PLAY

The Quotedian - Vol VI, Issue 42 | Powered by NPB Neue Privat Bank AG

“Those are my principles, and if you don't like them... well, I have others.”

— Groucho Marx

HOUSEKEEPING

When I called the last Quotedian nearly a week ago “PAUSE” I was actually referring to the Fed’s hiking policy, but it also turned out to be a PAUSE for the Quotedian. A pause I used to rethink the format and especially frequency of this fine newsletter …

Hence, I have taken the decision to go back to the pre-April 2022 format of a daily Quotedian - after all the publication’s name has a hint of daily in it. The format is one of shorter but daily mails, with all the market insight and wit we grew to love. The chart of the day (COTD) will hopefully live up to its name again…

I would only ask you to give your feedback where requested (e.g. Dashboard section right below), either by hitting the Comment button or sending me an email directly.

Last but not least, as is valid for all my decisions, I may reverse them sooner than you can finish reading this sentence…

So, we push that “PLAY” button again!

DASHBOARD

Ok, here’s the first feedback request. Is this Dashboard useful? Too much data (e.g. should we take out sector performance)? Too little data (e.g. should we add factor performance)? Wrong data ? Share your feedback:

AGENDA

CROSS-ASSET DELIBERATIONS

And what a day to choose to start writing on a more regular basis again, with volume well below the 100-day average on the SPX as I start writing this at about an hour before US market close:

During the early session it seemed that US investors who had forgotten to sell during Friday’s afternoon session came back to the office after the long weekend to finish the job, however, bargain hunters stepped in already after one of trading, reversing most of the day’s losses. Then, nothingness during the entire PM session (shaded area):

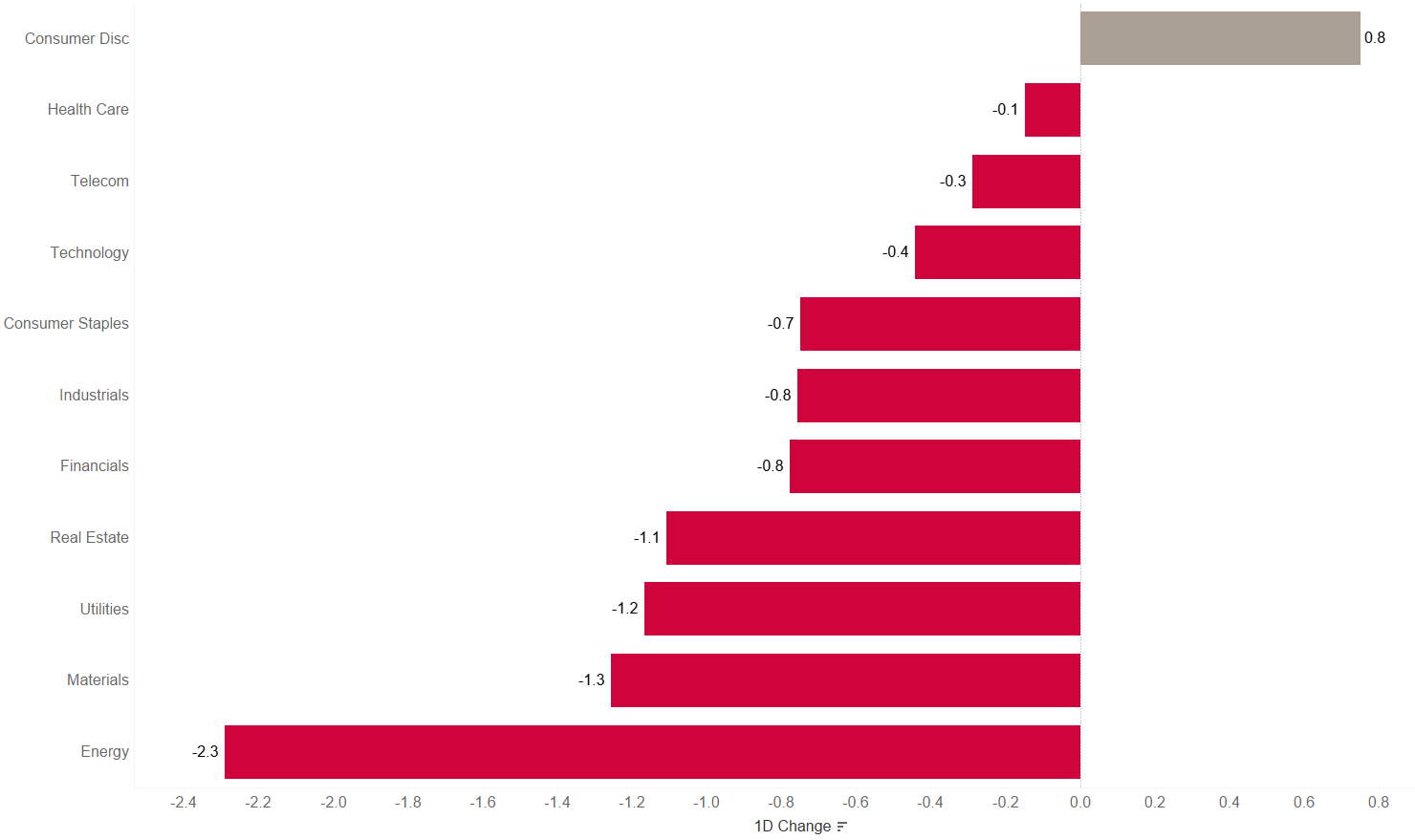

Let’s have a look under the if there was anything to be had in sector performance deviation. Here is the US sector performance:

Well, at least an over three percent spread between best and worst, but overall the tone was a negative one. A quick glance at the market heat map reveals that it was probably Tesla alone pushing consumer discretionaries into positive territory, whilst NVIDIA probably helped a lot the technology sector performance:

The heat map further reveals that the loser to winners was quite brutal (brutal = 4:1). Regarding this advance/decline ratio we actually have an interesting observation to make in today’s COTD section further down.

Asian stocks overnight are largely lower, with the biggest drawdowns registered in the Chinese complex (Mainland, HK), but also some notable ‘green’ exceptions such as India and Japan.

European futures point to a very mixed start amongst the various regional indices, leading probably to a flattish Pan-European opening.

The good old Quotedian, now powered by Neue Privat Bank AG

NPB Neue Privat Bank AG is a reliable partner for all aspects of asset management and investment advice, be it in our dealings with discerning private clients, independent asset managers or institutional investors.

Turning to fixed-income markets, in many aspects the “action” was more interesting in bonds. The US 10-year treasury bond yield dropped 10 basis points on Tuesday, not a bad move for just one session.

But probably more interesting was that this drop in yields, observable along the entire maturity spectrum though a bit less pronounced at the short-end, failed to ignite a significant rally in stocks.

Yield curves continue to invert, with the 10 minus 2 year version about the celebrate its one year anniversary of inversion! Remember, (US) recession in the past have taken place anytime between 3 and 18 months after curve inversion, quite frankly rendering it a pretty useless timing tool (as the current experience would confirm).

In the currency arena, the US Dollar strengthened versus most other major currencies over the past 24 hours,

however, this for now continues to seemingly be only a short countertrend rally within the larger downtrend, as the chart of the US Dollar index (DXY) would attest:

Finally, in the commodity segment, and forgive me to throw cryptocurrencies into this basket today, Bitcoin is having a small but steep renaissance after having been beleaguered over the past two months or so:

Ok, time to hit the send button, but just before that, again, according to Substack today’s letter is about a 4 minute read and this is my objective with this letter: A quick, macro-focused market round up of the session gone by on a (nearly) daily basis:

And again, feel free to leave your comments here:

CHART OF THE DAY

The chart below shows the S&P 500 in the upper clip and its cumulative advance-decline line in the lower clip. In short, the recent rally in stocks was often criticised for being “narrow”, i.e. few participating stocks. However, as the red line below shows, participation has been growing and a break-out to new highs seems imminent.

Stay tuned …

Thanks for reading The Quotedian! Subscribe for free to receive new posts the moment they are published.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance

Good morning all.

Andre don't touch the Dashboard... :)

Thanks Andre for sharing! It’s great to know that Quotedian comes back on a quotedian basis🫶😅