To Infinity and Beyond

Vol IX, Issue 17 | A NPB Original

“It isn't the mountains ahead to climb that wear you out; it's the pebble in your shoe.”

— Muhammad Ali

Uff. Wow. Incredible. Unbelievable. Gargantuan. Unstoppable.

To infinity and beyond:

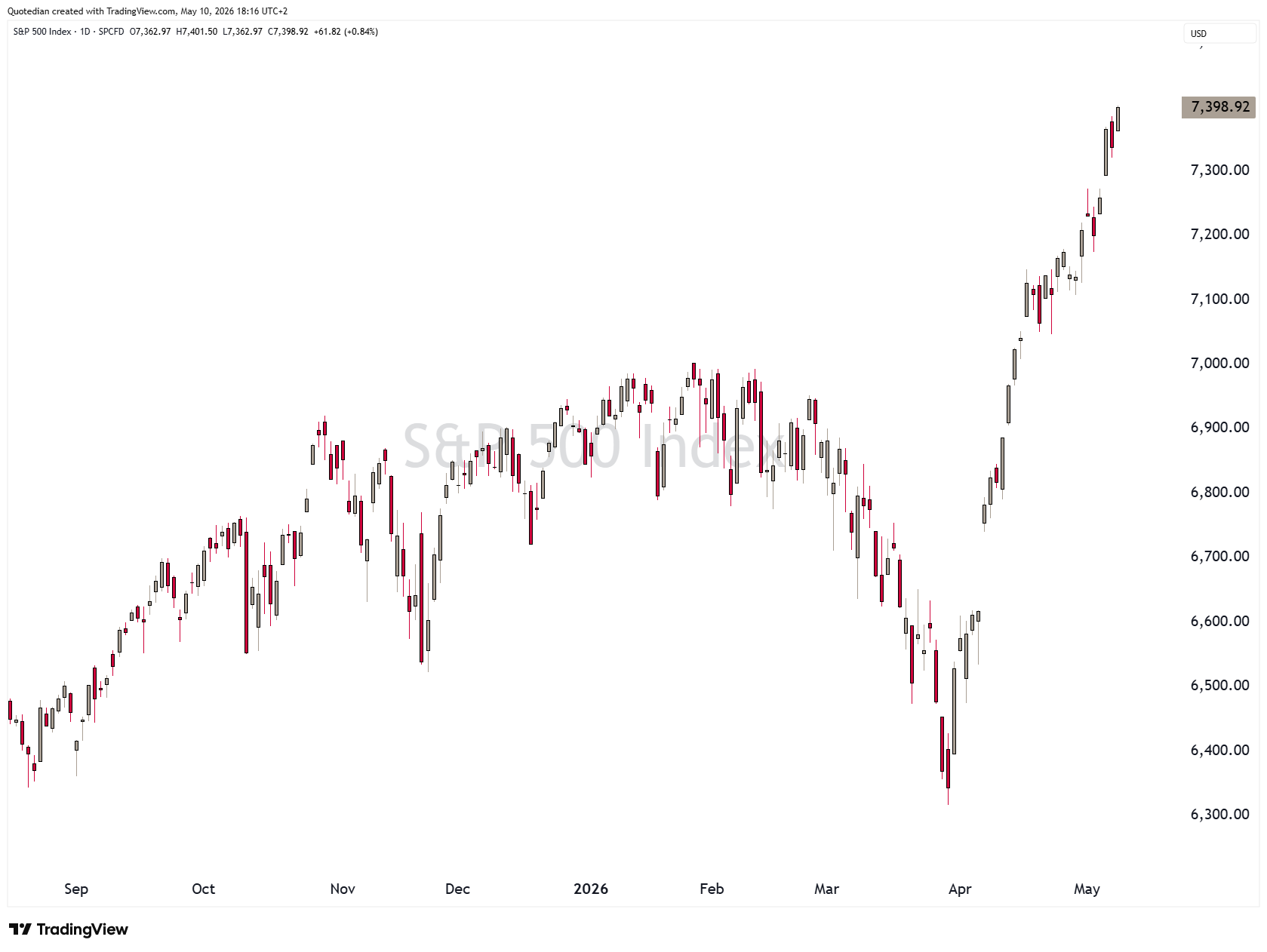

Since April 8th, most equity markets have been on a tear, not least the S&P 500 depicted above. True panic buying seems to be at hand, and for the older semesters amongst us, we have 30-year flashbacks to the late 90ies, where stocks ripped higher over years. Maybe it is time to dig out and update that good old Dow 10,000 hat:

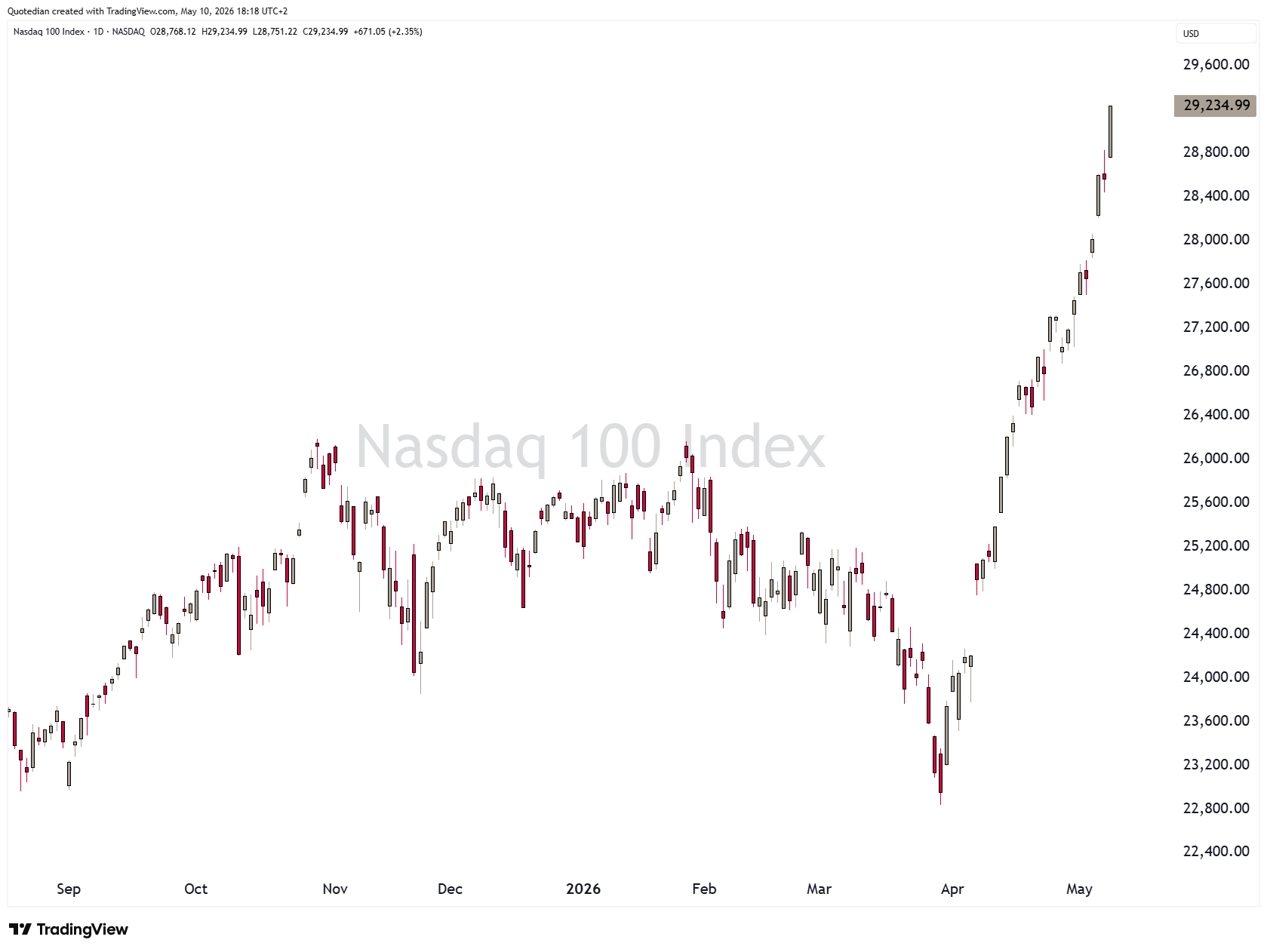

The rut has been even more relentless for the Nasdaq, up nearly 30% over the past month:

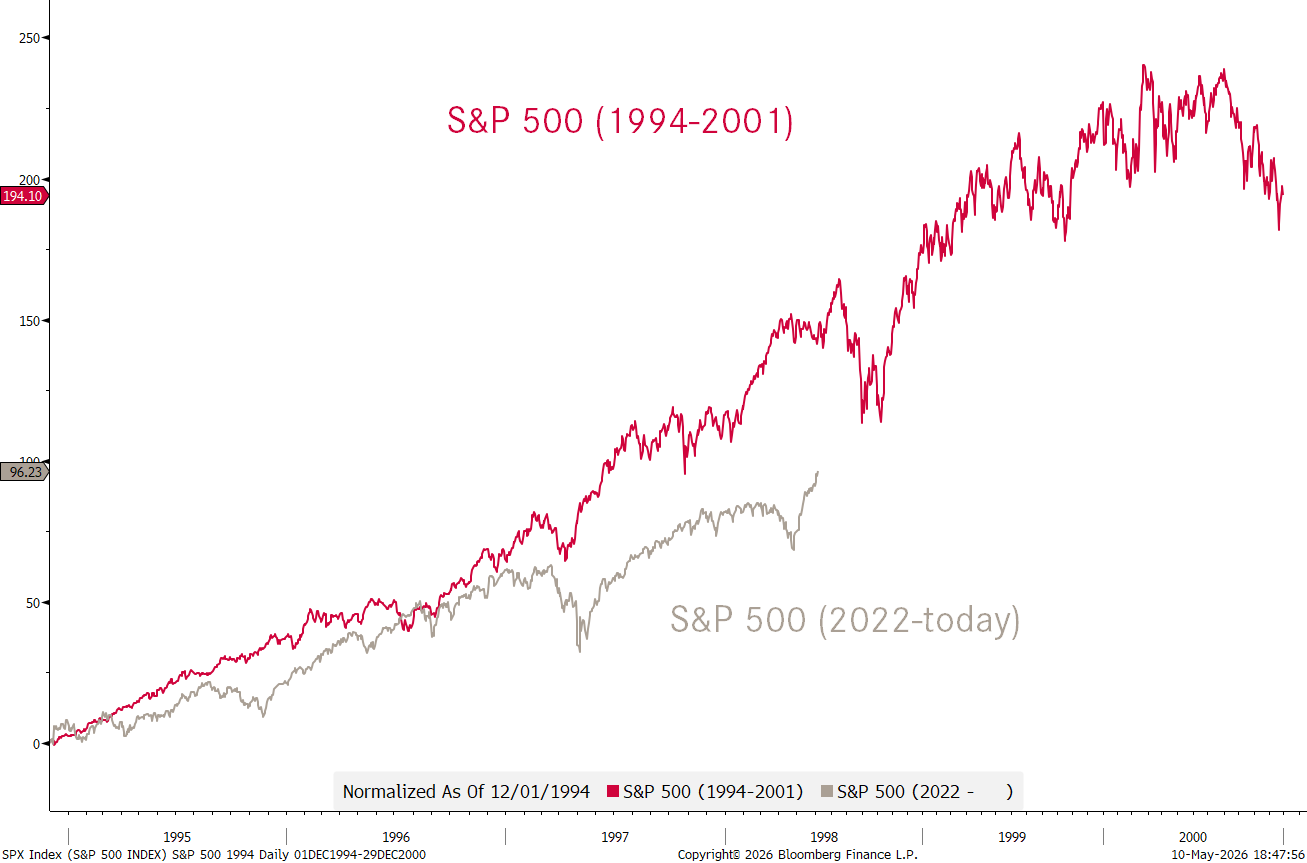

But, if we are indeed reliving Dotcom bubble of the late 90ies, let’s call it the Roaring 20’, how much more space is there left to the upside? If we align the release of the first web-browser in 1994 (anyone remember Netscape?) with the release of ChatGPT in 2022 …

… stocks will still more than double from here!

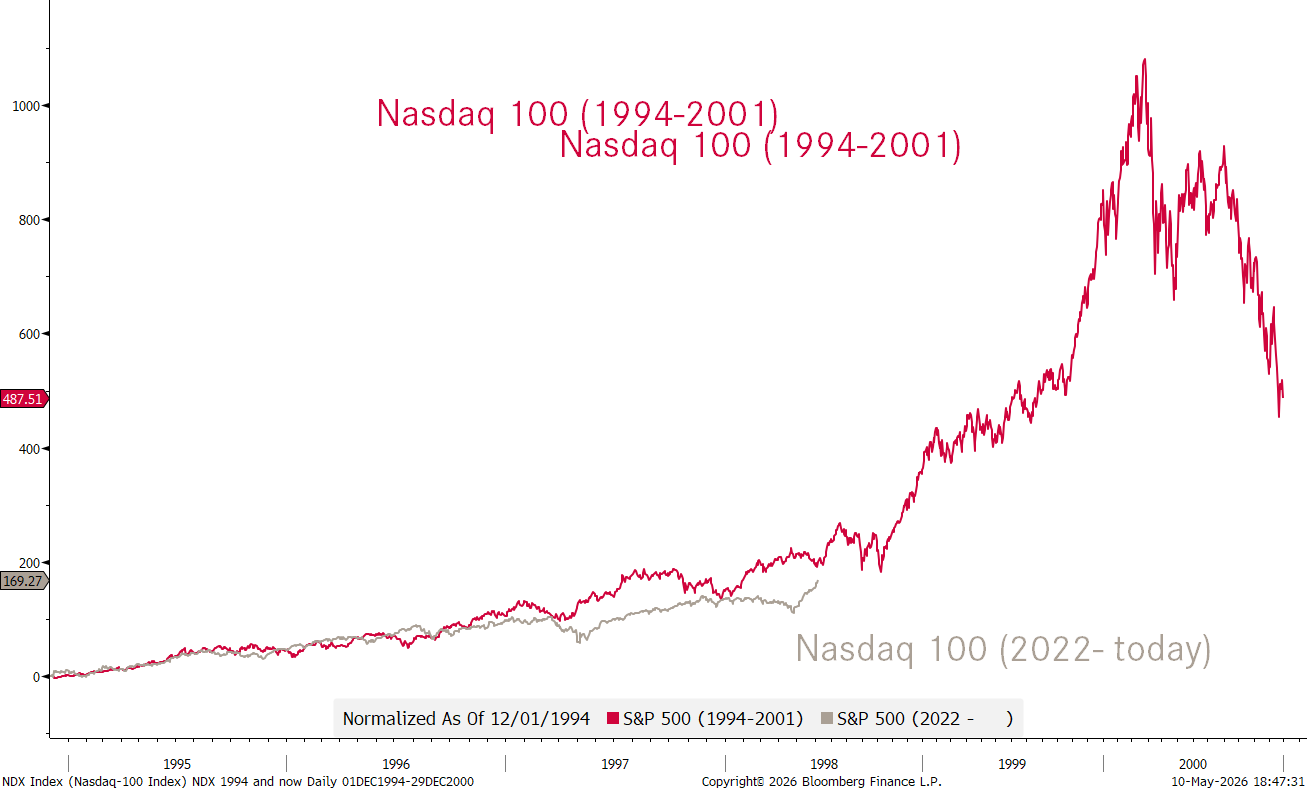

If that is not bullish enough for you, maybe let’s do the same comparison for the Nasdaq 100:

Any FOMO symptoms hitting you yet?

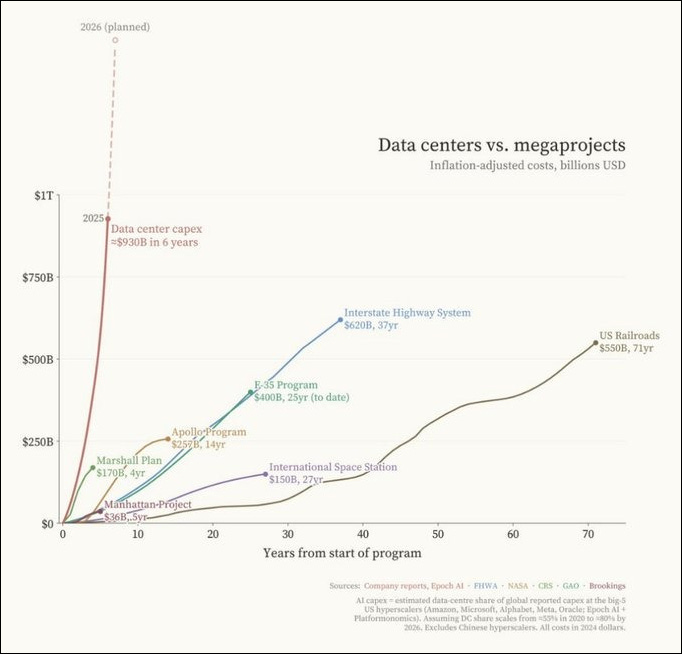

Clearly, we are in the midst of another global megaproject, but ‘recent’ previous experiences pale in comparison, even inflation-adjusted:

To be sure, whilst earnings usually beat analysts’ estimates, this quarter (red) is rather standing out:

However, this fantastic chart from Apollo’s CIO Torsten Slok shows how those EPS gains are increasingly concentrated, i.e. coming from a few, outstanding companies:

Now, having said that, ‘things’ are getting rather wonky here. Not only because the Philadelphia Semiconductor Index, more affectionately know as the SOX, is up 65% in just a bit over a month,

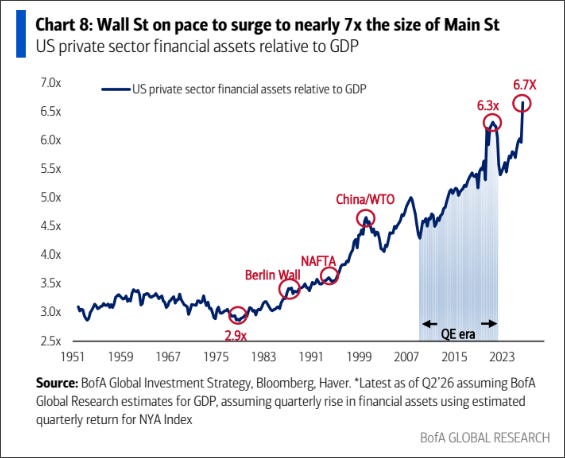

but also the overall size of market has become somewhat … surrealistic:

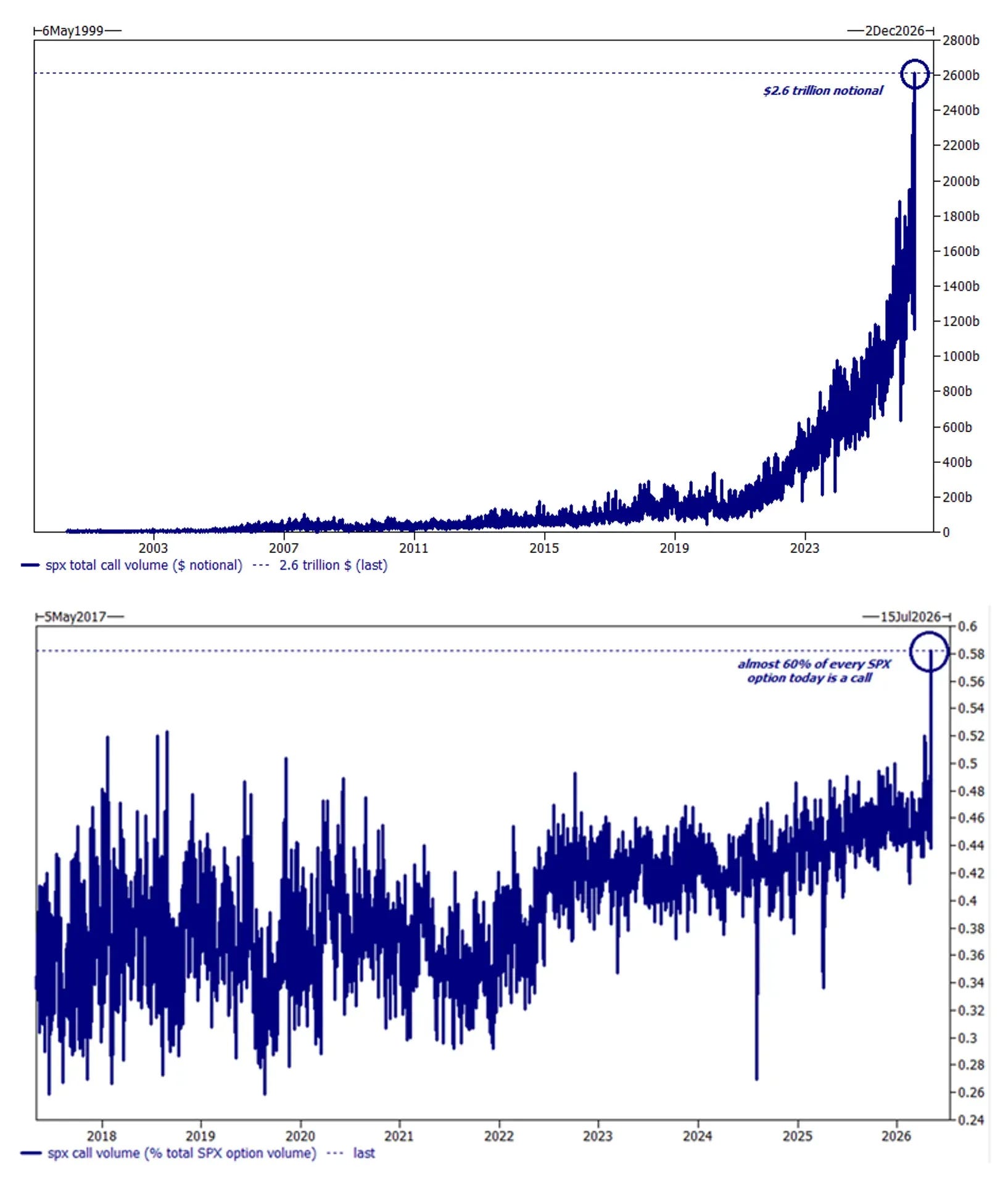

More irrational exuberance “to infinity and beyond” signs … option call volume has exploded, showing a certain speculative fervour:

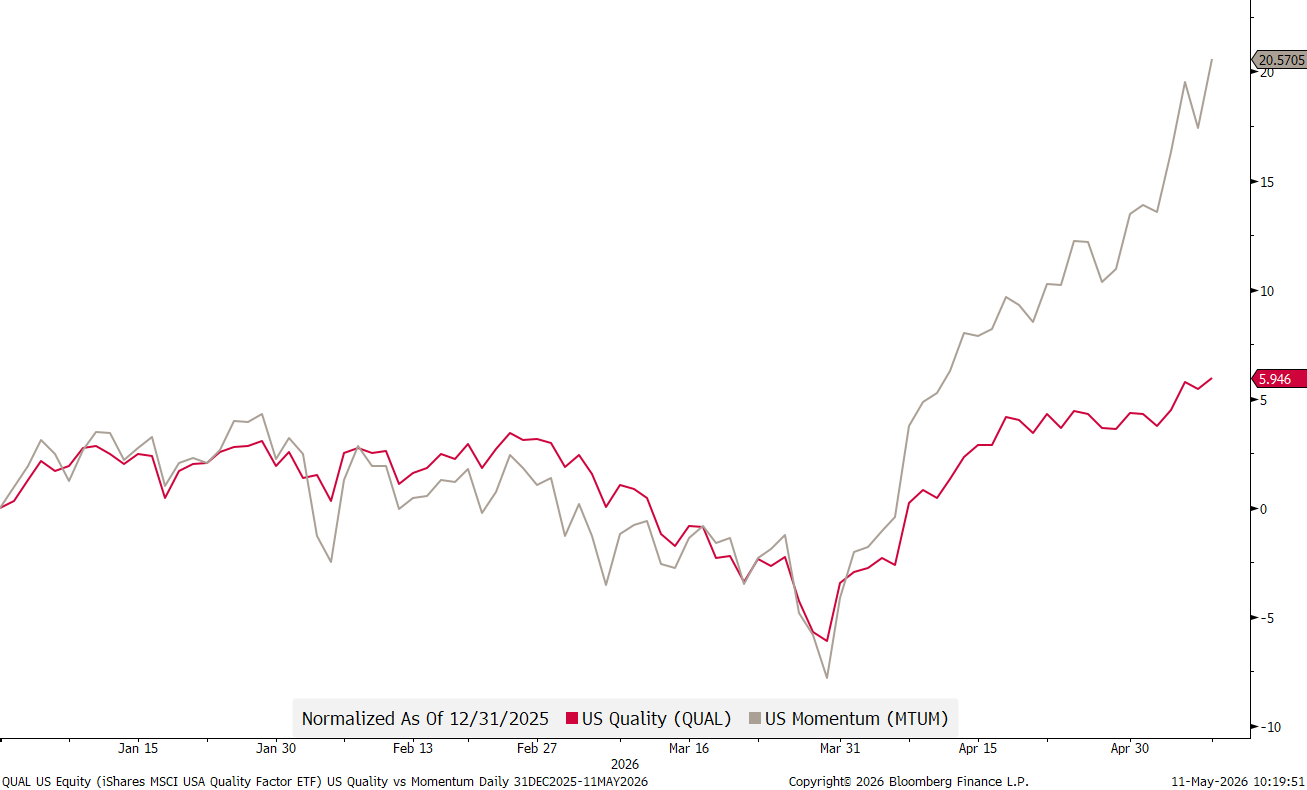

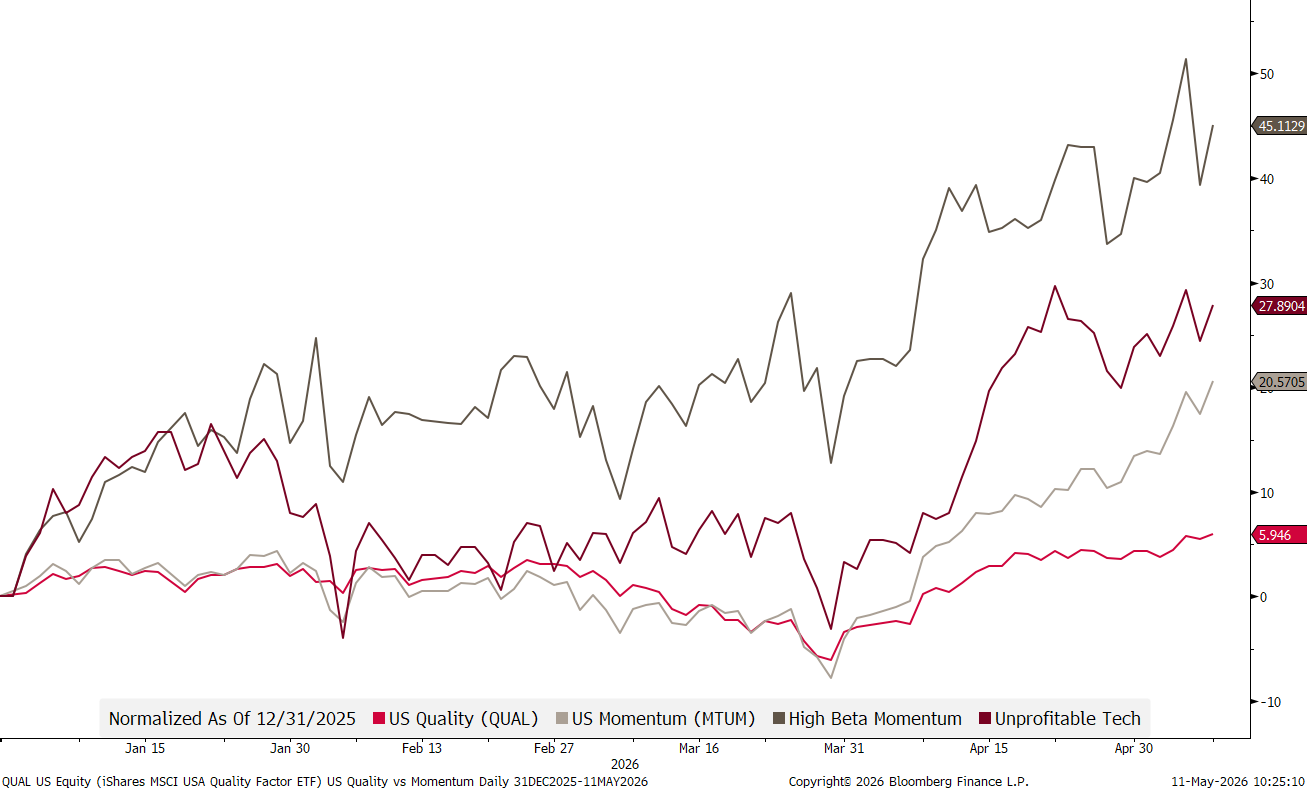

Quality (red) is left in the dust by speculative Momentum (grey) buyers:

And if we add even more froth to the mix, such as high beta momentum (dark grey) or unprofitable tech (dark red) stocks it gets really silly:

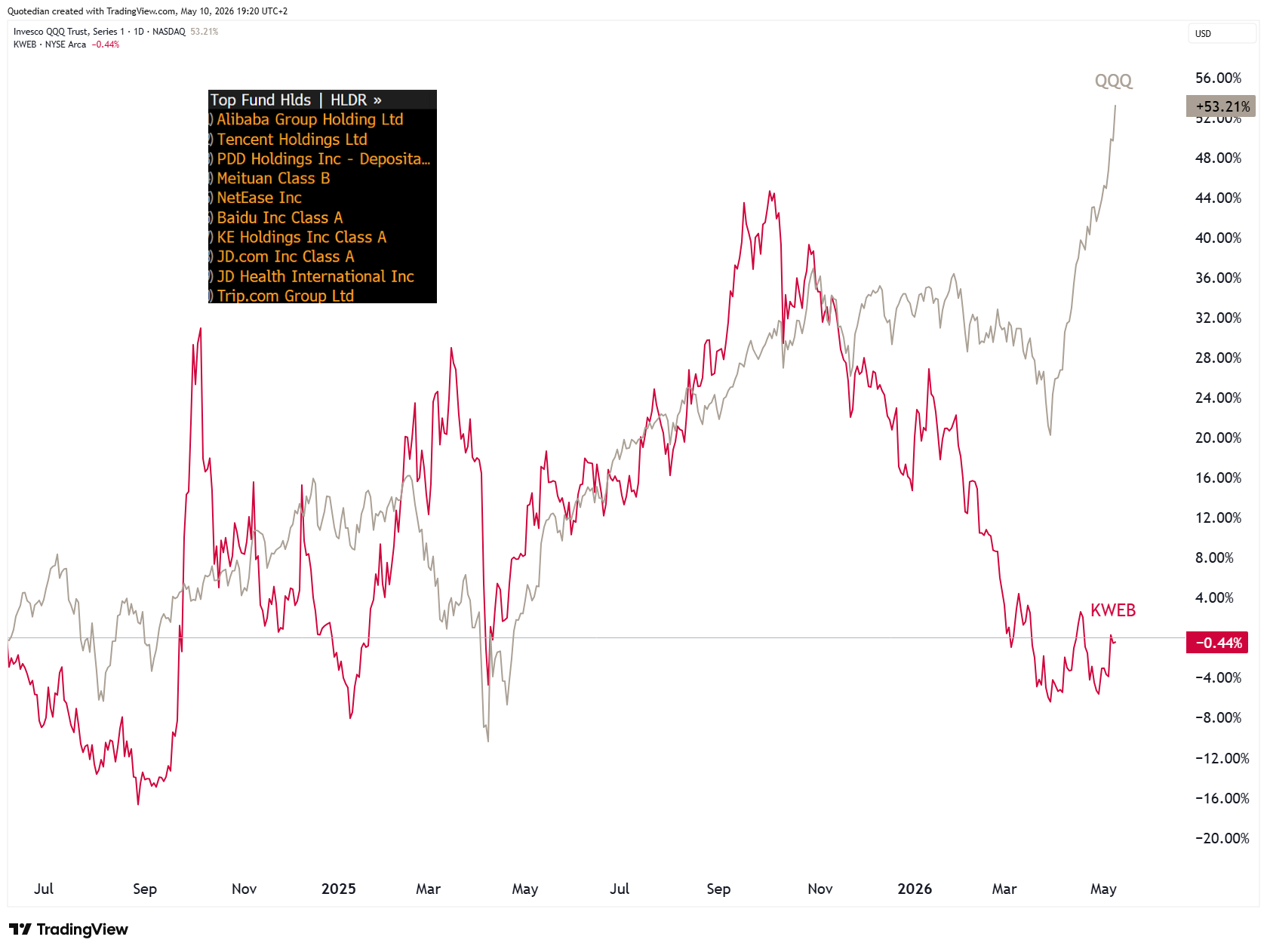

But let’s keep a positive spin on this and look for ‘stuff’ that may be due for a decent catch-up rally. For example, the KraneShares CSI China Internet ETF (KWEB) has been “left for dead” behind:

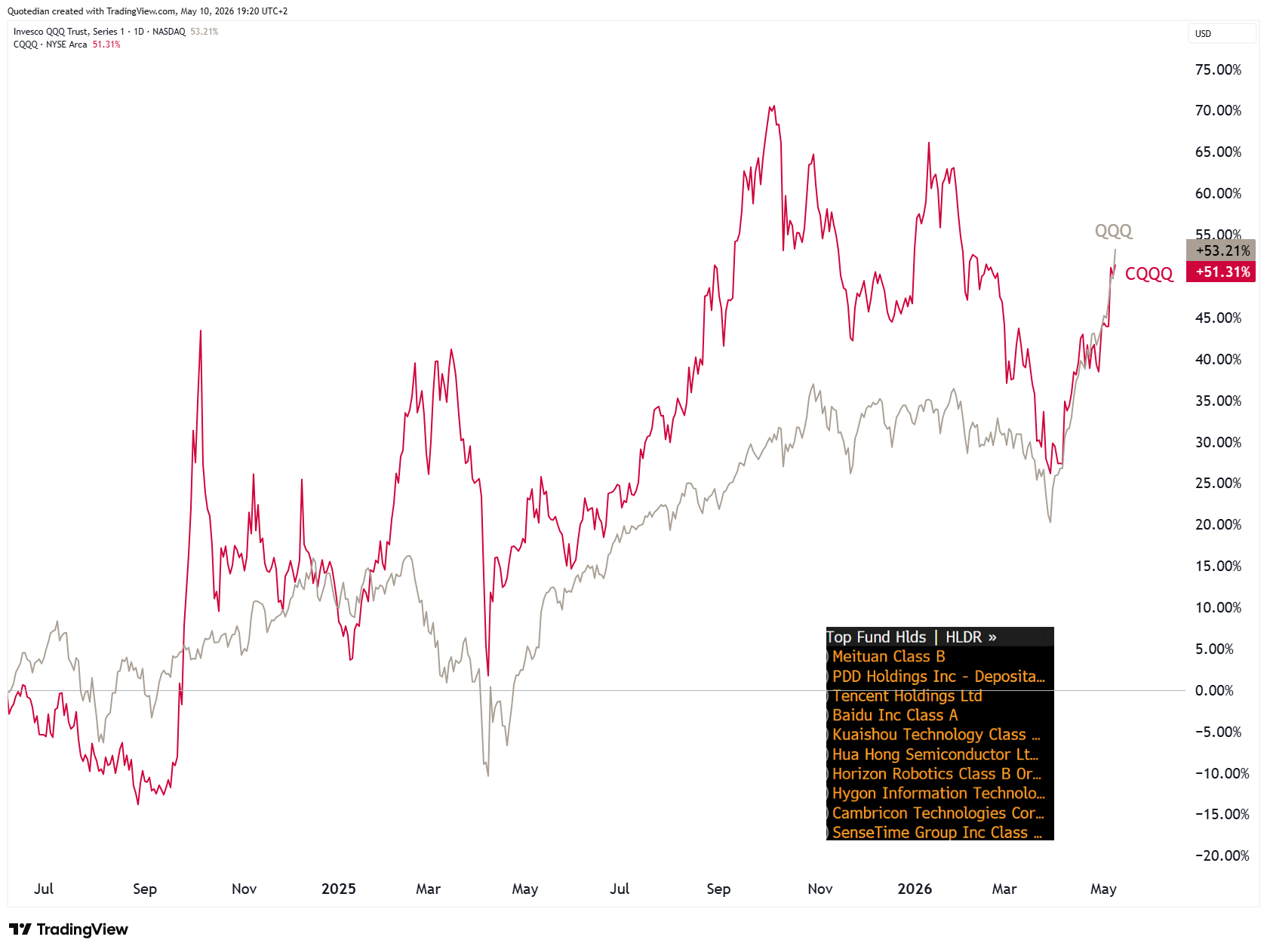

Albeit, all truth being told, the broader Chinese technology sector, here proxied via the Invesco China Technology ETF (CQQQ) has been keeping up with its US counterpart:

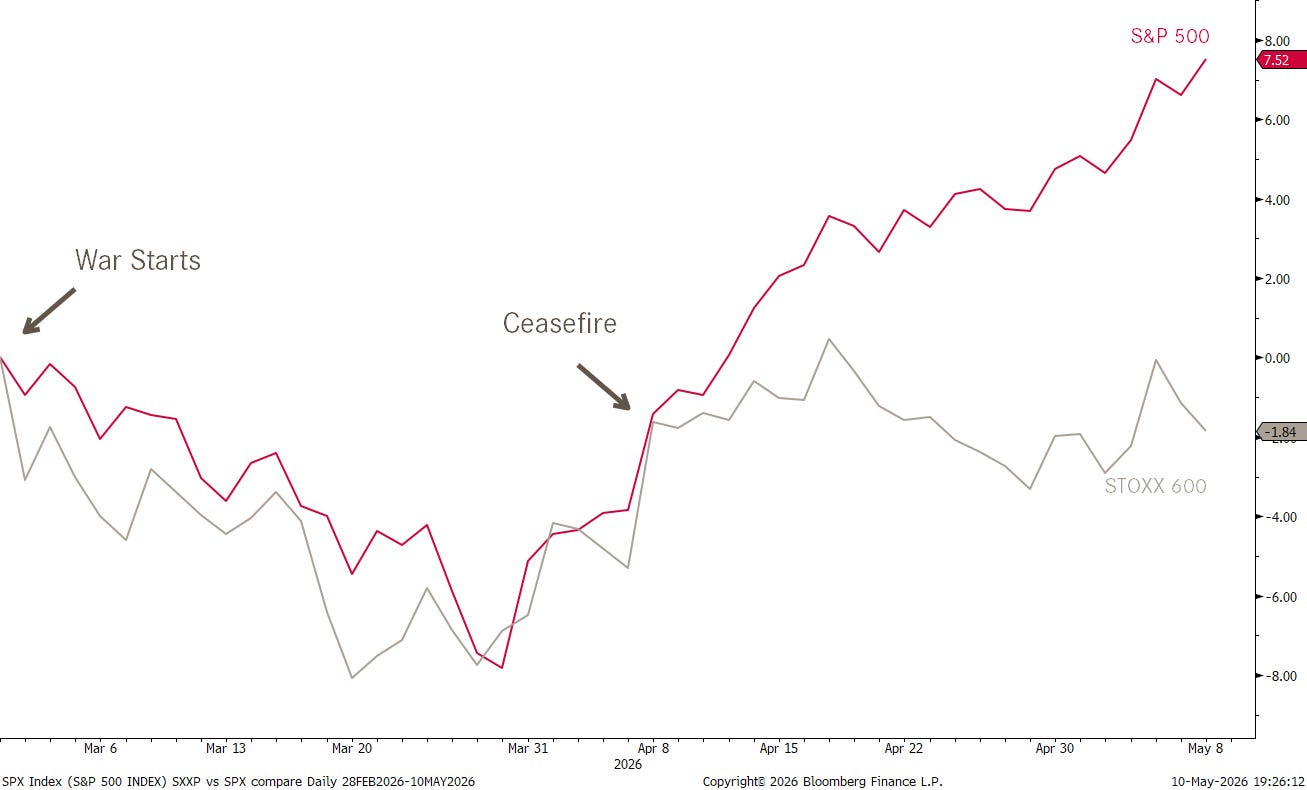

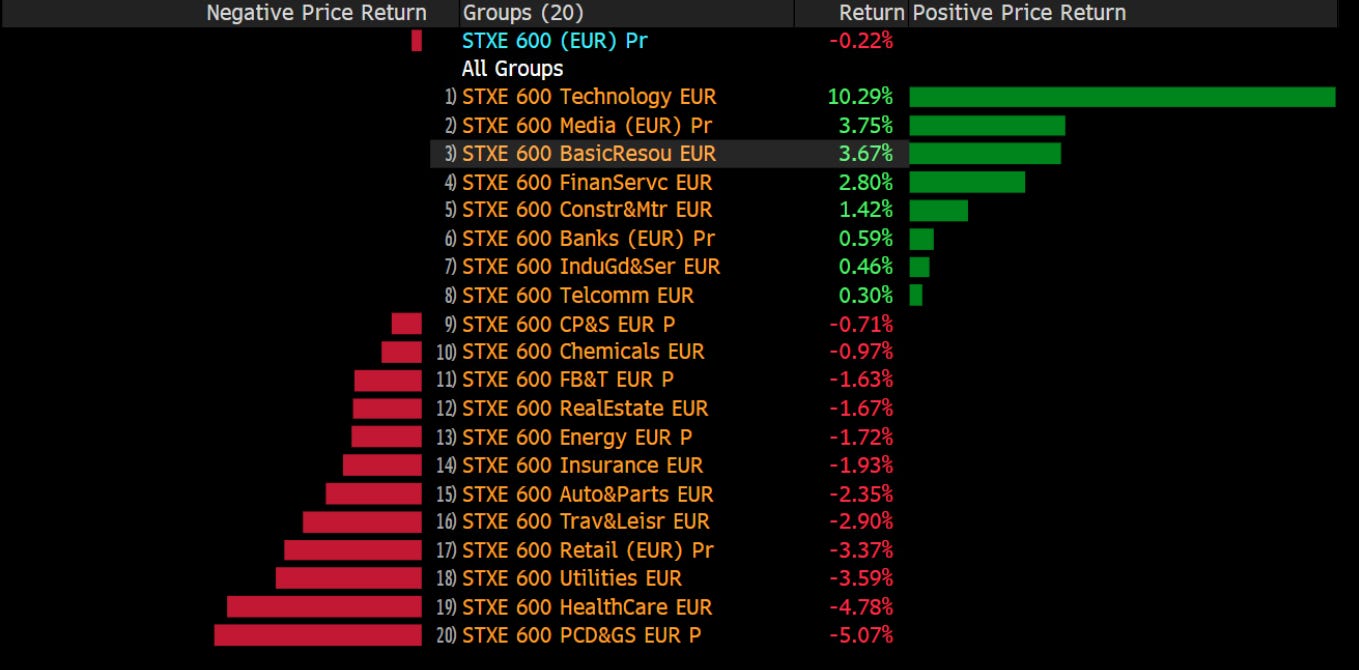

Speaking about “Left for Dead”, European stocks seem to be the big losers out of this Iran conflict. Check out this chart which I showed in a popular LinkedIn post (click here) on Friday:

What’s pulling European stocks lower? Curiously, more defensive sectors such as retailers, health care and utilities amongst others:

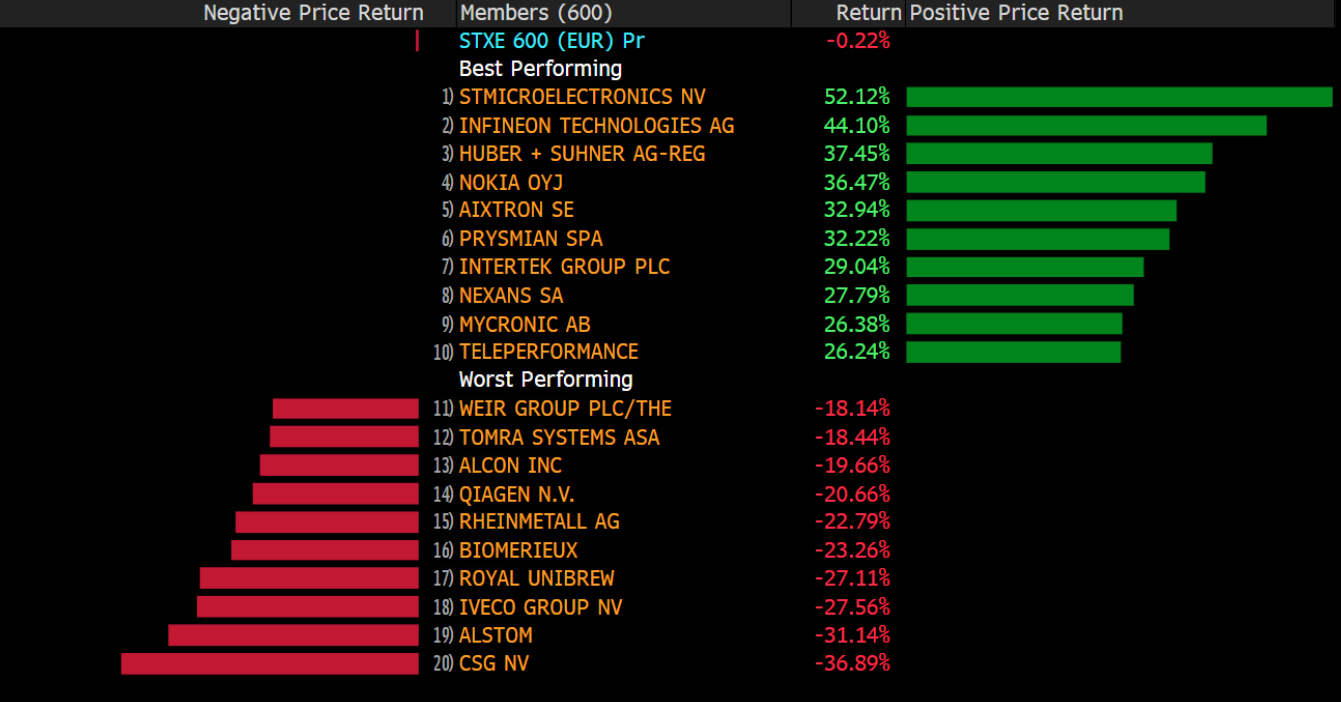

Surprisingly enough, defense stocks have not been helping either:

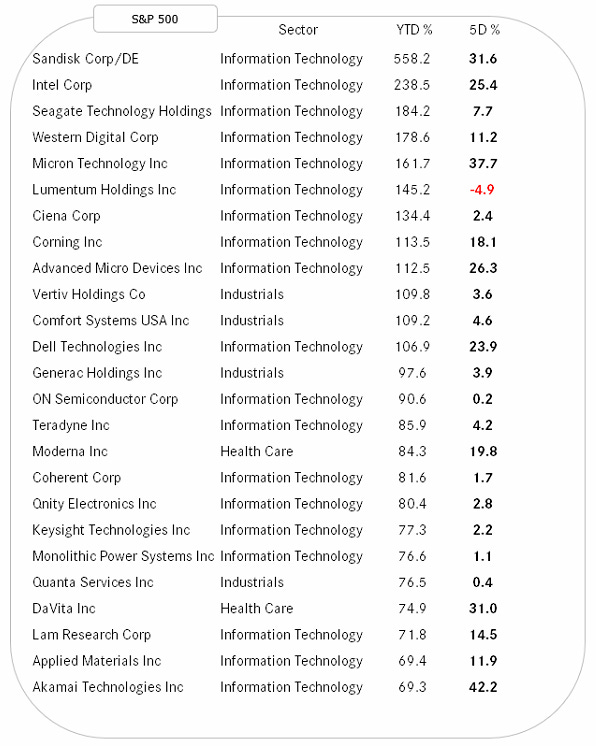

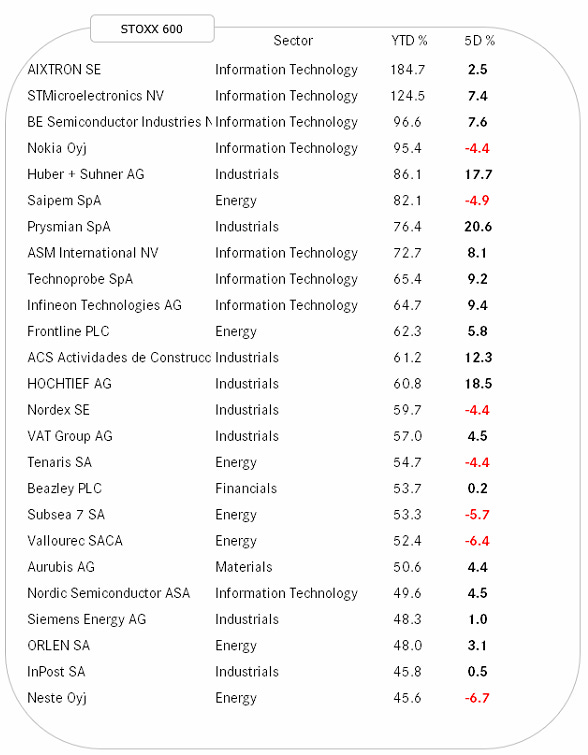

And as we are talking individual stocks, let’s have our usual weekly look at the best performing stocks year-to-date in the US (SPX) and Europe (SXXP) and see how they have fared over the past five trading session.

A little note of caution … the rightmost column in the table below is really only the percentage performance over the past week, not YTD or past 12 months!

Weekly returns for the top performing European stocks this year were a bit more normal, unless you are Prysmian or Hochtief or ACS …

Meanwhile, in the wonderful world of interest rates, bond yields continue to be stubbornly elevated. Starting with a look at the US 10-year US Treasury yield, we note that at 4.40ish the yield continues to move within our predefined triangle pattern, which is usually a trend-continuation pattern and where we expect a break out over the coming three to six months:

Albeit, at 3%-ish nominally lower, European rates, as usual proxied via the German 10-year Bund yield, have already broken out to the upside:

The political upheaval happening in the UK at the moment is fully expressing itself in the countries long-term (30Y) Gilt yields, which now have the lamentable distinction of being the highest out of the G-10 neighbourhood:

At 5.63 this morning, the 30-year Gilt yield is at a level not seen since Summer of 1998. That’s a long time ago:

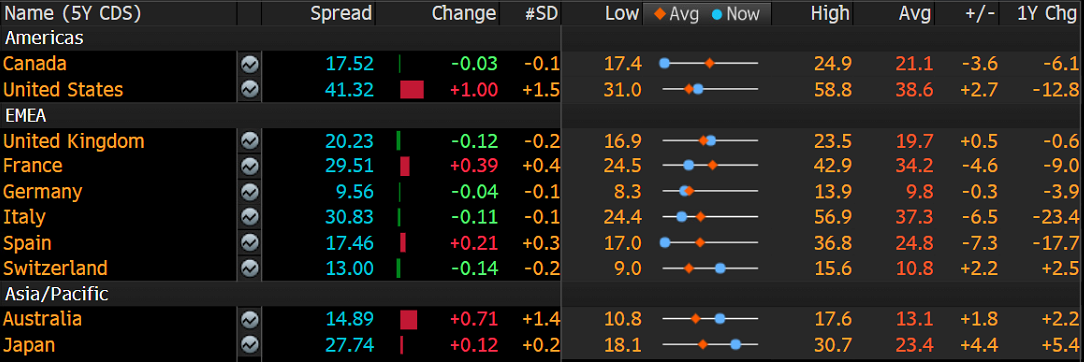

Surprisingly though, is the UK’s Credit Default Swap (CDS) rate far from being the highest:

Speaking of CDS rates, here’s one country that has seen its CDS nearly double before calming down again:

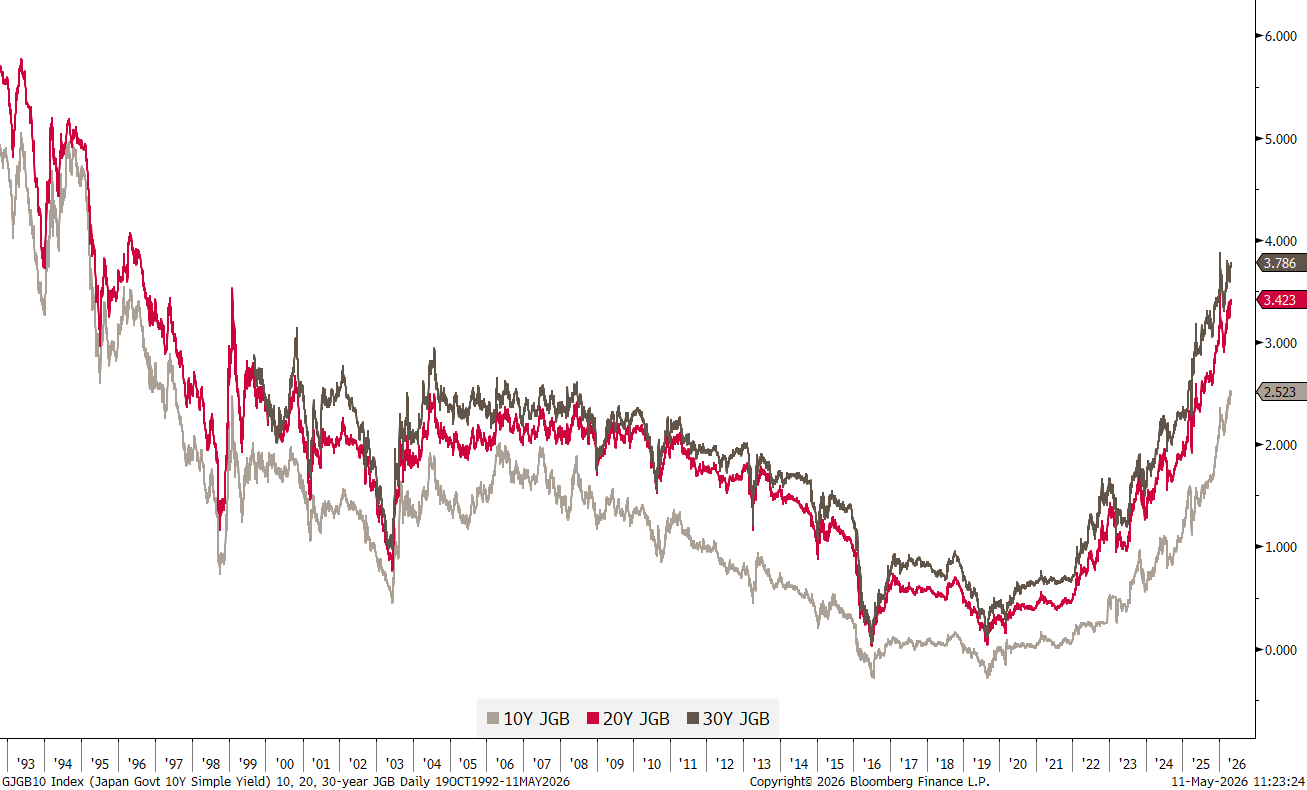

But back to bond yields, where in Japan the upside pressure on JGB yields continues to be relentless:

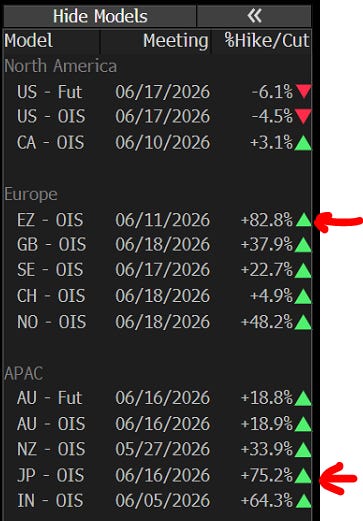

From a monetary poilicy point of view, only the ECB and the BoJ are expected to maybe move at their respective next meetings:

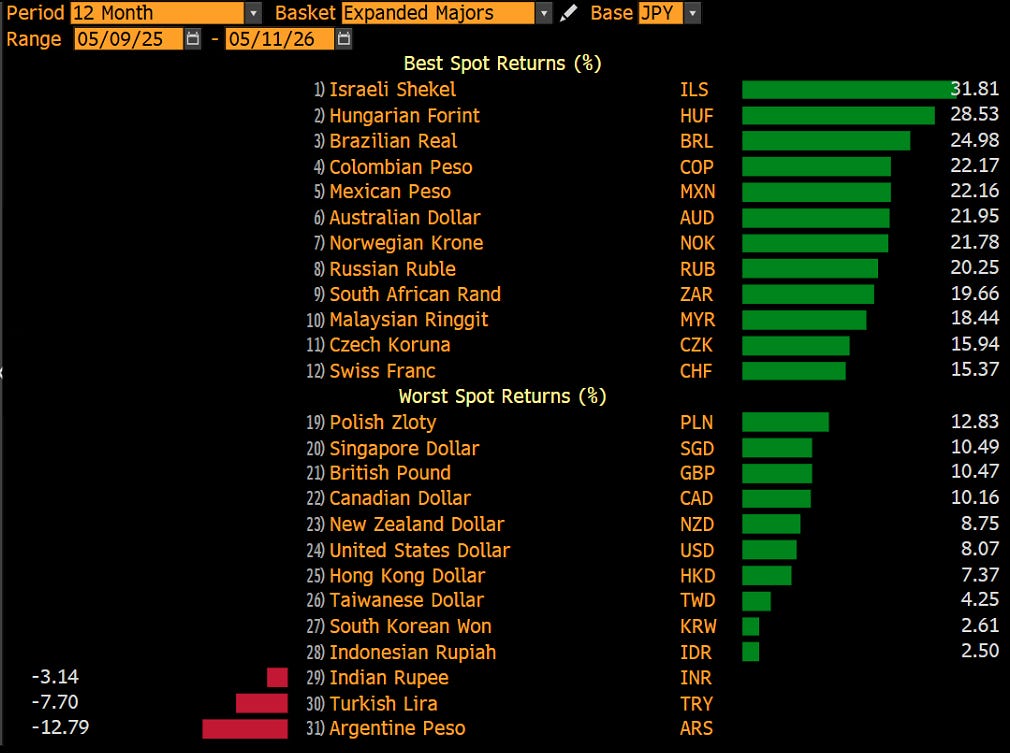

Moving over into the currency space, we note that the US Dollar has continued to lose ground versus other major currencies:

Thought the EUR/USD cross remains largely range-bound, it ‘feels’ like an upside breakout attempt may lay ahead in the coming weeks:

For the Bank of Japan and the USD/JPY rate it seems that “third time's a charm”, as the third intervention by the MoF finallly seems to have brought Yen-short speculators to their knees:

And speaking of the JPY, over a 12-month horizon, that currency is weaker against nearly every other currency,

which could partially explain the renaissance of the Japanese economy, not least expressed in the stock market:

Finally, just a quick glance at the cryptocurrency space, where Bitcoin seems to be quietly moving higher:

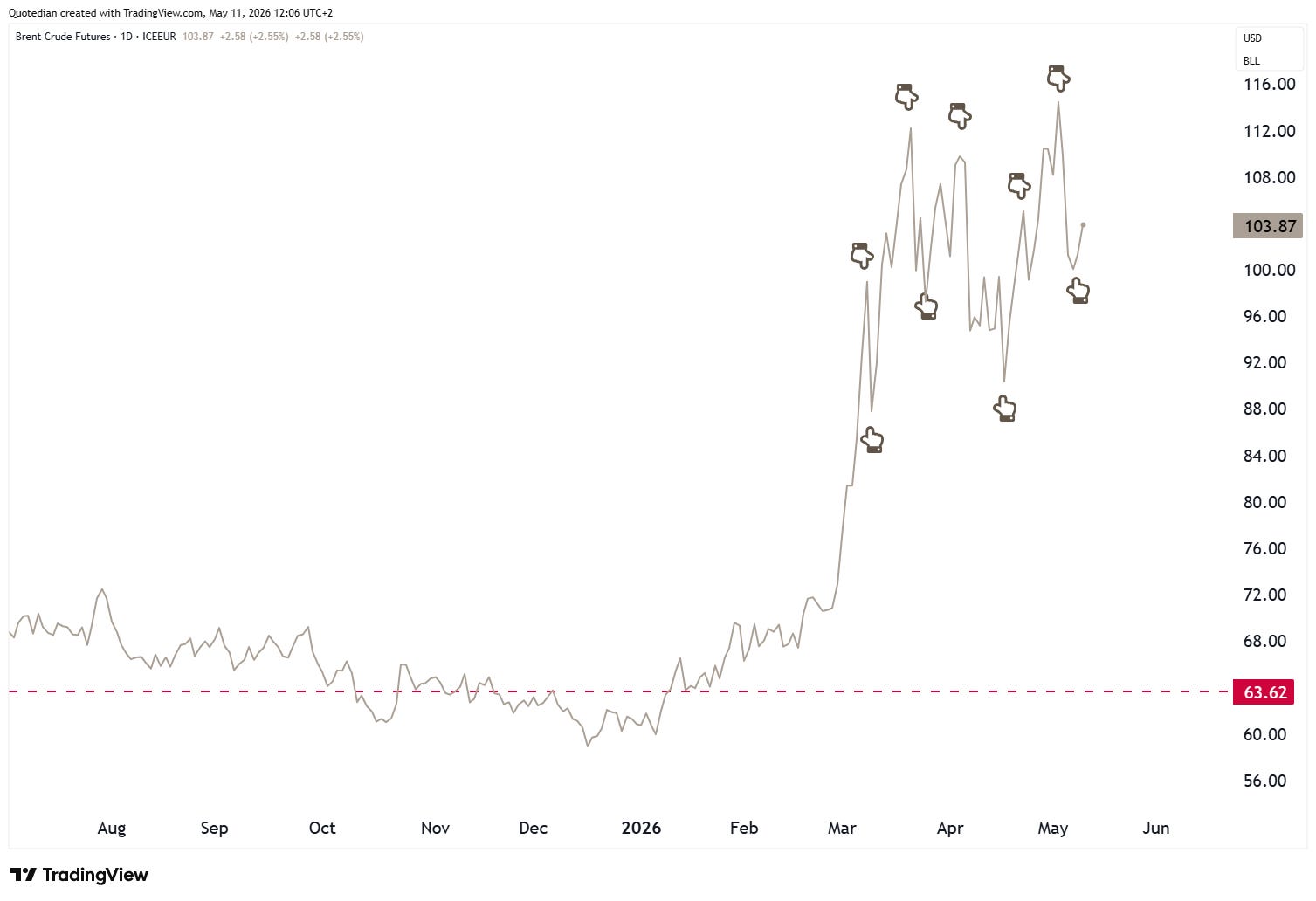

Over to commodities, where oil is exposed to the “wax on, wax off”, sorry the “war on, war off” seesaw:

Homer comes to mind here:

Gold’s direction is clearly unclear here, my best guess remains for a multi-month, wide trading range:

The only thing I would observe how Gold behaves during the Xi-Trump meeting later this week. Not a forecast, but it could be interesting to see if China tries to further undermine the US Dollar’s global hegemony, as they had on May 2nd by refusing to adhere to US sanctions on Iran. Watch this space…

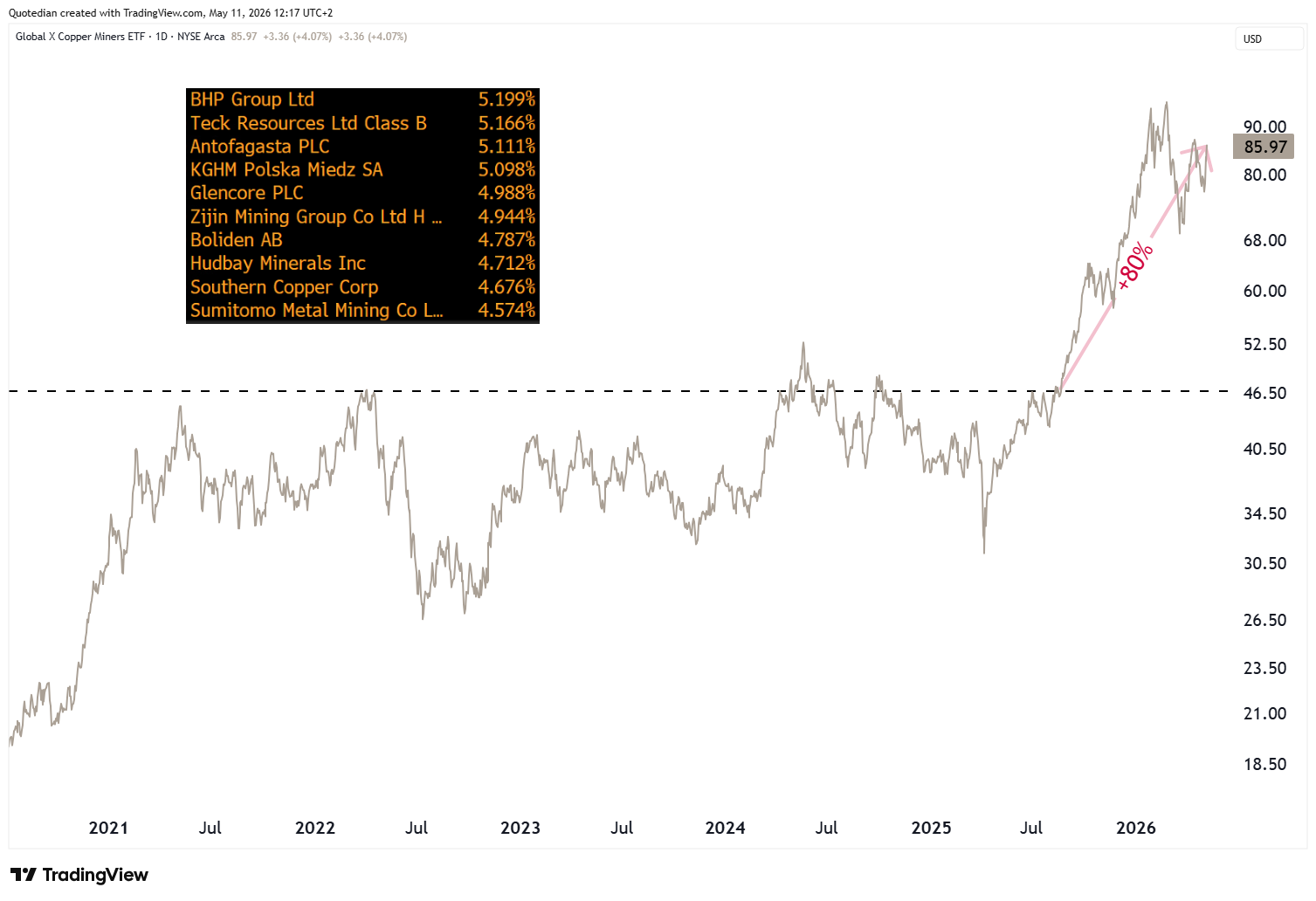

One metal I do really like here is Copper. The chart looks very constructive on the short term,

as much as on the longer-term:

A good way to ‘play’ the highe copper price continues to be via the Global X Copper ETF:

Whilst it is up meaningfully already since the clear break higher in August of last year, it has not followed the underlying’s metal recent rise to new all-time highs.

Whilst Earnings Per Share (EPS) have been soaring this earnings season, certain segments of the market seem to be getting a bit ahead of themselves

However, always remember: THE TREND IS YOUR FRIEND UNTIL THE END RIGHT AT THE BEND

Nevertheless, look for ‘laggards’ instead of piling to heavily in already strongly advanced stocks

Bond yields remain stubbornly high, which keeps the Fed from cutting and may force the ECB to hike

The US Dollar should resume its downtrend again soon

Gold’s moment to shine is over for the time being, consider purchasing the break in the red metal and associated copper stocks.

With all that out of the way, May the Trend be with You

AND

To infinity and beyond!!

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG