You are here •

The Quotedian - Vol V, Issue 136

“I felt a great disturbance in the Force, as if millions of voices suddenly cried out in terror and were suddenly silenced.”

— Obi Wan Kenobi

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

Some housekeeping first - You can now access the entire archive of The Quotedian and/or subscribe to any future postings at www.thequotedian.com (i.o. using the Substack subdomain). In other words, we have our very own domain now! Spread the word!

Ok, to the markets, and quite frankly, there is so much going on, it is difficult to keep track. So, instead of lengthy deliberations, I will today focus more on providing you with a lot of charts, so that we don’t lose collective track of where we are.

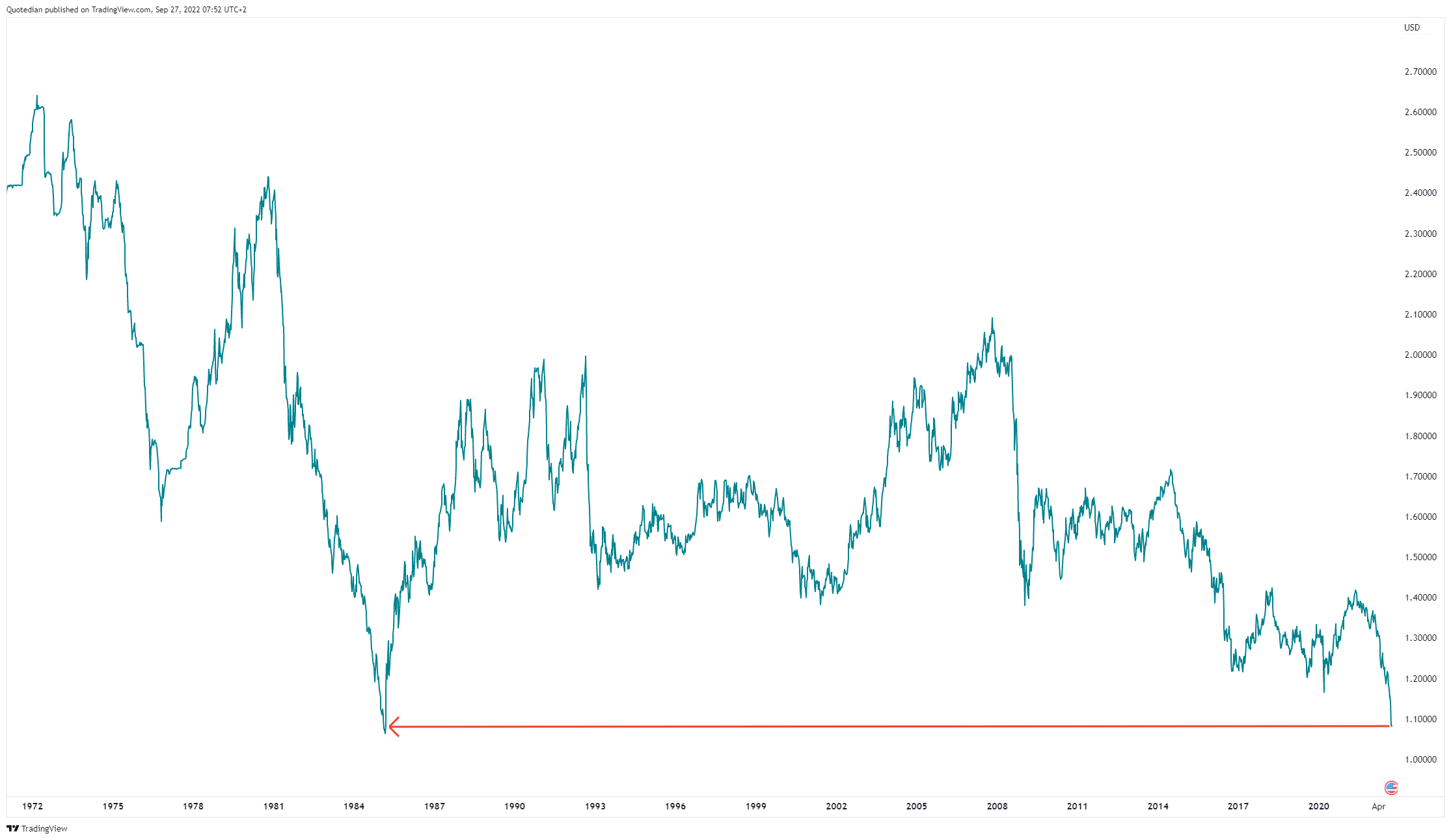

Breaking with the usual order of stocks, bonds, FX and commos, we start with currencies today, where the greatest disturbance to the force is taking place, especially so in the British Pound, which briefly undercut the previous all-time low set in 1985 during Asia’s session yesterday:

Just as a reminder: The Goonies, The Breakfast Club, Out of Africa and Teen Wolf were some of the movies of 1985 …

Zooming in, the question is whether this was the low (for now) or more immediate selling pressure to come. At a first glance, given the tremendous dip, despite taking place in the thinner volume Asian session, distance to MAs and an RSI reading at 15, it seems that at least a few days of relief could be on the books:

The detonator for the acceleration in the sell-off was of course Chancellor Kwasi Kwarteng’s lil’ fiscal package, which provoked this quite British reaction by the Bank of England governor Bailey:

“The Bank is monitoring developments in financial markets very closely in light of the significant repricing of financial assets.”

LOL.

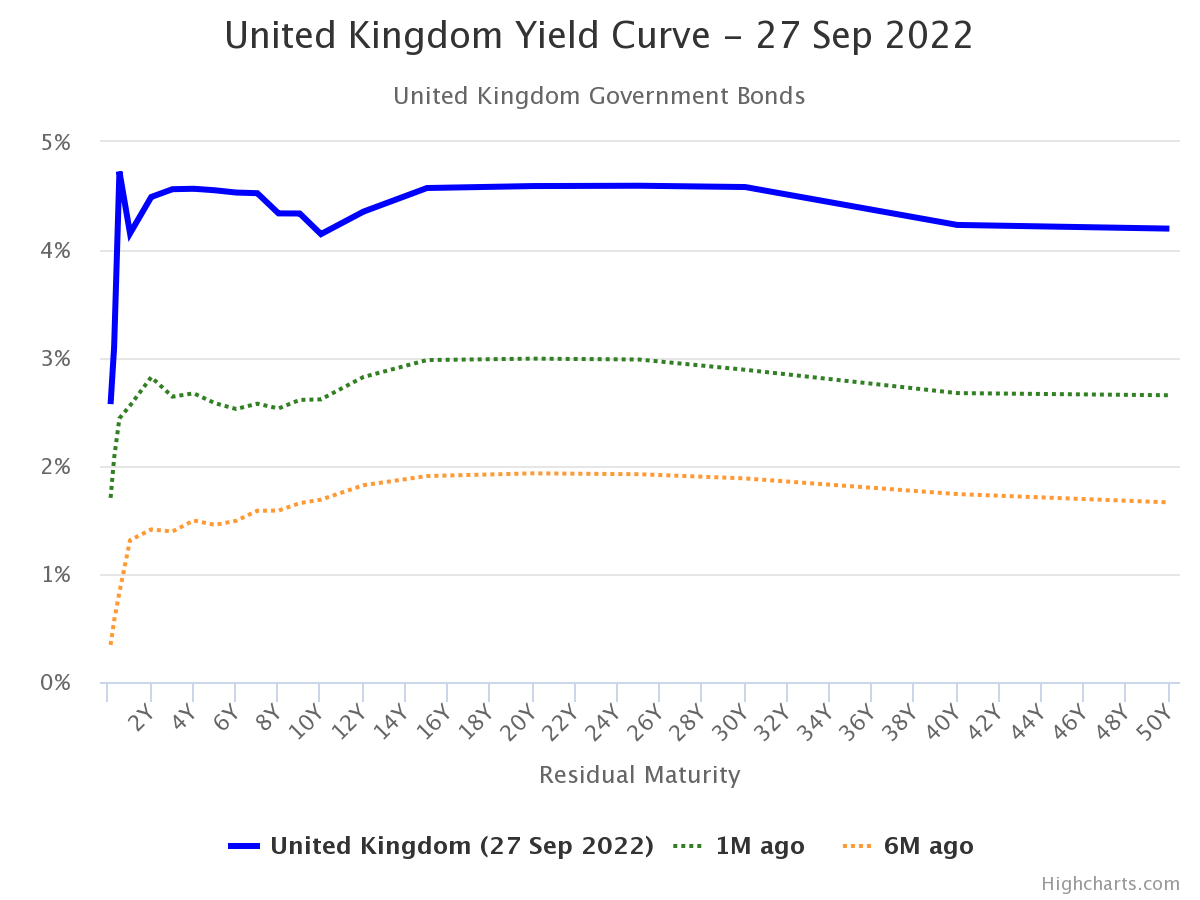

But the true bloodbath actually took place in Gilts, with yields shooting through the roof being a good indication of what the bond market thinks about the financing of that ‘fiscal event’:

In reference to yesterday’s Quotedian: OUCH, OUCH and OUCH!

Here’s the entire GBP Sovereign yield curve today compared to one and six months ago:

Impressive.

Ok, let’s move on, but we stay with currencies one more moment. I think I mentioned that EUR/USD shorts should be covered around 0.95 - an opportunity we may have missed as again, the sell-off into the vicinity of that level took place overnight (Sunday):

Without any major “unknown unknowns” over the coming weeks, I have no doubt that the Euro eventually will take out those lows, but for now, the odds for a relief rally have increased.

But, there are more FX markets worthwhile looking at, mostly in Asia and mostly courtesy of the Japanese Yen (or better said the BoJ and the Japanese MoF). Starting with the Yen itself, could somebody kindly enough point out where the FX intervention took place last week …

The weak Yen is creating regional competition fears, sending for example the Chinese Renminbi and the Korean Won lower too:

Ok, let’s move to equity markets, before all of you stock guys unsubscribe from this fine newsletter!

Equity markets also continued under siege yesterday, though for now the S&P 500 has held above the June lows - just about -

Once again, there were few places to hide, with nine stocks lower for the day for every stock trading higher on the S&P 500. Also, an eleven out of eleven for negative sector performance:

European equities, as measured by the STOXX 600 Europe index, need to turn around here and now:

Asian markets and Western index futures are giving hints of signs of our beloved Turnaround Tuesday at these early hours. Fingers crossed…

Going back to bonds briefly, of course, are not only UK yields pushing higher, but it is a globally observable ‘phenomena’. US 10-year yields are now scratching the belly of four percent, though the entire move starts looking somewhat parabolic, and we know that parabolic moves usually do not end in high, flat levels:

One interesting price to look at is the 5-year breakeven inflation rate, which is starting to head lower:

I will elaborate further on this in a future Quotedian, but basically, it could be a sign of (temporarily) topping yields (even without a Fed pivot).

On the commodity side of things, there is still a lot of price pressure on commodities for three main reasons (IMHO):

Commodities are measured in USD and the mighty Dollar has been, well, mighty

Commodity prices reflect recession and hence lowered demand fears

A lot of speculation has gone out of commos recently.

Let me try and elaborate on number three tomorrow, but point in case for bullet #1, I suggest you check today’s “Chart of the Day” below.

Ok, time to hit the send button, but just before we go, one more reflection here:

With all that has been going on and still is going on, the current market very much resembles the dynamite fishing scenario. The dynamite has come in various forms and shapes (e.g. geopolitical detonators, interest hike bombs, fiscal TNT, etc), and the fishes (growth stocks, Euro, Pound, Yen, bonds, etc) are popping up to the surface quickly. The question is: What will the whale be? [Given the size of the fish, the whale must be Moby Dick size minimum]

But anyway, do remember:

André

CHART OF THE DAY

This meme speaks to the sentiment of many of us - and just imagine how it must be for the true gold bugs:

But as mentioned in the deliberation section, this is actually only half the story. Most of us here on this list are actually NOT US Dollar based investors, so stop whining:

Thanks for reading The Quotedian! Subscribe for free to receive new posts and support my work.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance