Easy now ...

The Quotedian - Vol VI, Issue 72 | Powered by NPB Neue Privat Bank AG

“Tactics without strategy is the noise before defeat."

— Sun Tzu

Just a turbo note this morning, under suspicion of being the shortest Quotedian ever.

Market action over the past few hours involving some levels we have been closely looking at warrants a brief update, but my intention is to also take a deeper review of recent movements in a Sunday special issue. Stay tuned …

Need on-the-spot, up-to-date investment advice?

Contact us at ahuwiler@npb-bank.ch

Let’s dive right in…

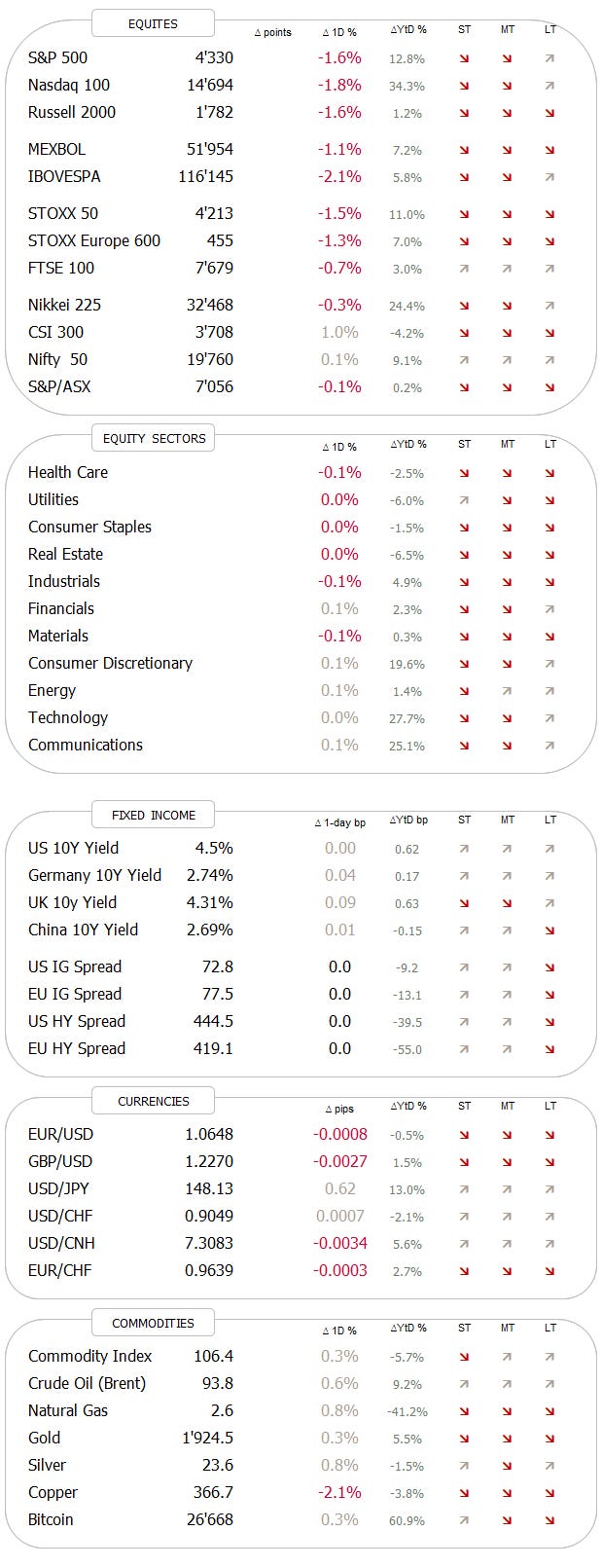

Equity markets took a day to digest the Fed’s “higher for longer” message from Wednesday evening, but once it settled in, stocks started selling off, pushing the S&P 500 1.6% lower on the day.

This move was big enough, to throw the index below our observed lower line in the sand:

Now, what is gonna happen from here is of course not written in stone, but if the index cannot turn around quickly (as in today), then 4,100 (-5.5%) becomes the next moving objective.

Adding to the importance of yesterday’s move that it was the first index move in excess of 1.5% since April this year:

In Europe, the sharp downturn yesterday puts the recent bullish breakout of a consolidation triangle at risk:

Asian markets are surprisingly resilient this morning, maybe thanks to a small uptick in SP futures over the past few hours.

The entire yield complex pushed higher yesterday, though this time to a larger extent at the longer end of the curve, unwinding the previous day’s flattening process.

The US 10-year is now at levels not seen since 2007:

In currency markets, after yesterday’s slide in the Swiss Franc upon the surprise ‘no move’ by the SNB, today’s its the Japanese Yen’s turn to ditch lower, after the BoJ also decided not to move their rate window.

Hence, between the Fed’s ‘hawkish hold’ and some surprise ‘no moves’ (BoJ, SNB, BoE), the US Dollar has been the big winner of the past 48 hours:

That’s all for today - as mentioned I will try to issue a longer note over the weekend.

In the meantime, you go and enjoy that weekend!

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance