Whale Watching

Volume V, Issue 163

“An empty wagon makes the loudest noise.”

— Joe Frazier

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

Remember we used on several occasions in the past the saying that the (equity) tail is wagging the (bond) dog? Well, there’s potential now that the (crypto) fleece will make the tail and dog jump up and down. The crypto saga continues …

With Binance (CZ) likely pulling out of the FTX (SBF) bail-out, the latter is quickly turning into a big fish in the famous dynamite fishing analogy. Maybe it is even a whale, a Humpback in our illustrative table above. But it is unlikely to be the biggest whale going belly up in this round. Maybe Microstrategy Inc (MSTR / -20.8%), the guys who put their entire cash balance sheet into Bitcoin and then issued convertible debt to buy more of that very same cryptocurrency, will finally cave in. That could be a Sperm Whale (and whoever listened to the company’s CEO Michael Saylor over the past years would probably agree on the name giving …). But the true honour and potential for a blue whale (if there’s any) is likely to fall, as usual on someone in the financial sector. Let’s keep spotting …

On to yesterday’s markets …

A pretty dull session most of the day for equities until some crypto-related liquidation panic started feeding on itself and pushed the major US indices two percent lower into the close. Here’s the S&P 500:

Volume was higher than in the previous two ‘up’ sessions, which is a small yellow flag. Breadth was very weak, with over 90% of the stocks in the S&P 500 down on the day. All eleven sectors in the same index were down on the day, with Energy down most and Utilities and Health Care providing some relative shelter:

Of course, this left our whale-spotting ground looking more like the Red Sea than a Blue Ocean:

With today’s release of CPI, which courtesy of the Fed has become of such a (largely unjustified) focus to investors nowadays, I will not indulge in trying to overinterpret the charts today. A reading of 7.9% or less should spark a rally, whilst anything north of that will likely make investors take some chips off the table again. And those may be quite a few chips, as the current seasonal rally has been well-telegraphed (not least in this space). Manage your risk and remember, nothing ever good happens below the 200-day moving average …

This early Thursday morning, Asian markets continue on Wall Street’s template of lower prices, with most markets dropping around the one percent mark. US equity futures are flat, whilst their European counterparts point to a lower opening (having missed most of Street’s sell-off last night).

Fixed-income markets had a bit of a strange day yesterday, where US yields moved sideways most of the day and the 10-year Treasury had one of its weakest auctions in many years. Then, yields slipped quickly lower right around the time the exchange close, maybe propelled lower by comments of Chicago President Evans that the FOMC should slow its hiking pace. Here’s the intraday-chart of US 10-year yield futures:

On a daily chart, rates start feeling a bit toppish,

but, again, with the CPI due today I would not hold any near-term waggers on this one.

Applying some chart voodoo, the divergence between price and momentum indicator (green arrows) is holding up so far, as yields failed to put in a new cycle high (…for now…):

Credit spreads ticked a notch higher yesterday, but the overall trend remains one of downwards consolidation:

Even though the iShares Corporate High Yield ETF does not really reflect this overall spread tightening, being only about one percent away from making a new cycle low:

That is definitely worth further observation and I will comment in a future Quotedian. So, if you are not subscribed yet, do this right here and now in order not to miss any of the daily mailings:

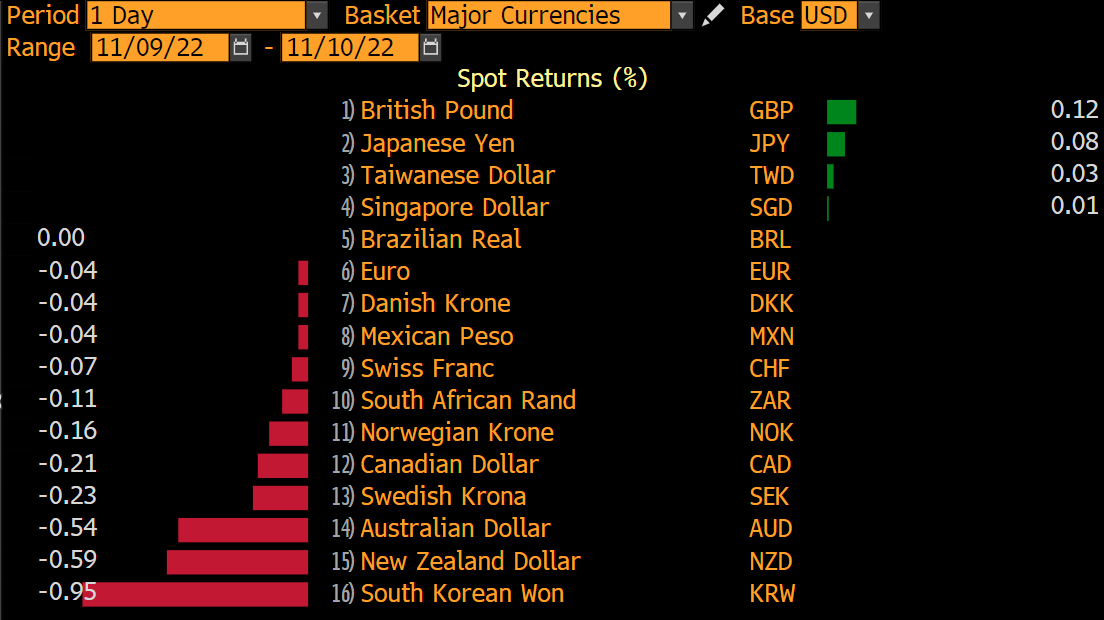

In currency markets it will come as no surprise that with risk-off ruling the US Dollar had a strong day against most major currencies:

This means that the US Dollar Index (DXY) has held for now above our wide but all-important trend-pivot zone of 108.50-109.50 (grey-shaded):

And then there are cryptocurrencies of course. And also, of course, they are facing the strongest liquidation activity.

Bitcoin, down 16% yesterday, has broken any reasonable zone of support and 13,000 could well be on the books. In crypto terms, that’s like a two-day move …max!

Ethereum, down some 30% in two sessions, may still have some support around the $1,000 level:

In any case, nothing nice here.

Finally, in the commodity complex, it has been more down than up over the past 24 hours, maybe partially due to a stronger dollar, partially due to growth worries or also just some liquidation:

I have grown quite bullish on Gold here, not least because of the crypto meltdown. But for that reason to hold up, Gold has to follow through NOW on recent strength, otherwise, all momentum will vane:

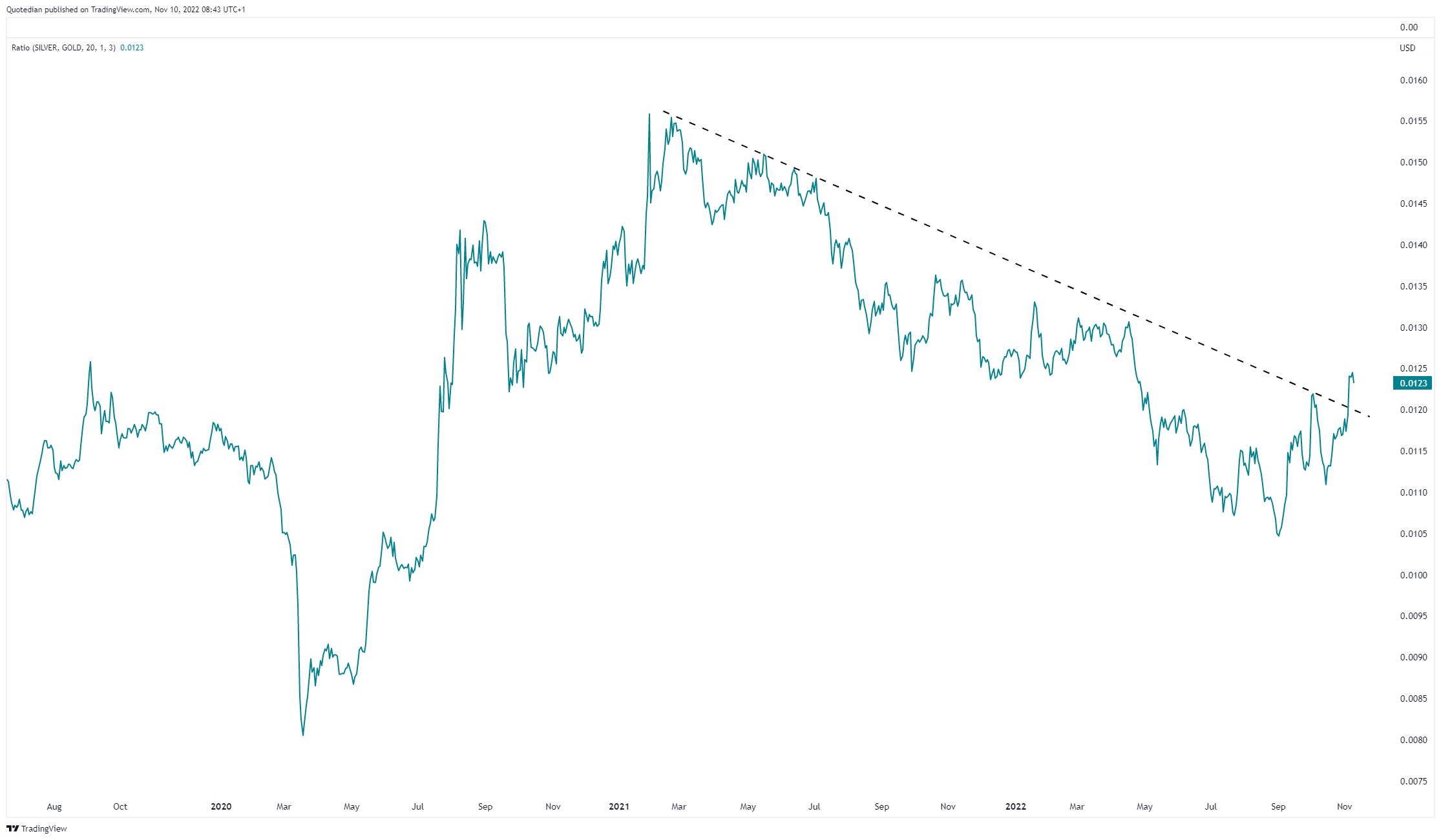

Maybe encouraging in that context is also the break-out of silver relative to gold, which tends to happen when both metals are on the rise:

Ok, ‘nuff said and time to hit the send button. Let’s see what levels await us tomorrow morning after this afternoon’s CPI. By the way, there is a good chance we will get 7.9% or “better”, so market reaction and follow-through will be even more interesting to observe.

Take care out there!

André

CHART OF THE DAY

The melt-down of higher duration stocks, here proxied via the Nasdaq-100, versus large cap stocks (S&P 500) is continuing. The question is: Where will it stop?

Thanks for reading The Quotedian! Subscribe for free to receive new posts and support my work.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance