FrankenstAIn

Vol IX, Issue 10 | Simplicity is the Ultimate Sophistication

"Learn from me, if not by my precepts, at least by my example, how dangerous is the acquirement of knowledge."

— Victor Frankenstein, in Mary Shelley’s Frankenstein (1818)

Of course, the news of the moment are the Israel/US joint attacks on Iran and that country’s retaliation efforts. However, the situation is is too fluid for firm positioning or even sense-making comments. Hence, this week’s Quotedian should hit your inbox before markets open and we will largely ignore those bellic events.

But,

we will cover this closely through the Daily Edition of the Quotedian (NFKAQ - the Newsletter Formerly Known As QuiCQ). Not signed up? What are you waiting for!

So, here’s this weeks TL;DR:

Equities did not live up to their (bad) reputation in February, though regional differences applied

Rotation is not only confined to geographics though; previous sector winners are now losers and vice versa

Watch financials carefully for further sign of contagion out of the private credit sector

Fixed income markets behaved well, but returns are now coming from rates rather than credit spread compression

The US Dollar’s failure to gain as a safe haven currency is worrisome and should be observed closely

Gold is heading towards new ATH

Oil will be subject to the newsflow surrounding the Strait of Hormuz

Have we created our own monster? We have created large language models (LLMs) to power artificial intelligence (AI). And now we use AI to create better LLMs. Don’t believe me? Here’s an excerpt out of the technical documentation accompanying the release of GPT-5.3 Codex:

“GPT-5.3-Codex is our first model that was instrumental in creating itself. The Codex team used early versions to debug its own training, manage its own deployment, and diagnose test results and evaluations.”

And those LLM monsters — will they then turn on us creators and eliminate our jobs? A report earlier this week by Citrini Research, a financial markets research hub I have been subscribing to for over two years now but which suddenly seems to be in everybody's mouth, paints a chilling thought experiment: what if the AI bulls are right about the technology — and that's precisely what makes it bearish? Written as a fictional macro memo from June 2028, it traces how white-collar job displacement could spiral from a sector story into a systemic crisis, complete with an S&P 500 down 38% from its highs. Shelley couldn't have scripted it better.

But enough gore for now, especially as this is the end-of-month of edition of the Quotedian and we will, as usual, concentrate on some market statistics and performances and throw in one or the other more long-term (monthly) chart.

Aaand off we go!

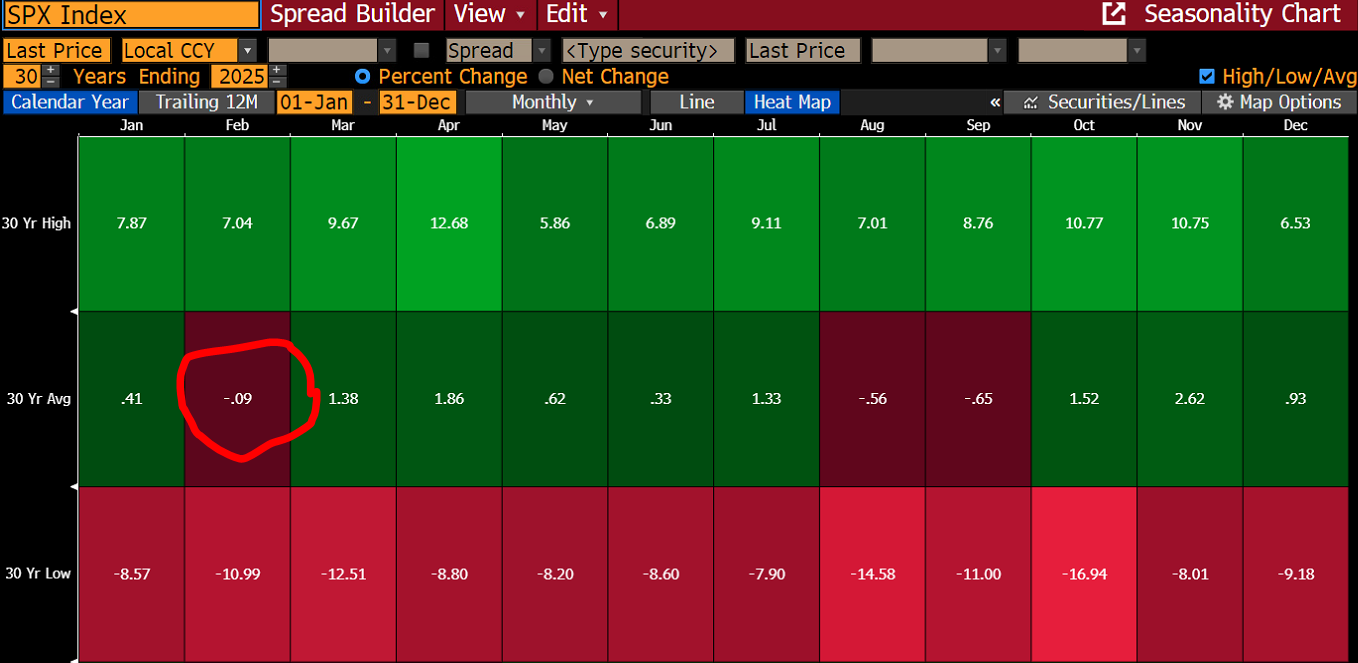

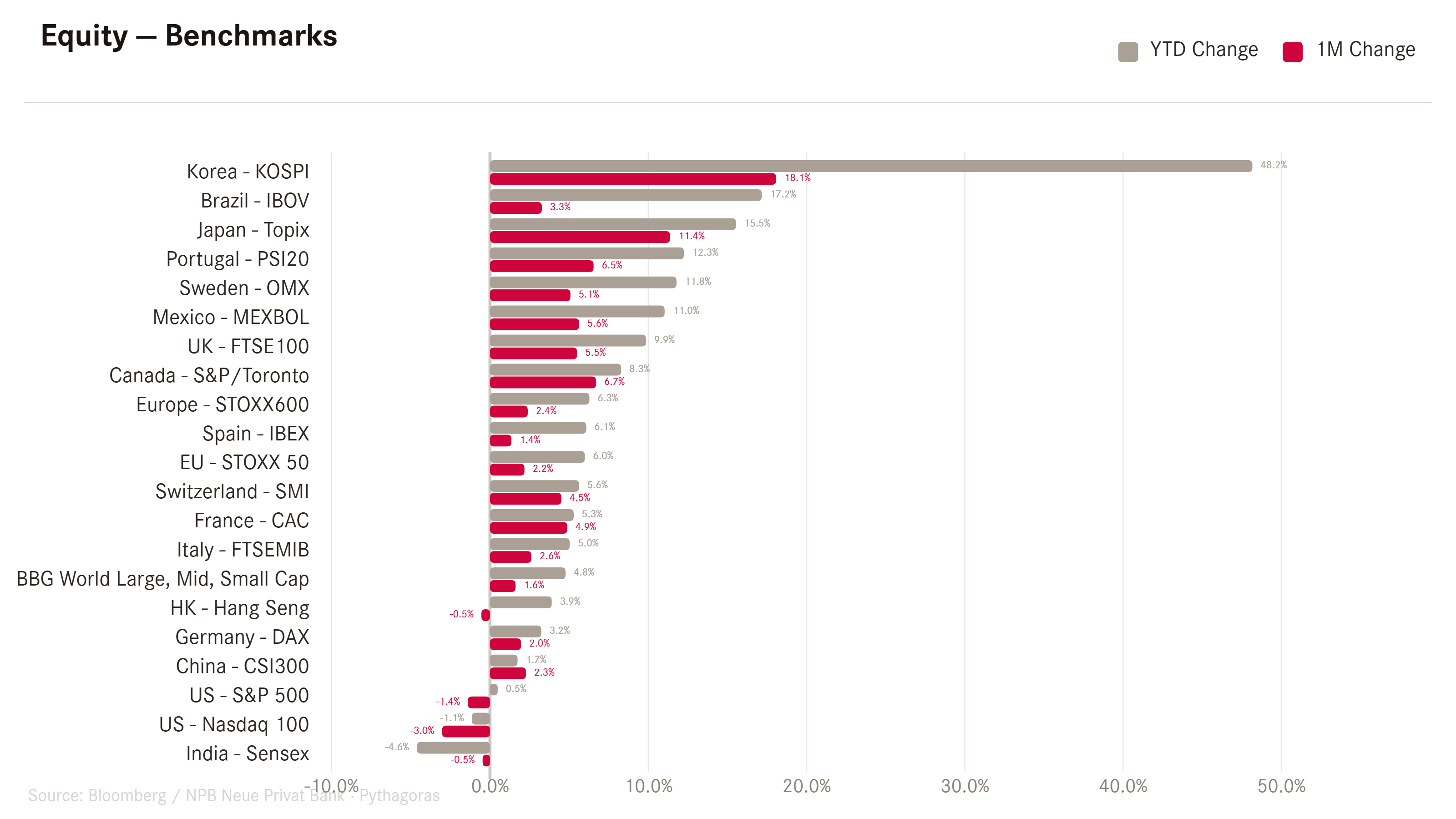

Starting with equities, February has lived up to its reputation to be one of the three more difficult month of the year,

but only in the US!!

In the graph above, grey bars are year-to-date performance while the red bars are the February performance. Hence, really only the US (S&P 500 and Nasdaq) had some meaningful downside. Everything else continued to tug happily along.

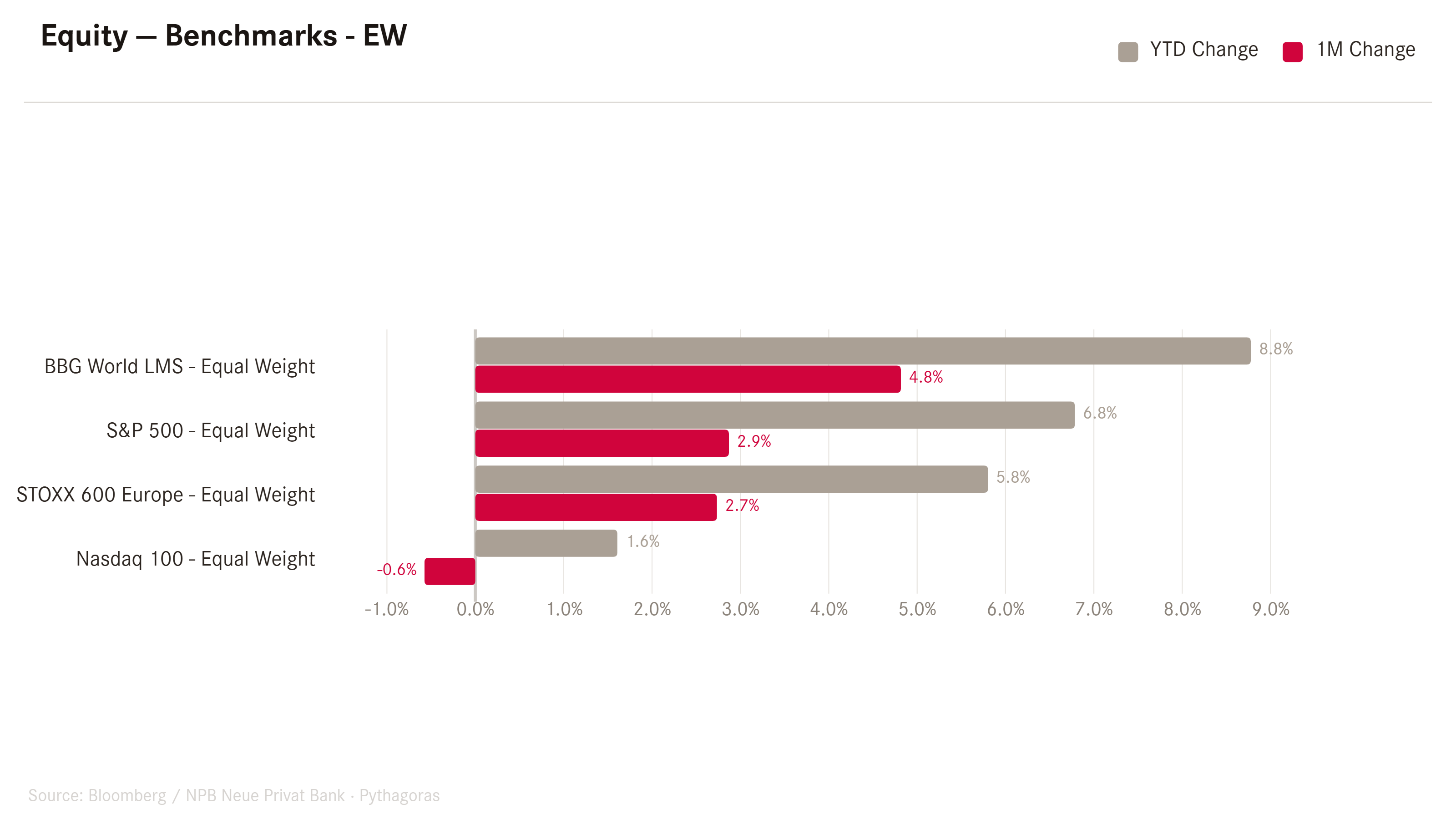

However, even the apparently mediocre US performance, is actual only … well … apparent. Digging below the surface, we note that on an equal weight-base the S&P 500 actually delivered a very respectable three percent advance in February:

Hence, compared to the 'normal’ cap-weight version of the S&P 500, which logged a negative monthly return,

the equal-weight version, below proxied via the RSP ETF, reached yet another new all-time high:

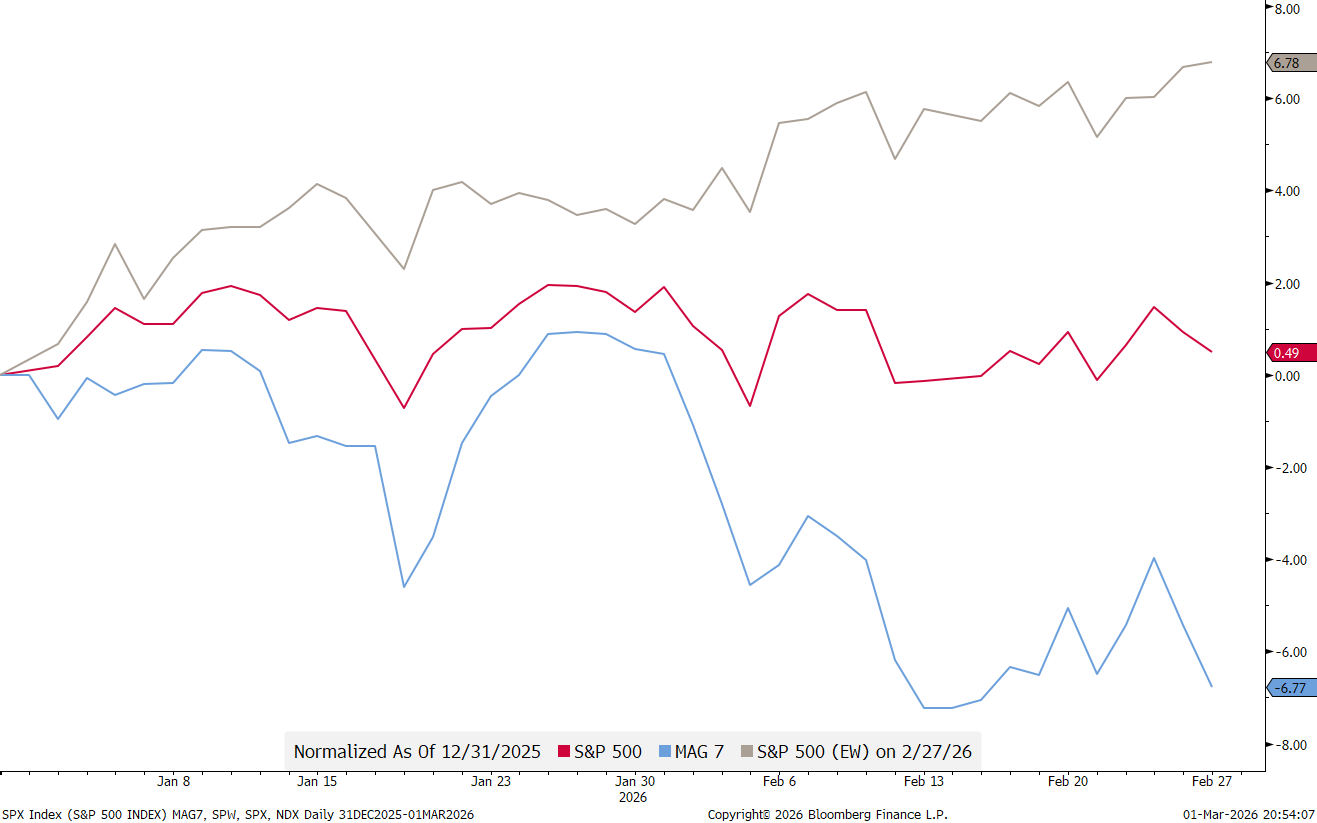

Hence, 2026 has been all about rotation, rotation, rotation:

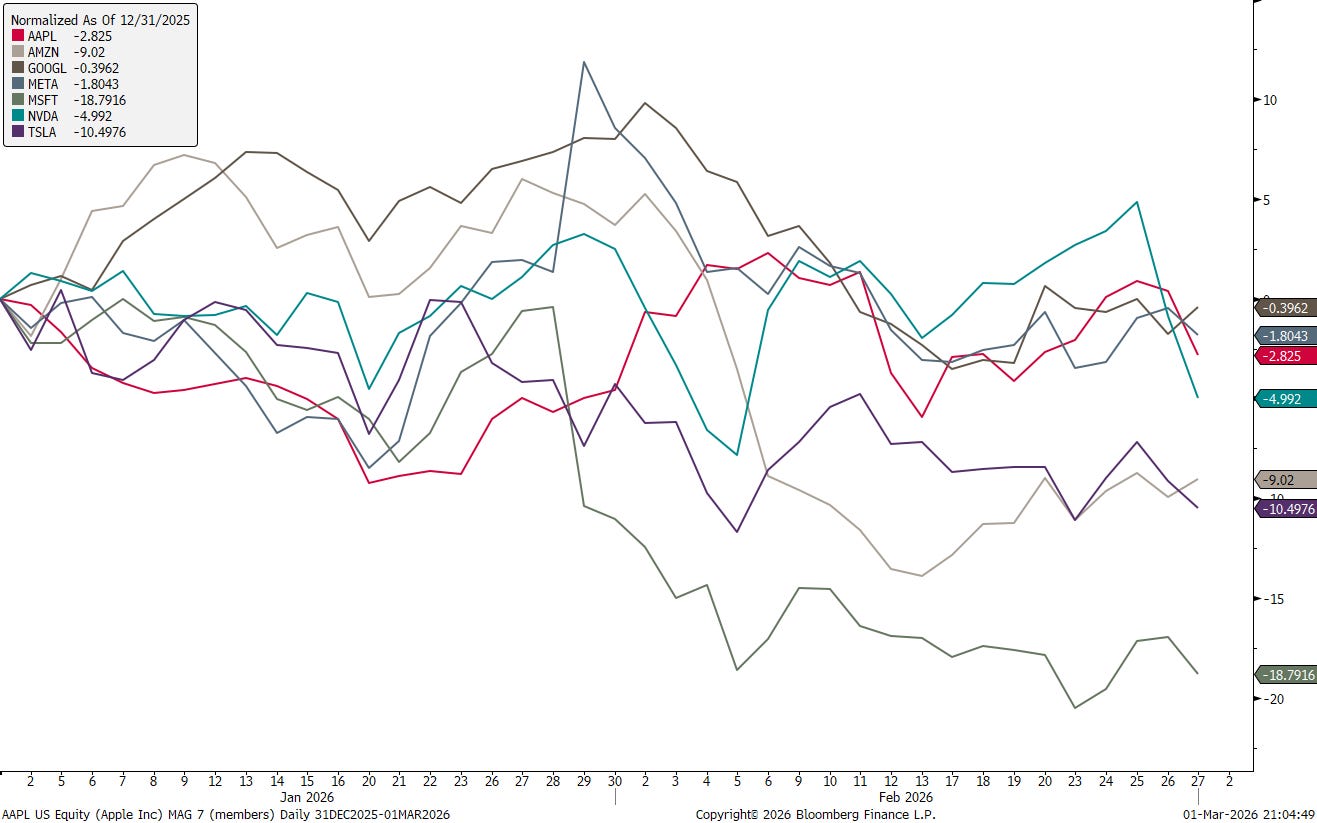

Accordingly, not one gang member of the clan of the Mag 7 is showing positive YTD returns:

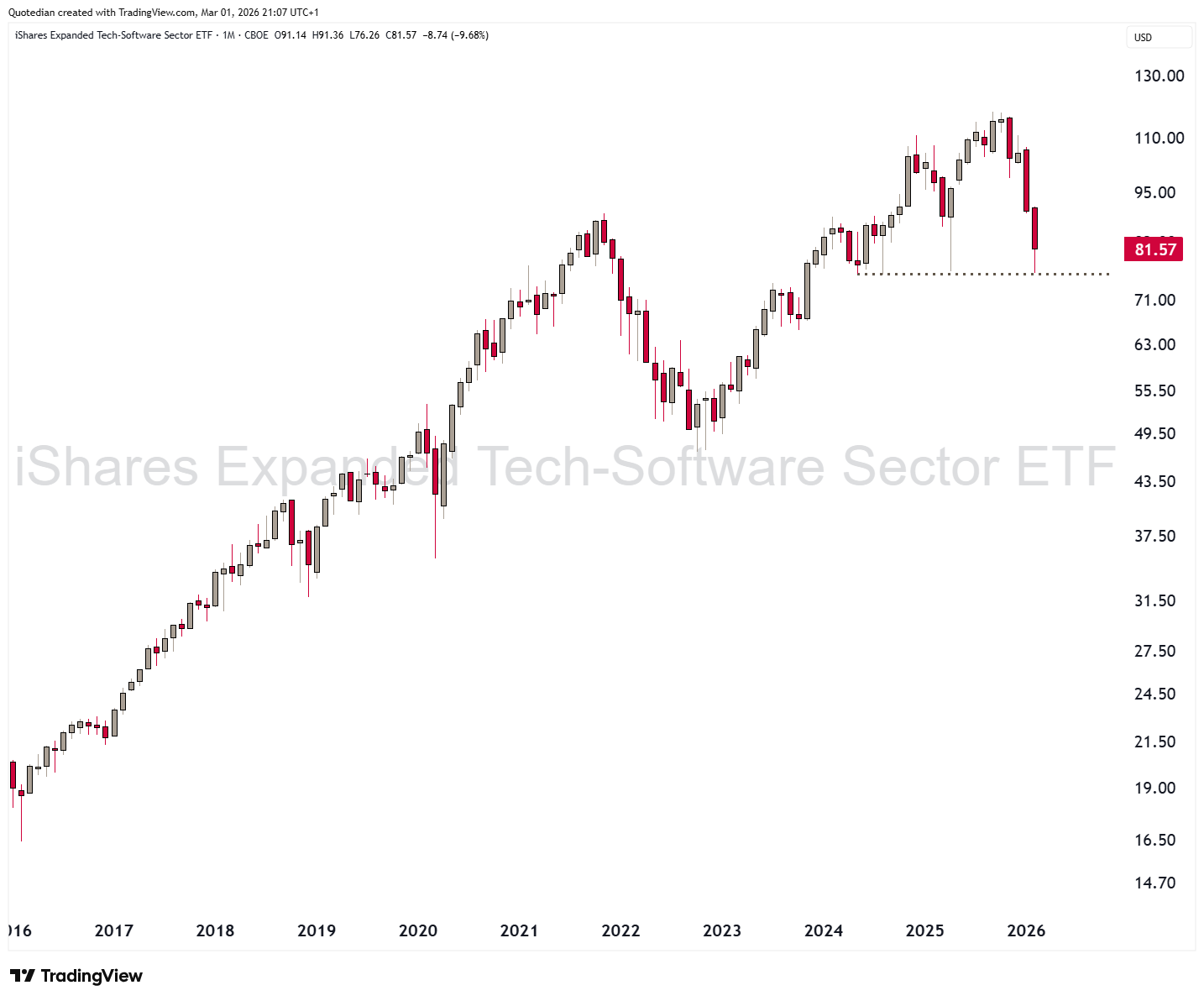

But with a difference, the worst wounded is the purest software play out of the seven, which of course brings us back to this week’s FrankenstAIn theme. Here’s the chart of the iShares Software ETF:

It would be a grave understatement to say that software stocks rebounded EXACTLY where they had to. But, a) the ETF is still down 35% peak to current trough and b) the current trough may be just that … current.

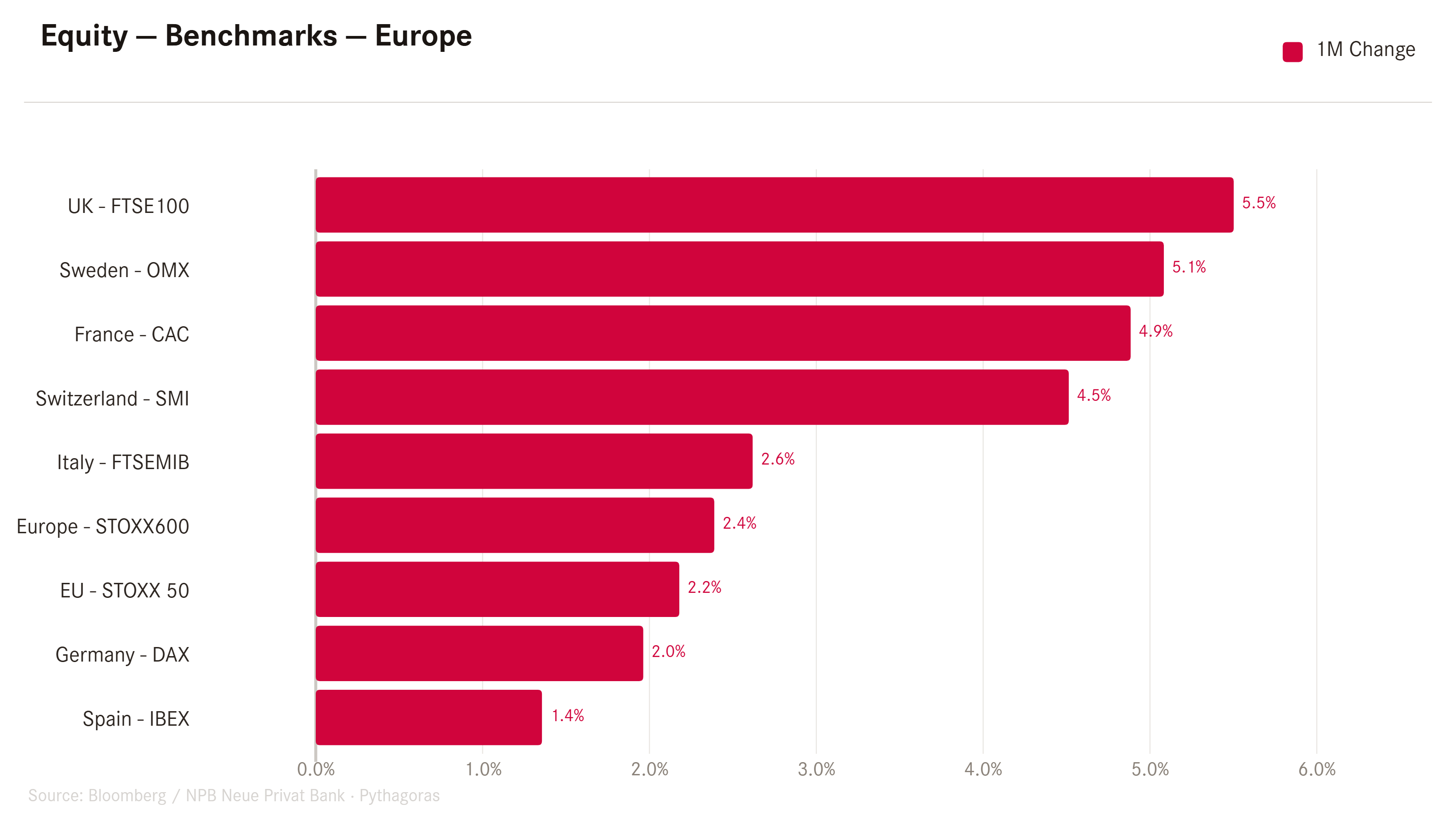

Turning to Europe, the STOXX 600 Europe Index (SXXP), had a very strong February:

All components, including non-Eurozone members such as Switzerland and the UK, showed strong advances:

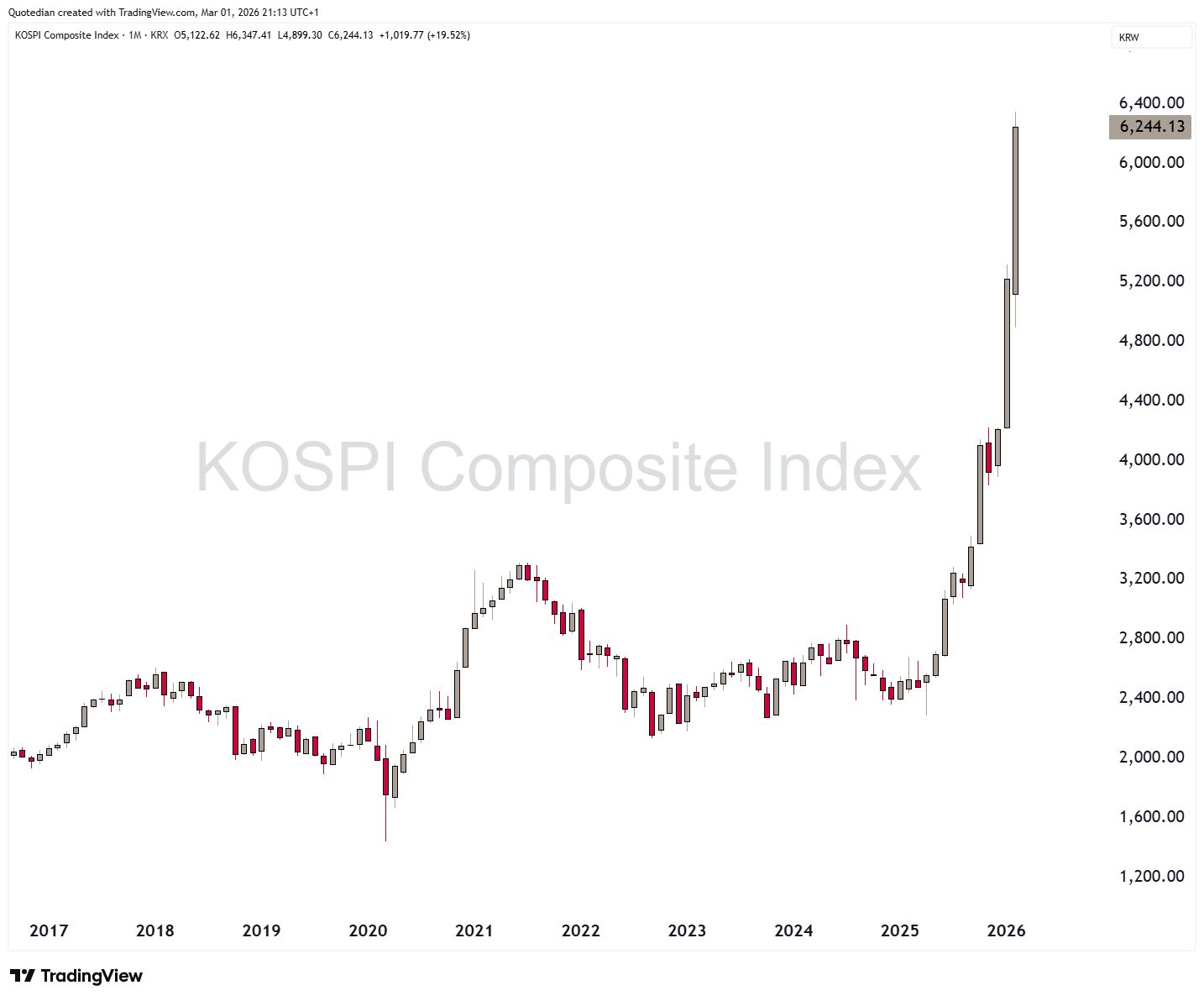

In Asia, Korea’s KOSPI,

and Japan’s Nikkei 225 stand out:

Though, admittedly, both look a tad too vertical just now and may be in for a pause soon.

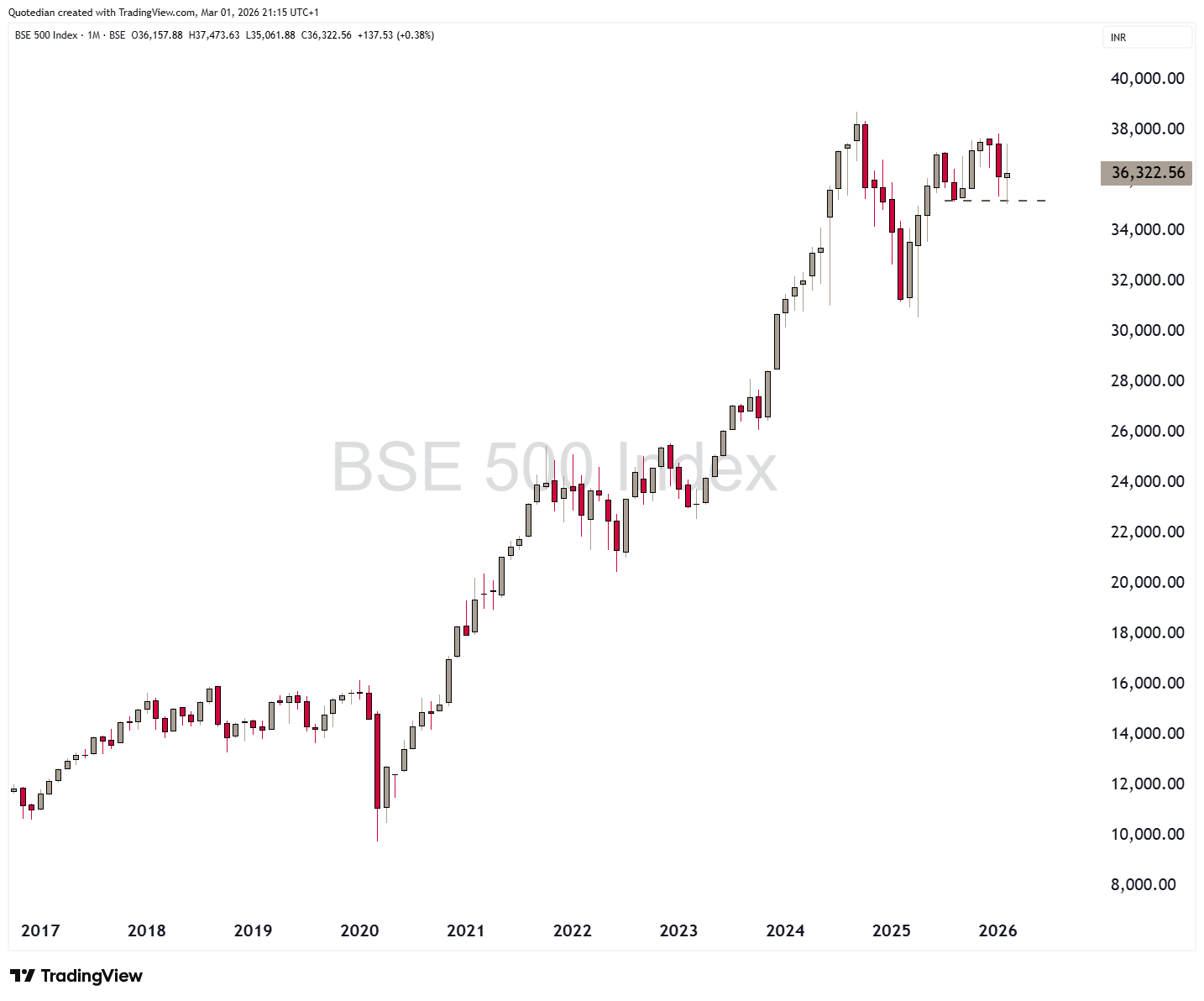

Continuing to tread water is the Indian stock market,

a situation that may become worse before better, given the current Iran conflict and India’s heavy dependence on oil out of exactly that country.

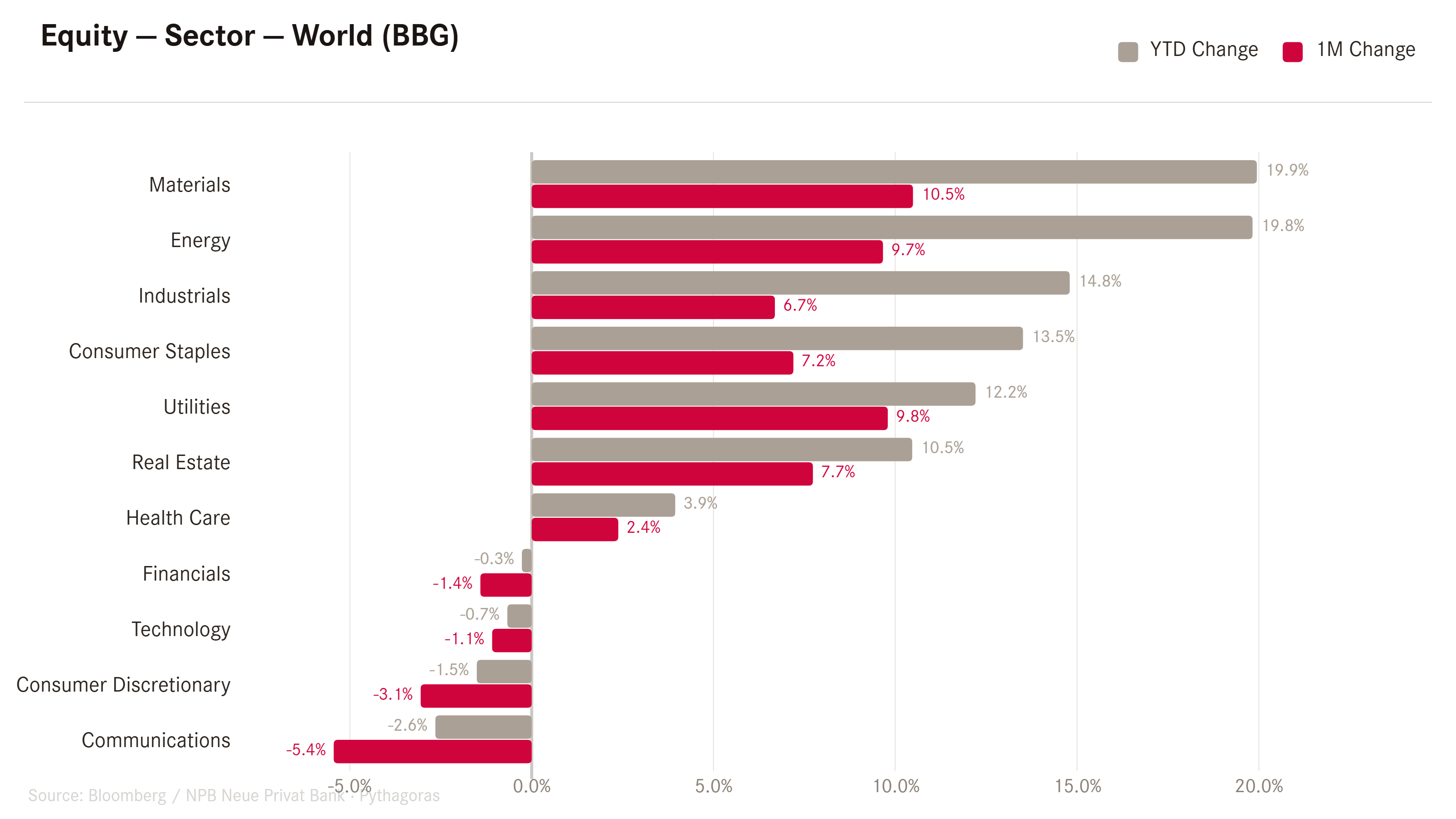

In terms of sector performance, the rotation of bits into atoms, continued:

But outside that major “bits to atoms” theme, which we also addressed in our 2026 outlook (click here), I would have a close eye on financials for signs of contagion out of the private credit disaster corner (click here). Here’s a US financials ETF (XLF) to follow:

A private credit proxy (BIDZ) is haemorrhaging:

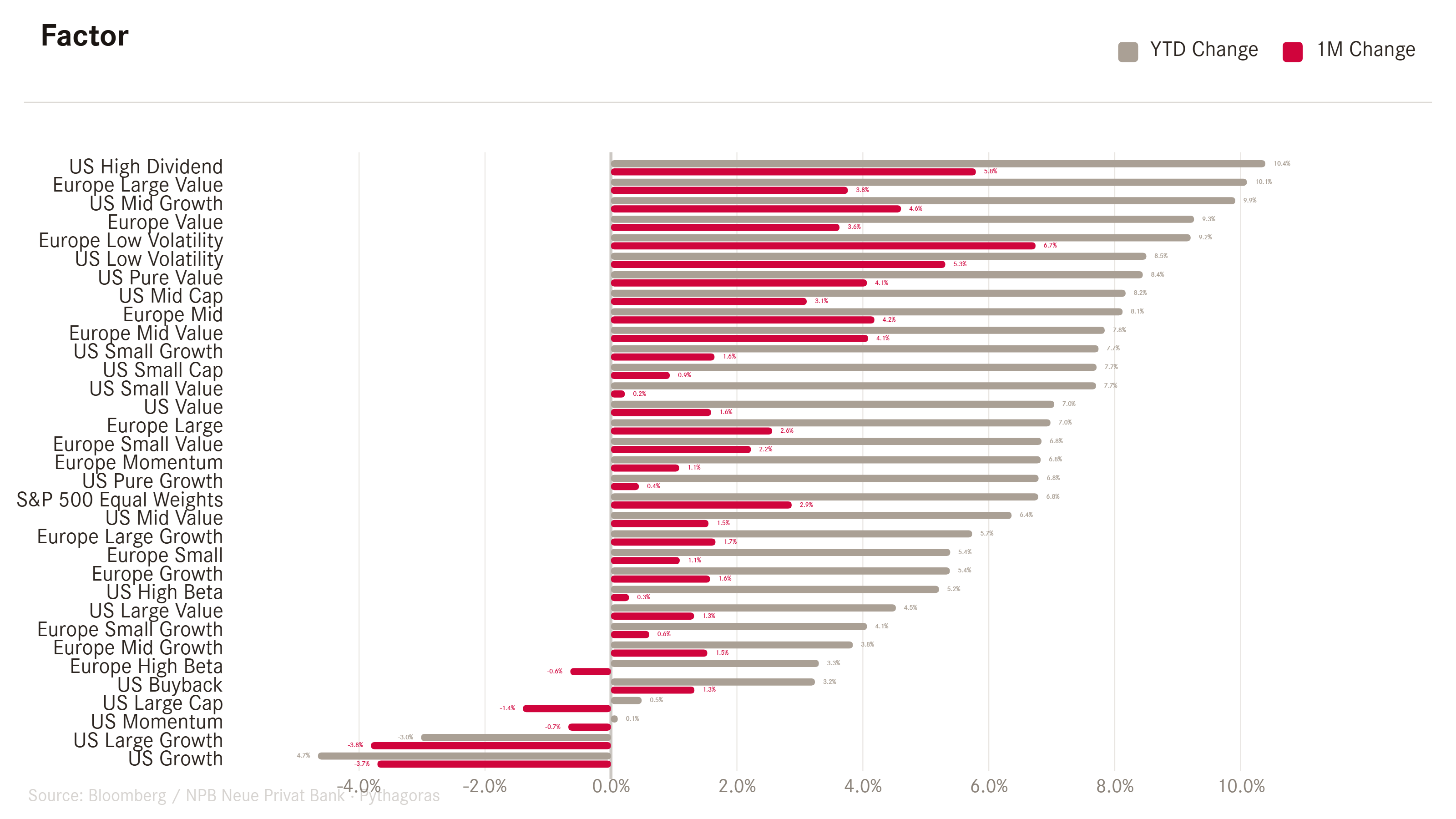

The factor landscape has also changed quiet dramatically in comparison to the past few years, with February further reinforcing those newly established trends:

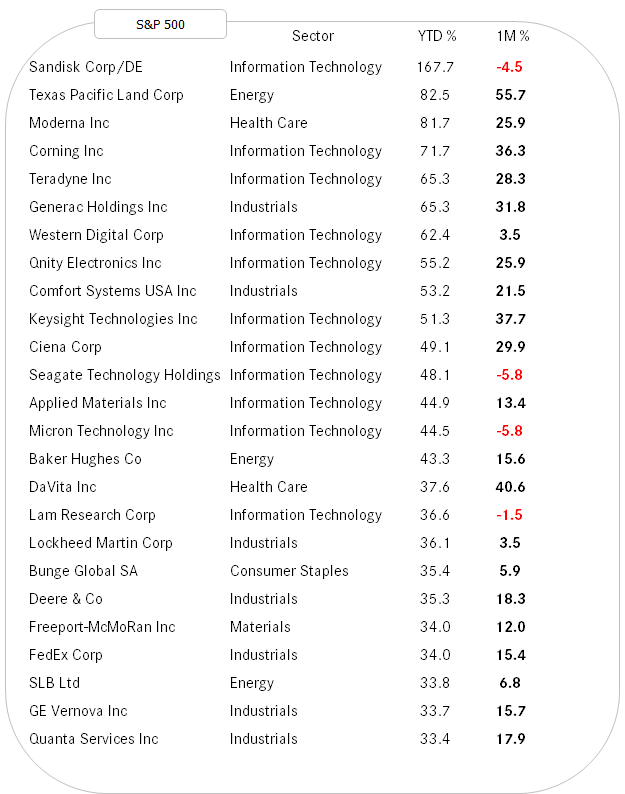

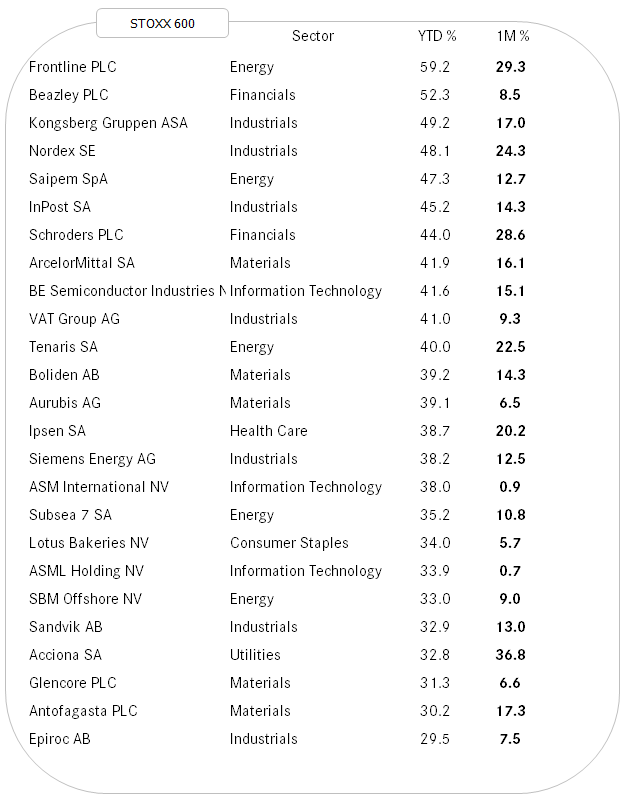

Before rushing over to observe fixed income markets, let’s look at some individual stocks. Namely, which stocks have performed so far (YTD) best in the US (S%P 500) and in Europe (STOXX 600).

Starting with the US,

we not two things:

Despite the rotation away from tech stocks, there are still surprisingly many of that sector in the top 25.

Some of the YTD gains are astonishing, despite being two months old only

In Europe, it stands out that not one top 25 stocks saw a reversal in February:

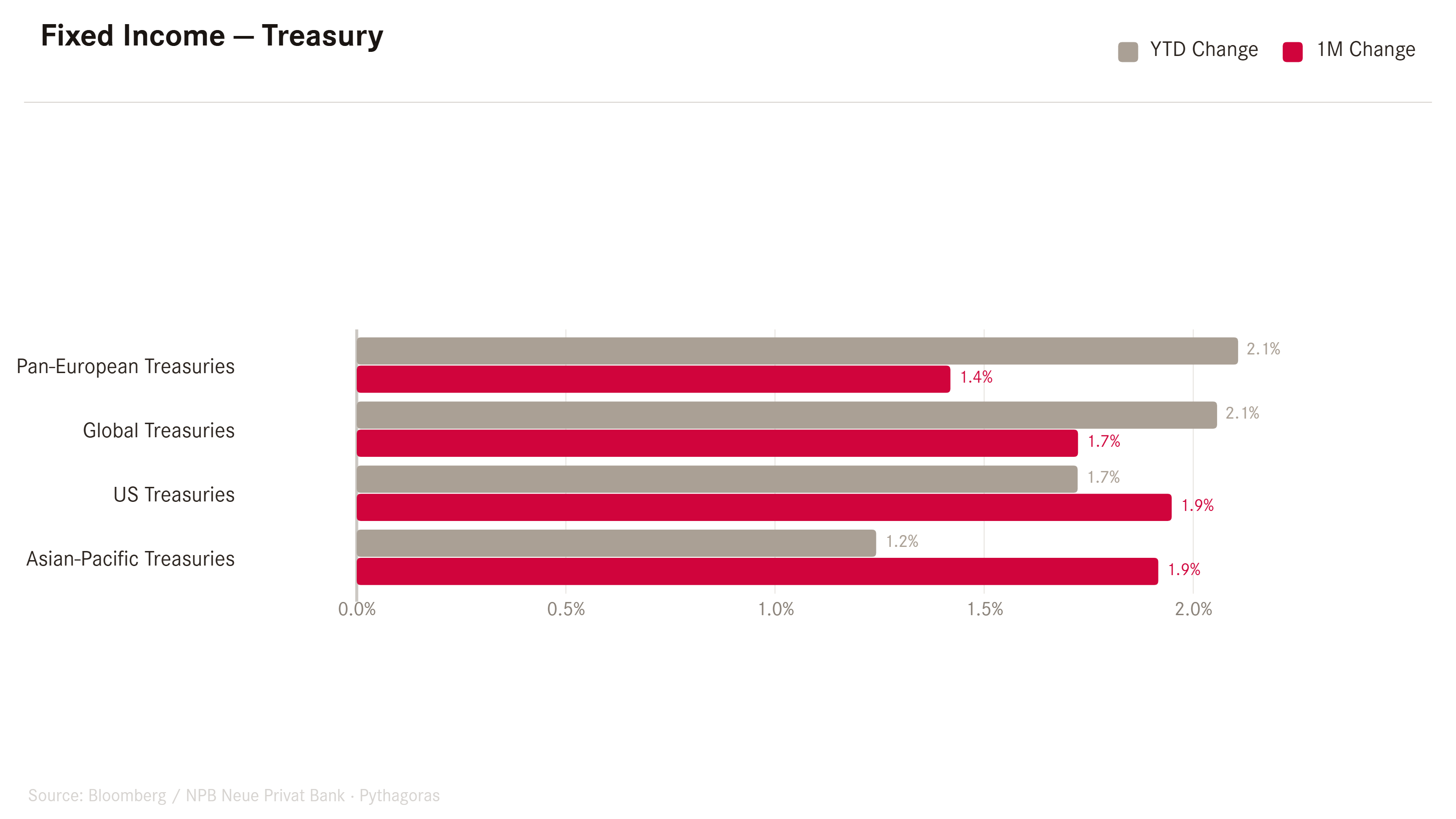

Now to the fixed income space, where returns have been great for Treasuries,

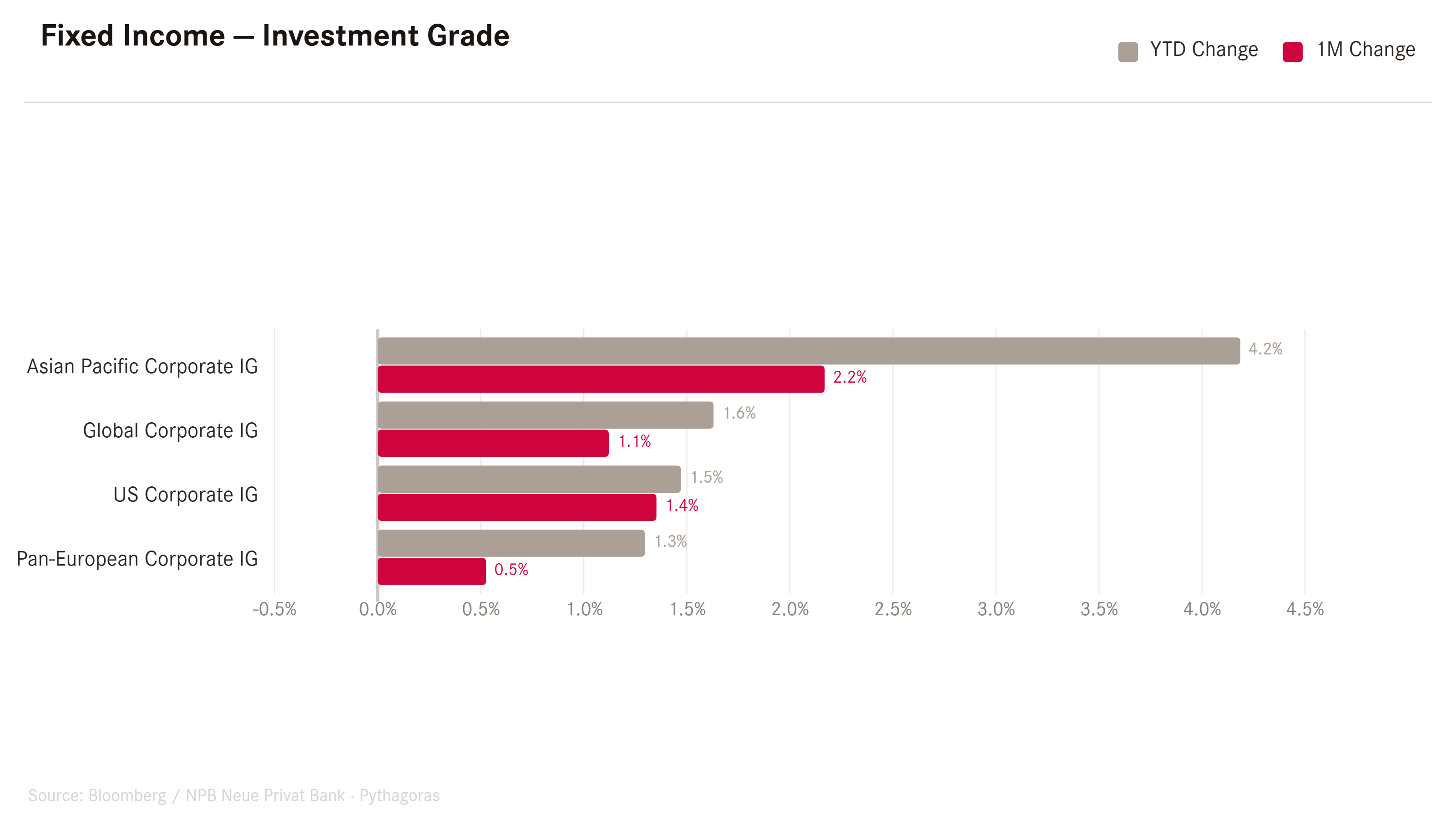

Investment Grade Credit (Corporate Bonds),

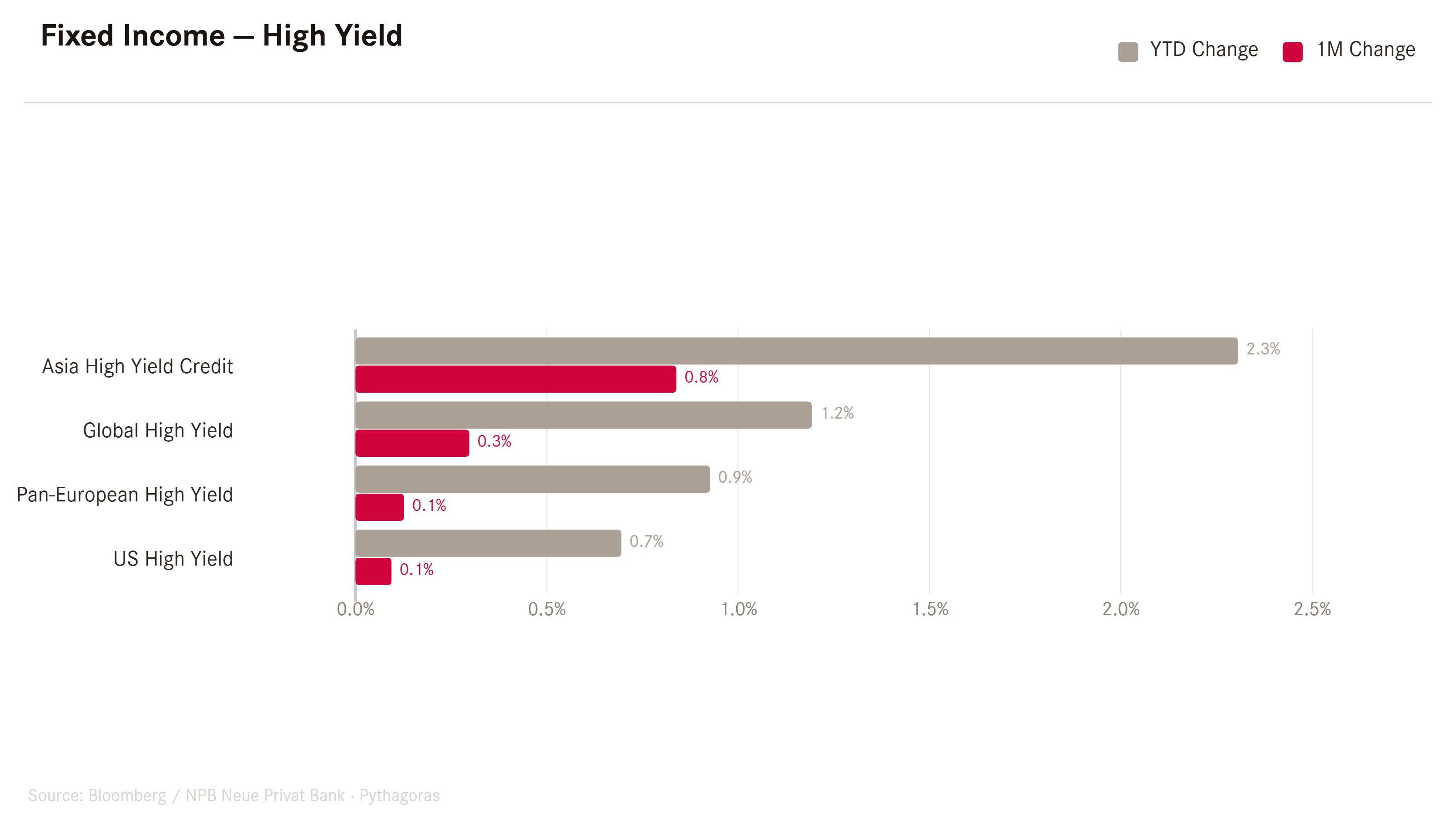

AND high yield:

across all regions.

But, revisiting those four tables above, it is clear that more return was extracted from falling yields (here’s the 10-yeaer US Treasury example),

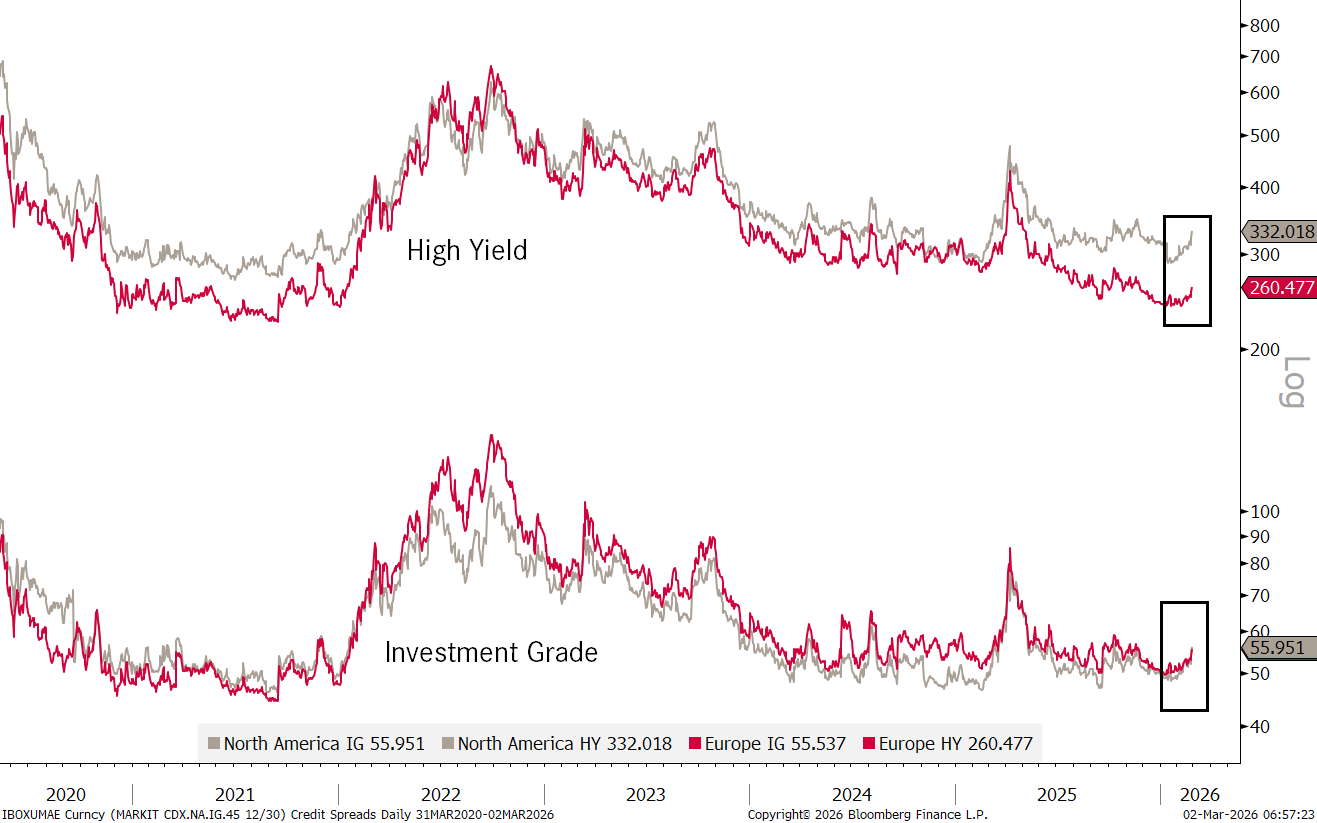

then from further credit spread compression, which rather seem to be turning higher:

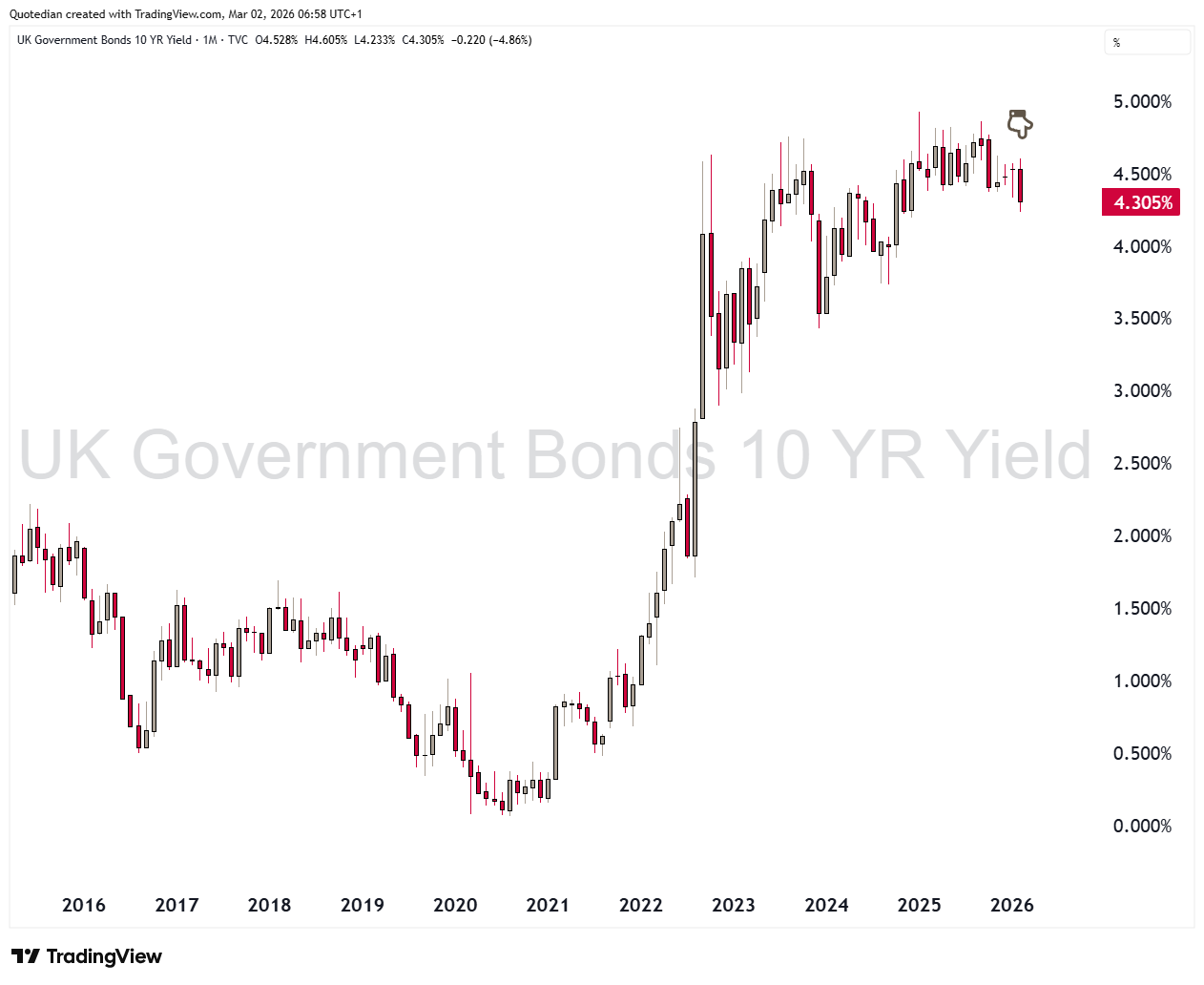

Of further note in the rates realm is the drop in UK Gilt yields, despite the ongoing political mess:

And Japan’s JGB yields seem to have found now an at least intermediate top:

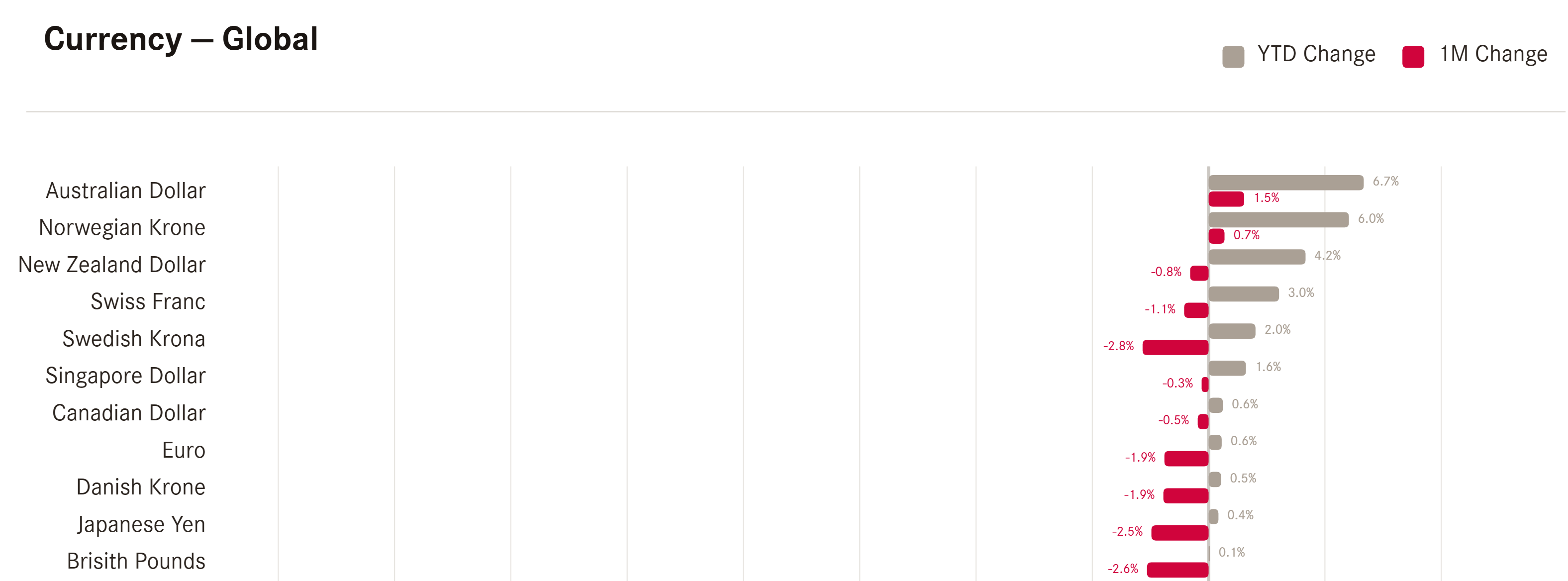

Which brings us to currencies, where the US Dollar has been able to gain some ground, except to safe haven (CHF) and some of the commodity (AUD, CAD, NOK) currencies:

Versus emerging market currencies, the picture is similarly “messy”, with the usual suspects (TRY, INR, IDR) the usual’losers’ versus the Greenback, but also some surprisingly clear winners (e.g. BRL, CNY, PHP).

The Dollar Index (DXY) gained some ground during February, but remains depressed and below the 100 level (even this am after the Iran conflict hit over the weekend):

Maybe it is still too early (06:30 am), but that failure of the USD, below versus the EUR, to show significant “safe haven” gains in the first hours of trading is somewhat worrisome and should be observed closely:

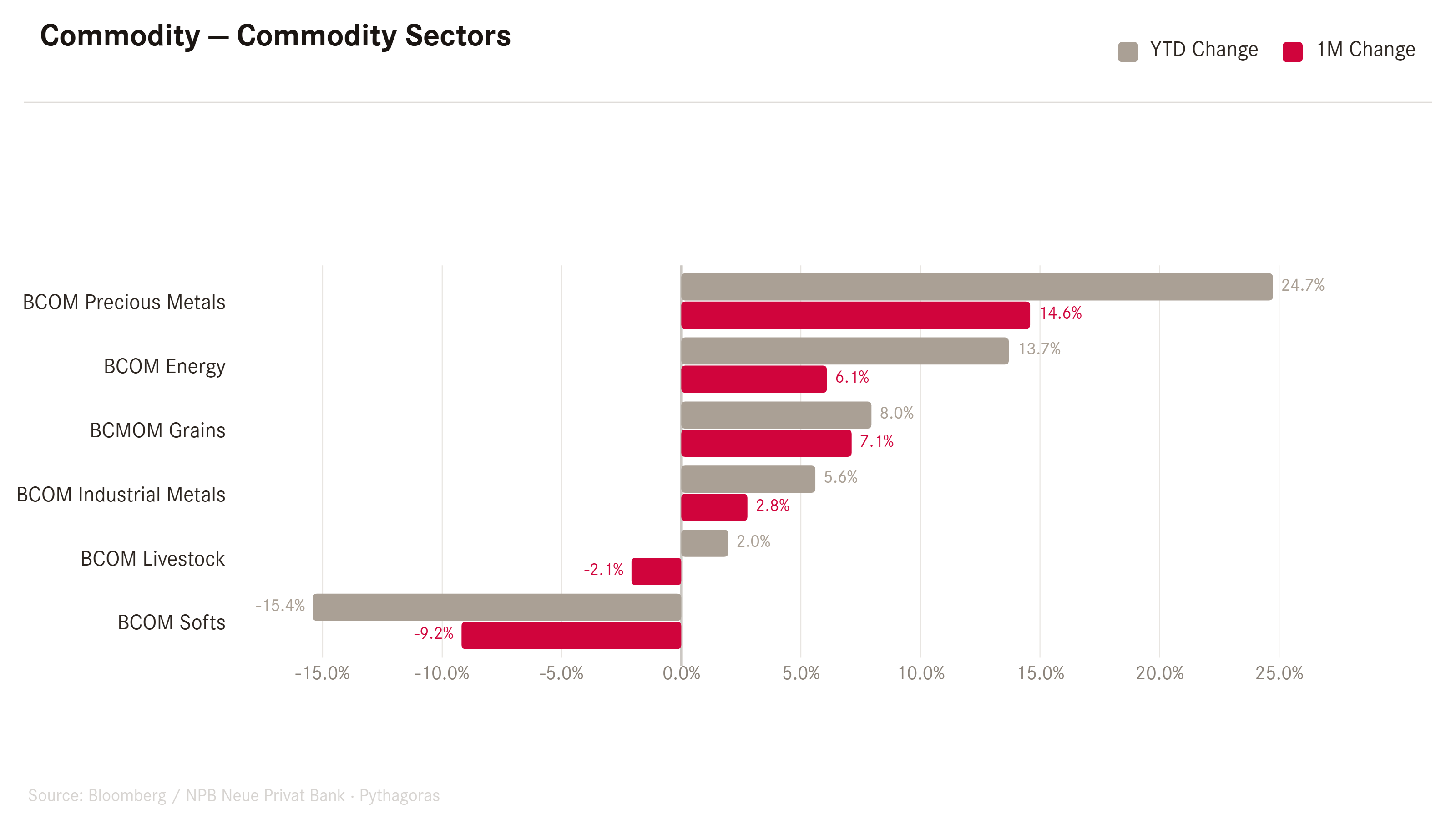

In commodities, it is of course difficult to make any qualified comments given the turmoil in Iran and the news surrounding the Strait of Hormuz. First to note is that all performance tables below are from BEFORE the kinetic action hitting over the weekend.

In terms of commodity “sectors” performance, precious metals once again are taking the lead, not least thanks to a very strong February performance:

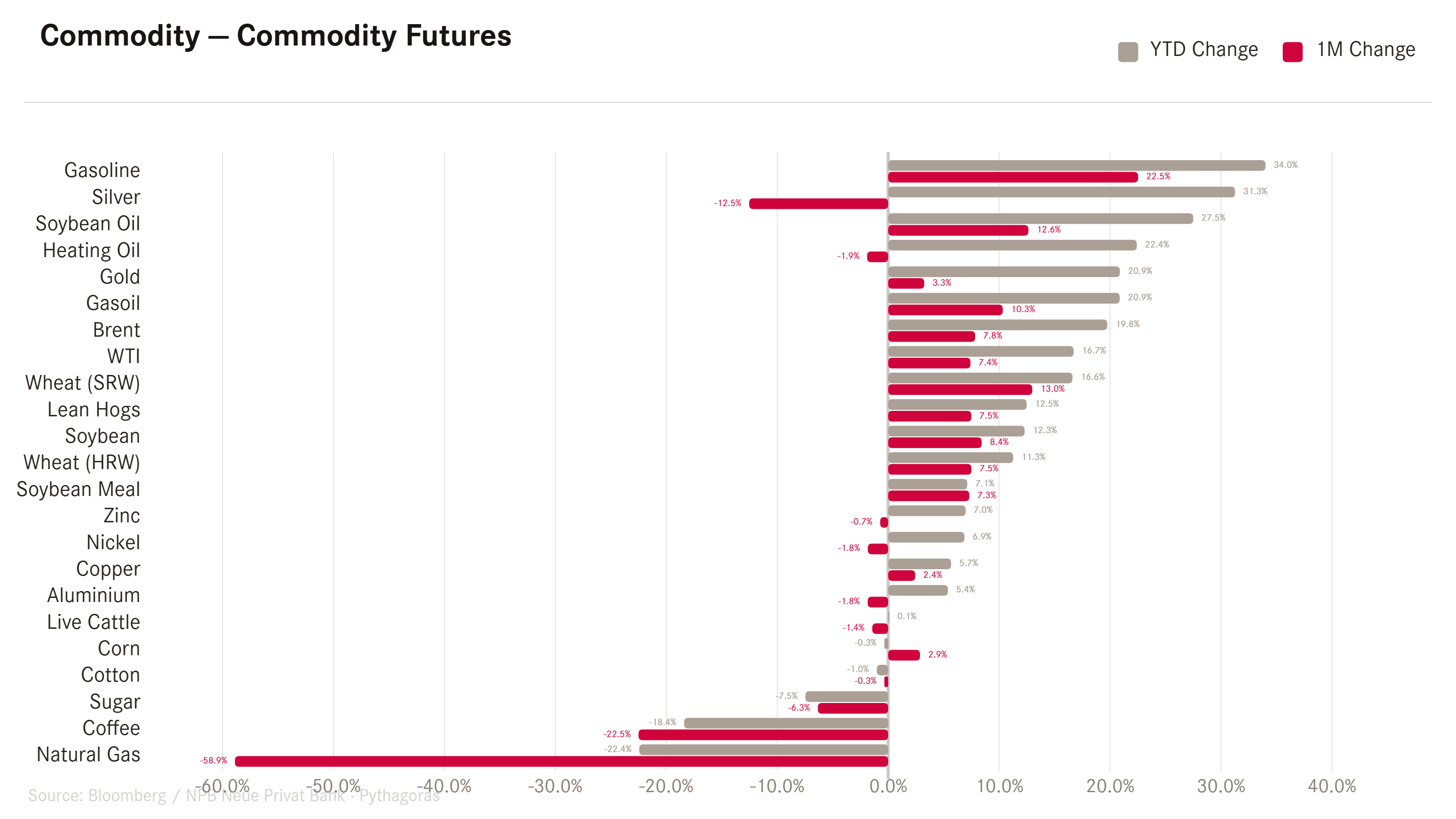

Looking at some popular commodity futures, we note that energy-related commodities (ex Natural Gas) have started climbing the leader-board ladder:

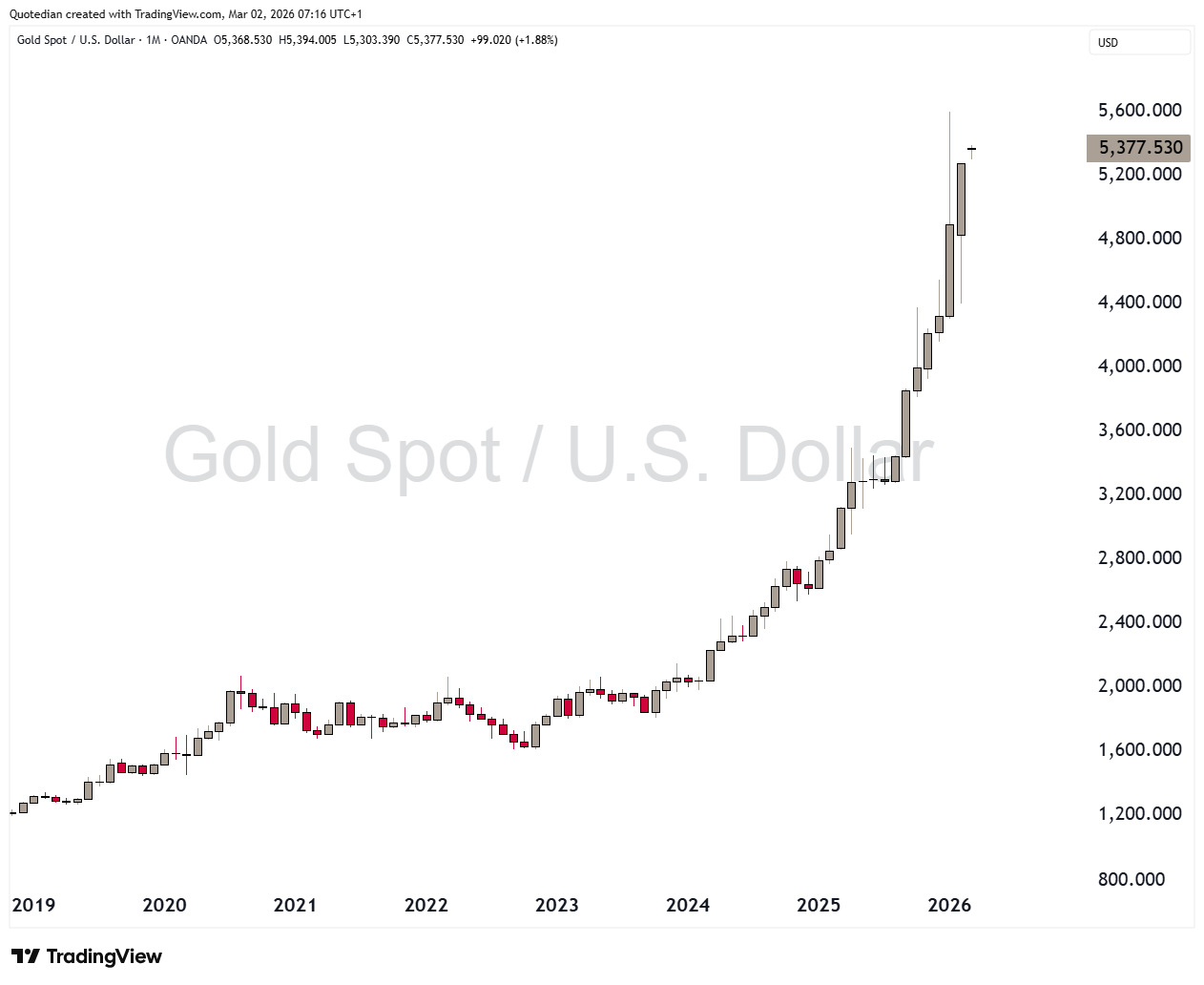

Following charts are now AFTER the Iran conflict, i.e. from this early Monday morning.

Gold is up about two percent, and whilst briefly trading higher in January is now at its highest would the month end today (which it of course does not):

Silver is up a ‘disappointing’ one percent only early this Monday:

Though, given that Silver is NOT a safe haven asset, this smaller reaction actually makes a lot of sense. Dynamics of tailwinds for silver are of other nature (supply constraints at COMEX).

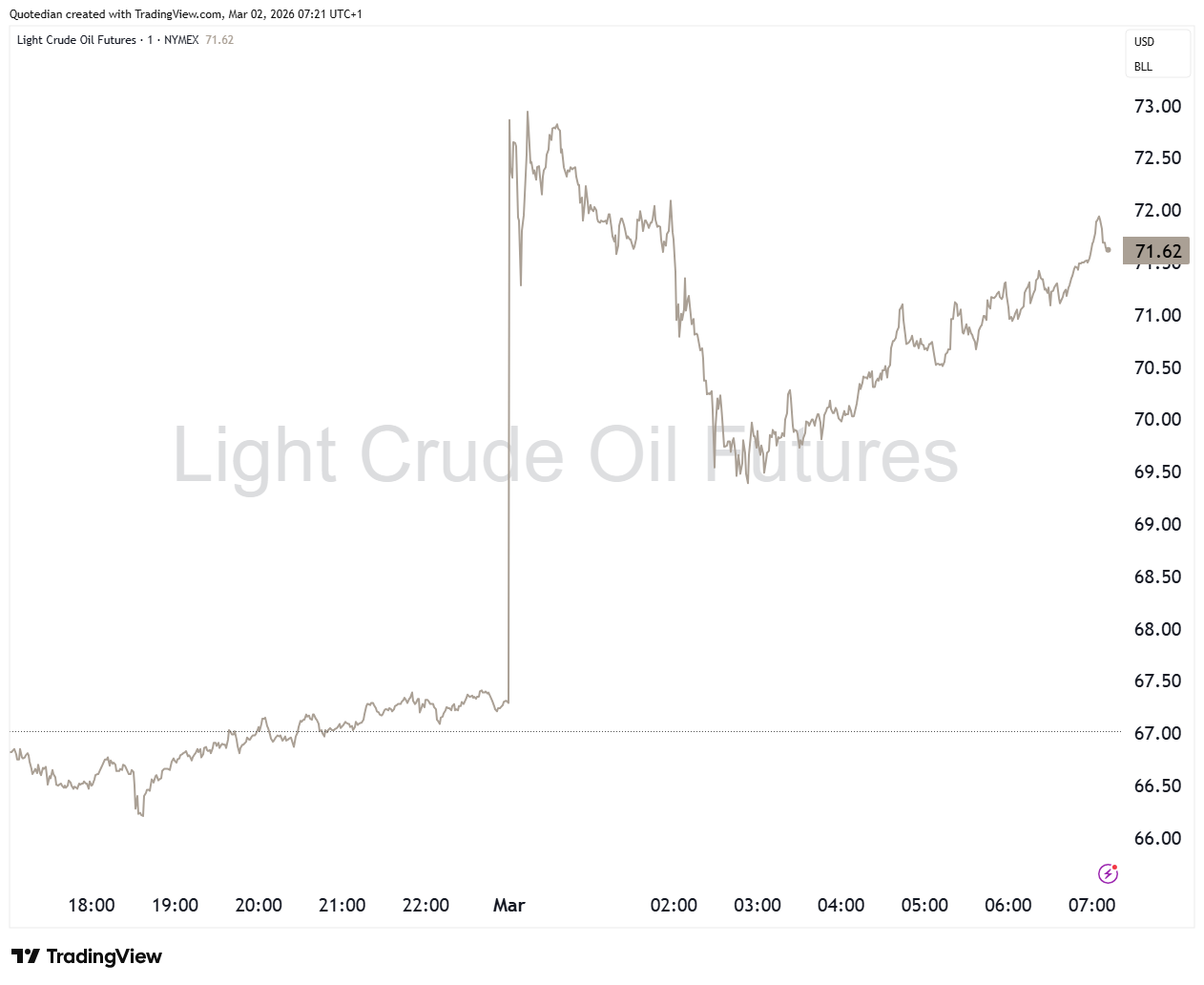

But THE commodity of focus is of course crude oil, which in its international Brent version is up seven percent his morning,

but hit nearly USD73 in overnight trading:

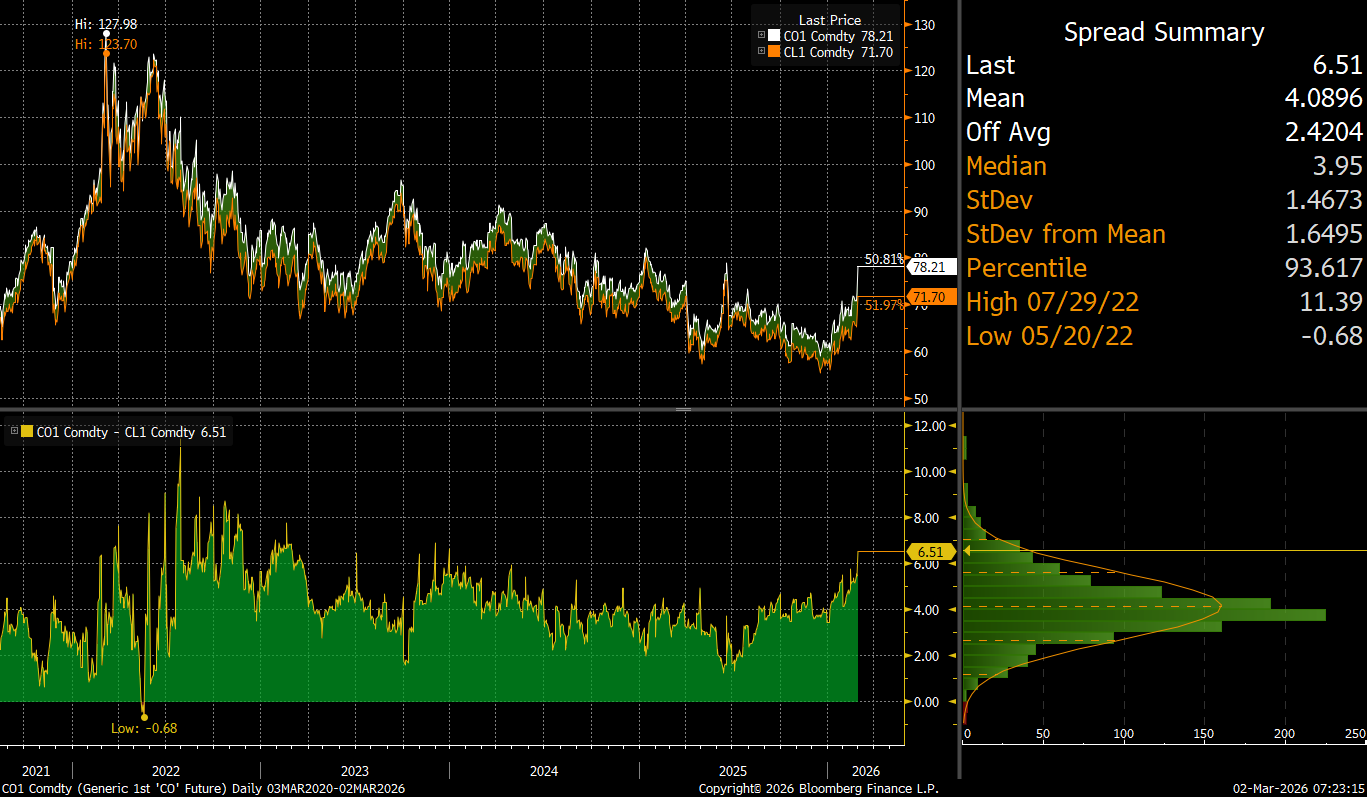

The spread between this more international (Brent) price of crude and its more US-domestic focused WTI price should probably widen further, as it did during the early days of the Ukraine-Russia conflict:

In conclusion, the best advice I can give you (for investment management) in the early stages of any kinetic conflict is,

DON’T BE A HERO

After all, even legendary trader Paul Tudor Jones told you that:

However, be smart, and become a NPB client (click here) for good, savvy, patient investment advice.

May the Trend be with You.

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG