June Swoon

Vol IX, Issue 21 | A NPB Original

"The job of the Fed is to take away the punch bowl just as the party gets going."

— William McChesney Martin, Fed Chairman, 1955

Actually, this week’s letter was going to be called:

Show Me The Money!

and this was going to be the lead picture/gif:

The theme of course was going to be the Wall of (equity) Supply coming to markets over the coming weeks, from high profile IPOs (SpaceX, Anthropic, OpenAI, many other) and capital raising (Google).

And all this, at valuation levels which no clear-, straight-forward thinking investor would ever touch. But, as one of my favourite Substack-Writers and Meme-Creators, Le Shrub, recently wrote:

“The latest Star Wars film, “Mandalorian & Groku”, is now out in the cinemas. Reviews were horrendous but I’m still going to watch it.

Space-X is about to IPO. Valuation is horrendous but investors are still going to buy it.

We know it’s all stupid and we are pretty good at playing along…”

For sure:

Look, as mentioned on several occasions in the past, , and we are trying NOT to be a grumpy old man, shaking his fist at the cloud,

or screaming at the TV,

increased IPO activity has come towards the end of a bull cycle, not at the beginning.

Don’t believe me, dear Jury? Well,

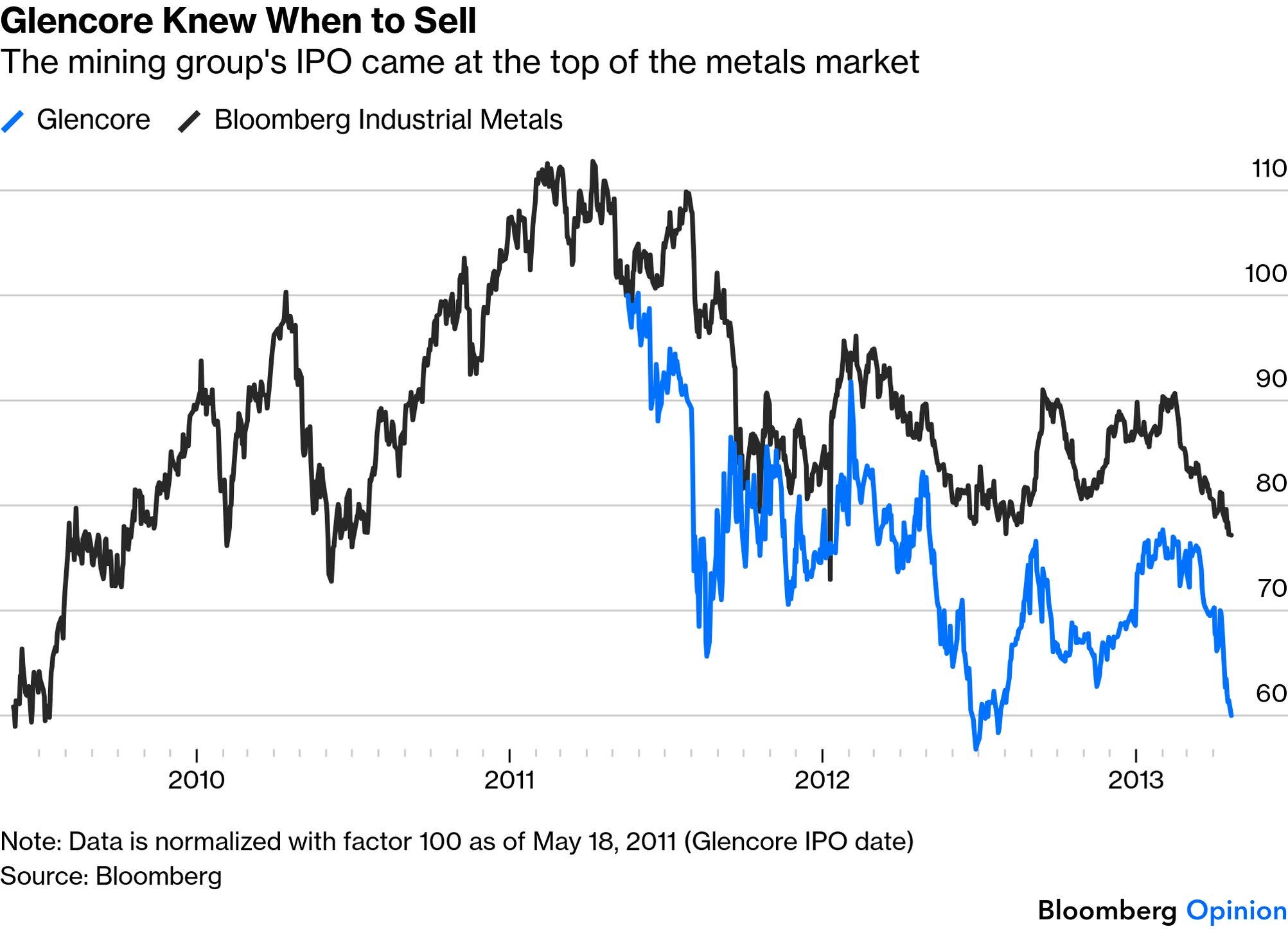

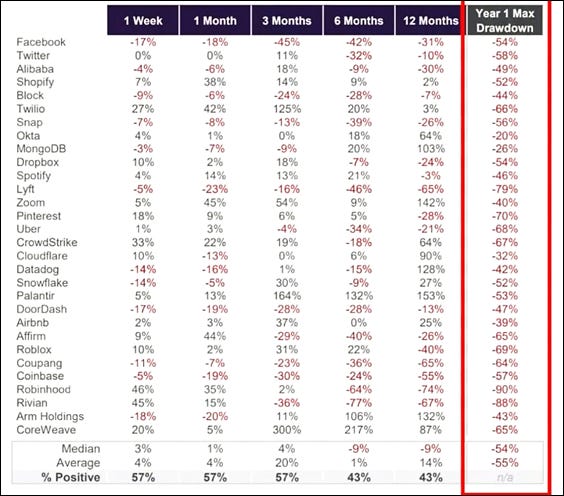

Exhibit 1 - Glencore

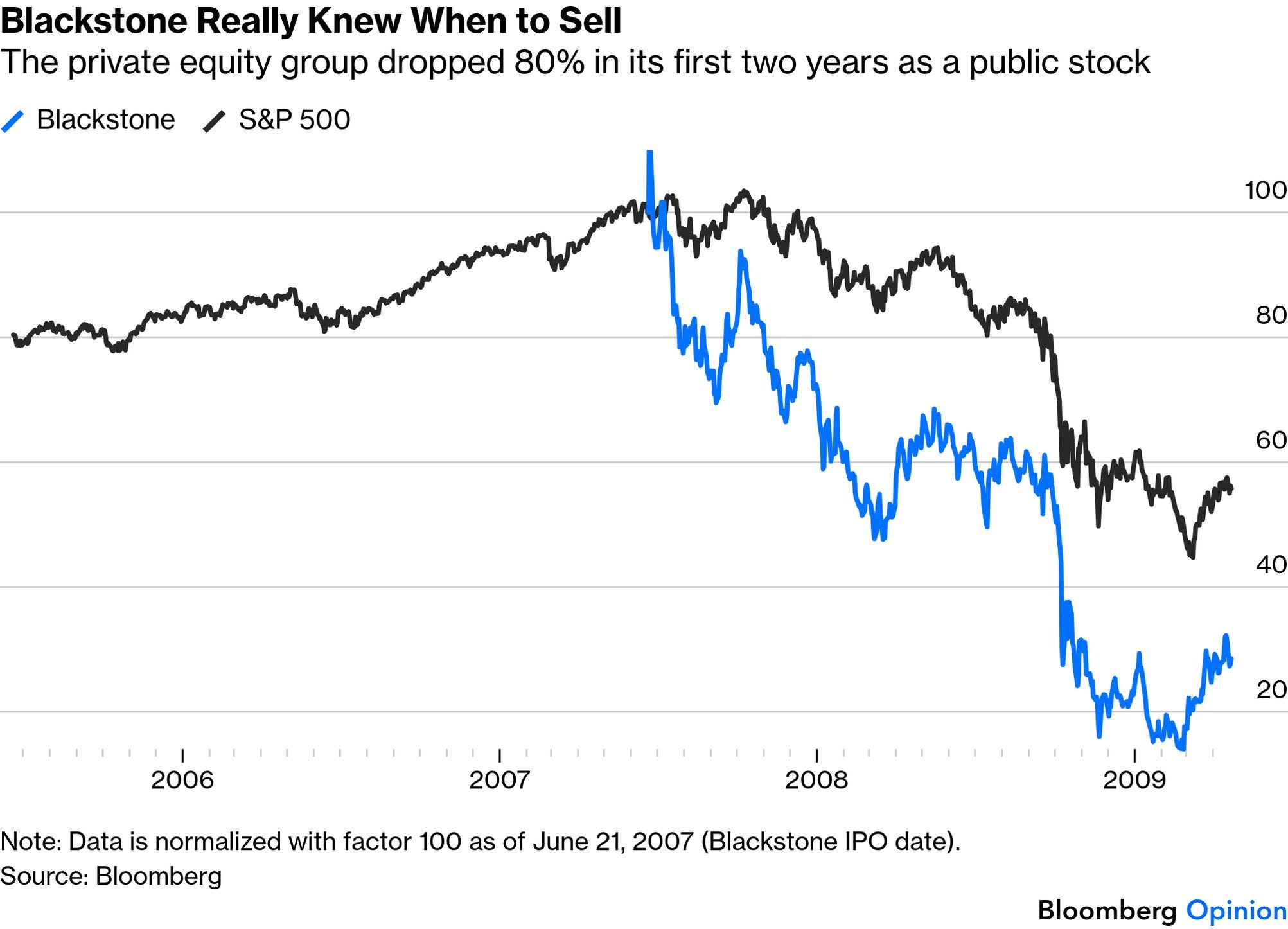

Exhibit 2 - Blackstone

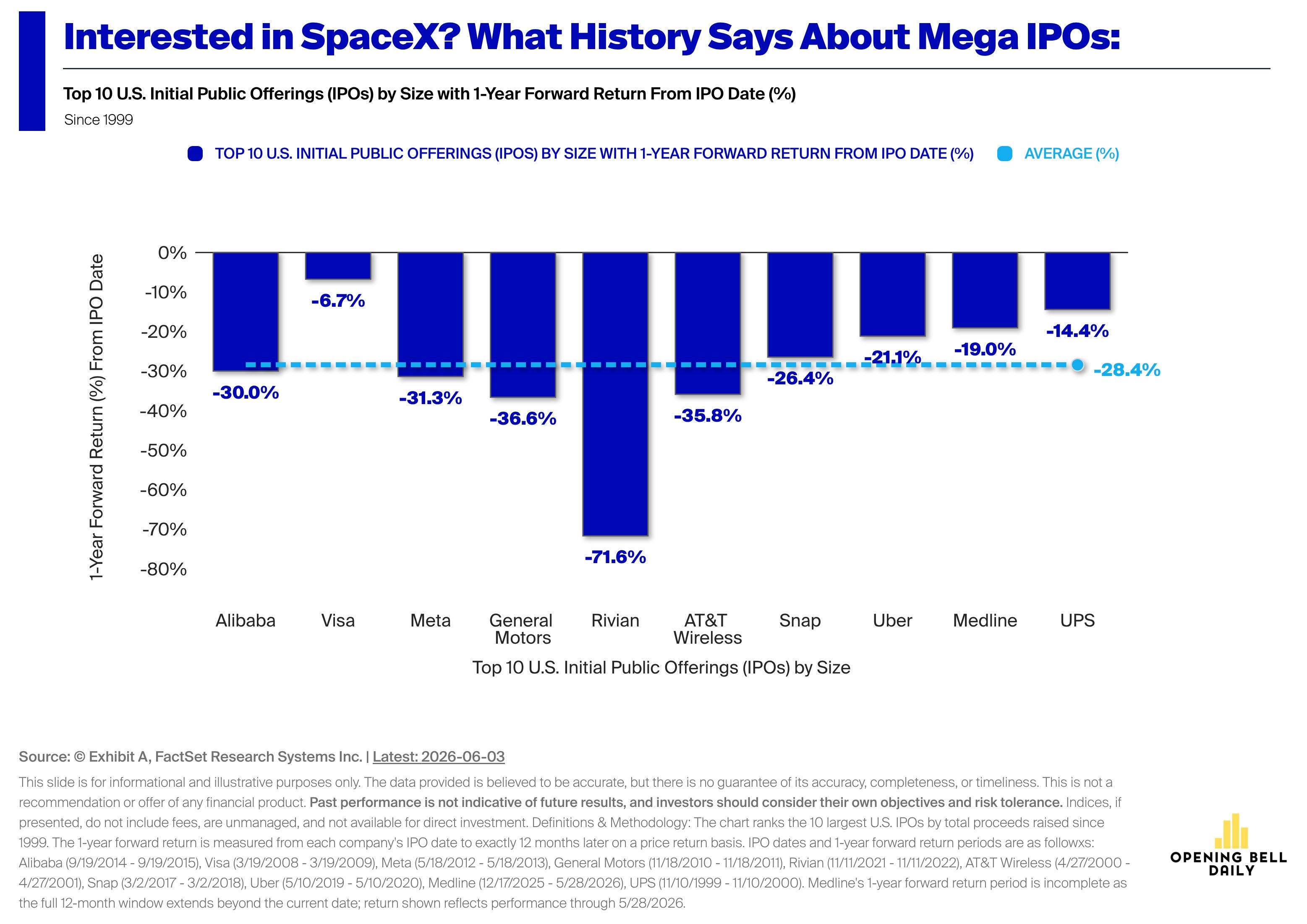

Exhibit 3 - More examples of “Success” investing into IPOs

Exhibit 4 - Even more examples of “Success” investing into IPOs

So, why is there such a bad outcome for investing into IPOs? Two main reasons, closely linked to each other:

Investment bankers will push companies to go public when the speculative fervour is elevated - like today.

Founders will go public when they think their companies may have reached full valuations - like today.

What’s that saying again in Poker? Ah, yes:

"As they say in poker, 'If you've been in the game 30 minutes and you don't know who the patsy is, you're the patsy.'"

— Warren Buffet, 1987 Berkshire Hathaway shareholder letter

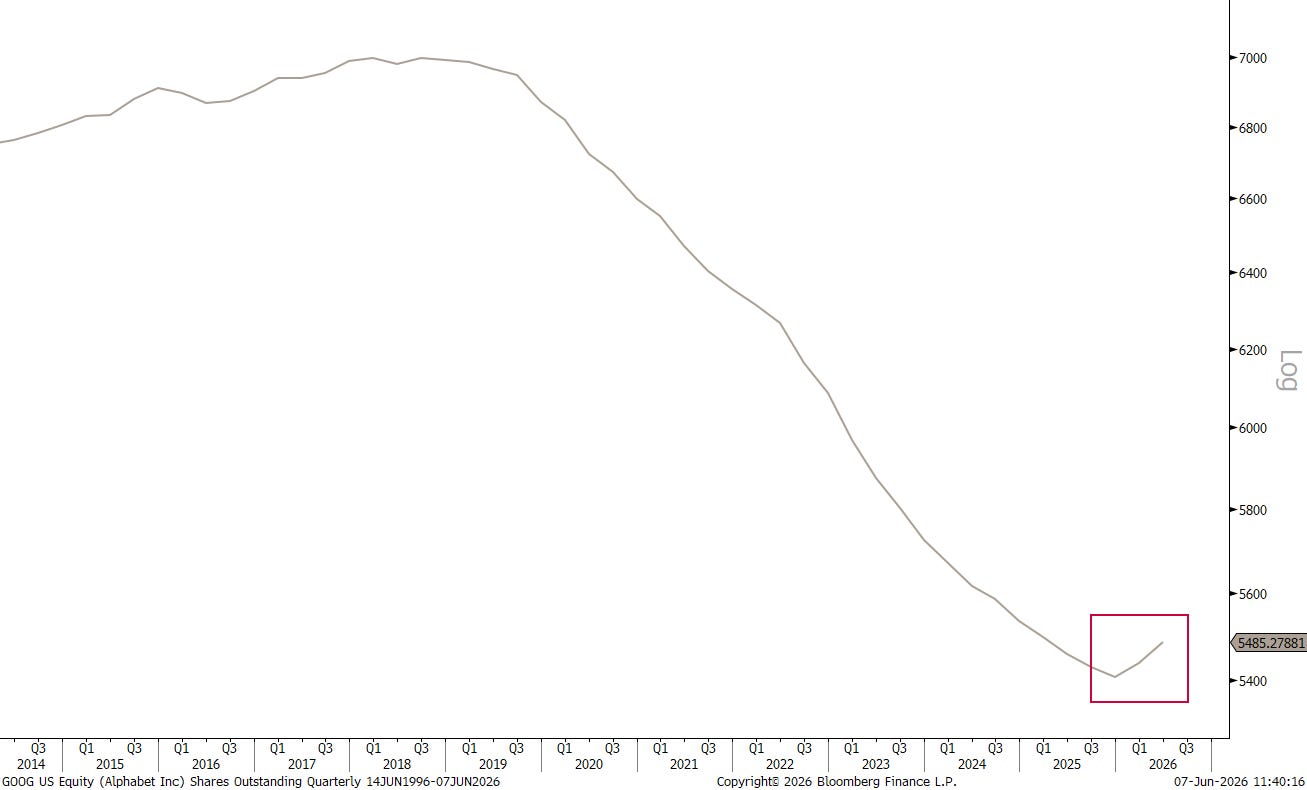

This pending flood of IPOs, which is now being ‘reinforced’ by companies which have been retiring equities for years, suddenly become net equity issuers again, such as Google,

or Meta

is one of two major concerns I highlighted earlier this year, not least in NPB’s Q2 investment committee outlook (click here).

The other, second major concern is a passive investing. Without going into details, Friday’s sell-off was a good example of what happens when an index (e.g. S&P 500) gets too one-sided (e.g. Technology), as passive Dollars have been flooding into the same 10 stocks at increasingly massive scales. But that’s a theme for another, dedicated newsletter…

In the meantime, let’s have a look at those last two, fatal trading days of last week, with especially the latter probably being a near-death experience for many over-levered investors.

It seems longer ago than only last week, that we wrote in the Quotedian titled “Chip, Chip, Hooray” (click here) the following:

Sooooo, what will it be? More CHIP, CHIP, Hooray or was that all, folks?

Probably this little GIF out of the Wile E. Coyote universe may be a close parallel of what is happening and may happen:

We were not surprised, as we manifested in a letter to your clients (click here).

However, there was at least one investor which was caught out wrong footed and in his usual spoil-sports manner got upset about it:

Let me try and make a simple drawing for you, Mr DJT:

Of course, Uncle Donald has a point, BUT only in a market not priced to perfection already, which, given the vehement sell-off on Friday it clearly was!

Again, what I did write last week was:

What I can to anyone willing to listen is a hunch, plus a not-so-bold-but-convinced prediction.

The Hunch: There’s more upside.

The Prediction: Volatility is about to increase.

Regarding the latter, here’s the full statement, which you can print and hang on your wall until true:

We only need one AI data-centre build being cancelled to violently shake-out the weaker hands … and given the record leverage, massive call buying and complacency going on, the maybe not so weak hands too.

So, as I often (and recently more it seems more often) like to say:

Right for the wrong reason, but I’ll take it!

Let’s look at some of the damage now … or, maybe, what little damage really has been done …

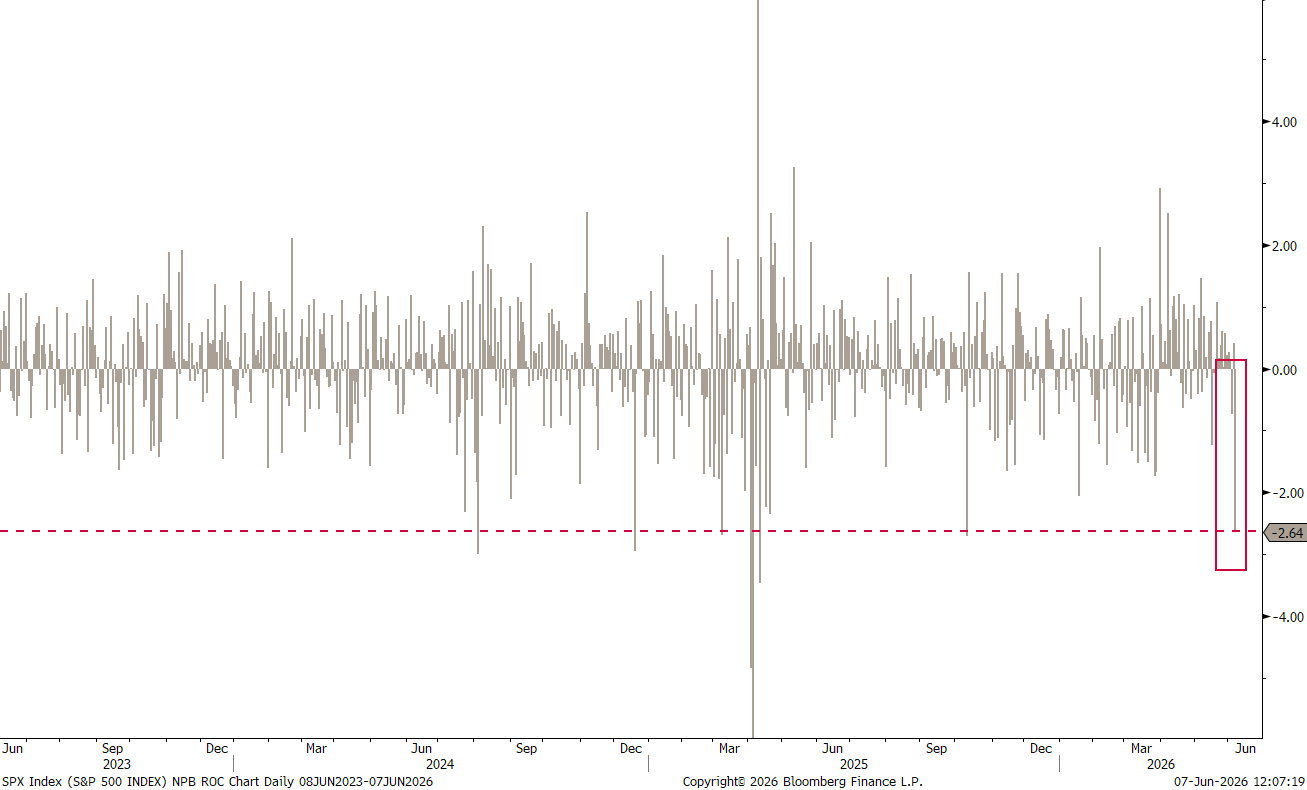

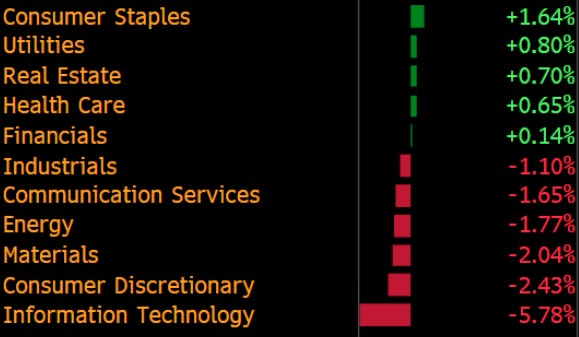

Whilst the S&P 500 had one of its worst days (-2.64%) in a while,

actually the ratio of up (237) to down (265) stocks was nearly balanced, and five out of eleven sectors actually managed to end up on the day,

leaving us with following where colourful heat map:

As unbelievable as it seems, but the Dow Jones Transport and Utility indices actually close up on the day:

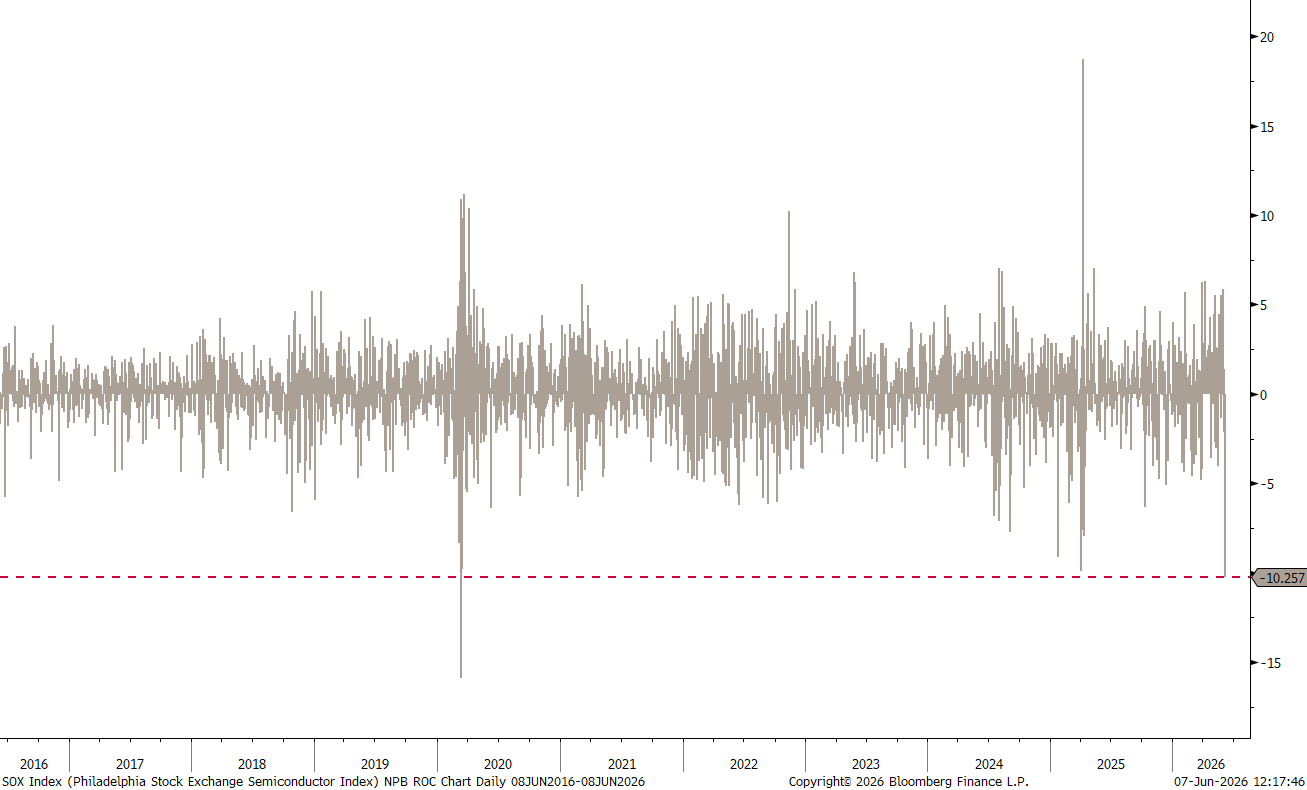

But back to areas where some real damage was done. The Philadelphia Semiconductors index saw its worst drop (-10.26%) since those dark COVID-days:

Of course, we are not all invested into the SOX stocks, but for sure many of us are exposed to the fortunes of the Nasdaq 100 (-4.77%) companies, where the largest distractors reads like the who-is-who of recent bellwhethers:

Should we have known a storm was brewing? Perhaps …

Whilst there is never somebody ringing a bell at the a top, there were signs to take some chips of the table.

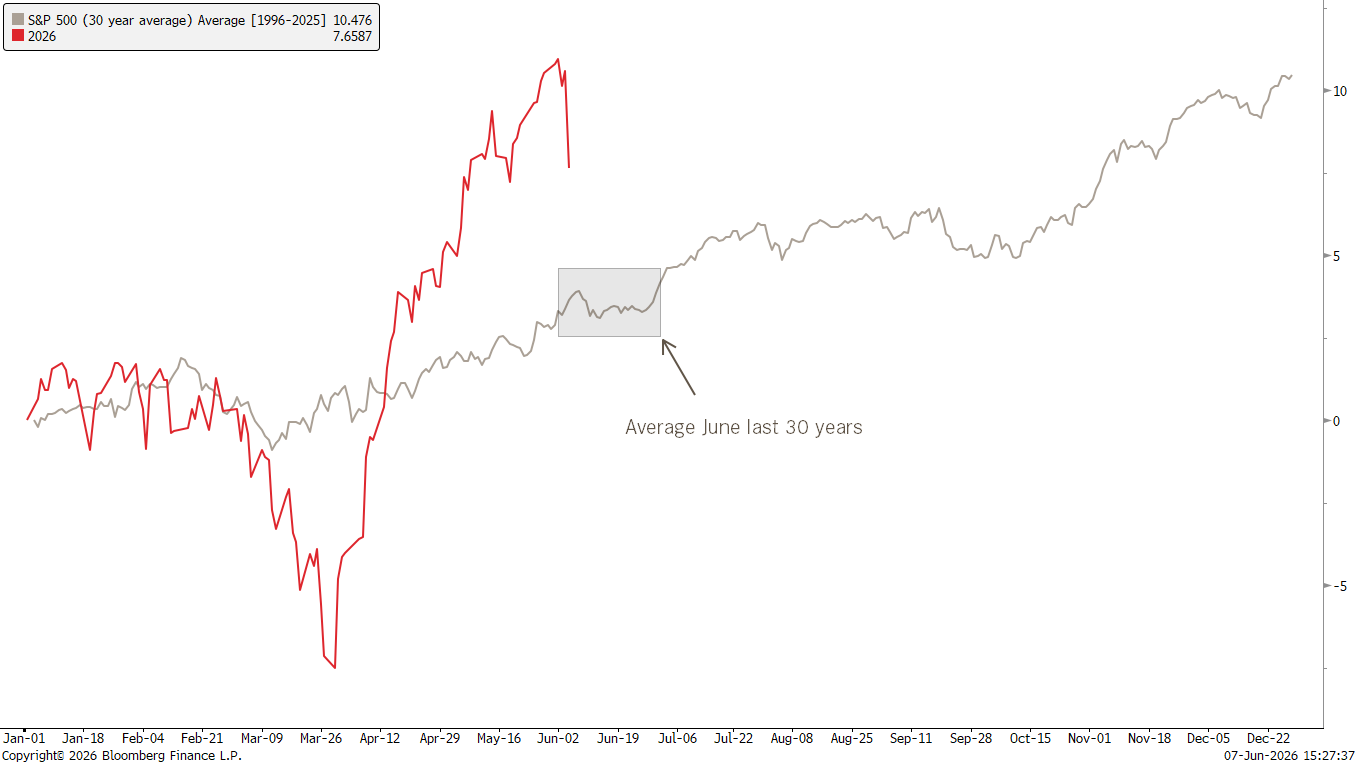

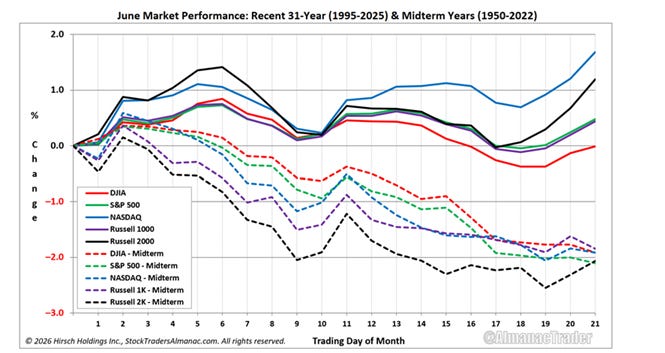

For example, has June been a month of “pause & reflection” over the past thirty years:

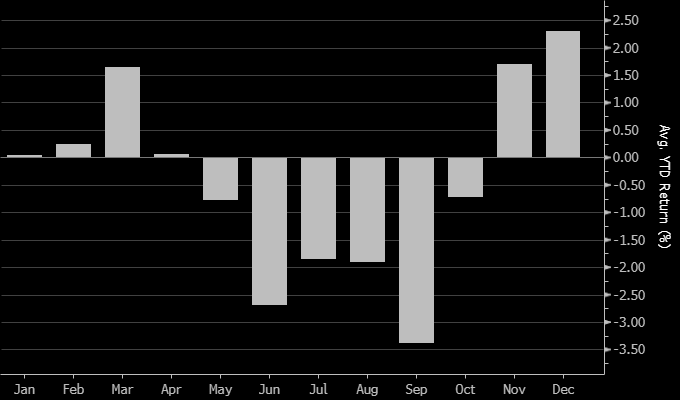

And if we take into account that we are in a (US) midterm election year, we should have been all the more warned that the difficult period is starting right now. The following chart combines the monthly returns of all election years going right back to the beautiful year of 1970:

Here’s another way to look at this - a direct comparison of June performance in all years versus mid-term years (dashed):

The following chart, which we already looked at last week, but now with the consquential update, was indeed also a “spoiler”:

The following monthly chart of the ratio between the Nasdaq Composite and the S&P 500 indices would become epic, should it indeed turn lower from here:

So this leave us with the questions: Was that it or is there more downside ahead?

Spoiler Alert:

But let’s have a look at some ‘evidence’ anyway …

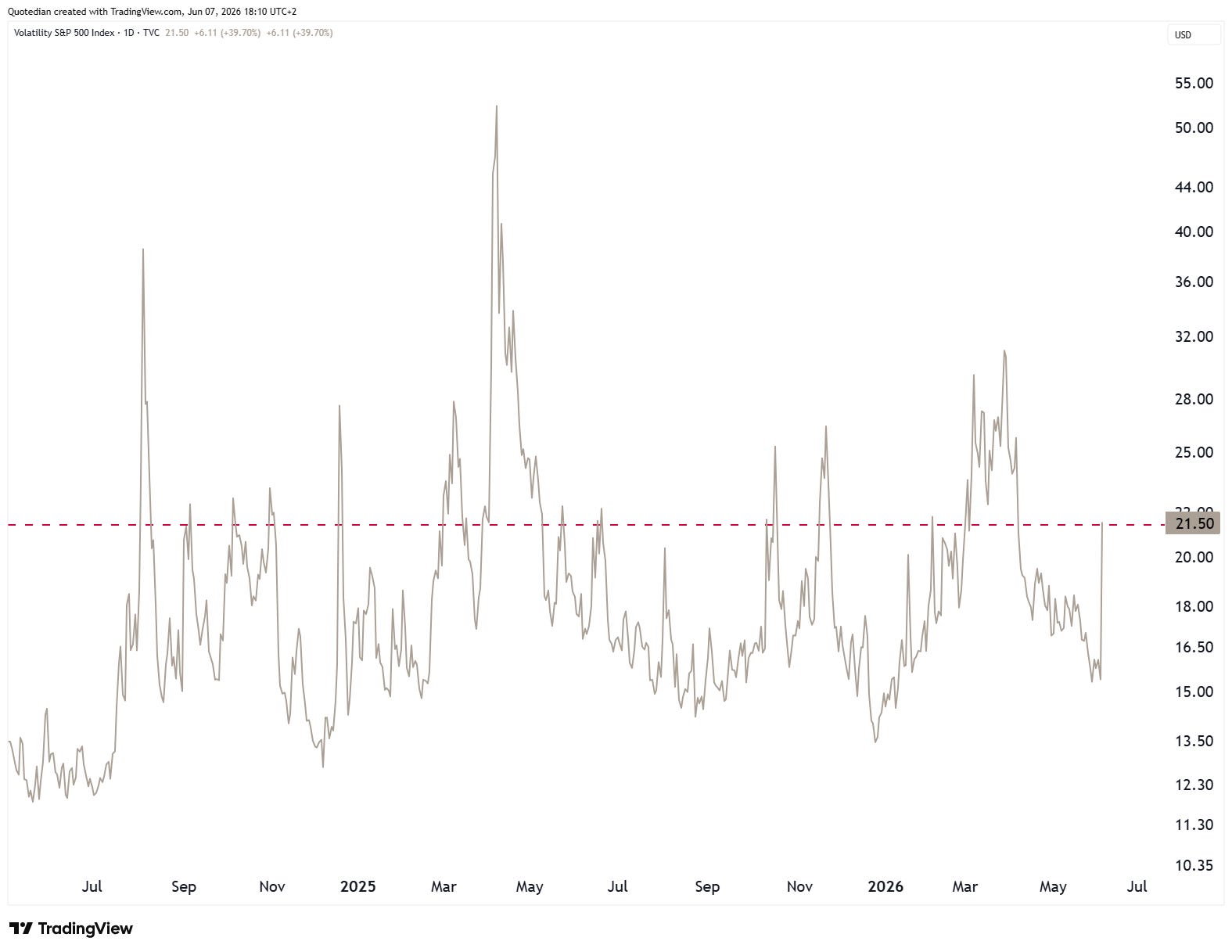

The VIX spiked, but is below most previous blow-out tops:

Bitcoin, on this occasion a liquidity AND risk-on/risk-off indicator did a good job of giving investors early warning signs, first through a topping out in early May and then a downward acceleration in late in the same month:

Over the weekend, the blood letting stopped, but BTC still moves within the downtrend channel, i.e. not giving a de-warning signal.

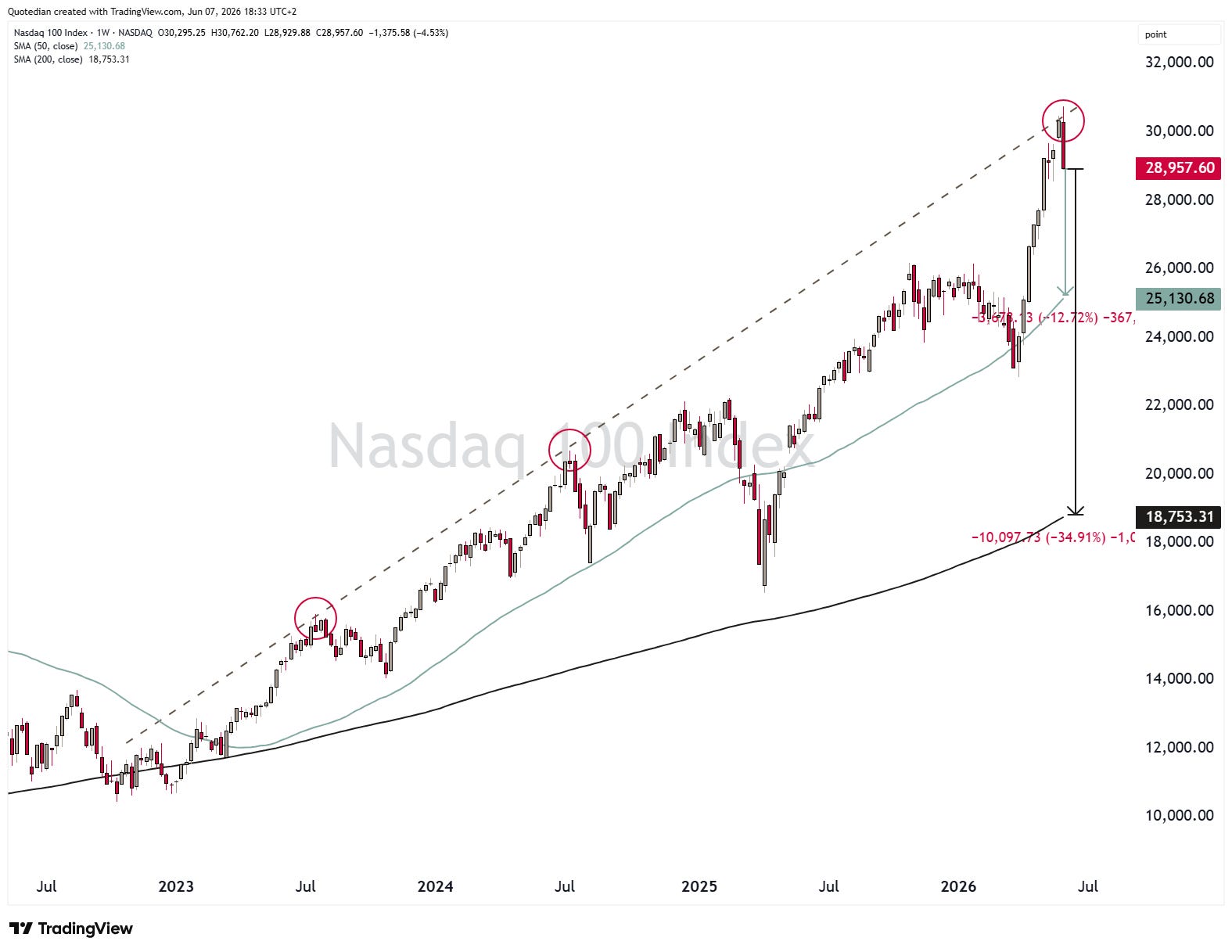

The Nasdaq 100, which also smashed its head against that beam of upper trendline resistance, is still 13% and over 30% above its 50- respectively 200-day moving average:

The SOX index, despite its 10% drop on Friday, is still …. oh, never mind…

Looking at a chart of the adults market (S&P 500), a pull-back to 7,000 would kind of make sense:

It’s the confluent zone of midway between the 50- and 200-day moving averages, roughly the 50% Fibonacci correction for the entire April/May up move AND the previous February/March resistance, now turned support.

Ergo, let’s prepare our buying list to be deployed as the S&P 500 pulls back some five percent or so from here…

Finally, a last equity observation before we head over into the fixed income section:

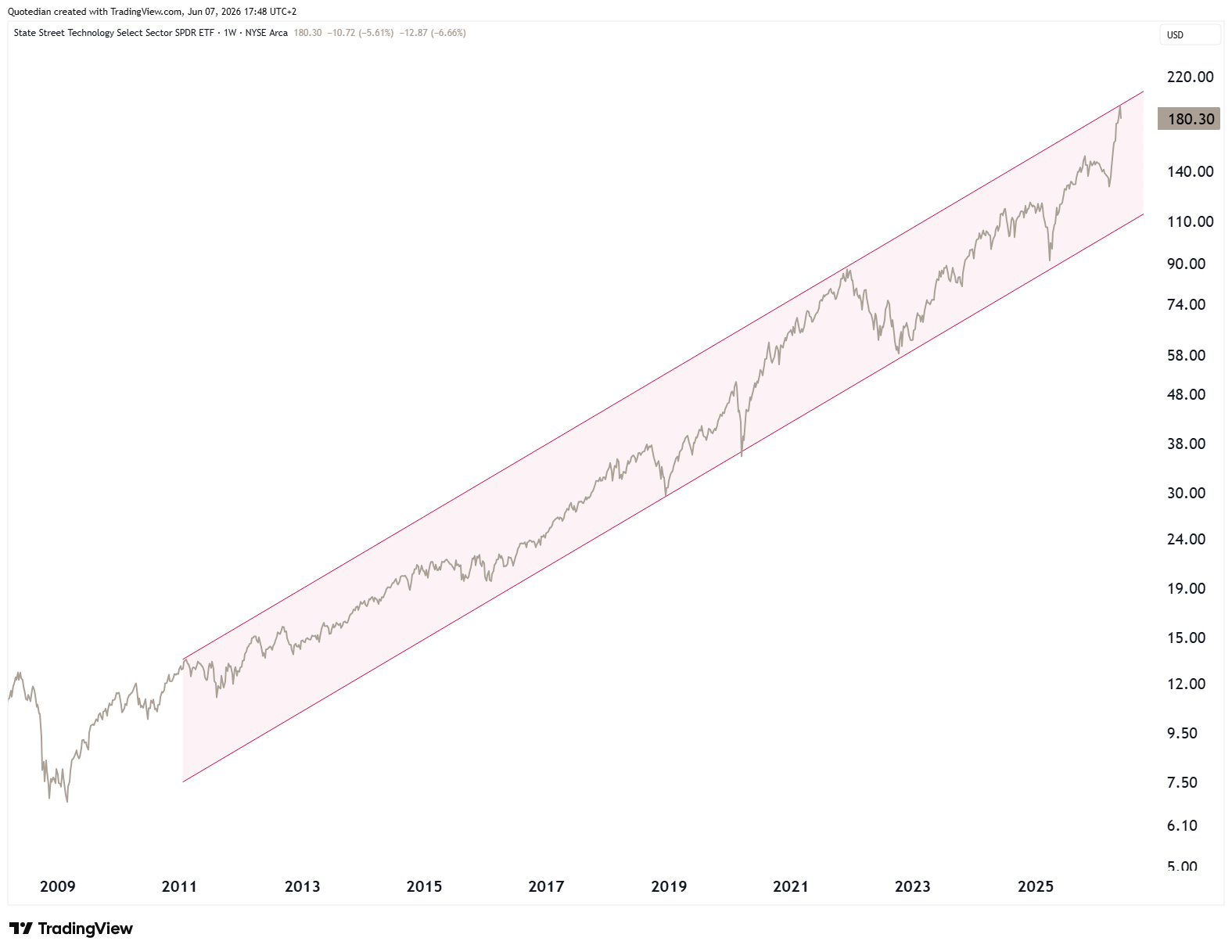

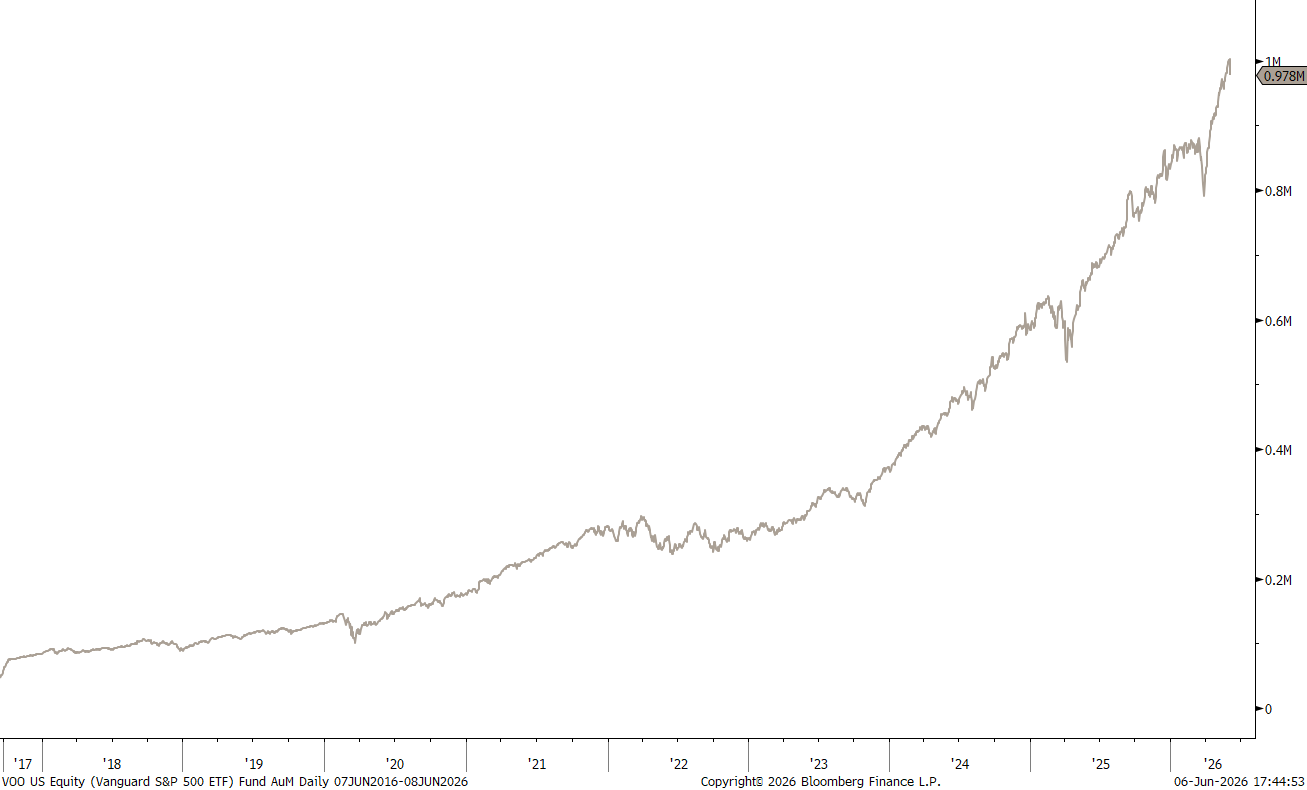

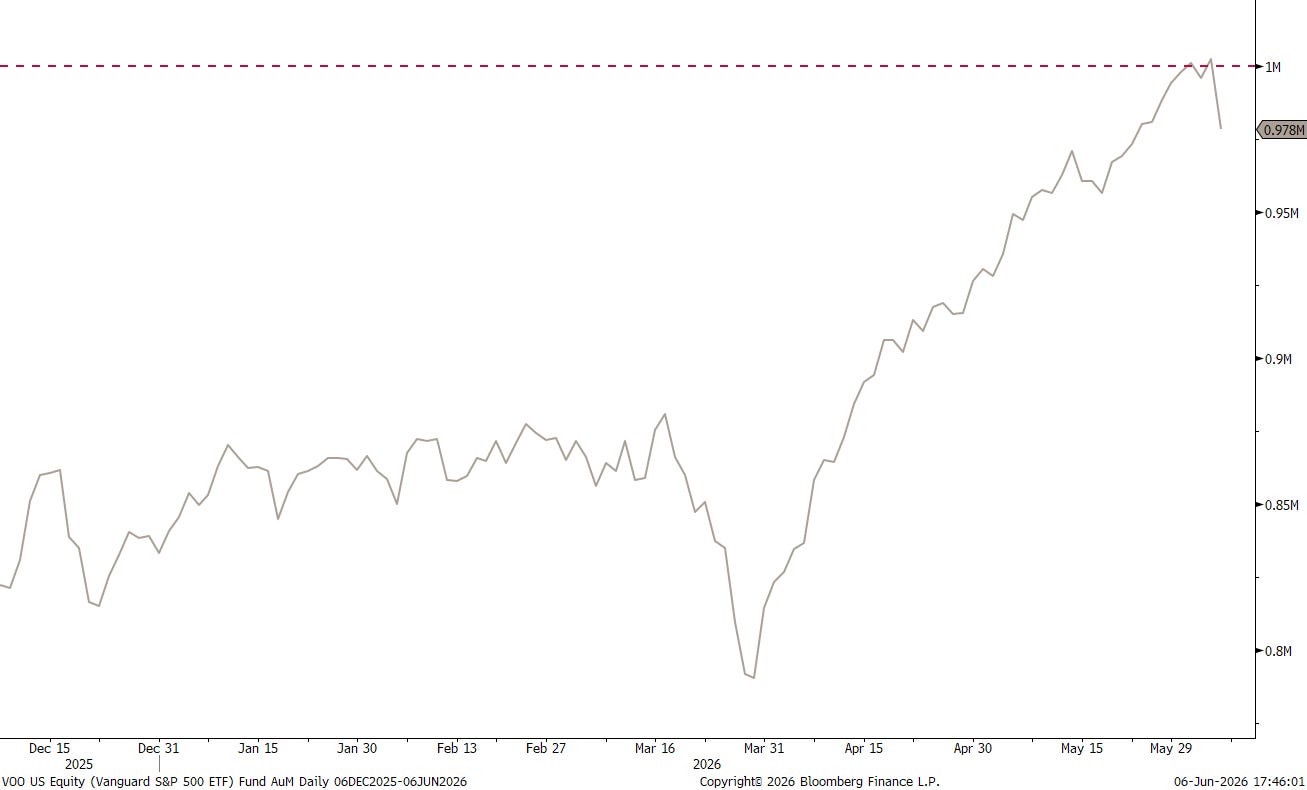

As usual, Mr. Market had sarcastically let the AuMs of the world’s largest hedge fund reach exactly USD1 trillion early on last week:

The increase in passively invested allocated assets as witnessed in the acceleration staring in late 2022 is absolutely impressive.

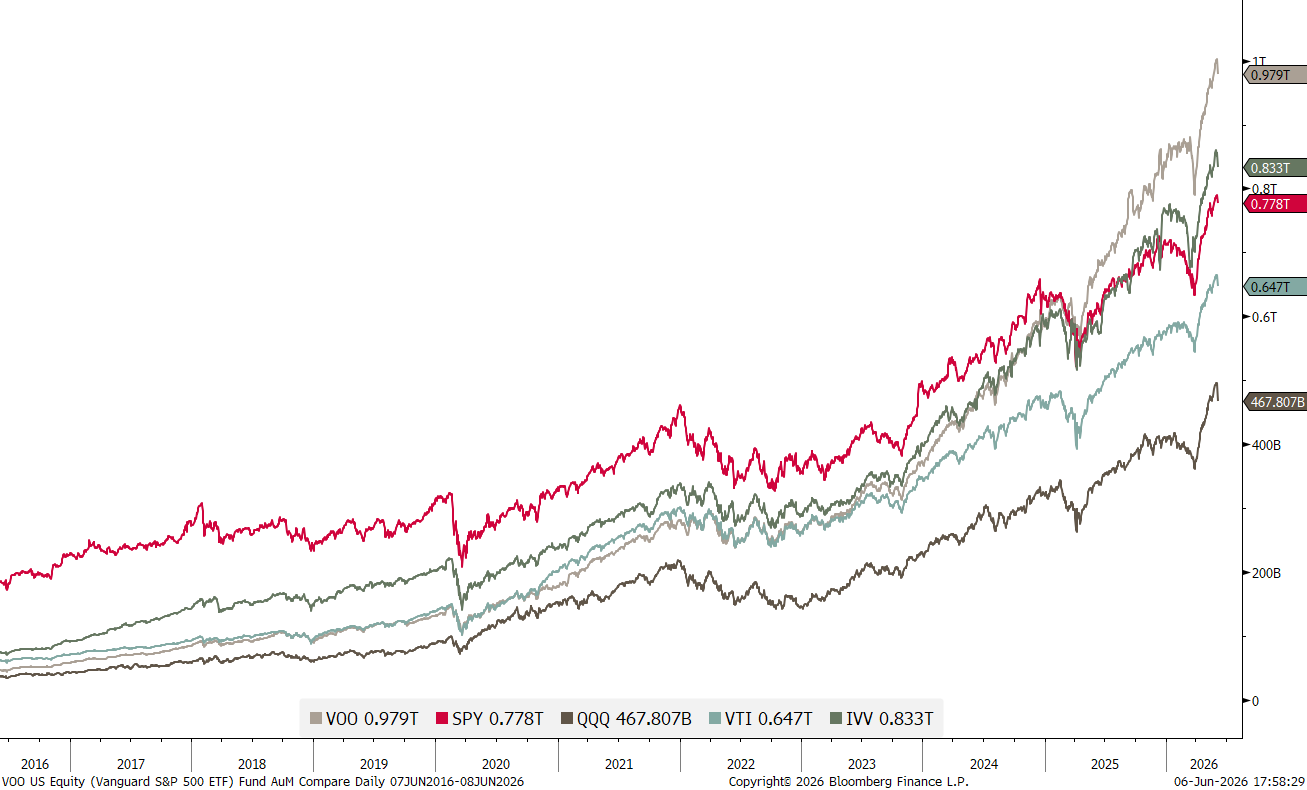

Also in relative terms to other major ETFs,

and then summing it all up … my word!

Anyway, the party didn’t last long as Friday the punch bowl was taken away for good …

and right now there’s seems to be no booze insight to get it started again …

Quite “au contraire”, if anything, it seems that all party-goers have been order an increased dose of monetary policy rate for the coming months. The Fed has gone from being expected to cut to at least one rate hike by year and (and rising):

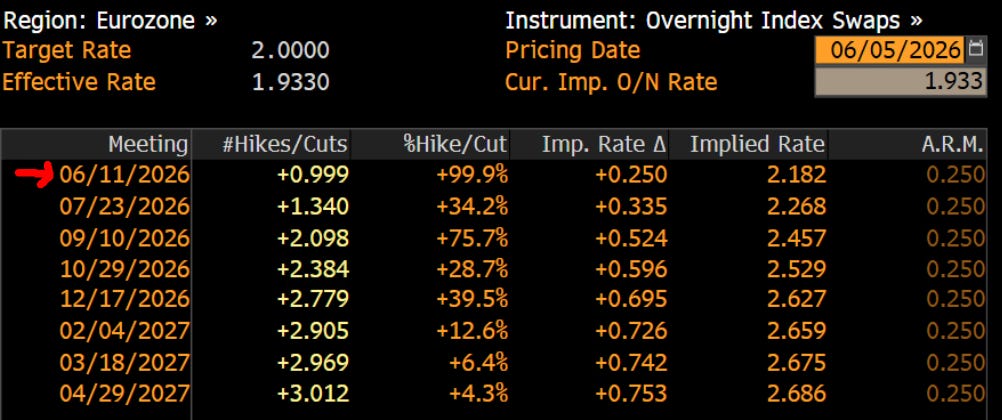

Whilst the ECB is expected to hike as soon as this week:

Friday’s NFP number, well above the esteemed (ehem) analysts’ expectations,

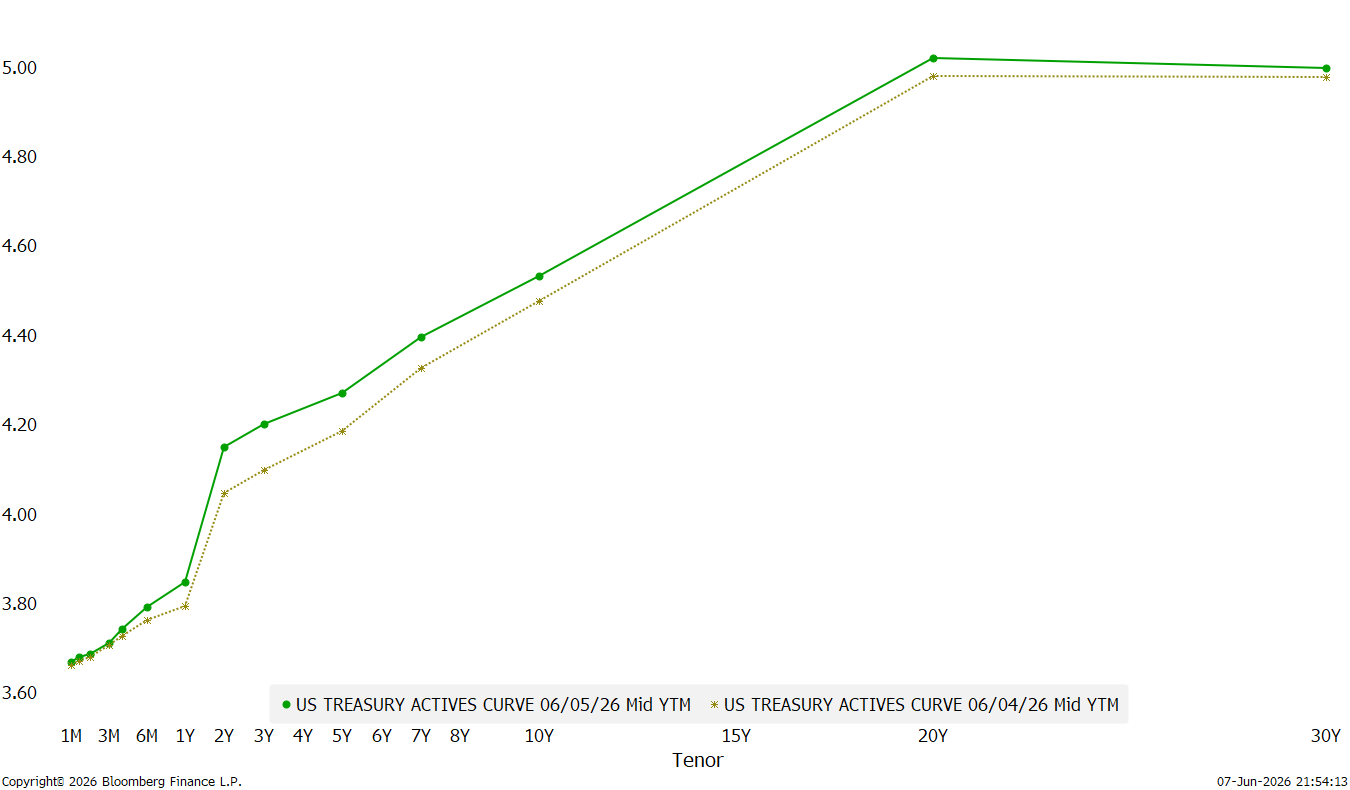

was of course one of the main reasons for that rate-path perception shift, as it was responsible for that jump in the entire yield curve:

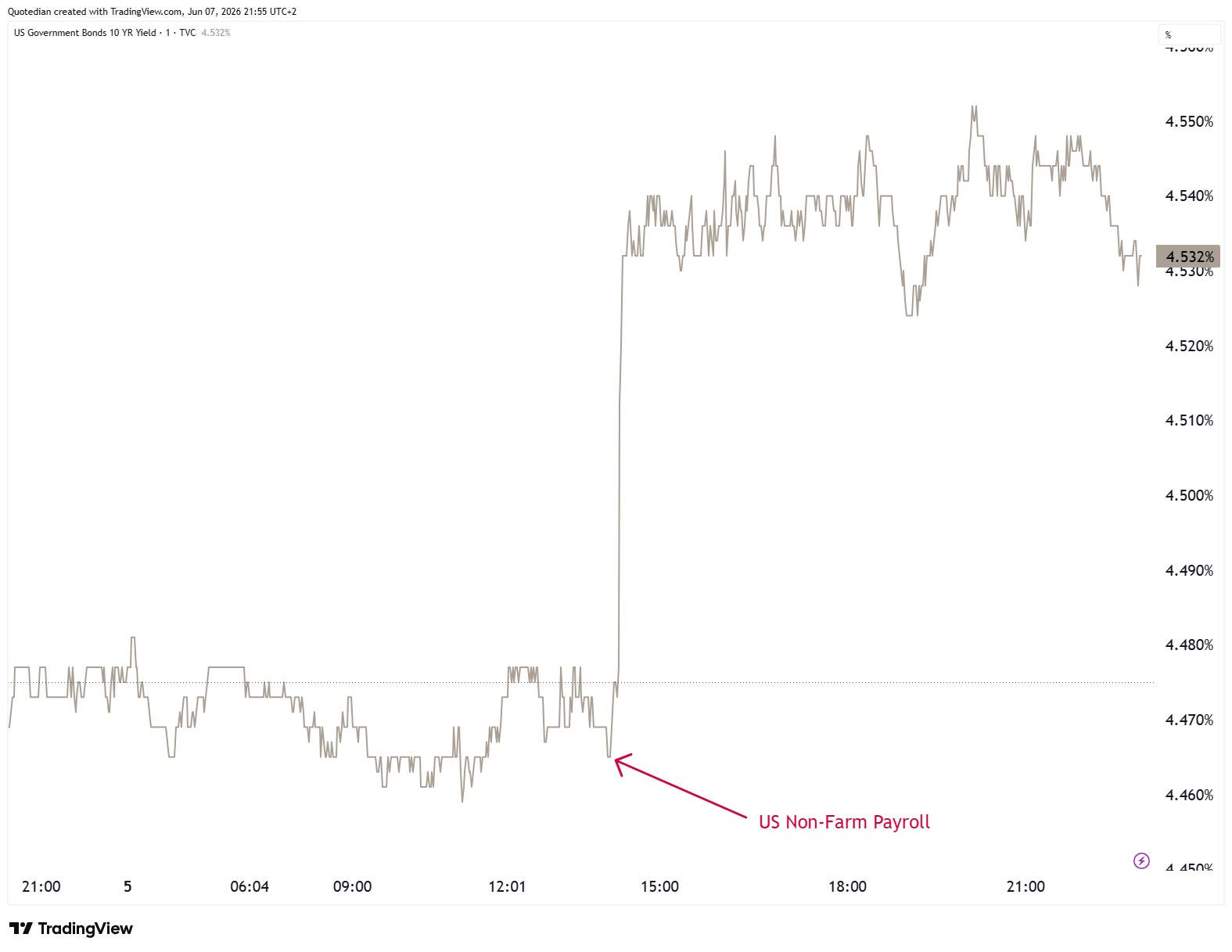

Here’s what happend to the 10-year US Treasury for example:

The daily chart of the same has turned upwards again, which takes our view that we may drop to 4.20ish before going higher probably off the table in favour of going higher directly:

US CPI is due on Wednesday - that could be a game changer either direction…

What else moved on Friday?

Currencies! The US Dollar is firmly up versus all other G-10 currencies since Thursday on the back of a sudden outlook of rate hikes i.o. rate cuts:

However, the US Dollar Index itself continues to remain range stuck:

The EUR/USD is heading towards key support zone at 1.1400 again,

whilst the USD/JPY cross is once again at the 160 BoJ/MoF intervention level:

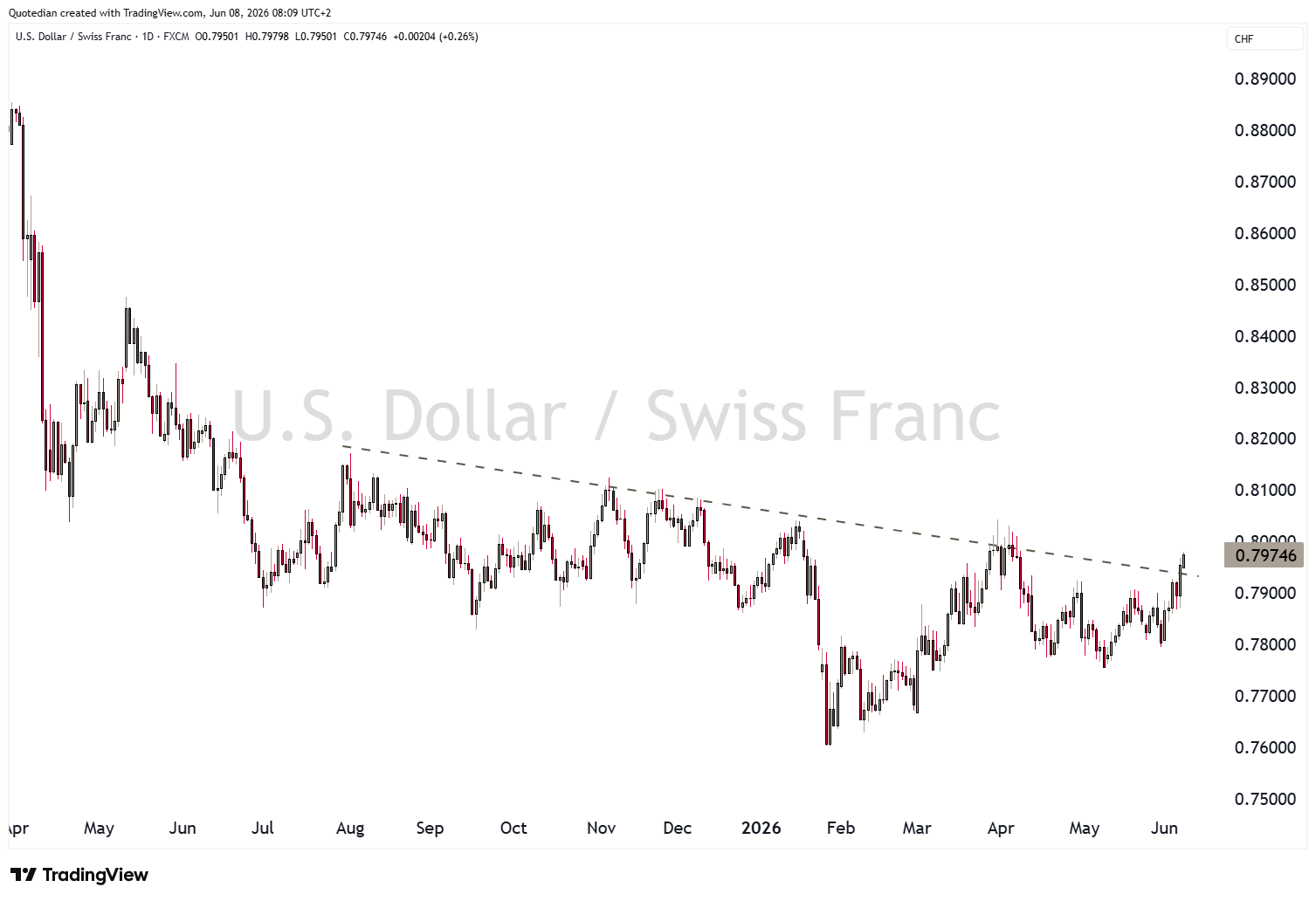

Finally, we are sure the Swiss National Bank doesn’t mind the break-out higher of the Greenback versus the Swissie on this chart:

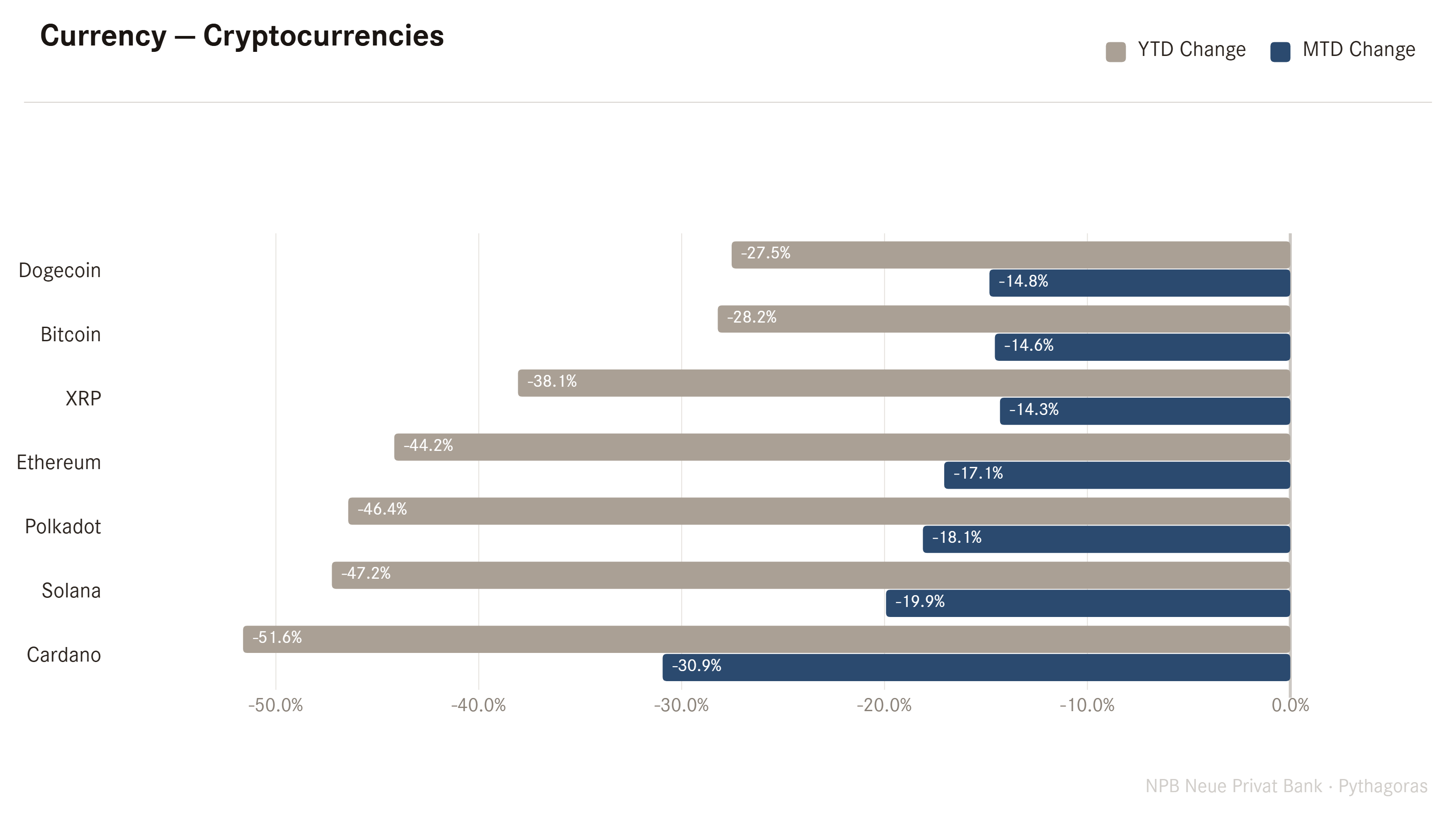

Cryptocurrencies, as already hinted to via our Bitcoin discussion further up, are having a ‘annus horribilis’, with a lot of the losses coming over the past 30 days:

Finally, if the US Dollar has moved, it is safe to assume that some commodities have been on the move too, as for example Gold:

Gold how now given back all year-to-date games and is exhibiting typical behaviour of a “burst-bubble”. For sure, its time to shine will come again, but not for the very foreseeable future.

Similarly, silver is on the cusp of breaking key support and will probably struggle to show any meaningful absolute returns over the coming months:

With this week’s letter already lengthy enough, I will stop here. Make sure to stay “a jour” with our market thinking in what will be probably a violent volatile week, by signing up to our daily Quotedian, if you have not done so yet:

But just before I let you go, do you not also feel a bit like this?

May the Trend be with You!

André

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG

Thanks. Wednesday's CPI is crucial. Here are my May CPI estimates, which have been better than Wall Street 70%-75% of the time:

https://arkominaresearch.substack.com/p/may-2026-cpi-estimate