You Can't Print Molecules

Vol IX, Issue 14 | A NPB Original

“For a successful technology, reality must take precedence over public relations, for Nature cannot be fooled.”

— Richard Feynman

This week’s Quotedian has a somewhat special format, as I will be showing you some of the key charts just published in Q2 outlook and its accompanying chart book. If you’d like a copy of either or both, do not hesitate to send me a personalised email to ahuwiler@npb-bank.ch with your request.

No other TL;DR than the above this week, so let’s dive right into our deliberations!

This is part of our executive summary:

Is this the easiest or the most difficult outlook the NPB Investment Committee had to put together? A bit of both. The Strait of Hormuz crisis has triggered a near-complete reset across markets, providing plenty to write about and plenty of fog to navigate. With information overload and uncertainty still elevated, markets have turned to trading the headlines.

We therefore take a step back to analyse the bigger picture, which has shifted materially over the past 20 months - and dramatically so over the past six weeks. All without losing sight of shorter-term allocations.

As we outlined in our previous outlook “Age of Empires”, the world has entered an era of multipolarity where resources are hoarded, not sold. And as US President Trump has just discovered, unlike in crises of the past three decades, you cannot print yourself out of trouble when the problem is physical, not financial - “You can’t print molecules”!

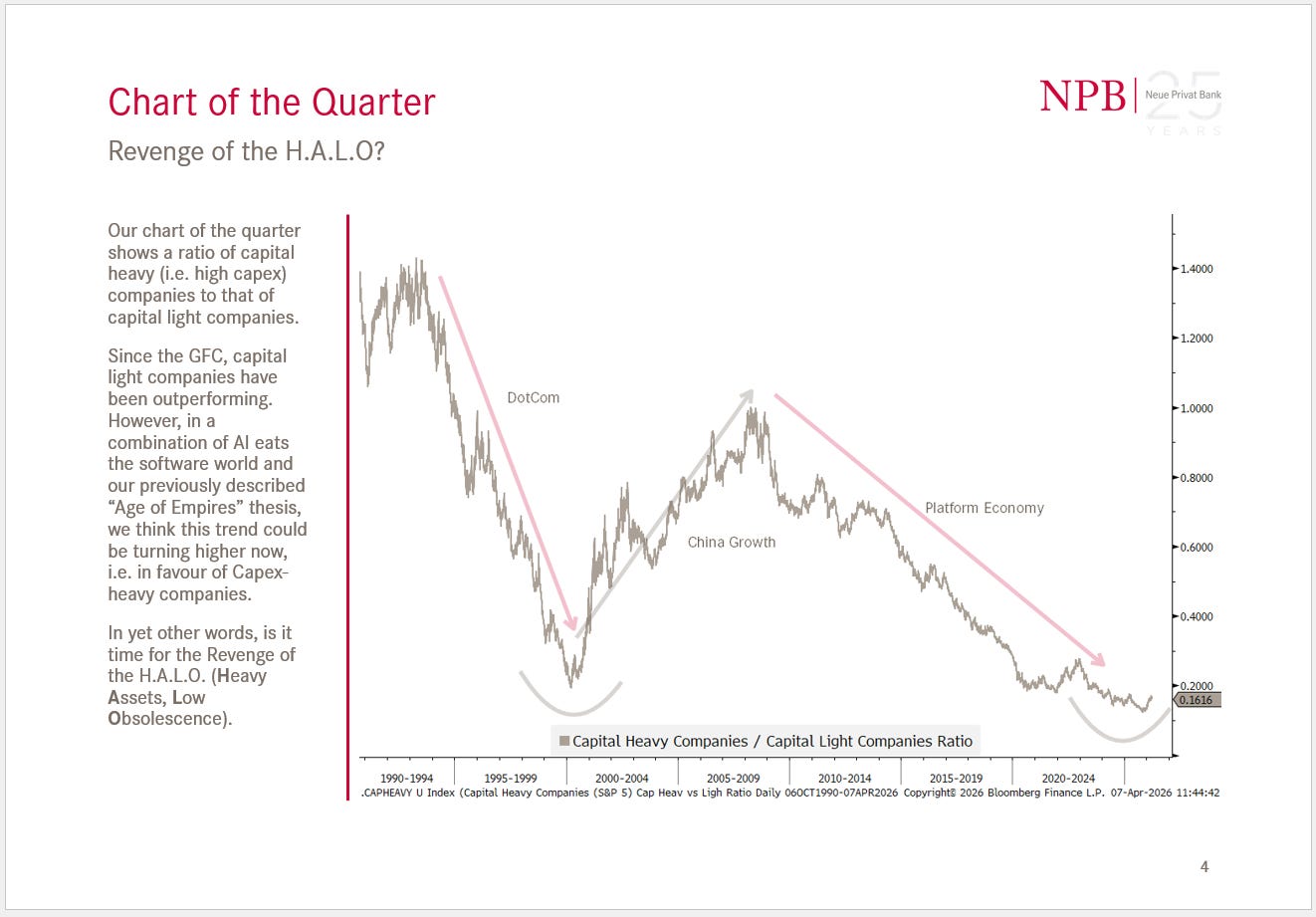

There is already a first investment implication from this, which we show in our “Chart of the Quarter”:

And if you wonder how I created the Cap Heavy / Cap Light indices to create the ratio in the chart above, you already know I believe in LdV’s SITUS:

Hence, the proxy for the capital light segment is or are simply information technology stocks. For the capital heavy index I equal-weighted following four sectors into an index:

Energy

Materials

Industrials

Utilities

Now, completely independently but not by coincidence, please check the top four ranked sectors on our aReS proprietary model:

Exactly!

Next our outlook went to ask the question whether with slowing growth,

and like rising inflation,

STAGFLATION is a true threat.

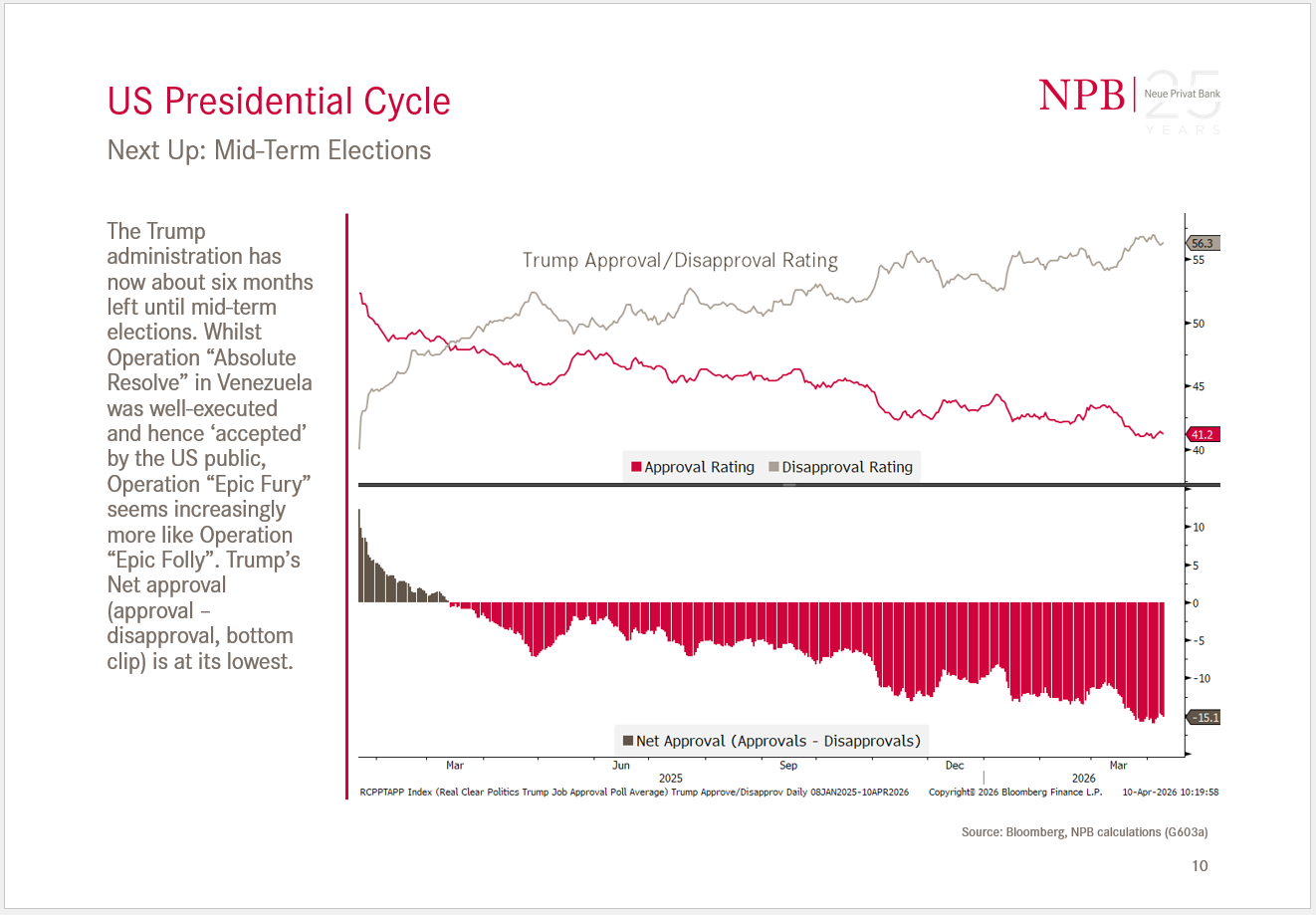

And we also discuss the upcoming mid-term election, now only some six months away, and for the Republicans to lose:

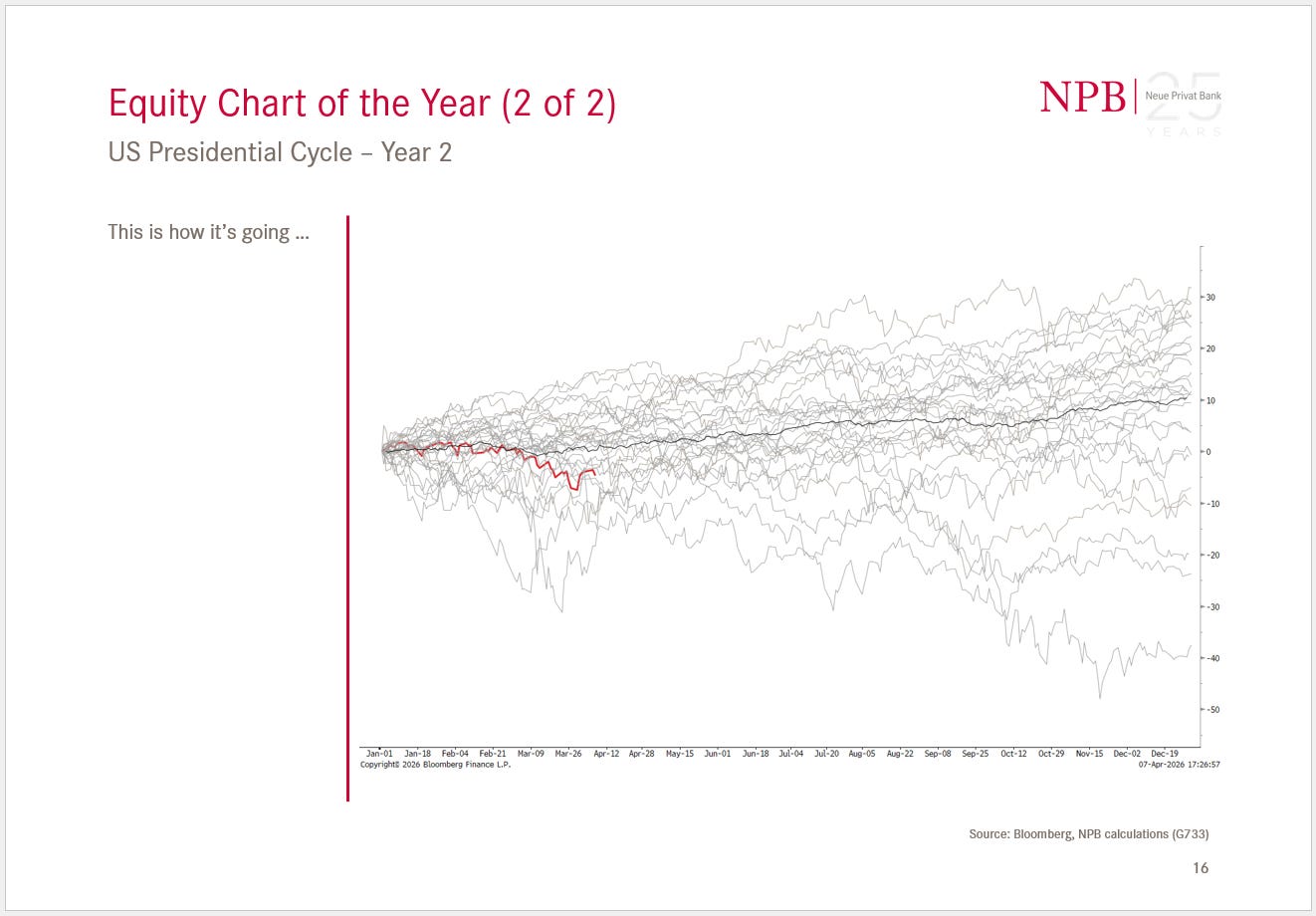

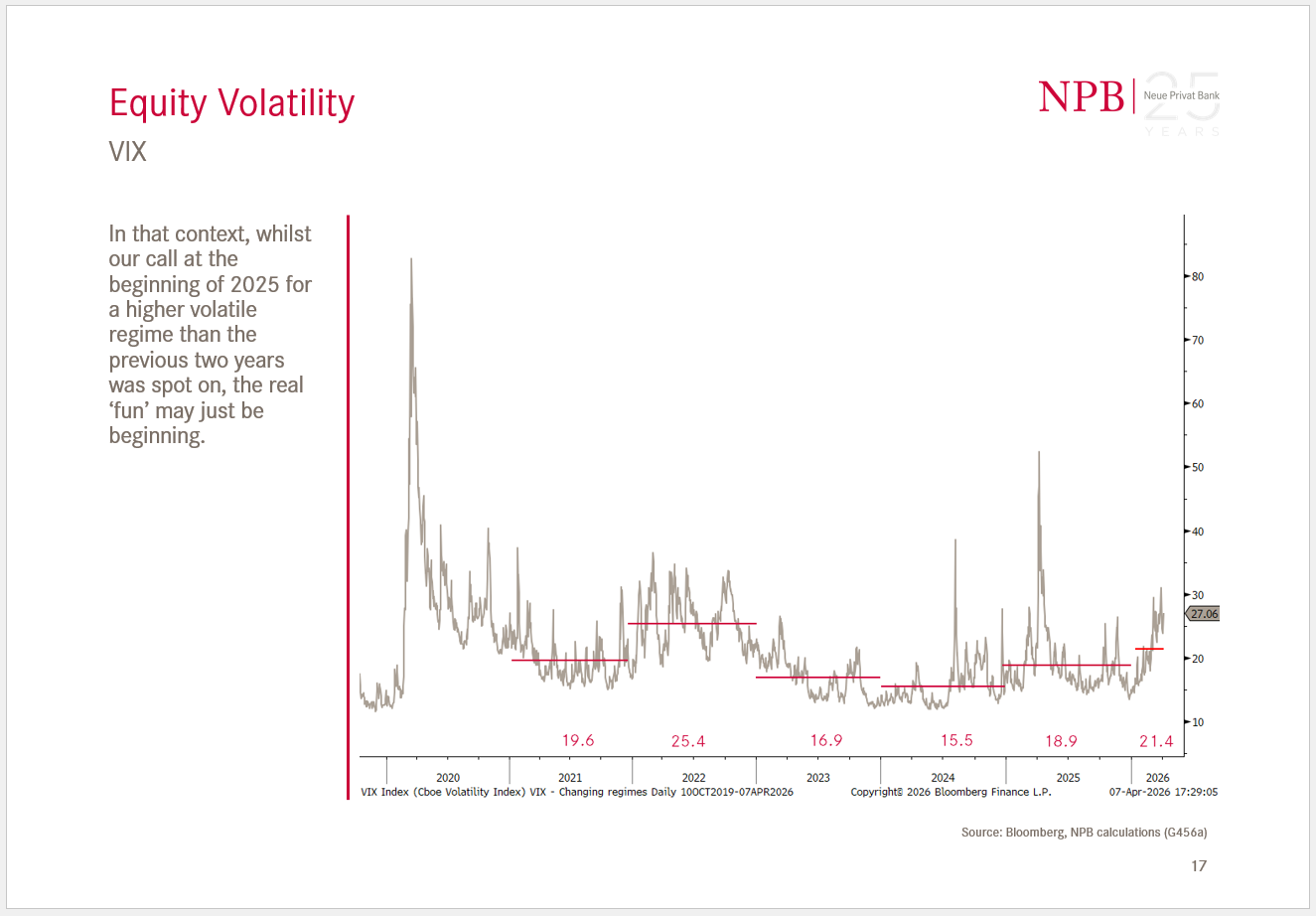

In the equity section, we discuss the difficult start to the year for equity markets,

and the increased volatility,

which is quite typical for the mid-term year in the US presidential cycle (see 2022 and 2026 above).

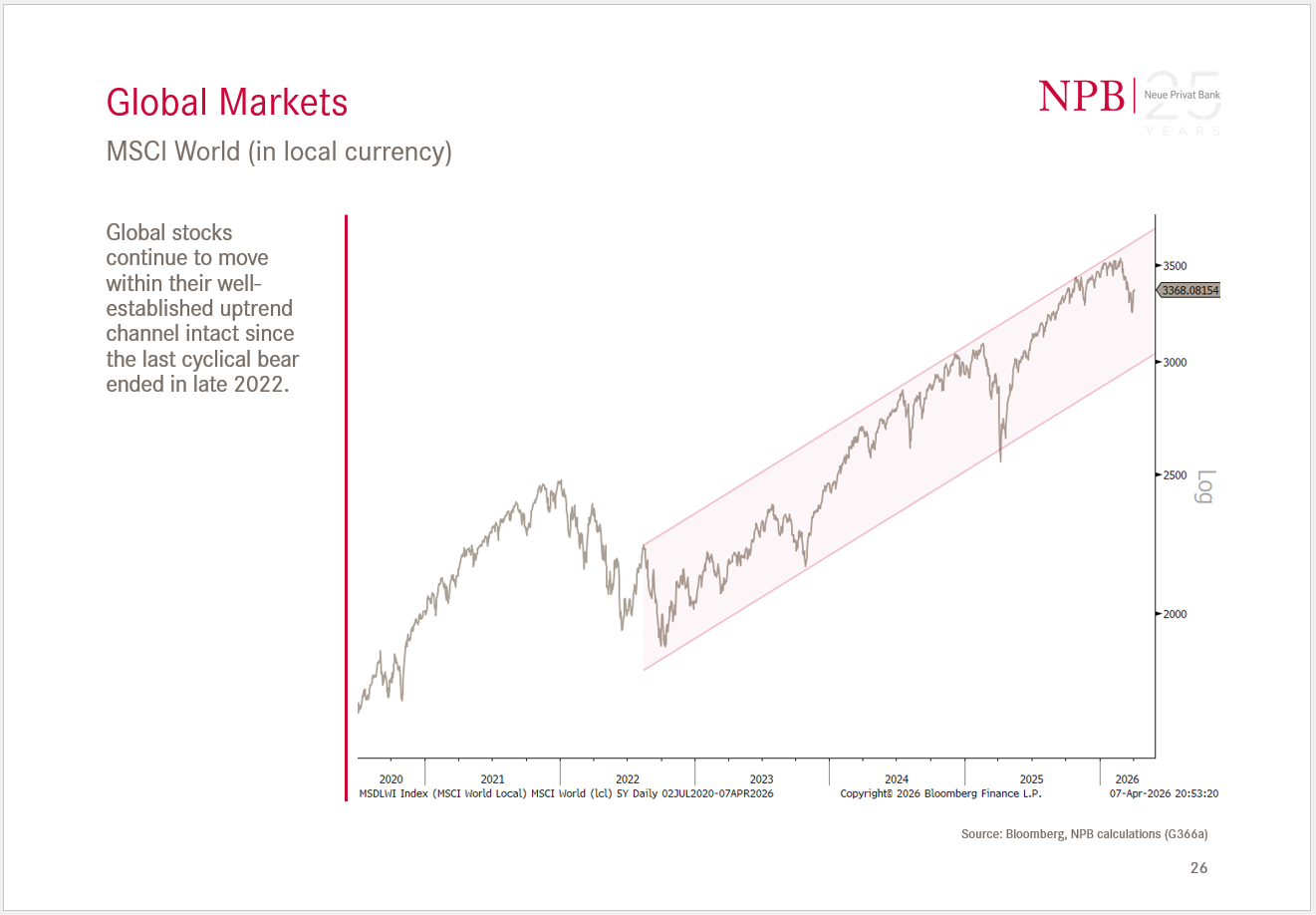

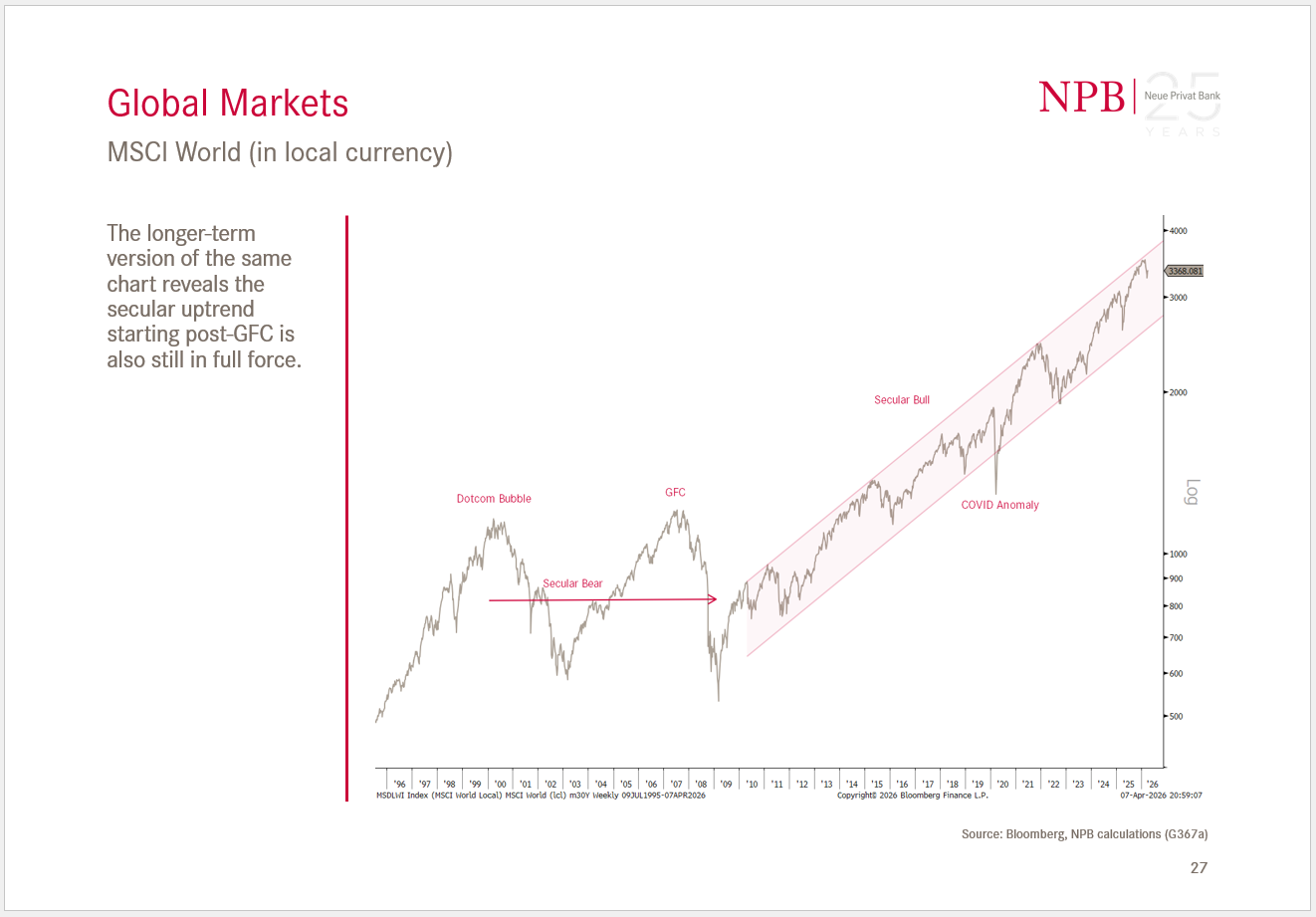

We observe that from a cyclical,

AND a secular point of view,

global stocks remain in an uptrend.

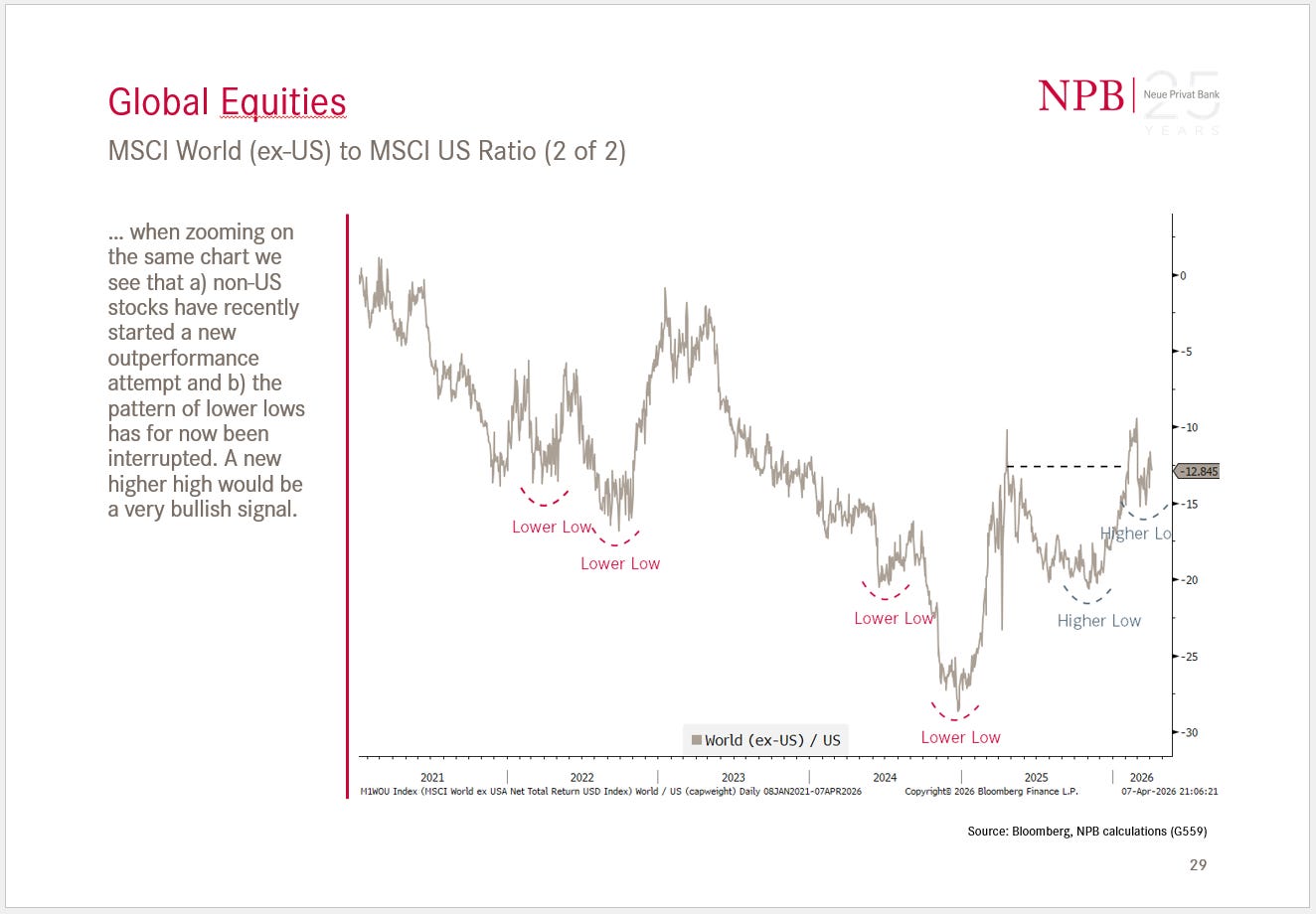

Plus, we also conclude that chances for the trend of Global stocks ex-US outperforming US stocks have increased, as we see a pattern of high lows and higher highs in the ratio between the two:

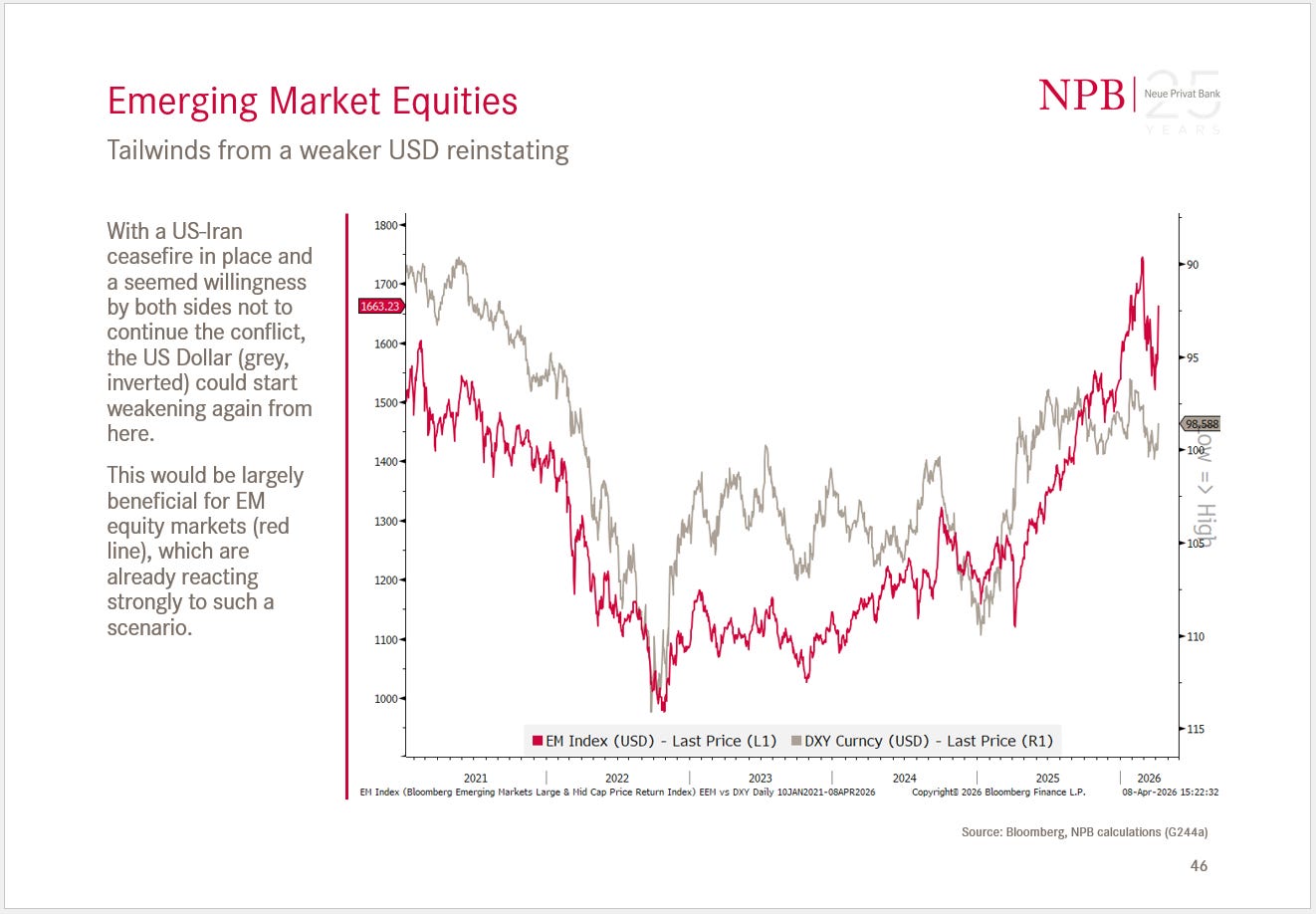

We also confirm our overweight of Emerging Market equities,

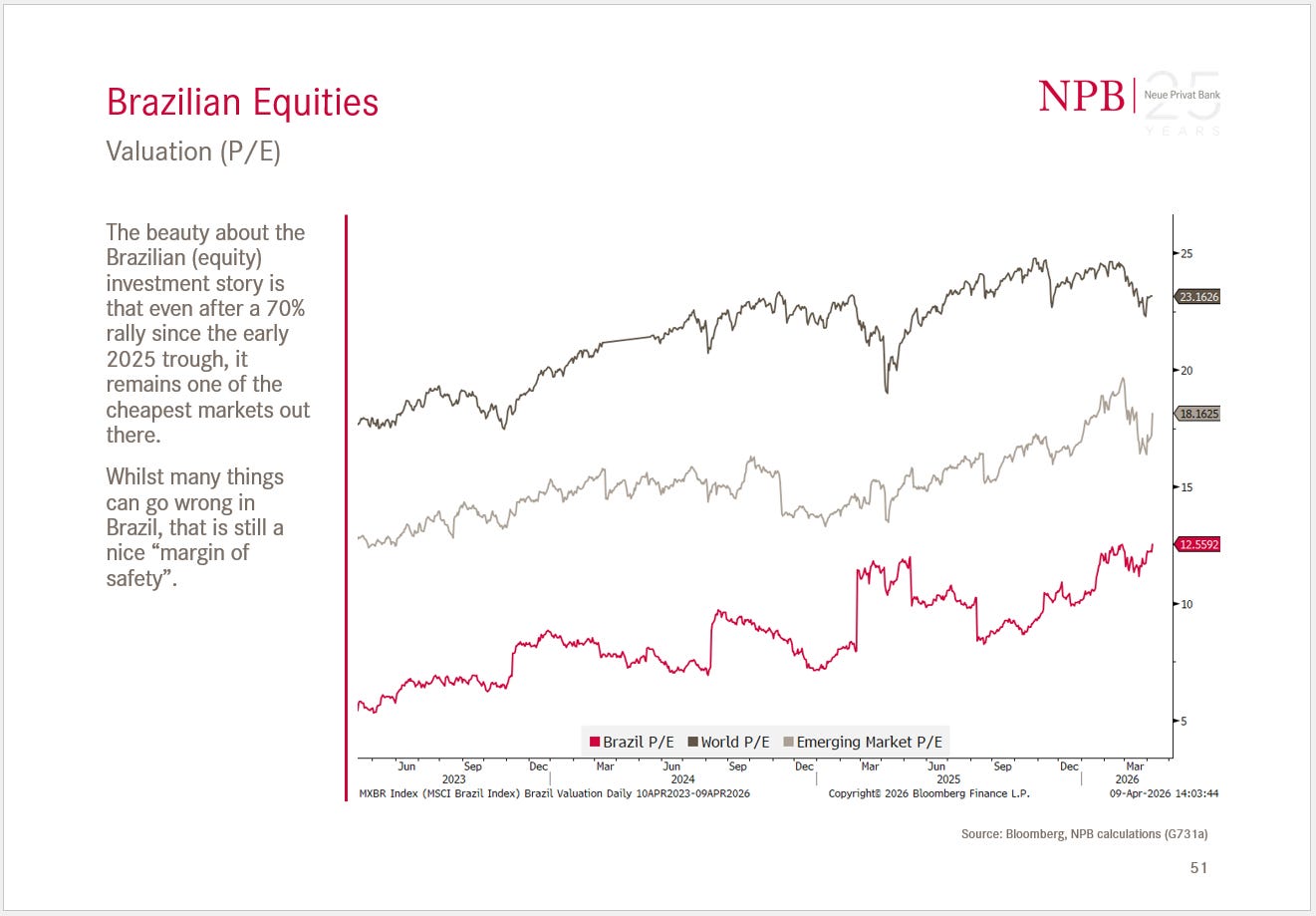

and highlight Brazilian stocks, which even after a massive 80%-plus rally since early 2025 are still not expensive in DM and EM comparison:

In the fixed income section, we wonder how that “Reservoir Dog”-like no one trusts no one between the main actors will end:

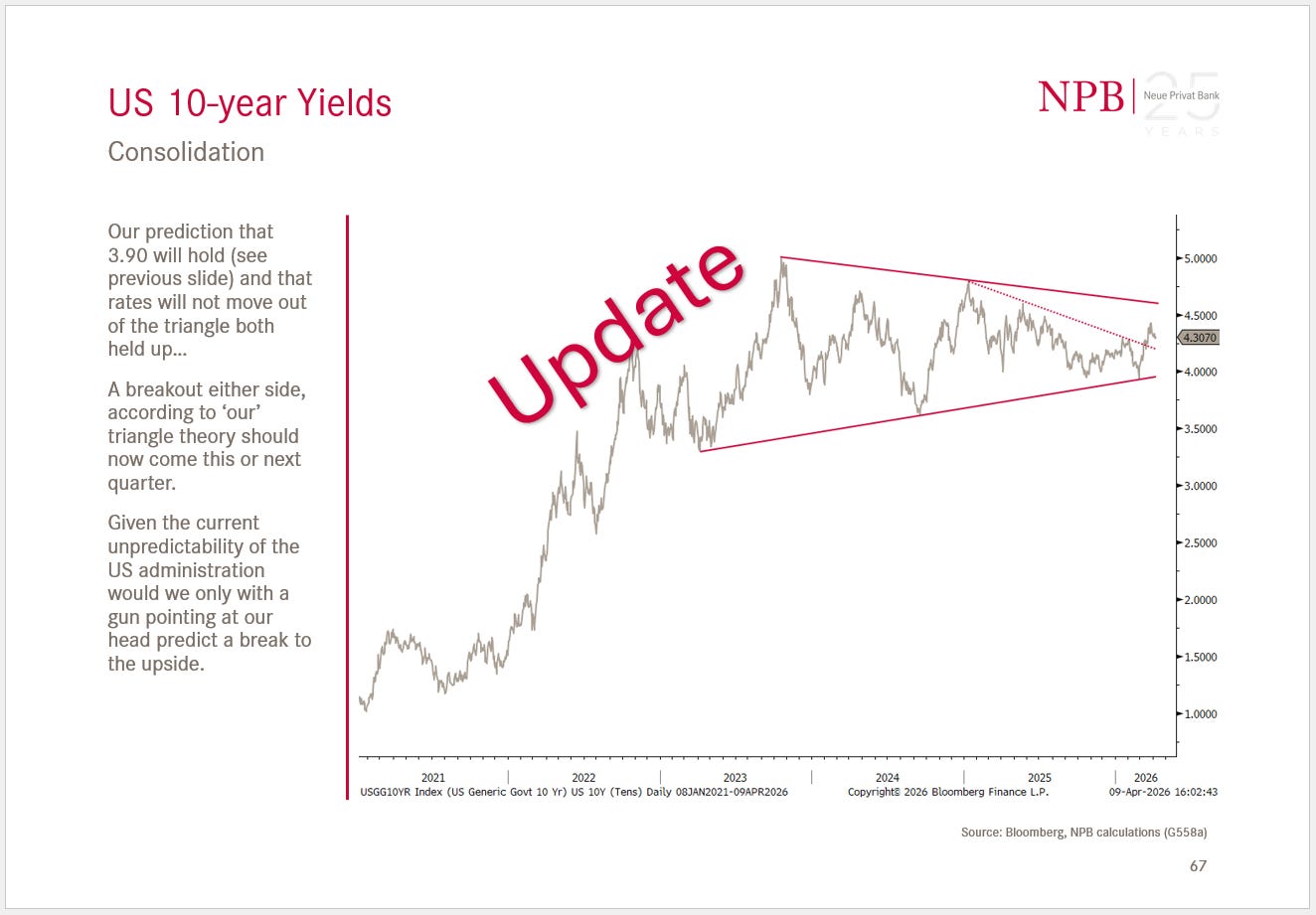

We show that US 10-year yields are for now continuing to follow the (technical analysis) script, which does not allow rates to break out either side of the triangle and next quarter earliest:

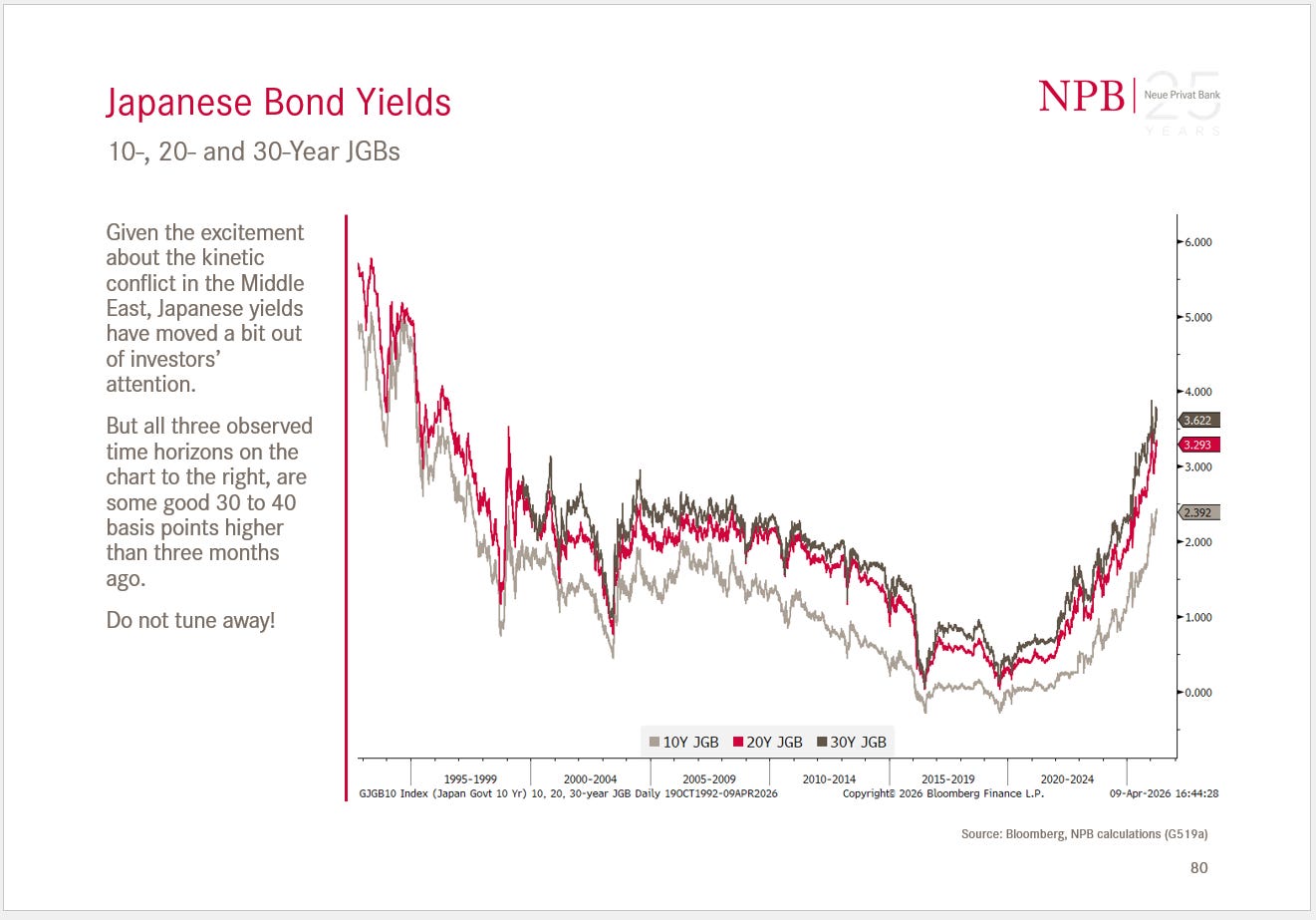

Also, we set a reminder that nobody should forget Japanese yields, as they continue to move higher and possible threaten the largest carry-trade this universe has known:

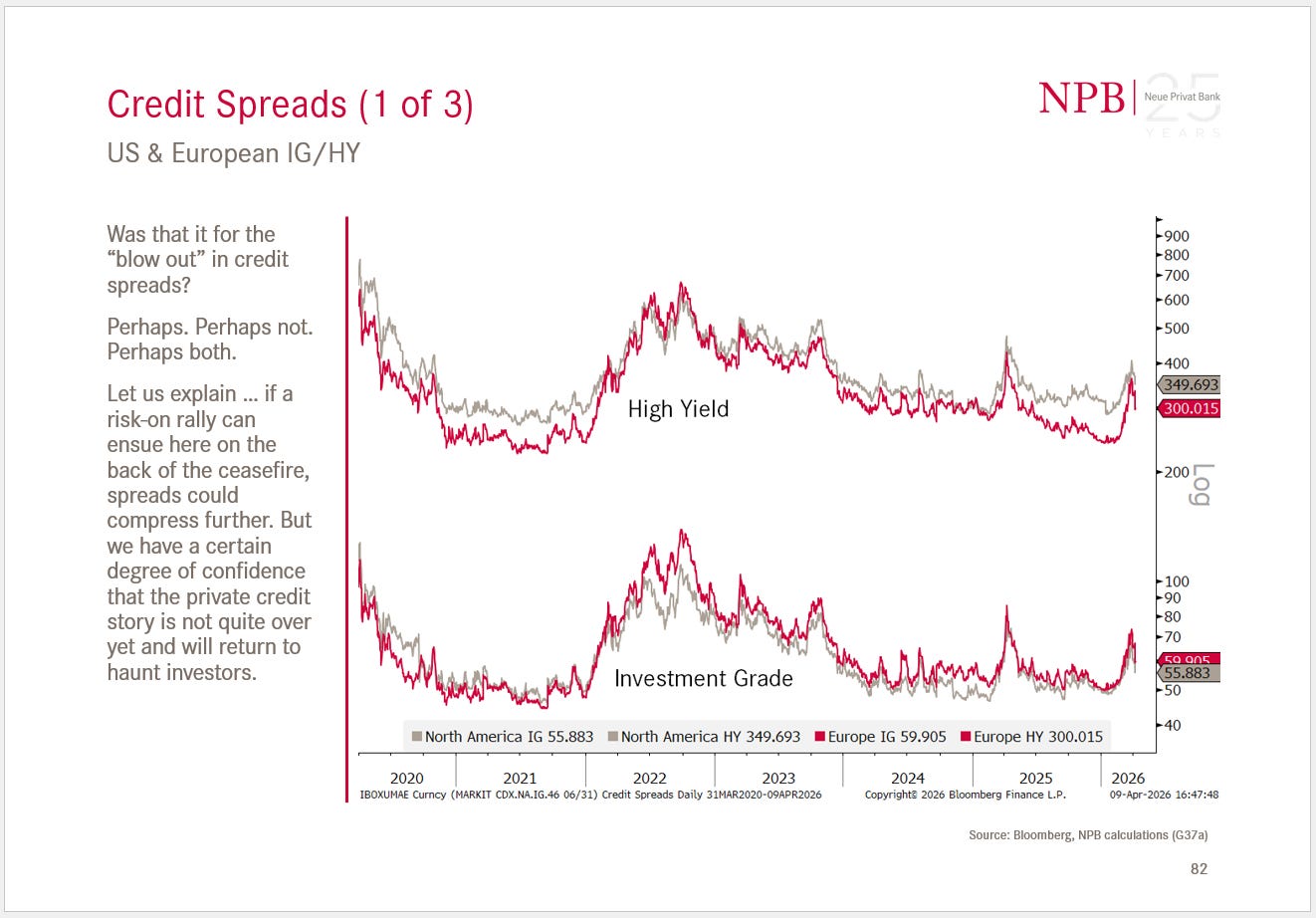

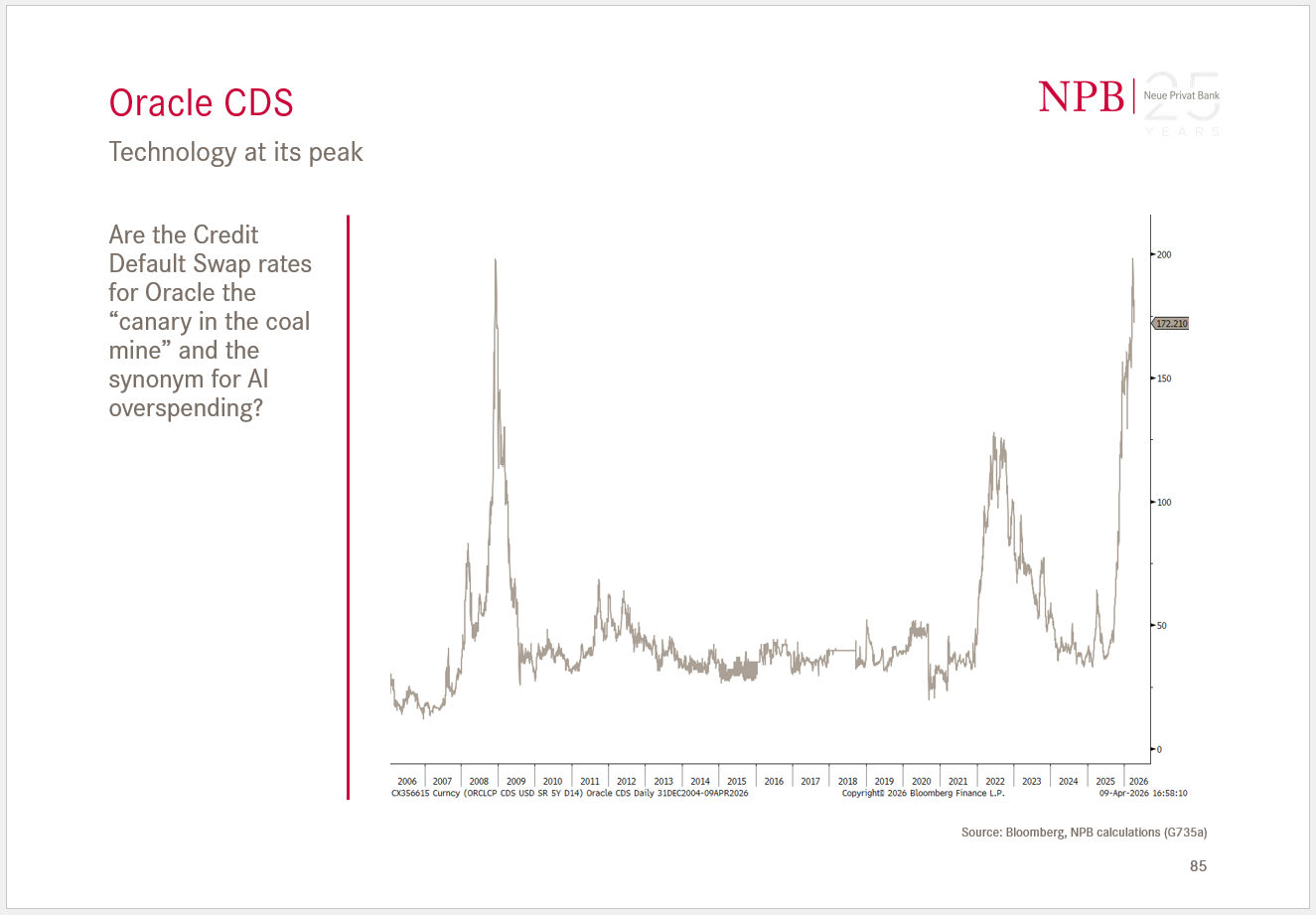

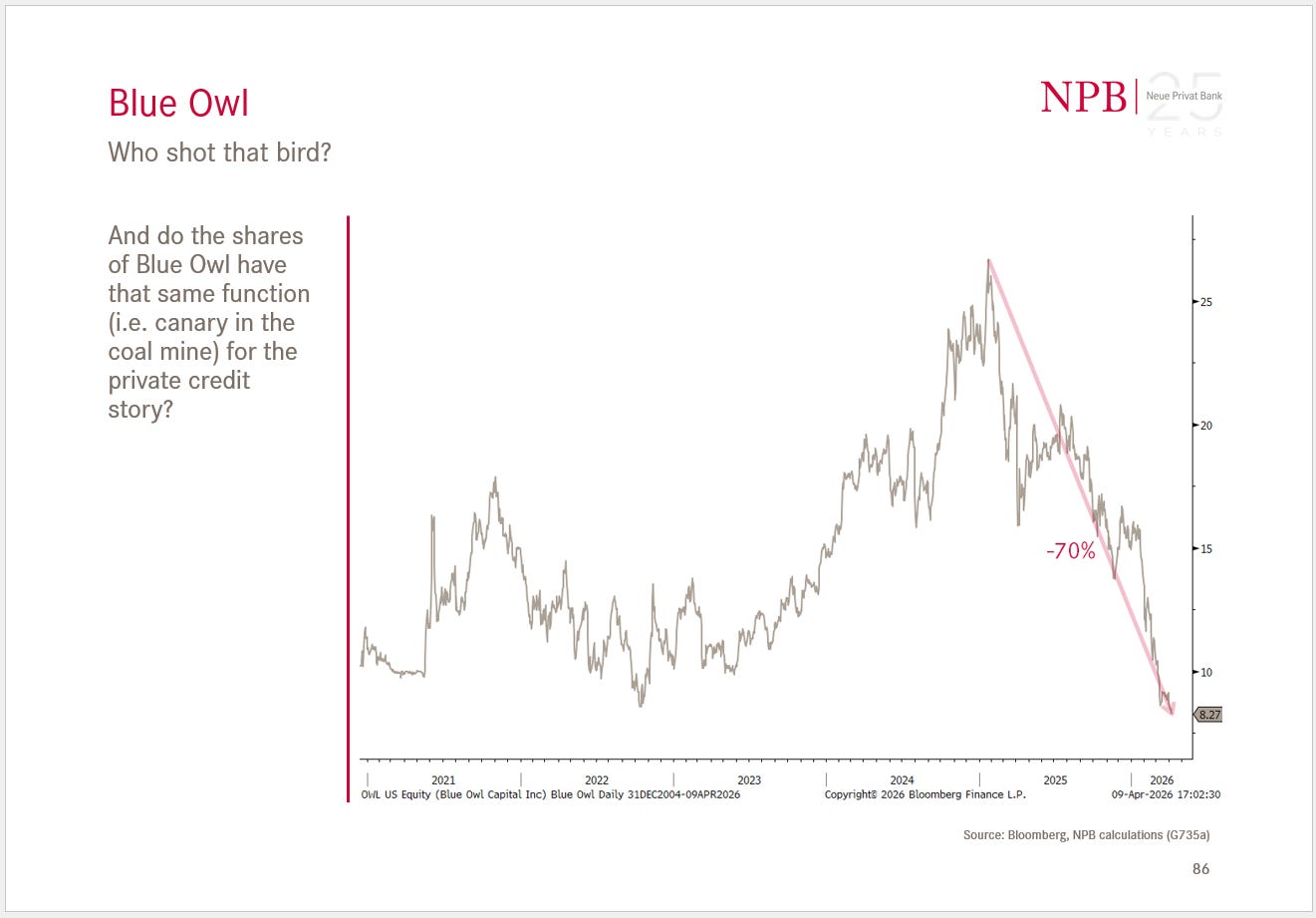

We deliberate whether the widening in spread (and recent reversal) really takes into consideration all private credit woes,

as some anecdotal evidence would suggest not:

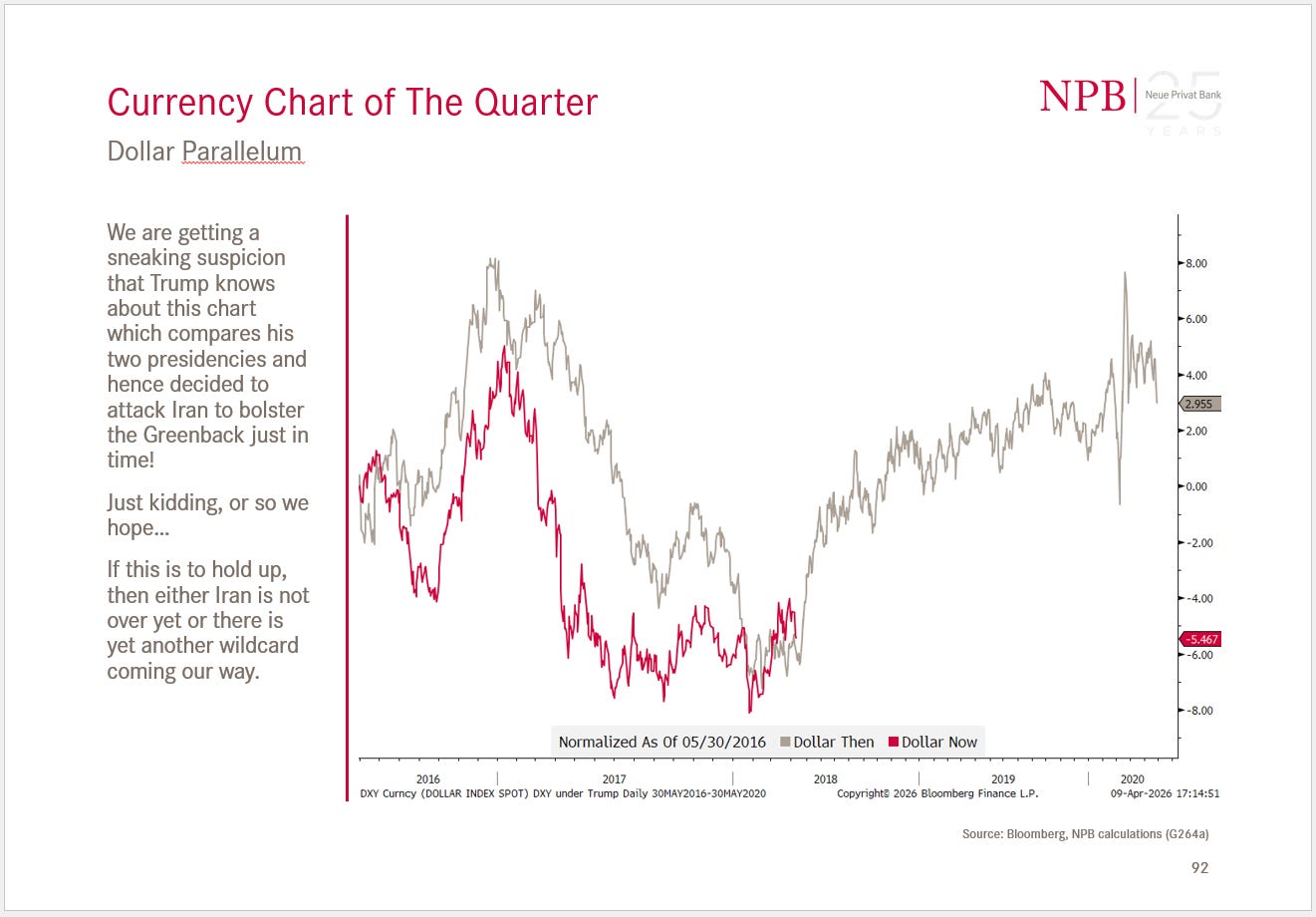

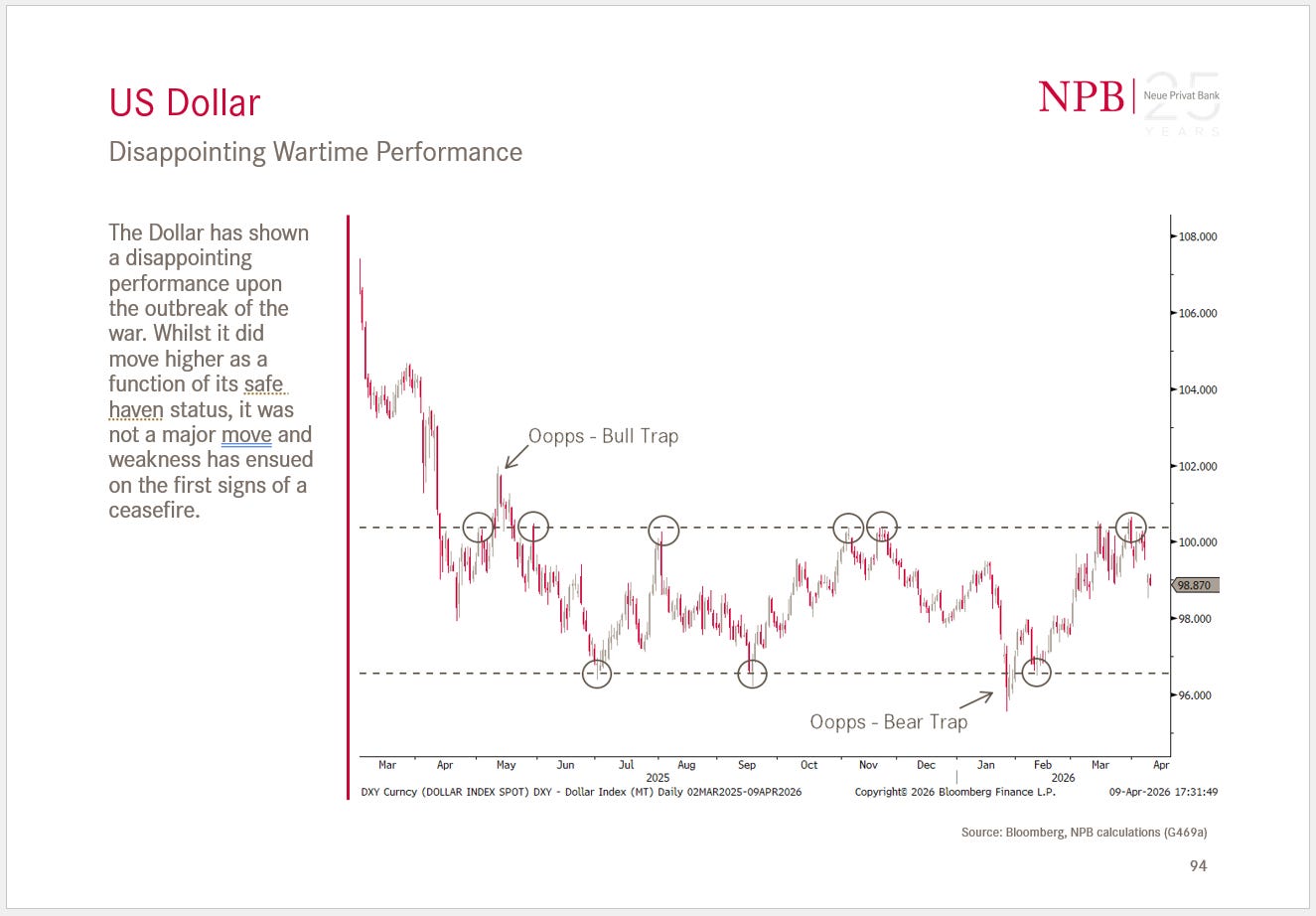

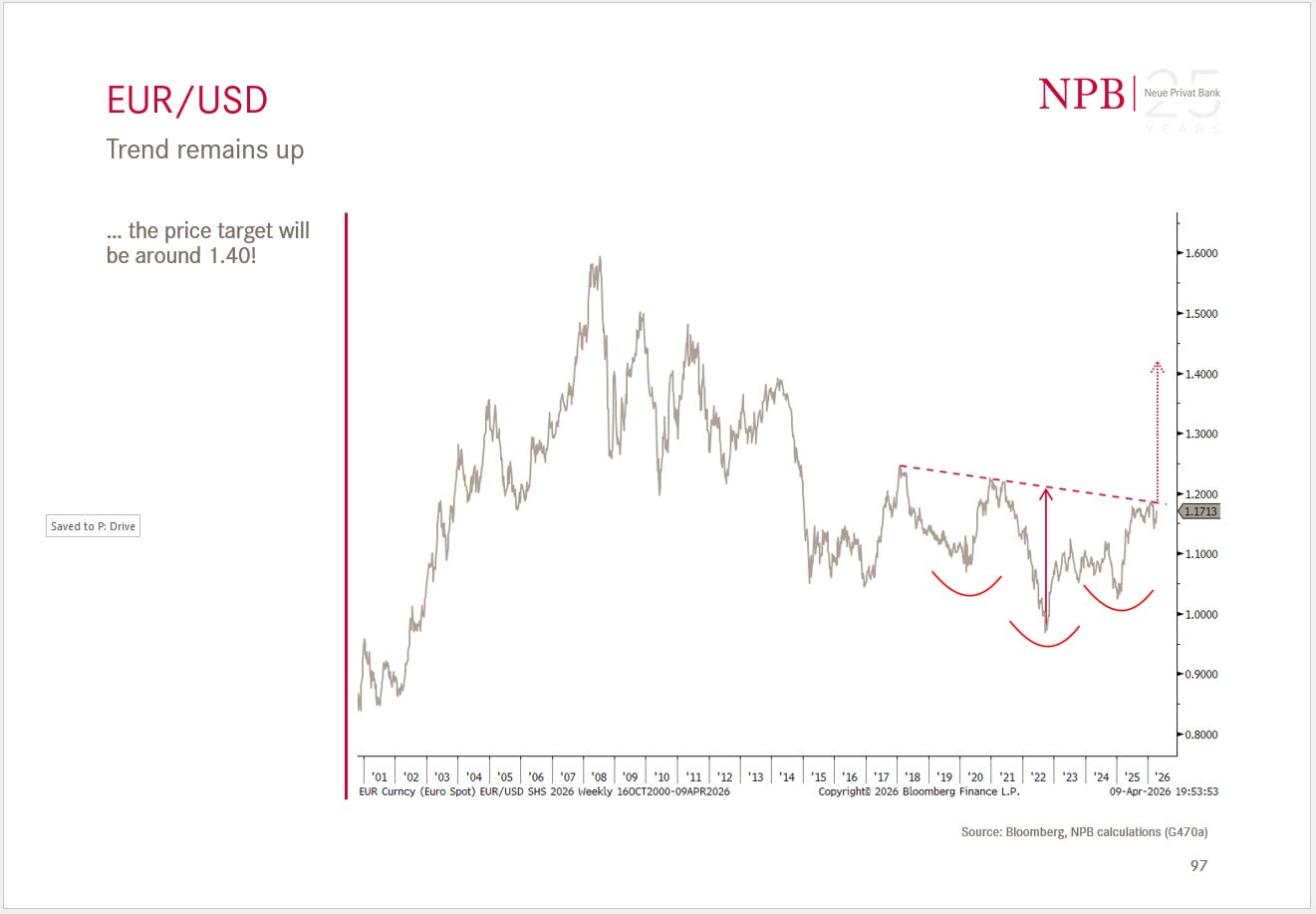

In the currency section we express our view that it will be able to uphold following chart,

as the greenback has been disappointingly ‘not strong’ during the six weeks or so of the Iran conflict:

The following chart carries a bold statement regarding a possible EUR/USD target IF the dashed red-line breaks:

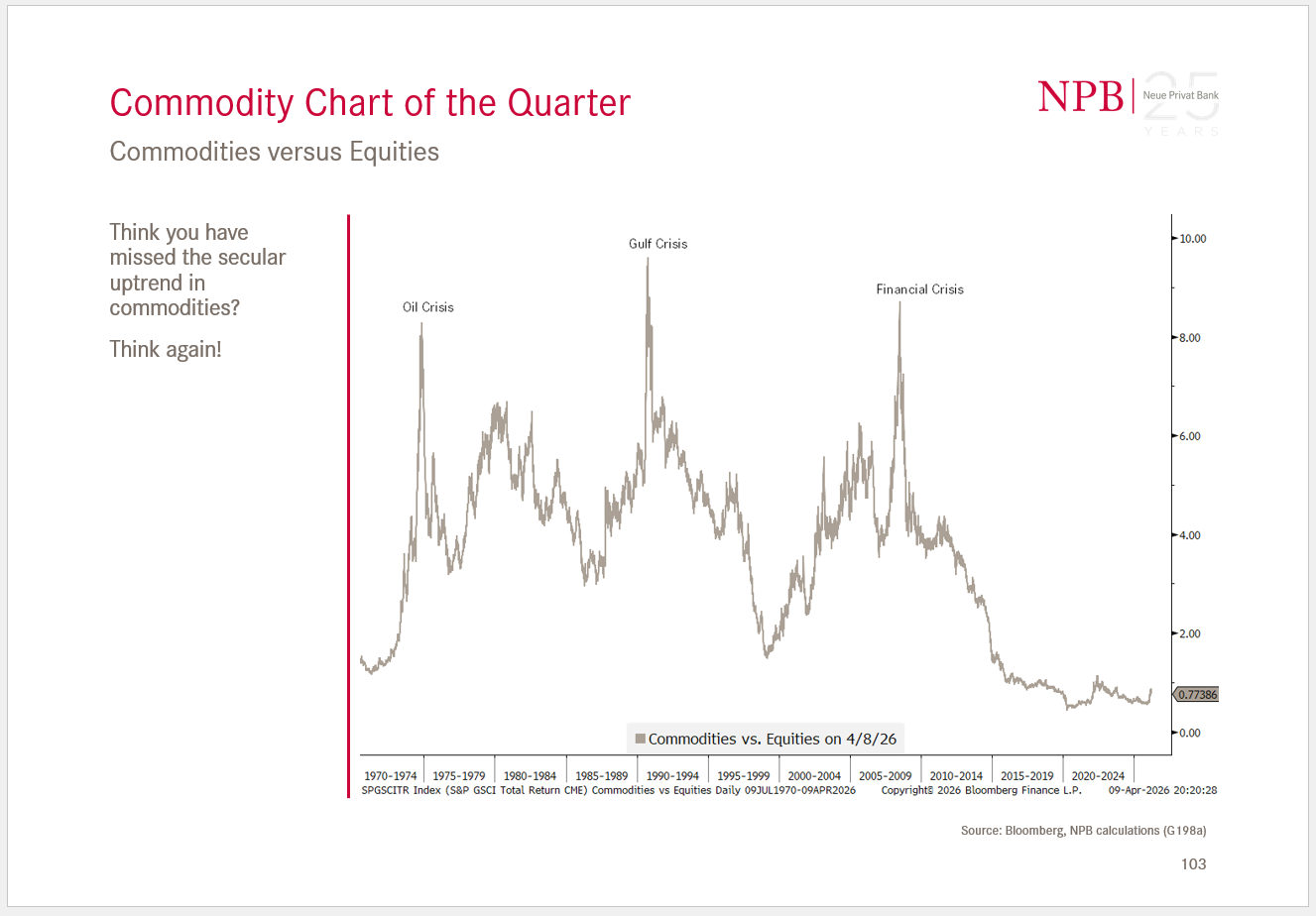

And in the final section, we put the current commodities rally into historic context comparing them with equities:

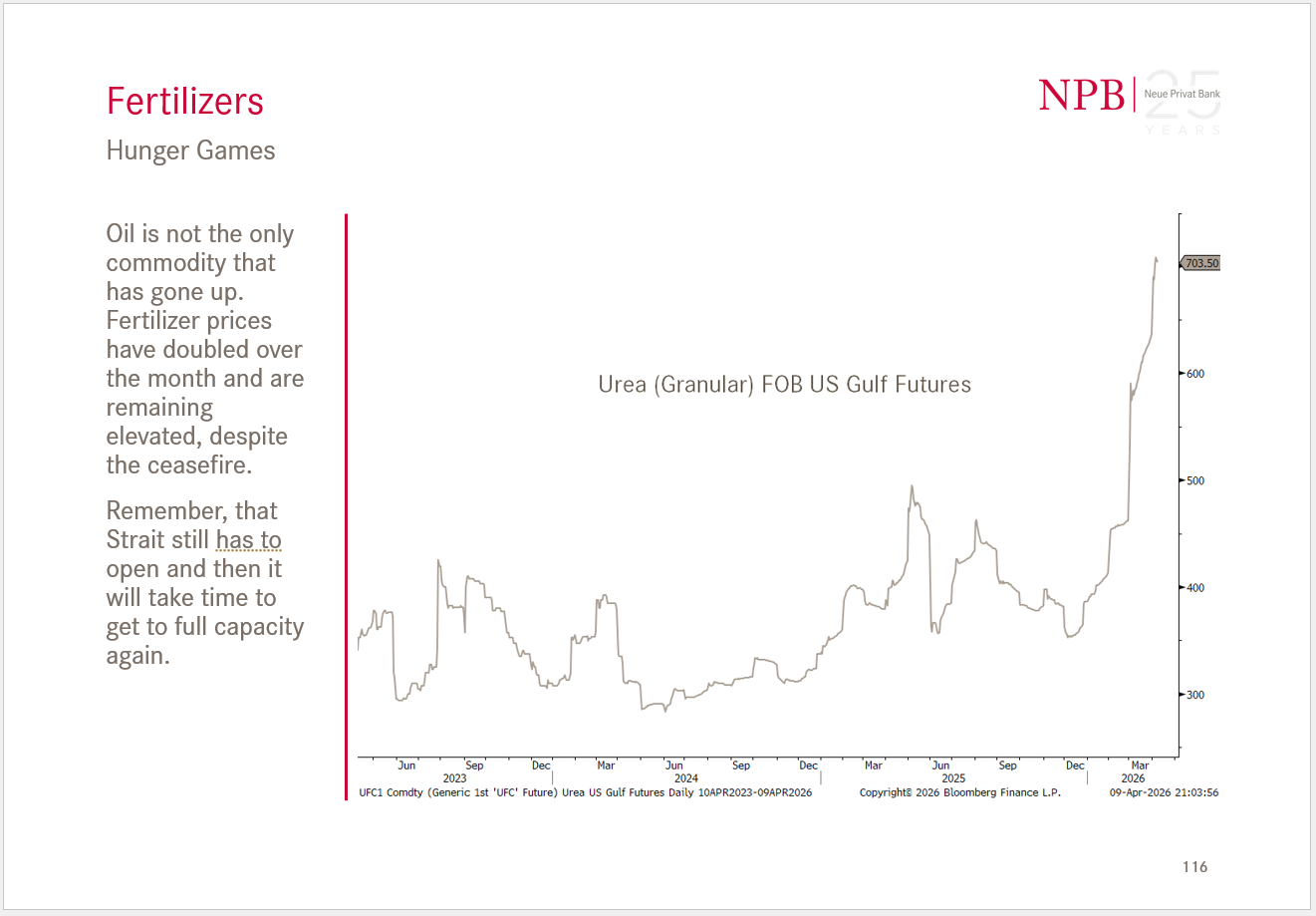

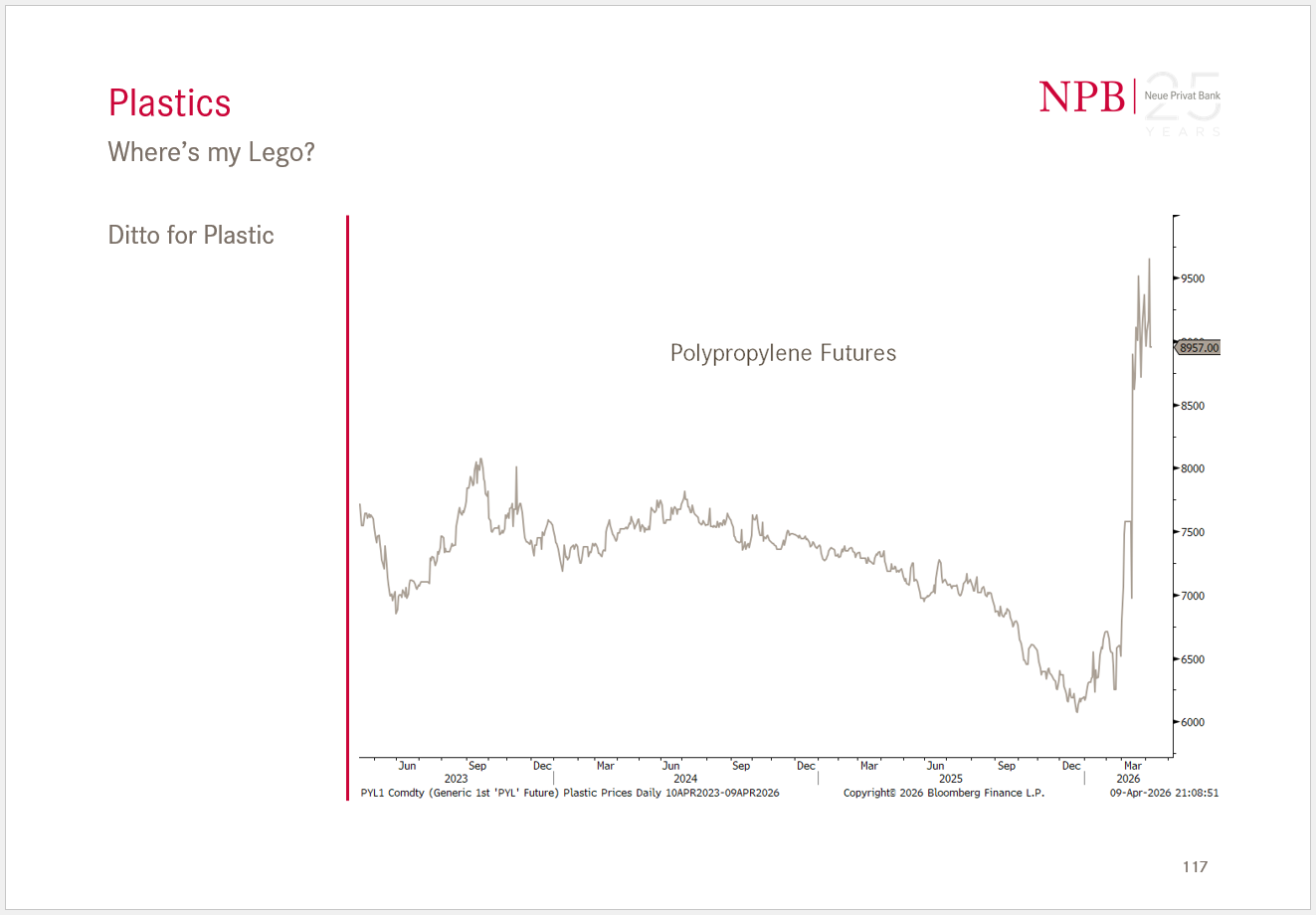

And to round off our “Ages of Empire” and “You Can’t Print Molecules” themes, we highlight the following two charts:

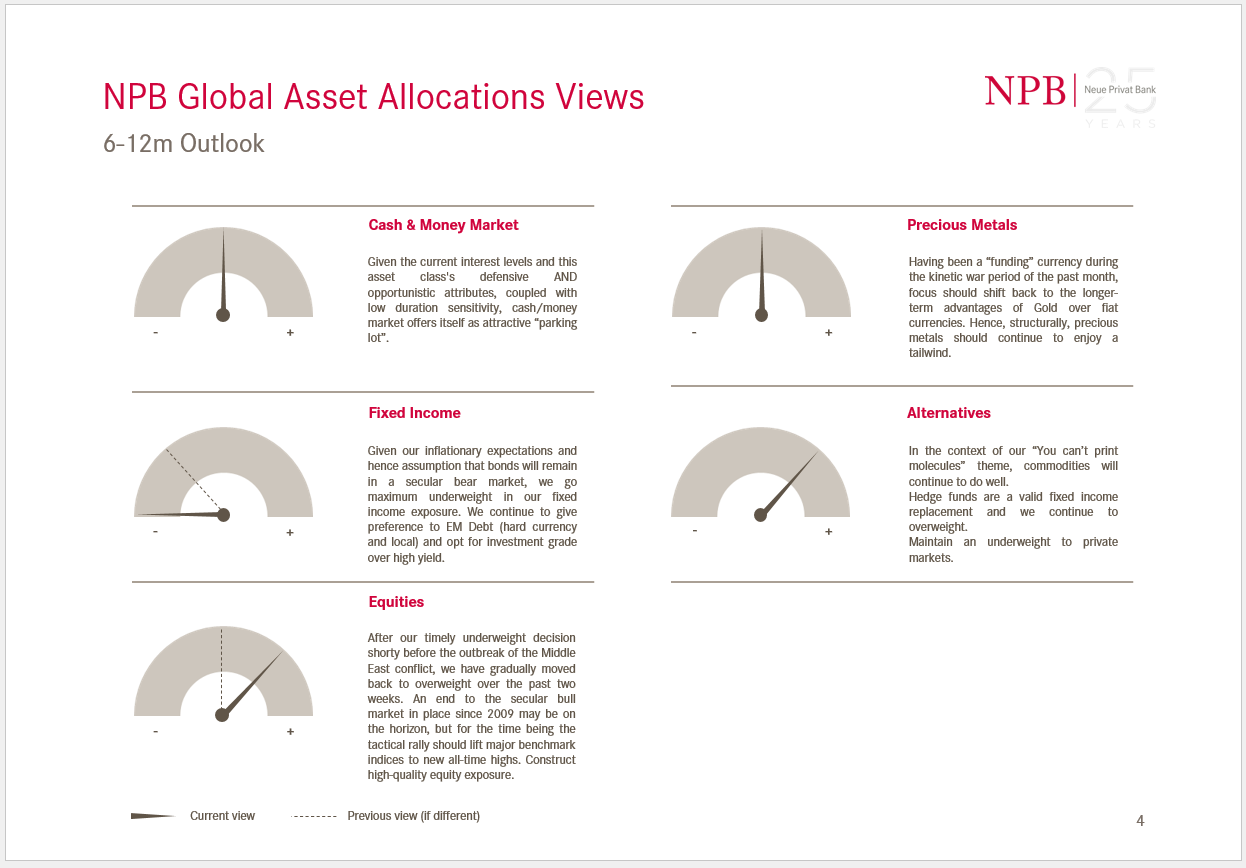

Finally, to square that circle, here’s another excerpt from our NPB Global Asset Allocation Q2/2026 document:

Again, should you wish to receive either or both of the documents, make the effort to write me a little email at ahuwiler@npb-bank.ch or even better, contact us to become a client ;-)

May the Trend be with You!

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG