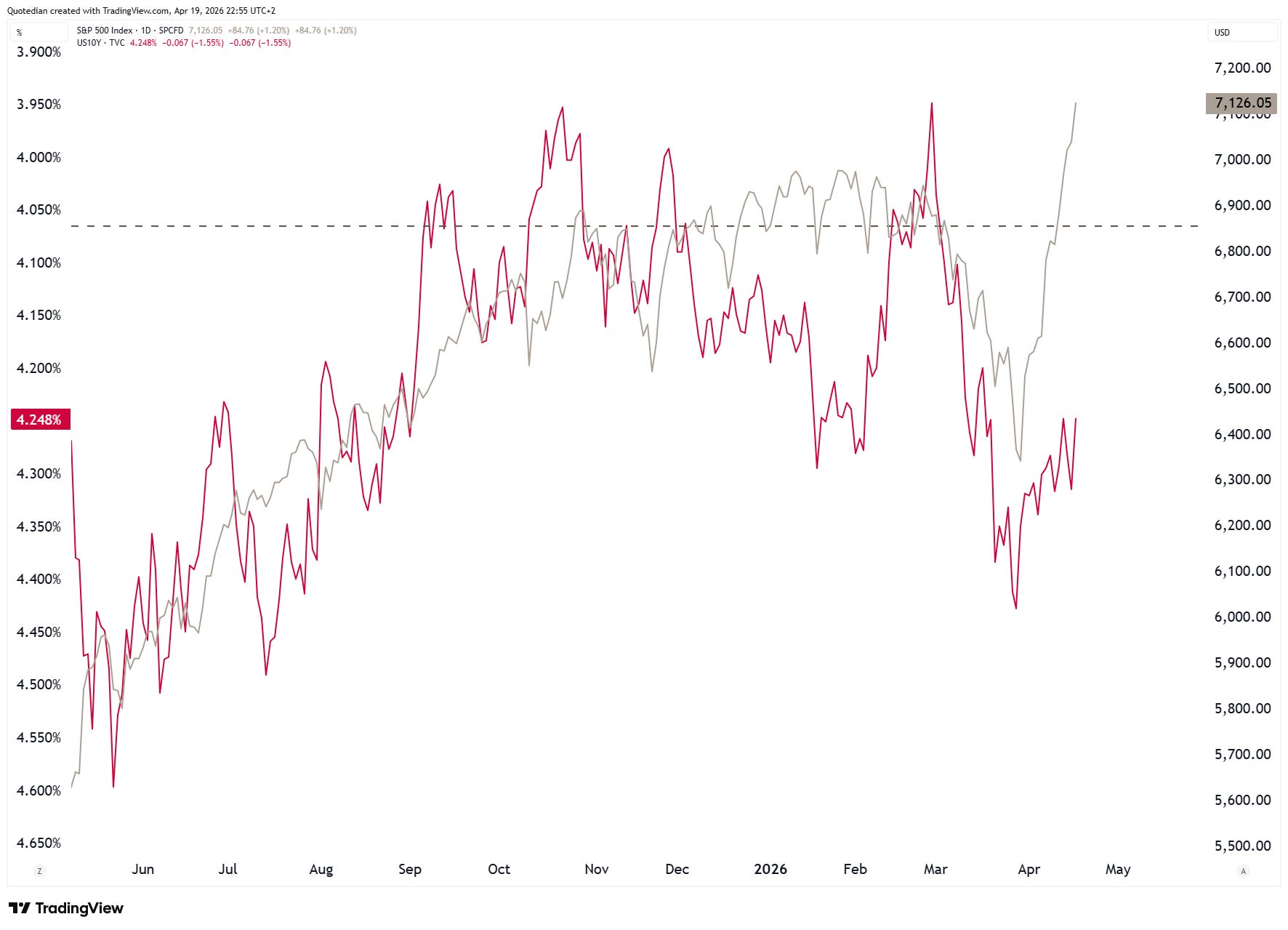

The following chart illustrates that disconnect between US10YT yields (red, inverted) to the S&P 500 (grey):

Back in the old days, it was (bond) yields, that were right, with stocks eventually giving in …

European yields, proxied via the 10-year German Bund, are refusing to come lower:

Which means the interest rate differential between European and US yields (grey line) is rising, increasing upside pressure on the EUR/USD cross (red line):

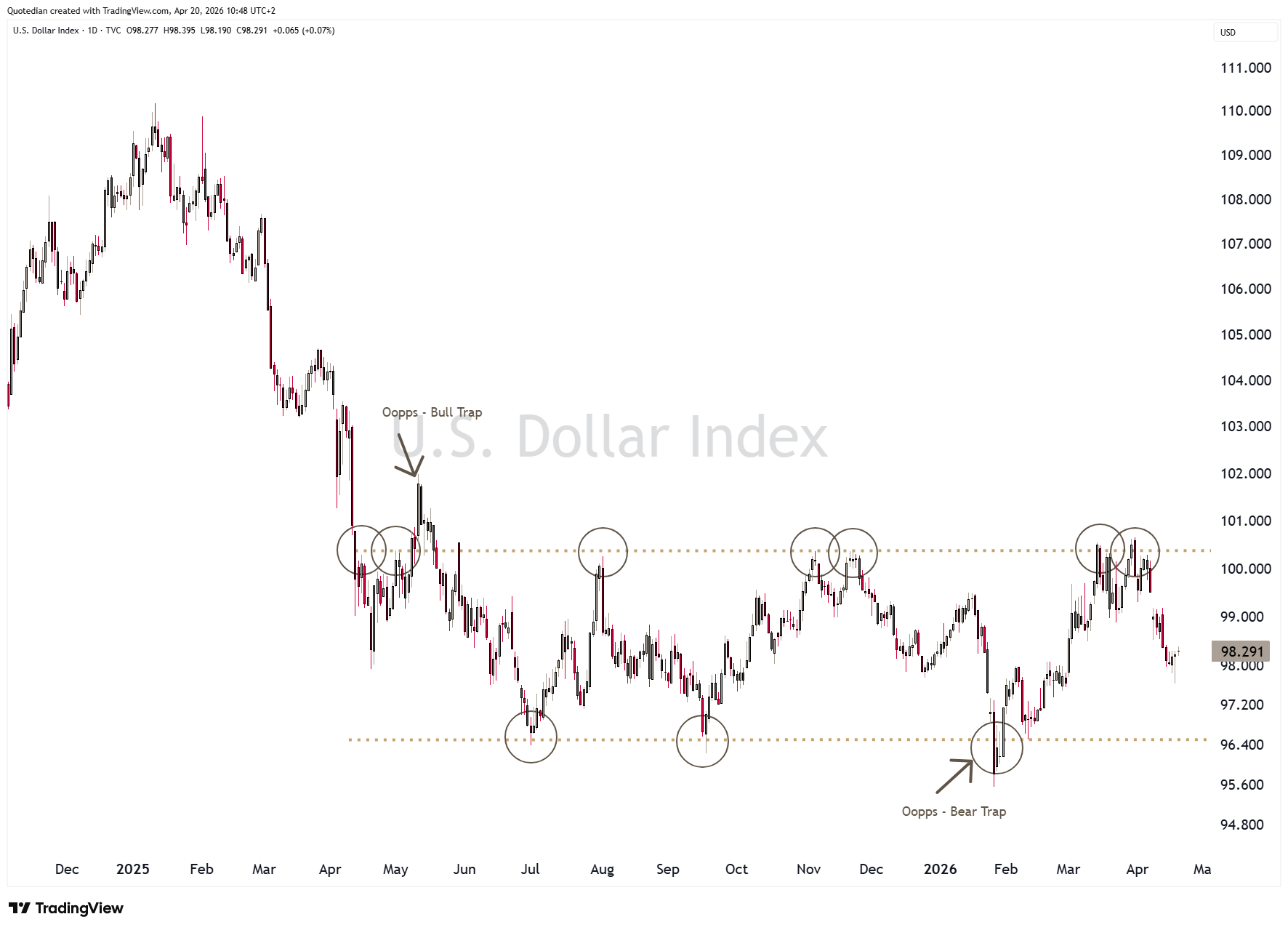

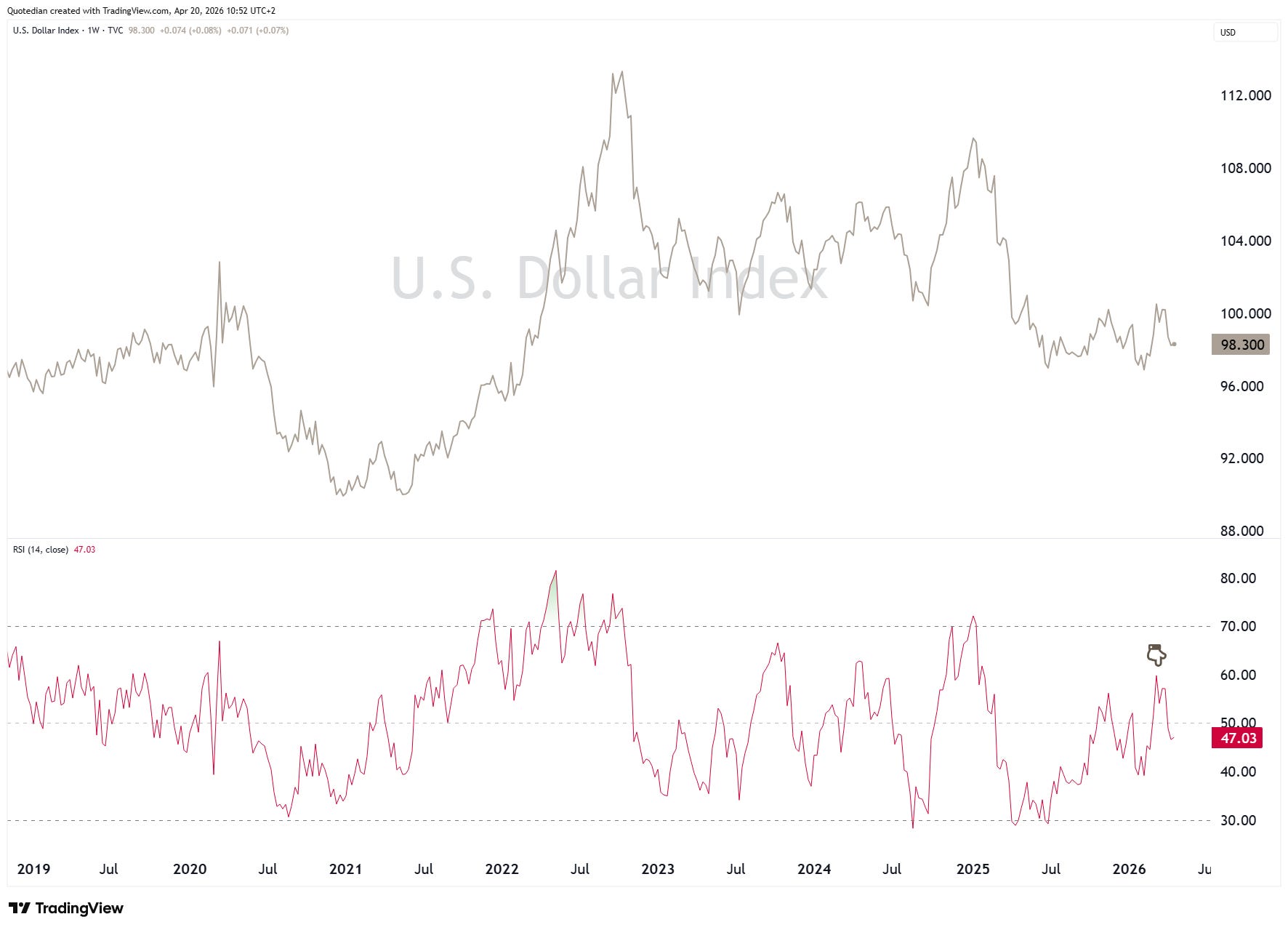

The US Dollar Index itself continues to trade in its wide trading range,

and it is noteworthy that during the last USD-rally the RSI was unable to rise above 60, which can be interpreted as a sign of underlying weakness:

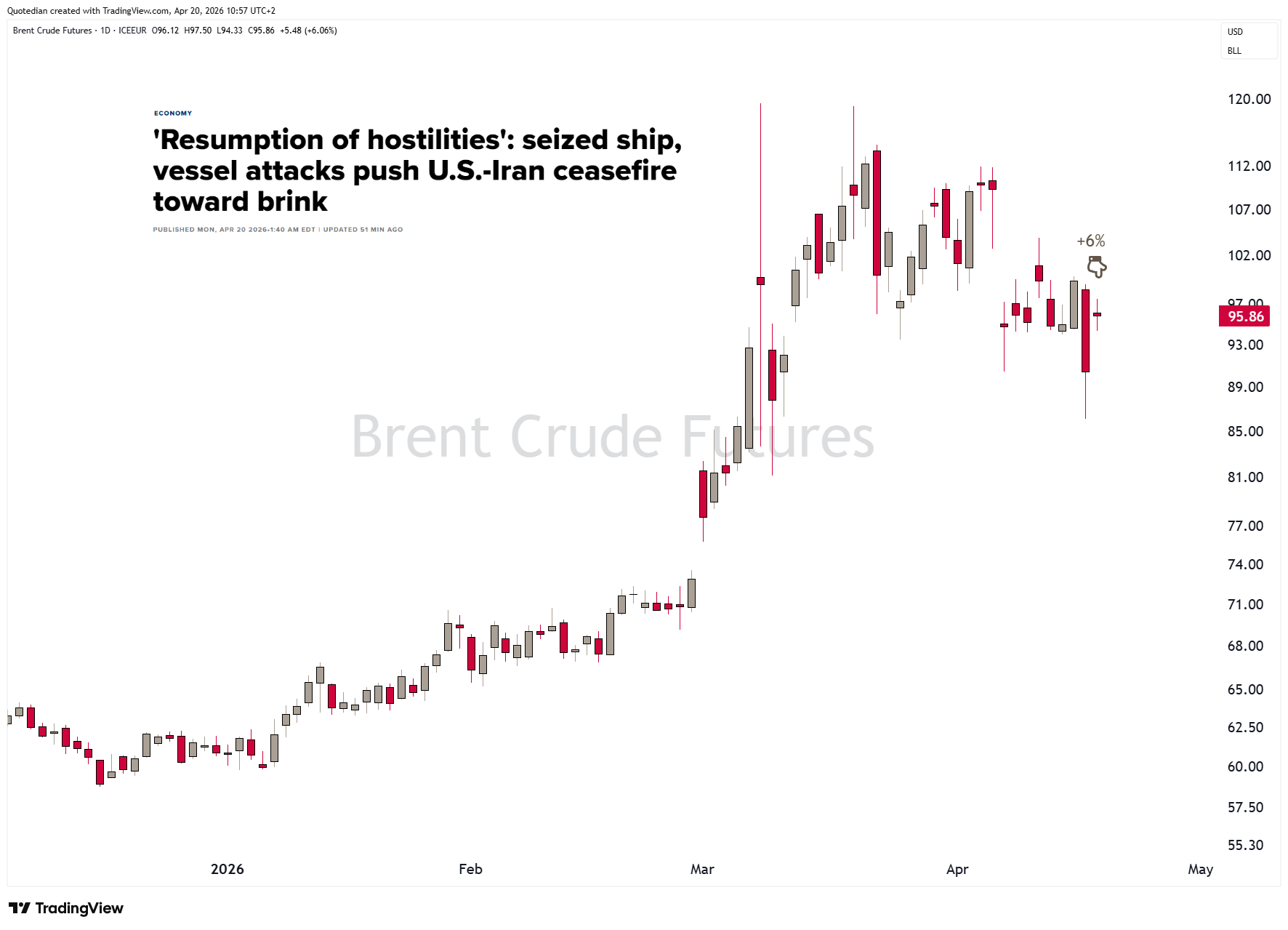

In commodity markets, where oil is still dominated by headlines, such as for example this morning,

it is probably better to be minimally exposed OR focus on the longer-term trend (which is UP for the commodity complex).

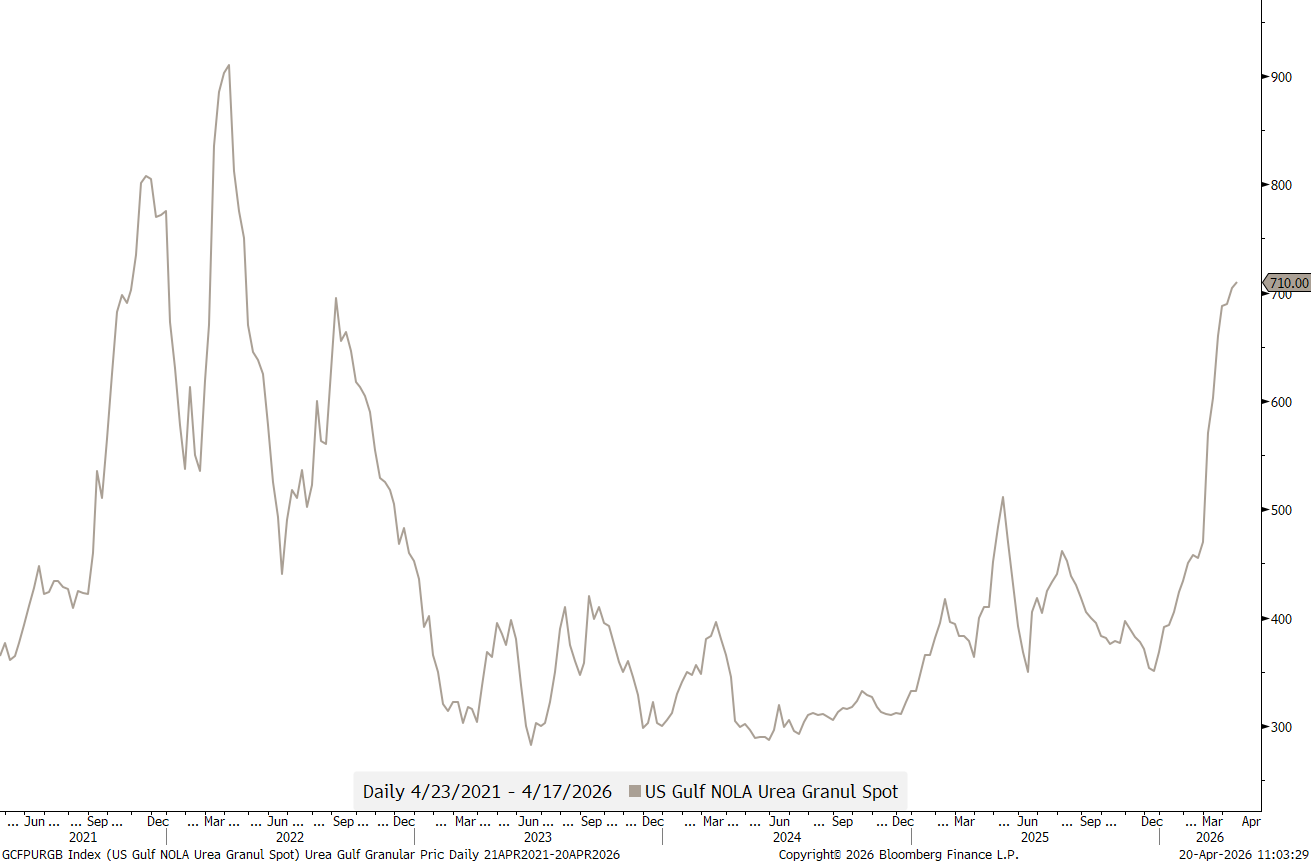

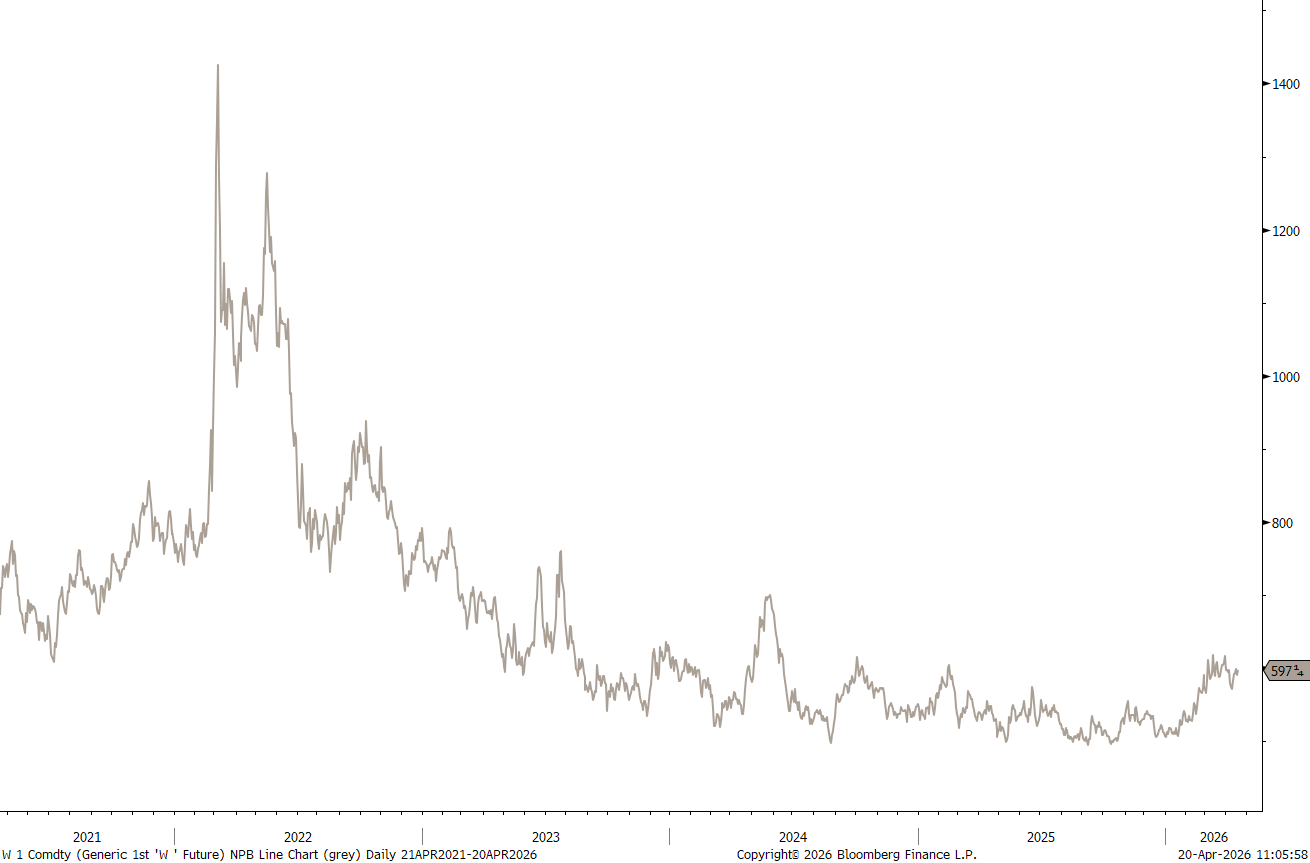

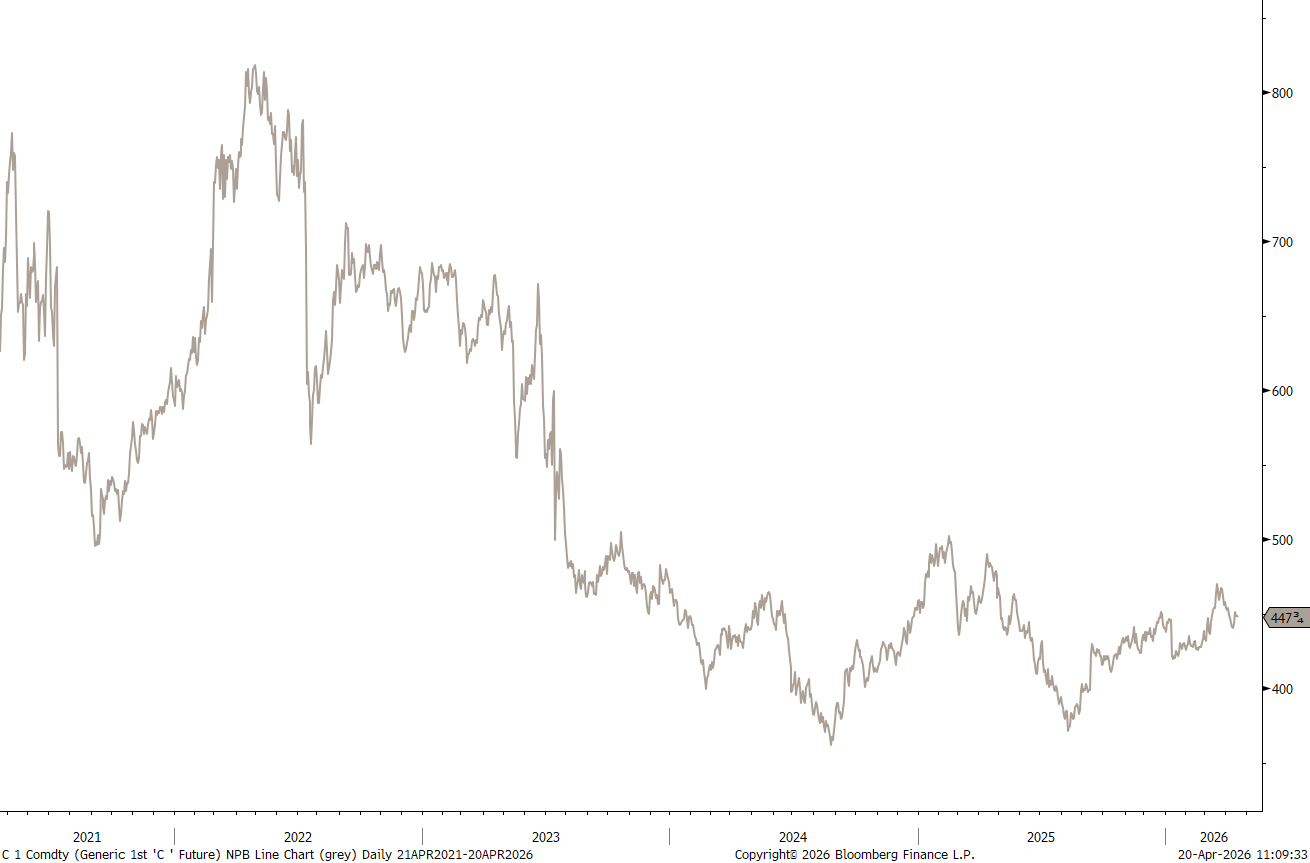

One area to closely keep an eye on are agricultural commodities. With Fertilizer prices refusing to come lower,

‘aggs’ such as Wheat

or Corn

are probably trading too low.

As proxy trade, consider the Invesco DB Agriculture ETF:

Equity markets are very short term somewhat overstretched, but should continue to do well into the early summer months.

Longer-term, we fear the 16 year bull market may be coming to an end.

However, a equity market top is not an event, rather a process.

Continue to underweight bonds as yields are refusing to head lower.

The US Dollar is likely to weaken further.

Look for more upside in the agriculture commodity space

That’s all for this week - May the Trend be with You!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG