PerFert Storm

Vol IX, Issue 12 | Simplicity is the Ultimate Sophistication

“Hell is empty and all the devils are here.”

— William Shakespeare, The Tempest

Fertilizer prices are rising and will bring food inflation with it.

Equity markets are falling into correction territory

Bond yields are flying and previous central bank rate cuts have now converted to expected hikes.

The US Dollar has rallied - but not as much as one could expect.

Gold is melting down as investors rush to sell what they can sell (and real rates are rising.

Oil prices are adjusting for a lengthy war.

Mr Shakespeare wasn’t writing about fertilizers. But he might as well have been.

Sometimes markets hand you a thesis so clean it almost feels suspicious. This is one of those weeks. A confluence of forces — geopolitical, macro, and structural — is quietly assembling into what we’re calling the PerFert Storm: a perfect setup for fertilizer stocks and agricultural names more broadly.

Let’s walk through the logic.

It starts, as so many things do right now, with Iran. The US-Israel strikes of February 28th didn’t just rattle oil markets — they introduced a non-trivial probability of Strait of Hormuz disruption into every commodity pricing model on the planet. Oil spiked. And where oil goes, natural gas follows. And where natural gas goes, nitrogen fertilizers follow — because ammonia doesn’t synthesize itself. The Haber-Bosch process is brutally energy-intensive, which means every tick higher in nat gas is a direct input cost shock to fertilizer production.

Here’s where it gets interesting. Not all producers are equal. European names like Yara and Grupa Azoty are squeezed between high feedstock costs and price-regulated domestic markets. Meanwhile, US producers like CF Industries sit on cheap Henry Hub gas and are laughing all the way to the ammonia plant.

Layer on top of that the Russia factor. Moscow remains one of the world’s largest exporters of potash, nitrogen, and phosphate. Sanctions have never fully normalised supply flows. Any further escalation — and the current geopolitical temperature is not cooling — tightens the global supply picture further.

Then there’s the macro overlay. In a stagflationary environment — which is increasingly what the data is whispering — hard asset producers with pricing power outperform. Food is the ultimate inelastic demand. You can defer a car purchase. You cannot defer eating. Fertilizer demand doesn’t go away; it reprices. And when it reprices, the producers with the right feedstock, the right geography, and the right balance sheet collect the windfall.

The PerFert Storm isn’t a single catalyst. It’s the convergence of all of them at once. And historically, that’s exactly when the most asymmetric opportunities emerge.

With that out of the way, let’s take our usual tour-de-force across the macro landscape, to see what has been going on and quite frankly, how sour everything is turning for investors …

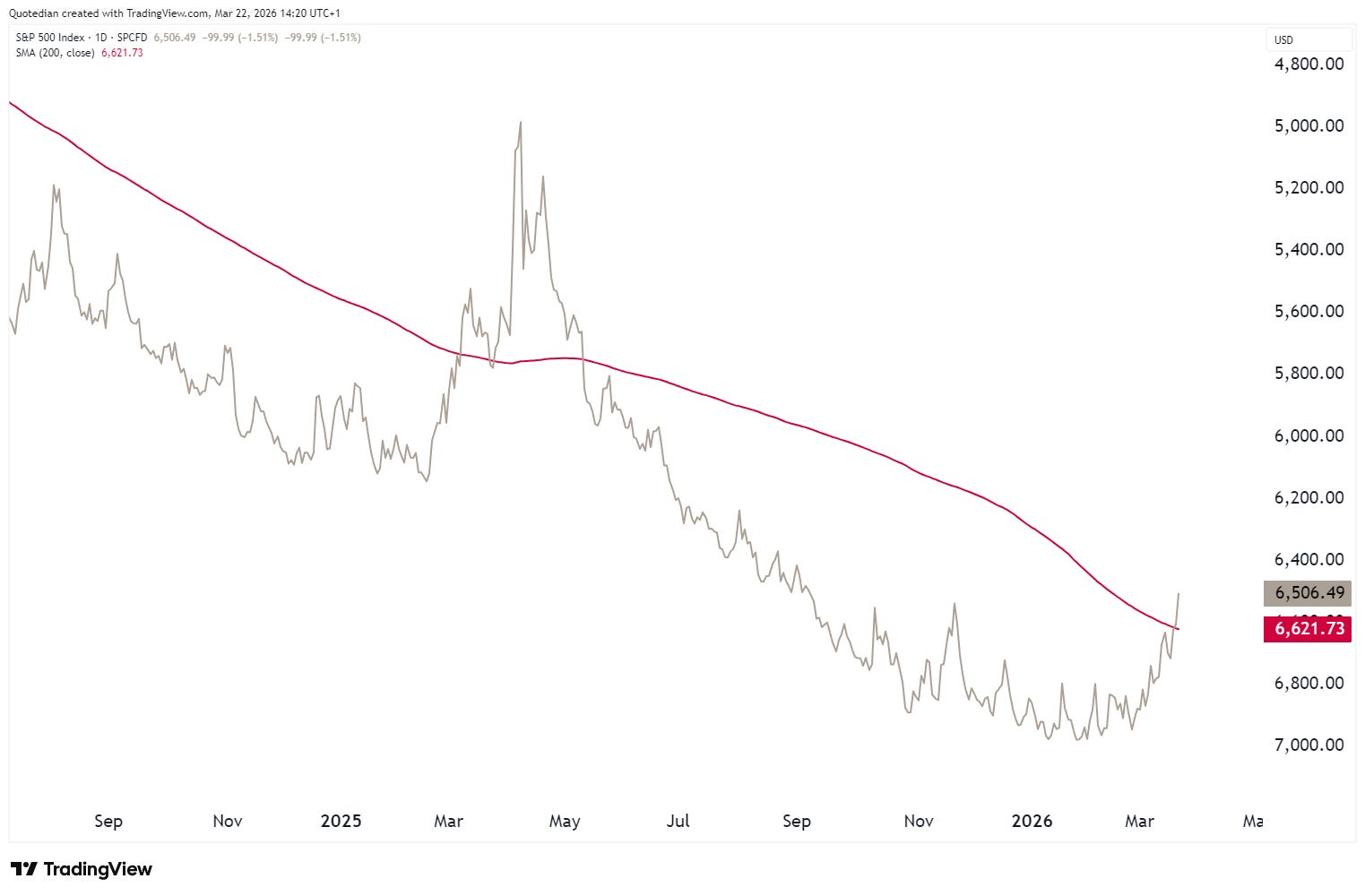

I would have loved to say that the S&P 500 has arrived at a critical point, but the truth is, with Friday’s sell-off, key support levels (plus the 200-day MA) have given way:

You could always argue that maybe we are seeing a major bear trap, magnified by the quadruple witching activity (Stock index futures, Stock index options, Single-stock options and Single-stock futures) on Friday,

but if in doubt … invert. Would you buy or sell this?

The Nasdaq is also trading below its 200-day moving average:

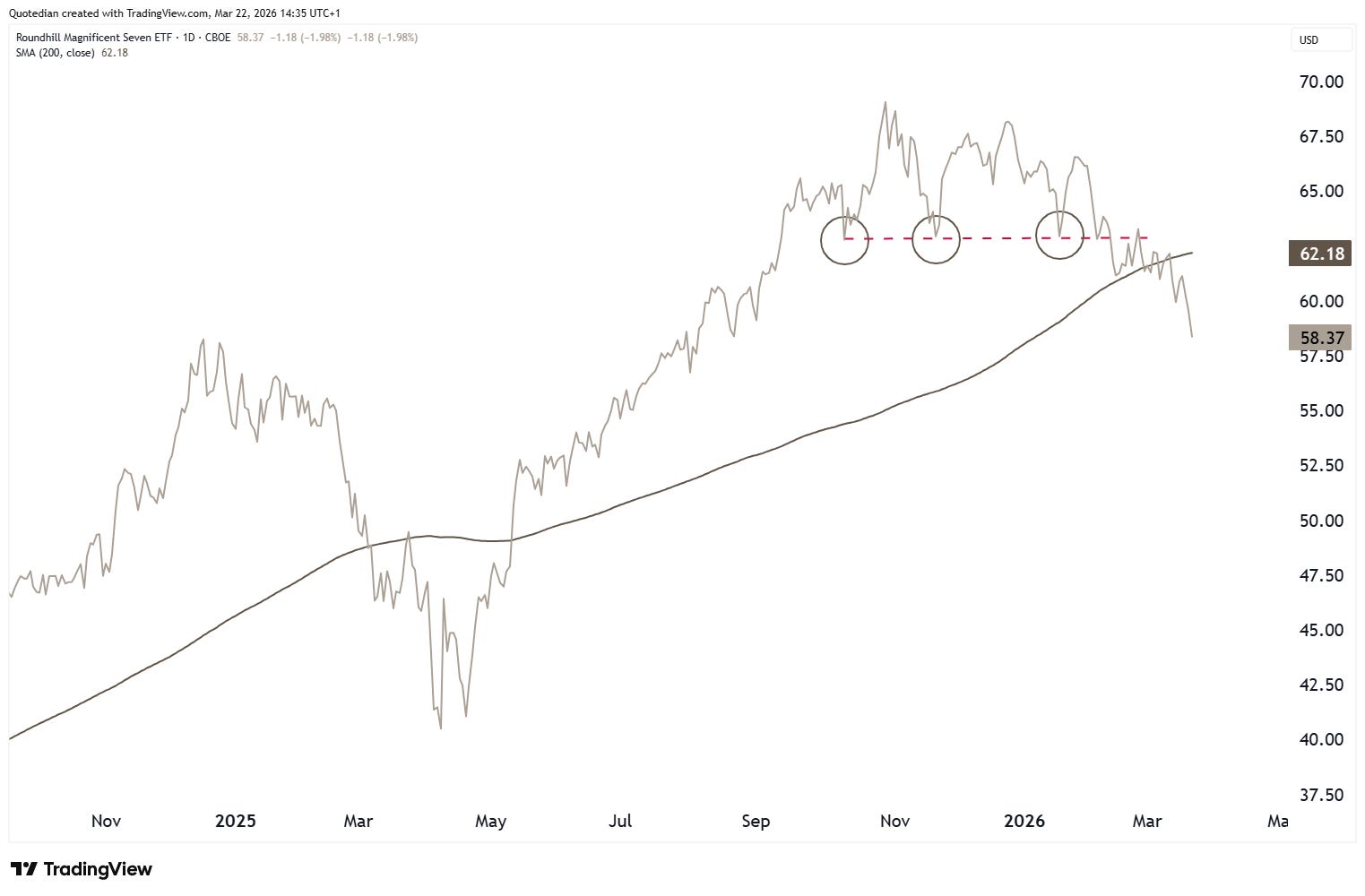

The Mag-7 stocks are not coming to the rescue, down over 15% now since the all-time highs back in October:

The small-cap focused Russell 2000 is still above its 200-day moving average,

which is somewhat surprising, because it is also the first main index in the US to enter correction territory (drawdown >10%):

European markets (SXXP - STOXX 600 Europe) are on the brink of a major breakdown, as much as in terms of the 200-day MA support, as entering ‘official’ correction territory simultaneously:

Will this level hold?

If Germany’s DAX is a leading indicator, all hope is lost:

In Asia, Japan’s Nikkei index is also about to violate an important key support zone, though all truth being told, it can (will?) drop another 10% and still trade above its 200-day MA:

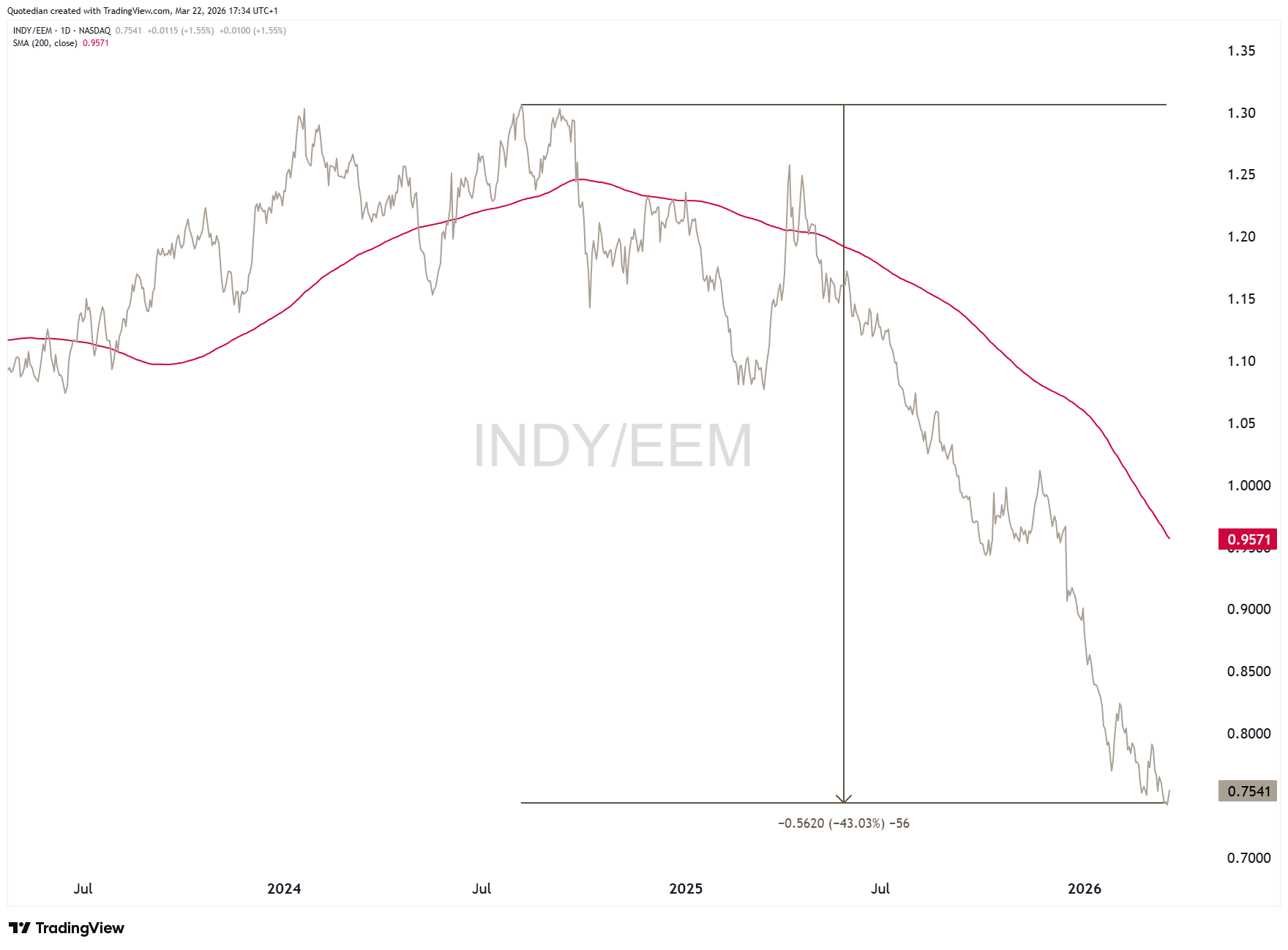

The Indian stock market, already in a “bear” markets since nearly two years, is suffering under the prospect of higher energy prices:

In relative terms, this market has underperformed overall emerging markets by over 40% since summer 2024:

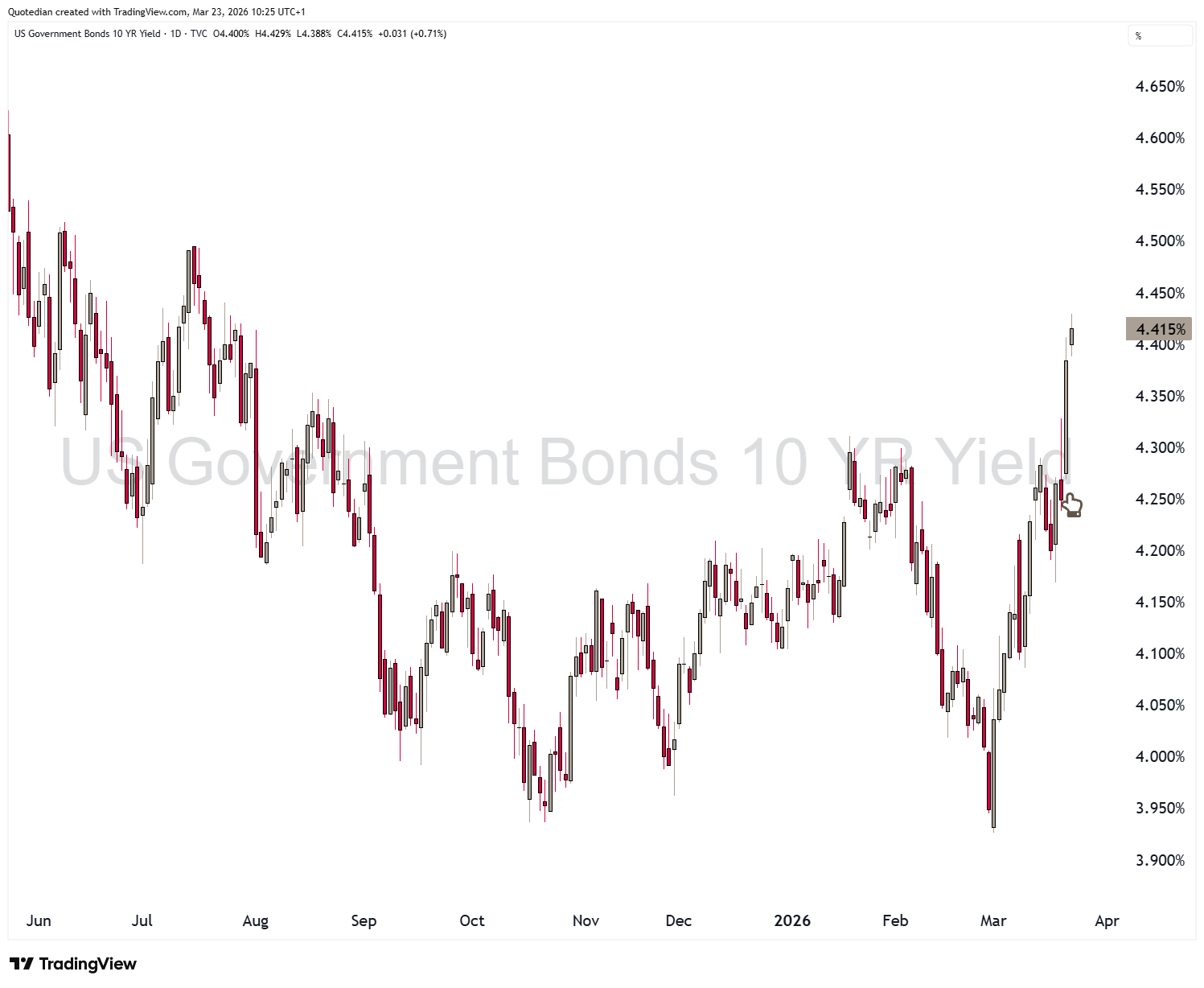

Moving over into the interest rate/fixed income space, developed treasury yields seem to have resumed their secular uptrend. Take the US 10-year for example:

That move higher on Friday was NOT orderly. Zooming out on the same instrument, we note that a first resistance (red dotted line) has been taken out and 4.60ish is now the level to watch:

Market-implied inflation expectations (breakevens) have been exploding higher:

However, the yield curve is flattening,

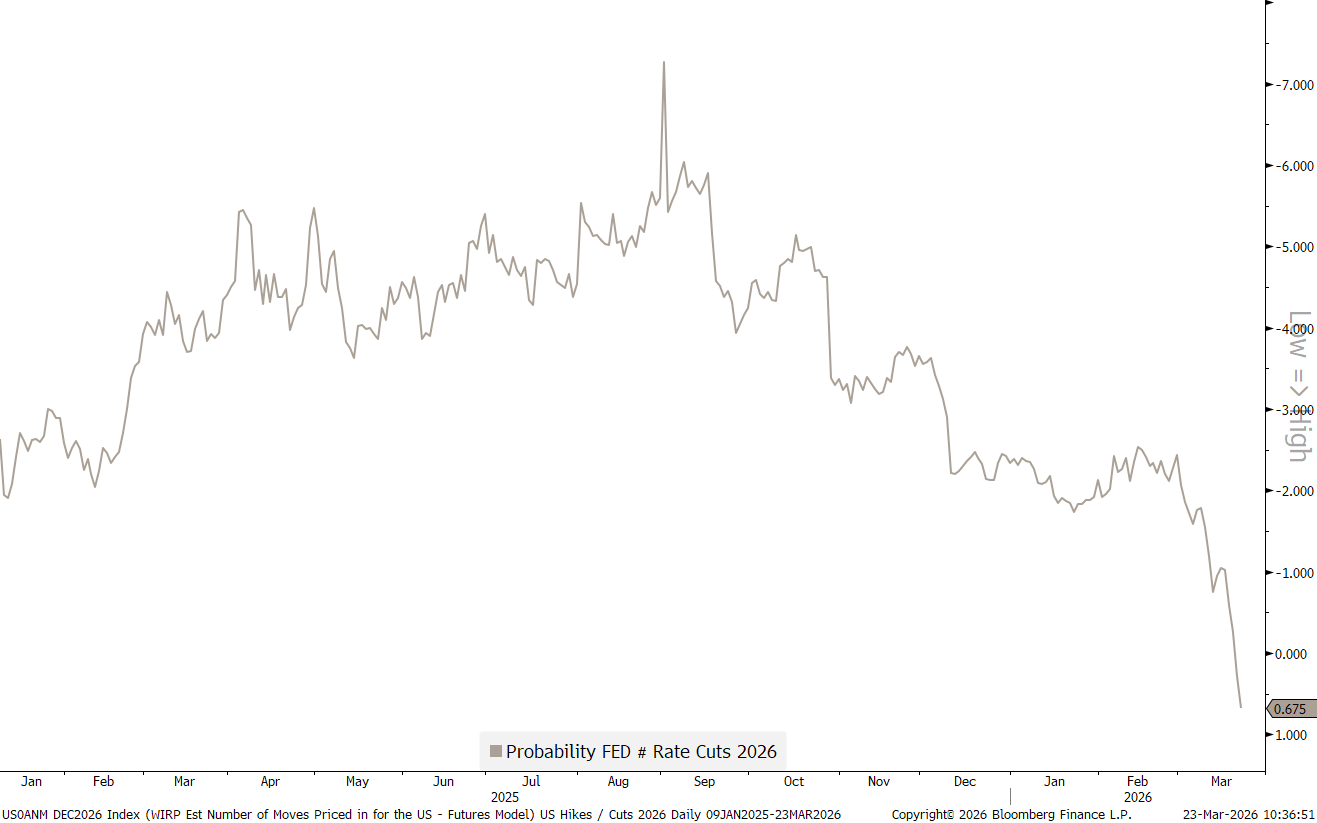

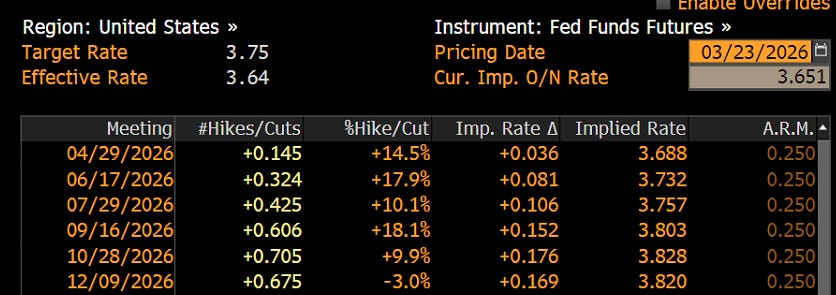

as the market is pricing out further FOMC rate cuts:

As a matter of fact, rate HIKES are now more likely according to futures markets:

European yields, below proxied via the German 10-year Bund, are also sky-rocketing in the face of increased energy costs:

Zooming out here again too, we have to take note that any reasonable resistance has been broken:

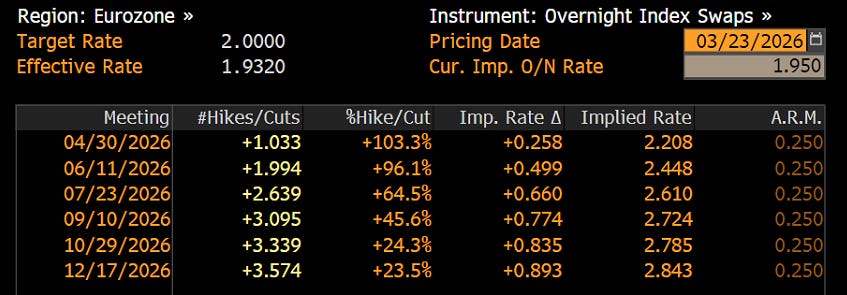

According to markets, the ECB will HIKE interest rates as early as April and at least three hikes are priced in into year-end:

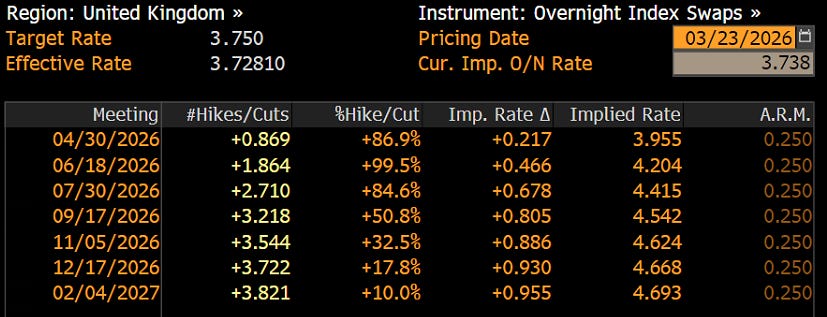

Similarly, any hopes for further rate cuts by the Bank of England have been buried:

The 10-year UK Gilt is at its highest since 2008!

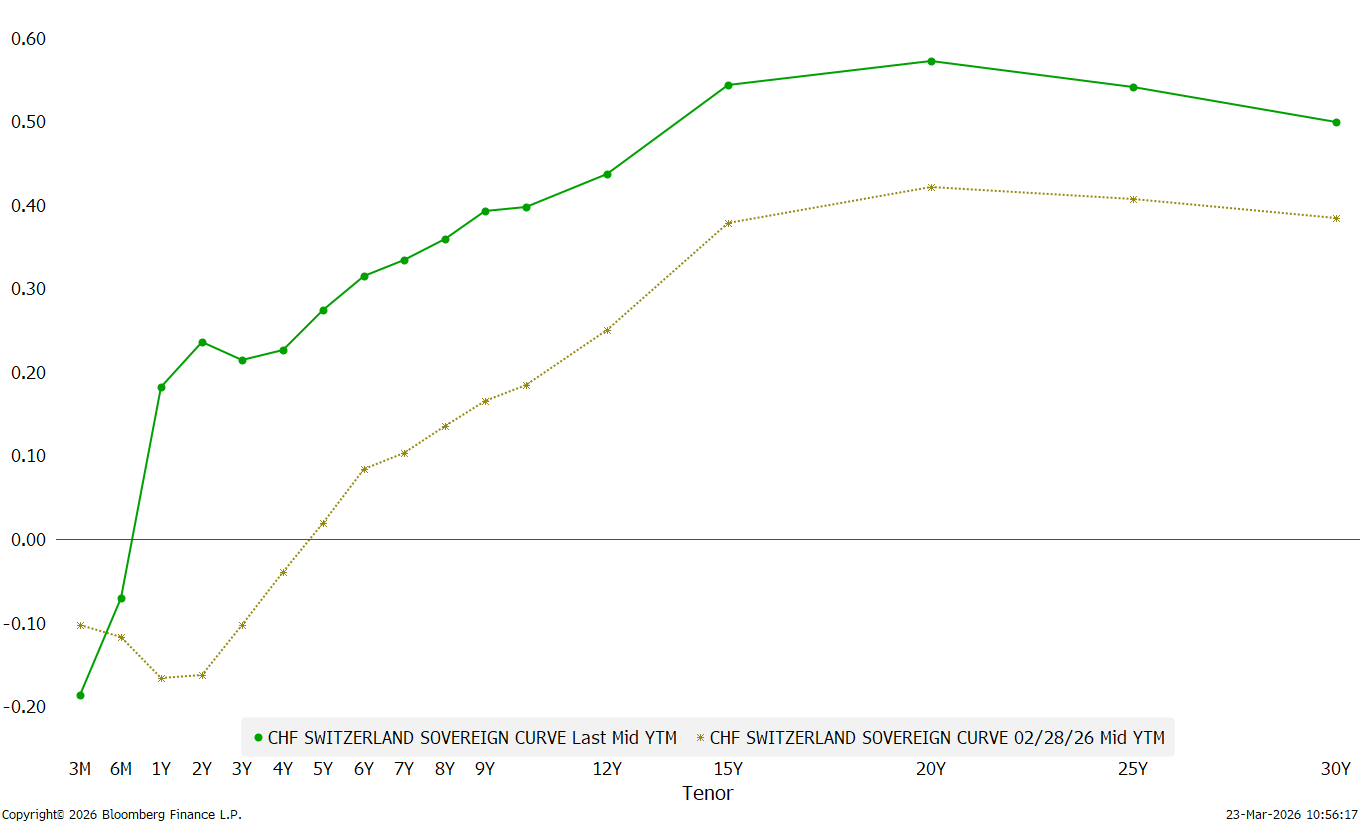

What a difference a war makes! The Swiss are suddenly ‘celebrating’ a positive yield curve starting at the 1-year maturity:

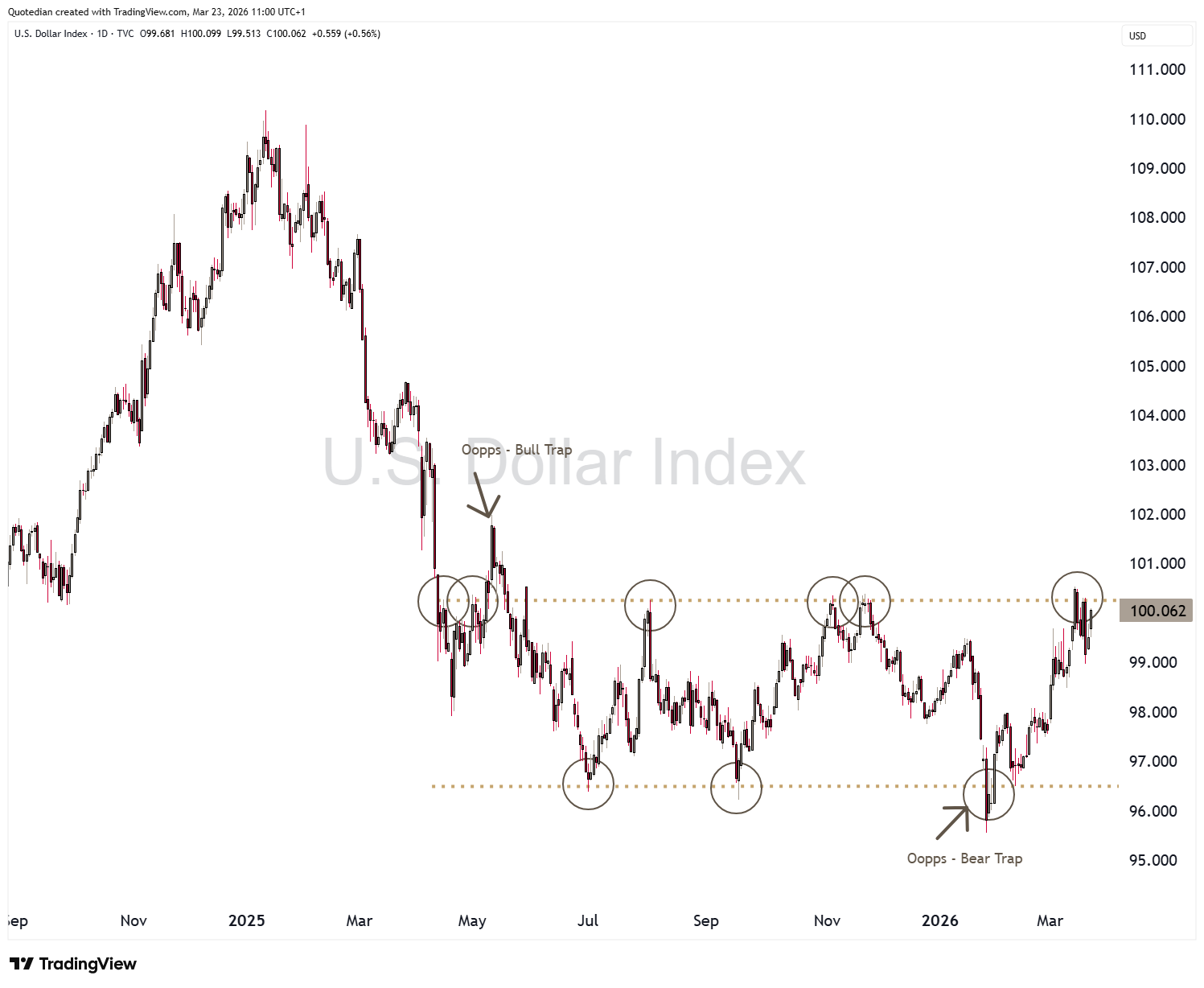

Turning to currency markets for a moment, the US Dollar is finally living up to its safe haven status during times of geopolitical crisis:

But given the ‘size’ of the Middle East conflict, the strength of the USD could be called benign and may be hinting to future weakness to come for the greenback:

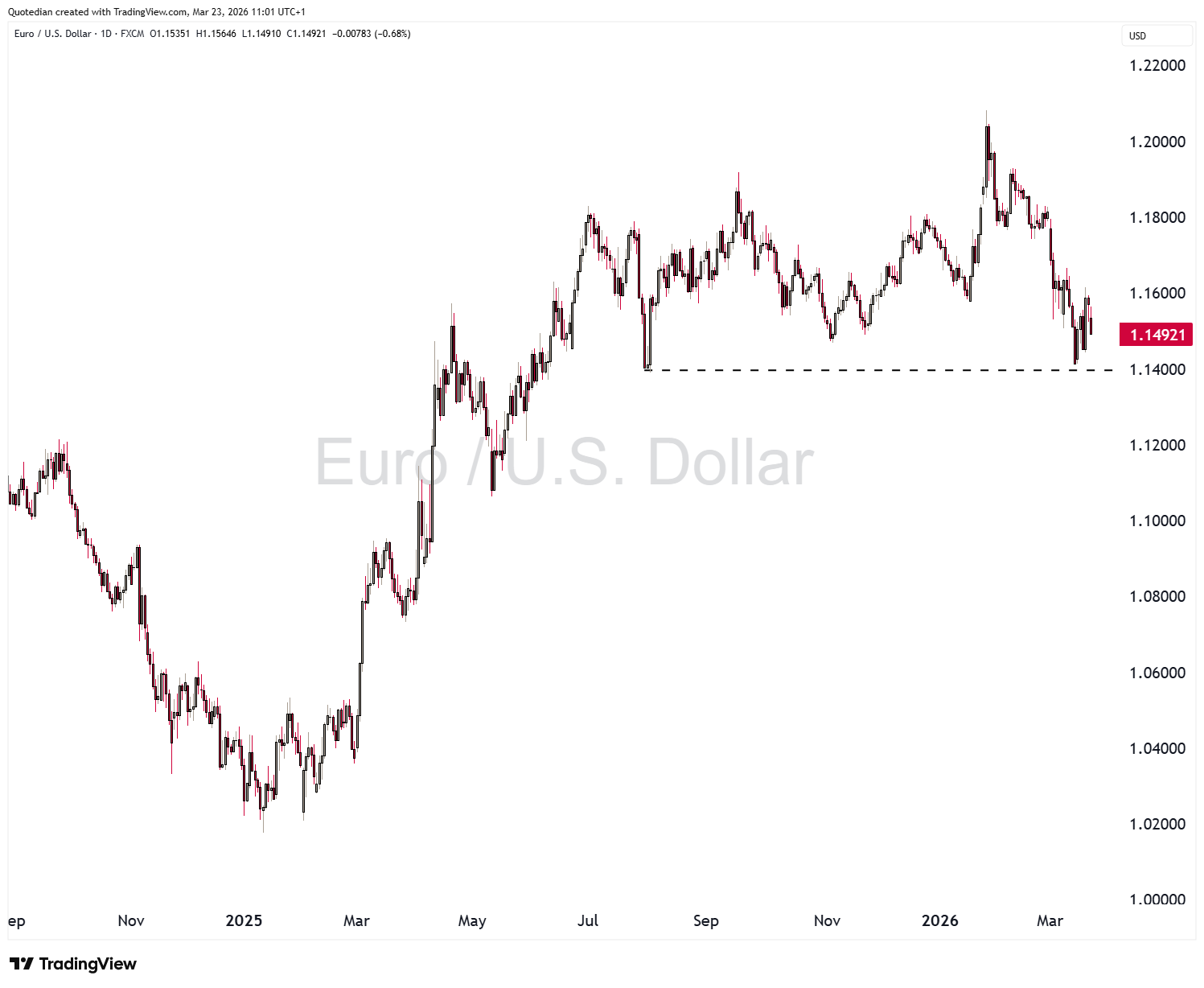

The key level to watch on the EUR/USD cross is 1.1400:

The same level to watch on the USD/JPY pair is 160.00 - not least as this is where the BoJ/MoF intervened the last time:

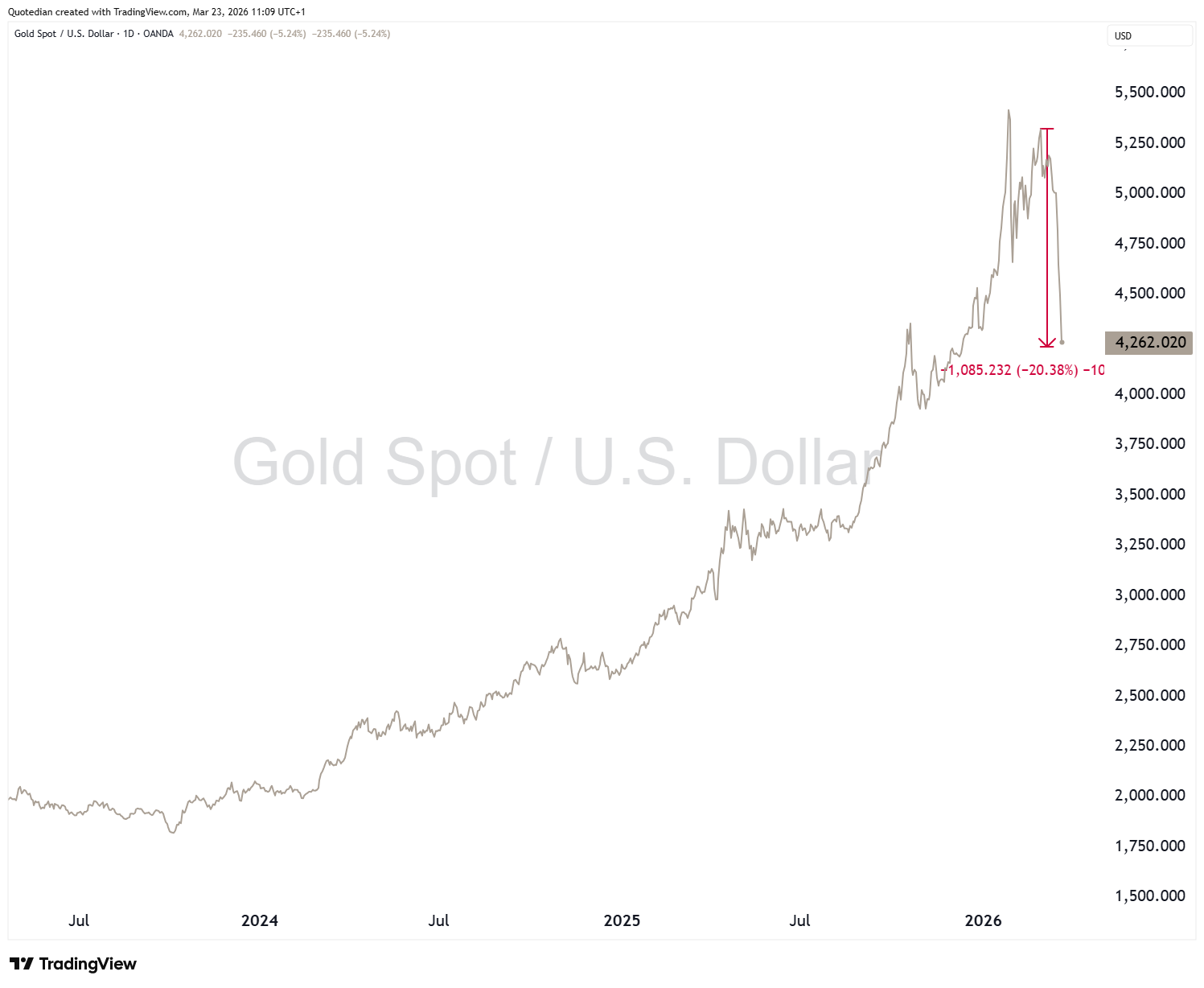

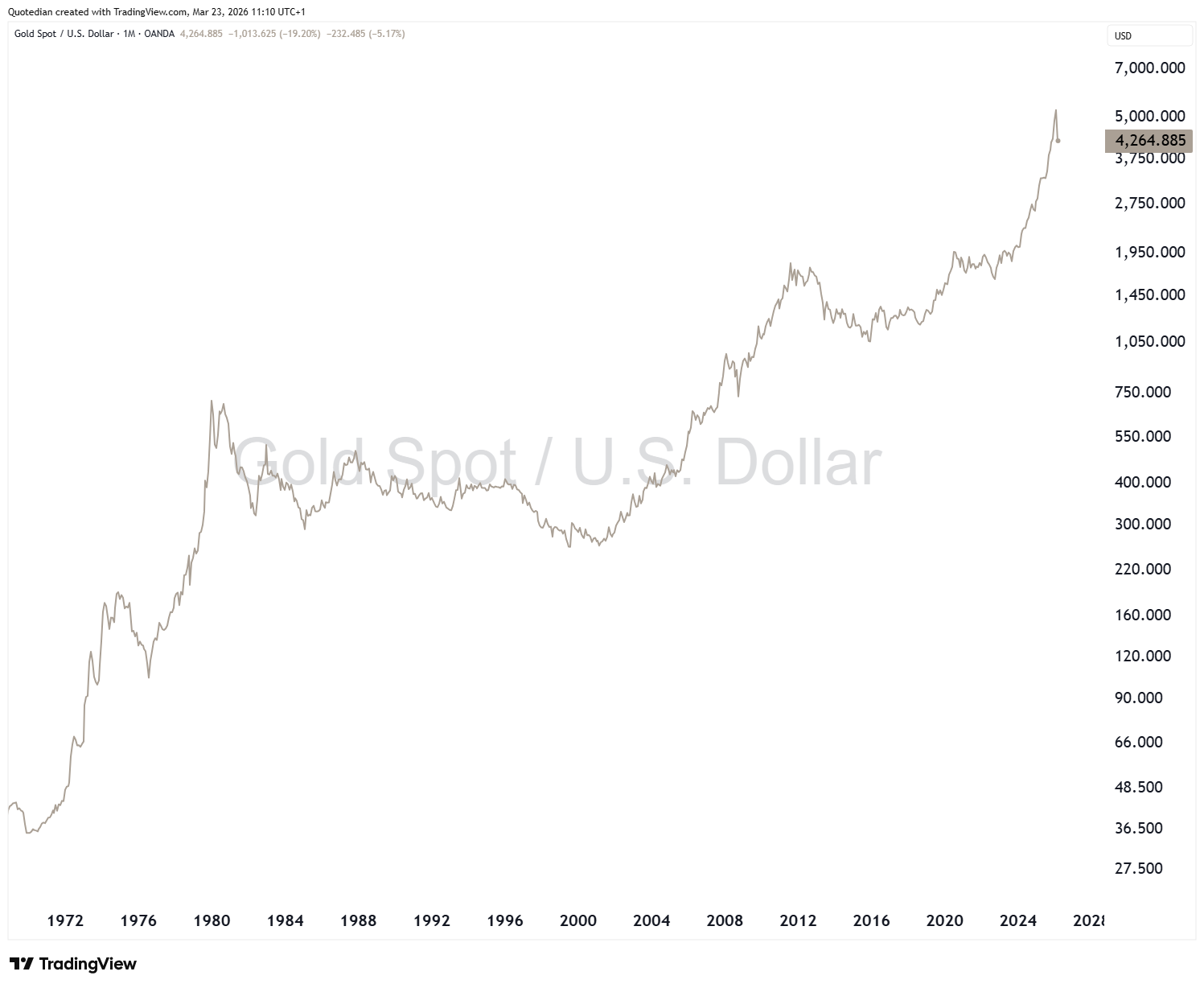

Finally, we need to address the question why GOLD IS MELTING DOWN …

Here’s the dramatic chart:

And here’s the same dramatic chart again:

Exactly!

What we need to remember here is that in times of dire straits (no pun intended), investors will sell what they easily can sell - and this includes Gold and other non-interest bearing investments…

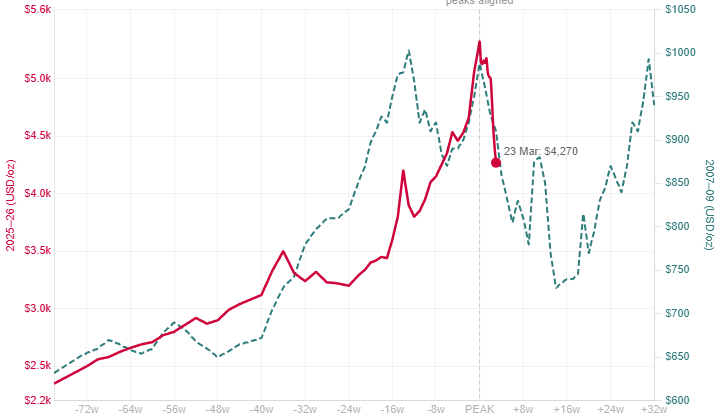

Take the GFC for example back in 2007-2009 …. gold suddenly sold off 25% as the extent of the crisis before than rising 160%-plus into the 2011 at around $1,900. Here’s a chart overlaying that price behavior now and then:

Hence, Gold will eventually stop falling and recover, but the risk of a multi-year consolidation period has risen.

However, the rally in Silver is over, something we timely called for after the price hit $120. A drop to USD45 minimum is likely:

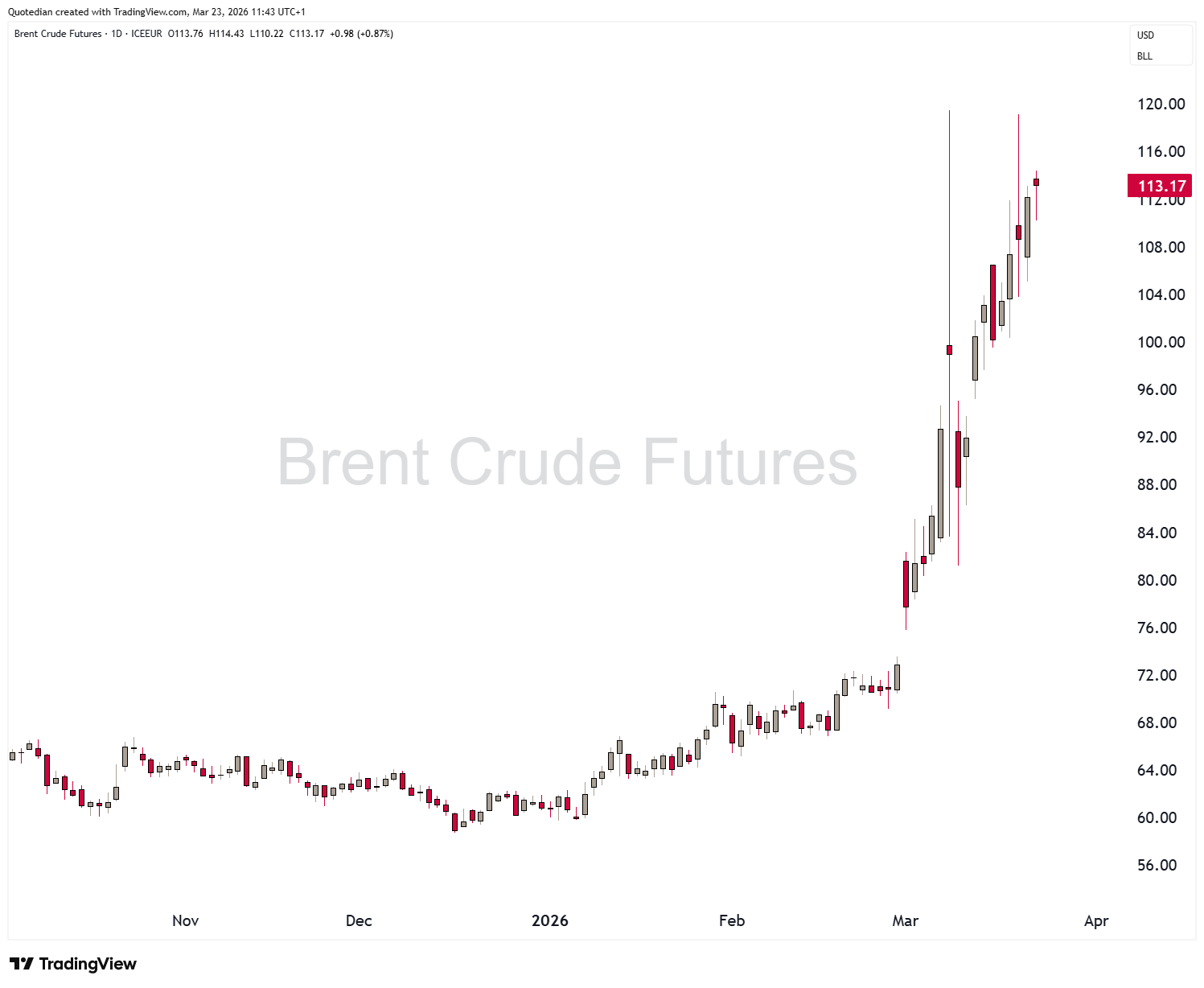

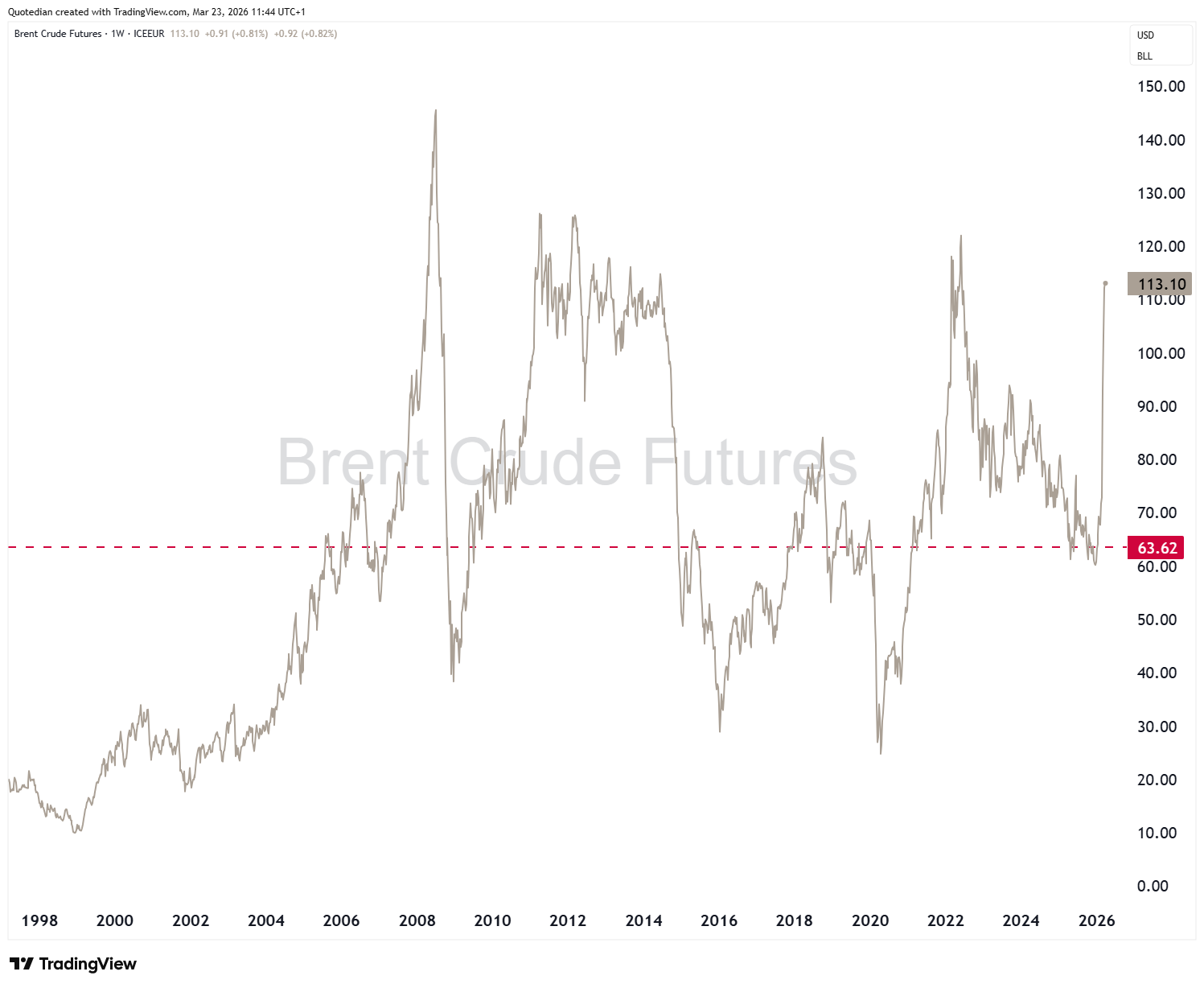

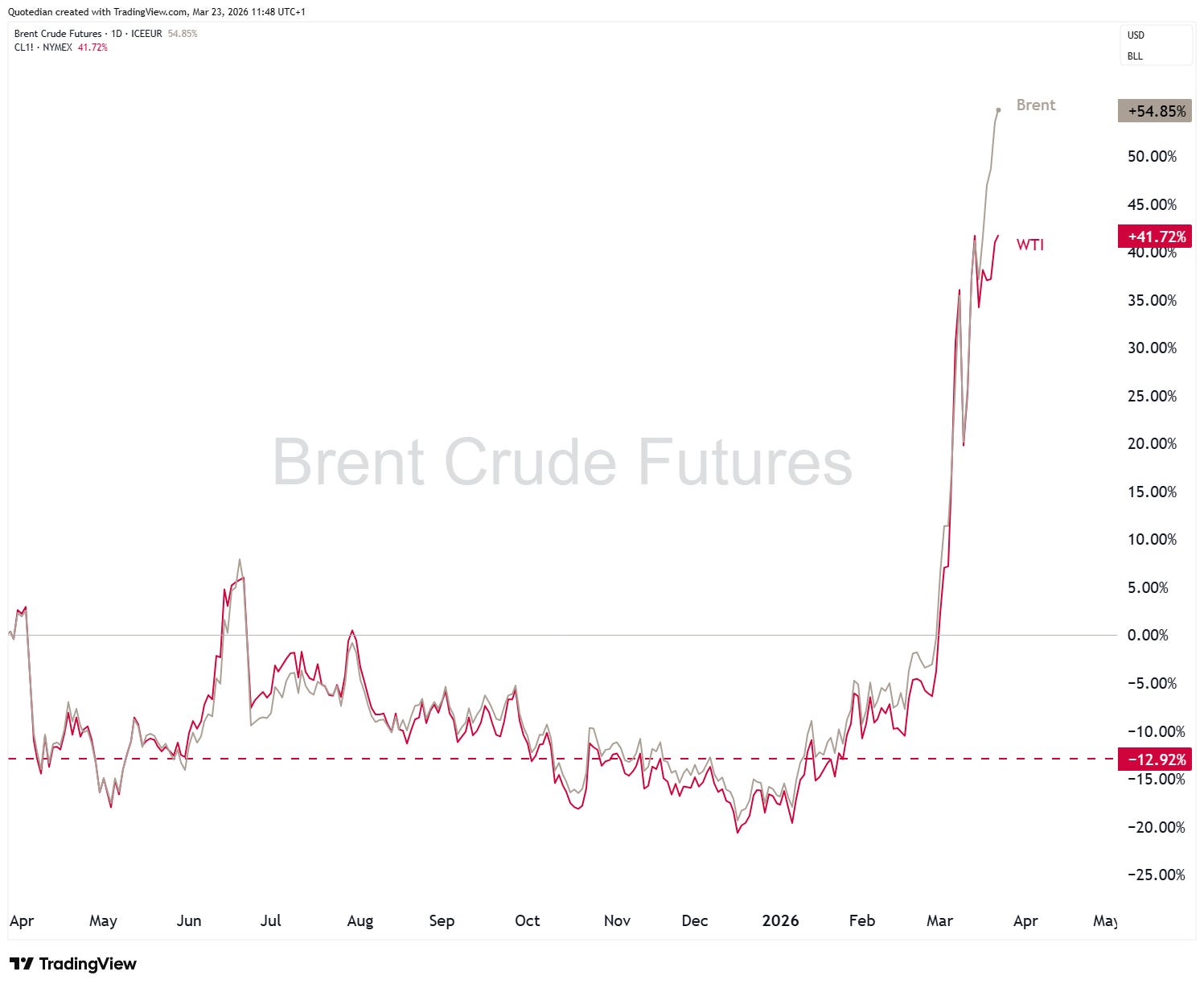

Crude Oil (Brent) is defying gravity and negating previous experiences of short-lived price spikes:

Will we see USD150 (or more) again?

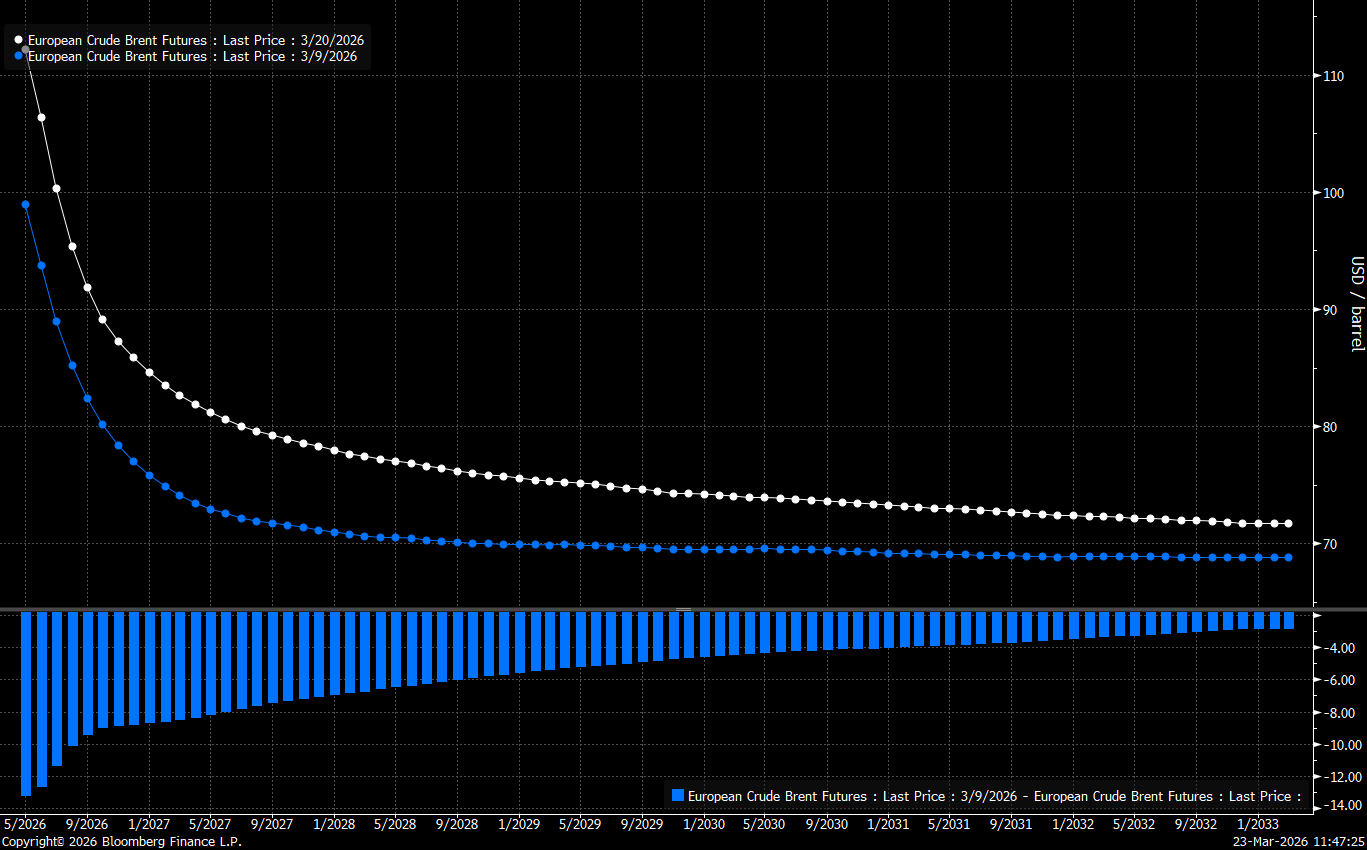

The backwardation has diminished as market participants expect a longer war now:

WTI continues to trade at a discount to Brent:

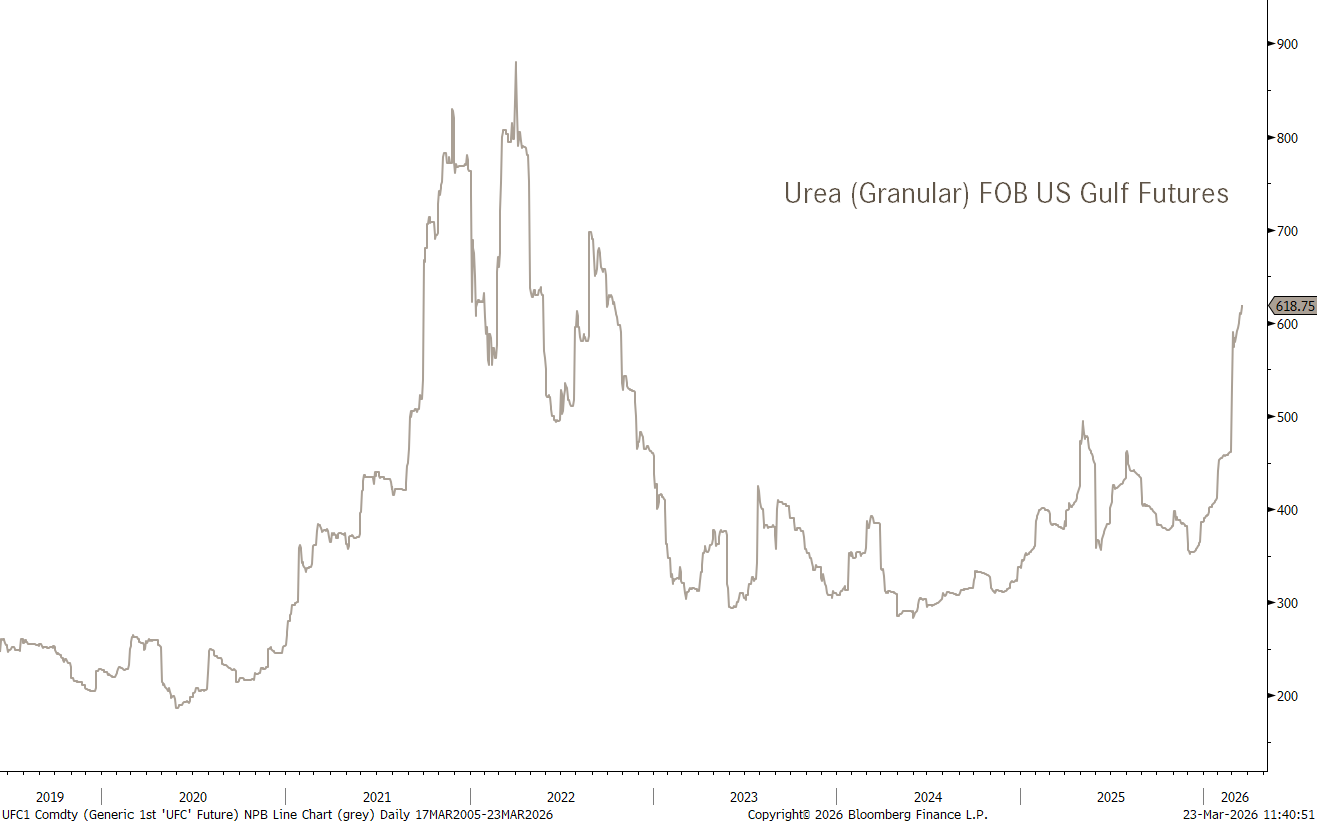

And finally, to come full circle, fertilizer prices are sharply higher as we discussed at the outset, but have potential to rising further into the 2021/22 highs:

As everyone and his mother said a few weeks ago, fade geopolitical events (aka BTFD) as nothing ever happens, and it is always a great buying opportunity. I warned you of that groupthink in our weekly Quotedian on March 2nd (click here).

And so here we are … markets may still turn on pin’s head and head higher the rest of the year, but any purchase intents should be executed only with clear stop-loss plans.

Most of the time, (equity) markets go up and any bad news is good news. During the painful bear markets (2000-2002, 2007-2009) any news is simply bad news.

The odds for more downside have increased.

May the Trend be with You!

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Investing real money can be costly; don’t do stupid shit

Leave politics at the door—markets don’t care.

Past performance is hopefully no indication of future performance

The views expressed in this document may differ from the views published by NPB Neue Privat Bank AG