This Is The End

The Quotedian - Vol V, Issue 139

“New beginnings are often disguised as painful endings.”

— Lao Tzu

“Now this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”— Winston Churchil

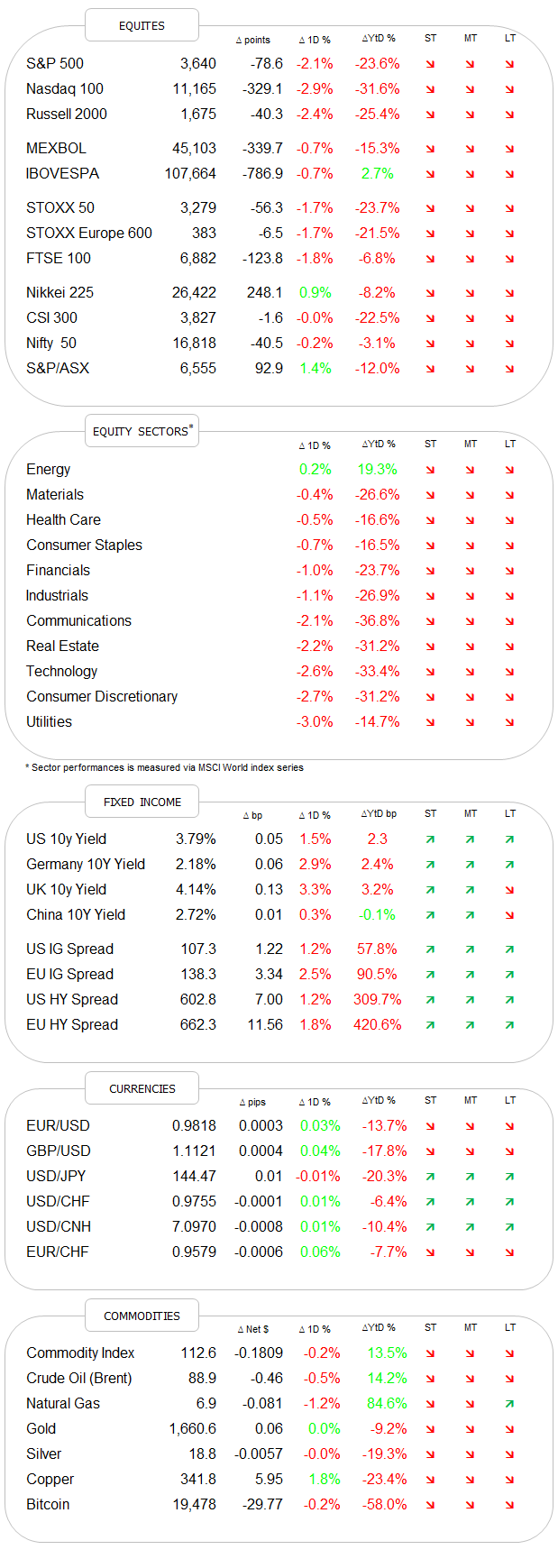

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

Today is a special day. It’s Friday. It’s the end of the week. It’s the end of the month. It’s the end of the quarter. It’s also the end to other, more personal matters… but above all, I think we are collectively happy that this very difficult week in financial markets is coming to an end. Unless you were short, then long, then short and had nerves of steel (no, I couldn’t write balls of steel, that would not have been appropriate).

In any case, with a very looooong Quotedian ahead on Sunday (remember, end of week/month/quarter), let’s keep it sweet n’ short today (is that a collective sigh of relief I am hearing there?)

Starting with equity, if we defined Wednesday’s session as ‘Vengeance Wednesday’ (58% of you voted so), then yesterday Vengeance was taken out in the backyard and shot in the head, as markets reversed once again lower. The distance covered on stocks (here’s the S&P 500 as proxy) is astounding:

My idea for traders yesterday to give a try to trading the bounce would probably be stopped out now, though it does not feel like markets have completely broken support (yet?):

But the important message here is keeping discipline with your risk management (aka money management aka stop losses):

"The key to risk management is never putting yourself in a position where you cannot live to fight another day."

[Note to self: Not sure Dick is the most adequate person to talk about risk]

Interestingly enough, the session may have turned out slightly less negative if Apple, weighing 7% in the S&P 500 and 13% in the Nasdaq, would not have plunged five percent. But it has:

Hard to believe now that the stock was only four percent from a new all-time high only one and a half months ago!

In any case, breadth was not good either yesterday and on the chart, the cumulative advancers-decliners spread is about to break lower together with the index:

Asian markets are giving little hope for a turnaround of the turnaround confirming the preceding turnaround (I am getting lost, but you know what I mean), as most local benchmark indices are printing red in the excess of one percent. European and US equity index futures seem to hold up though for now … sort of …

As a segue into bonds, consider the following chart, comparing the SPDR S&P 500 ETF (SPY - top clip) to the iShares Corporate High Yield Bond ETF (HYG - lower clip):

Scary thought #1 here is that HYG as already broken lower and could be an indication of what is to come for SPY. Scary thought #2 is that it looks like HYG may retest the March 2022 lows (less than 5% to go). What if SPY would try to do the same? Hush, shut up me!

As a matter of fact, that is (nearly) the only bond observation I will make for today, but I recommend you not to miss today’s chart of the day, especially you equity-focused hot-heads.

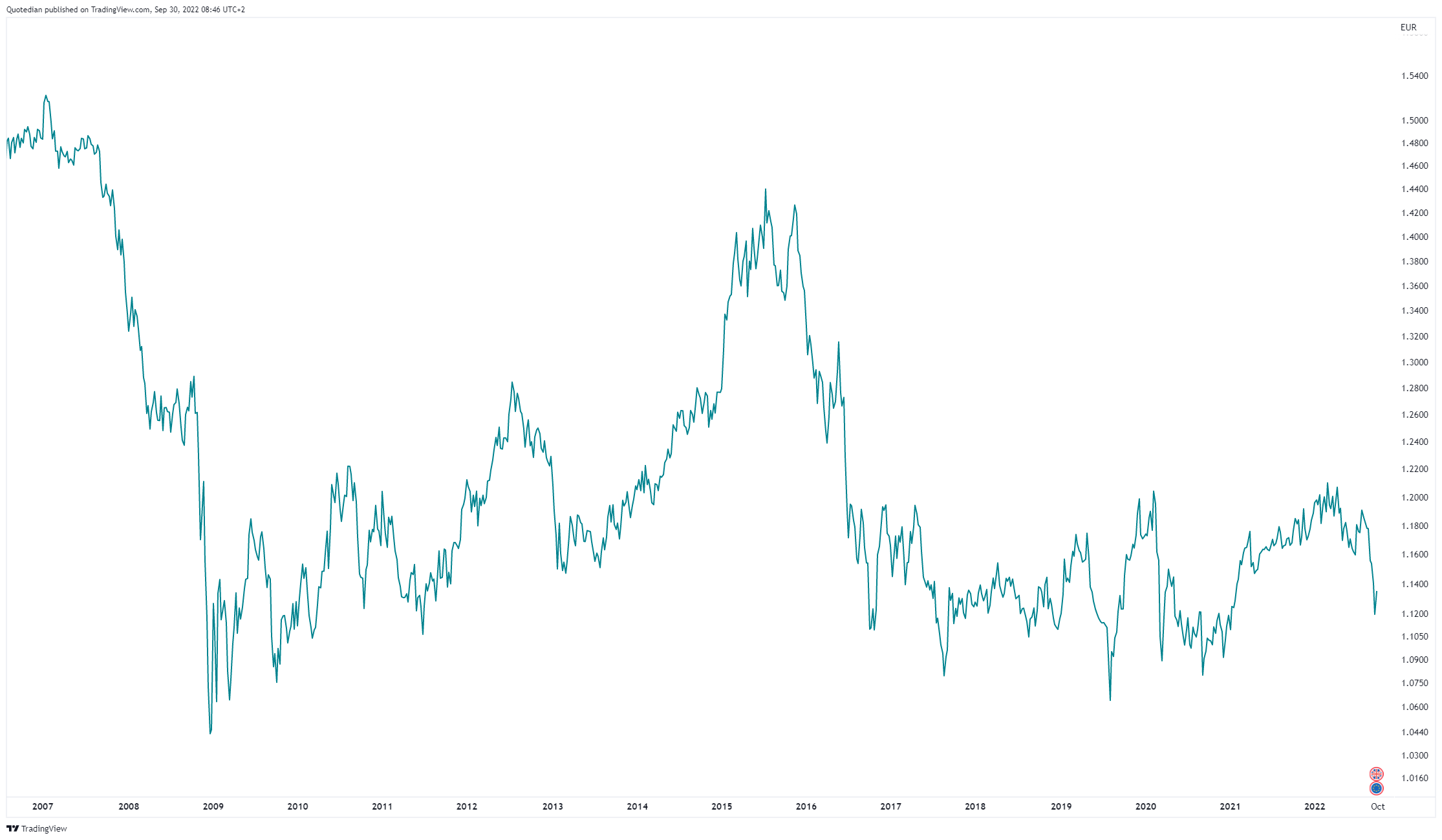

On to currencies then … Remember how we have discussed in the past how magazine covers in the past have often served as a contrarian indicator, especially as a trend started to get long in the tooth. Well, maybe we’re getting there on the US Dollar:

Interestingly enough, and in a complete reversal to our most recent experience, has the Dollar seemingly topped out - at least on the short-term, whilst risky assets haven’t yet:

Of course, could it just be another of those consolidation periods, but even those were enough in the past to give a reprieve to for example stocks. Important note: I am not trying to convey a bullish picture, still a long-term secular bear supporter, but as always try to highlight all possibilities.

The GBP/USD is close to having reversed the entire ‘glitch’ starting last Friday:

Another quick observation … few of us are actually USD-based investors, however, we always speak about the Cable (GBP/USD), albeit the cross that should interest us is GBP/EUR (or EUR/GBP, whichever parity you prefer). Not THAT much happened there this week in comparison to previous moves:

By the way, do you know why the GBP/USD cross-rate is called the cable? Leave your guess (no Googling) in the comments section:

Let me hit the Send button and please make sure you have a great weekend!

C U Sunday,

André

CHART OF THE DAY

For all you equity-focused investors (I know most of you are), here is a COTD that should make you think before stopping to read (I know you do) The Quotedian when we arrive at the fixed income deliberations section.

Consider the moves this week on the 40-year UK Gilt, a non-leveraged, highly liquid and tradable instrument:

Go short before going to lunch Friday a week ago, party hard all weekend long, awaken from your hangover on Wednesday morning and quickly reverse your position before starting your weekend early with a liquid lunch…

AMC, Bed Bath & Beyond, Gamestop, etc … boy’s playground in comparison!

Thanks for reading The Quotedian! Subscribe for free to receive new posts and support my work.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance