Scam Bankrupt-Fraud

Volume V, Issue 185

"I would like to start by formally stating under oath: I f*cked up"

— SBF’s prepared remarks to Congress before he got arrested shortly before his testimony

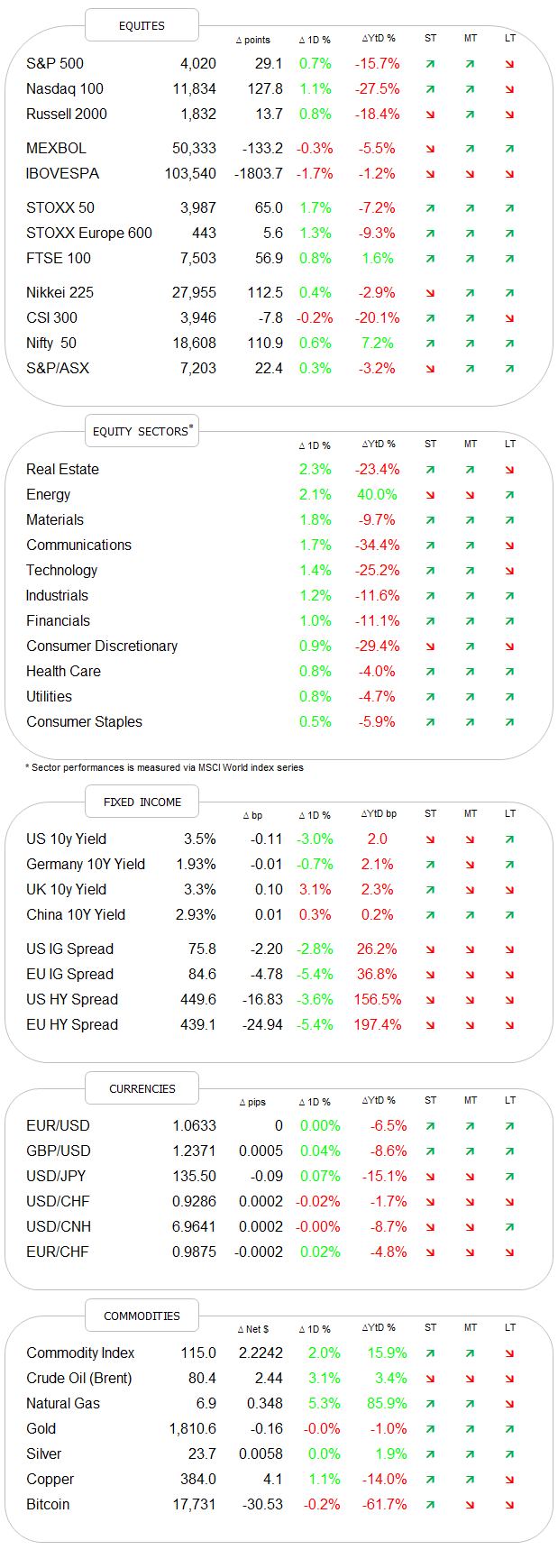

DASHBOARD

AGENDA

CROSS-ASSET DELIBERATIONS

Ok, I am tired of him too and I promise that today will be the last mention of him (transitory promise). But reading the new meaning of his initials was too good to not use it as a Quotedian title!

On to more serious matters …

On any given day, a one percent plus up move on the Nasdaq would be reason to celebrate for long equity investors. But somehow did yesterday’s gain leave a stale taste in many mouths, given the early potential seen for a 5% day:

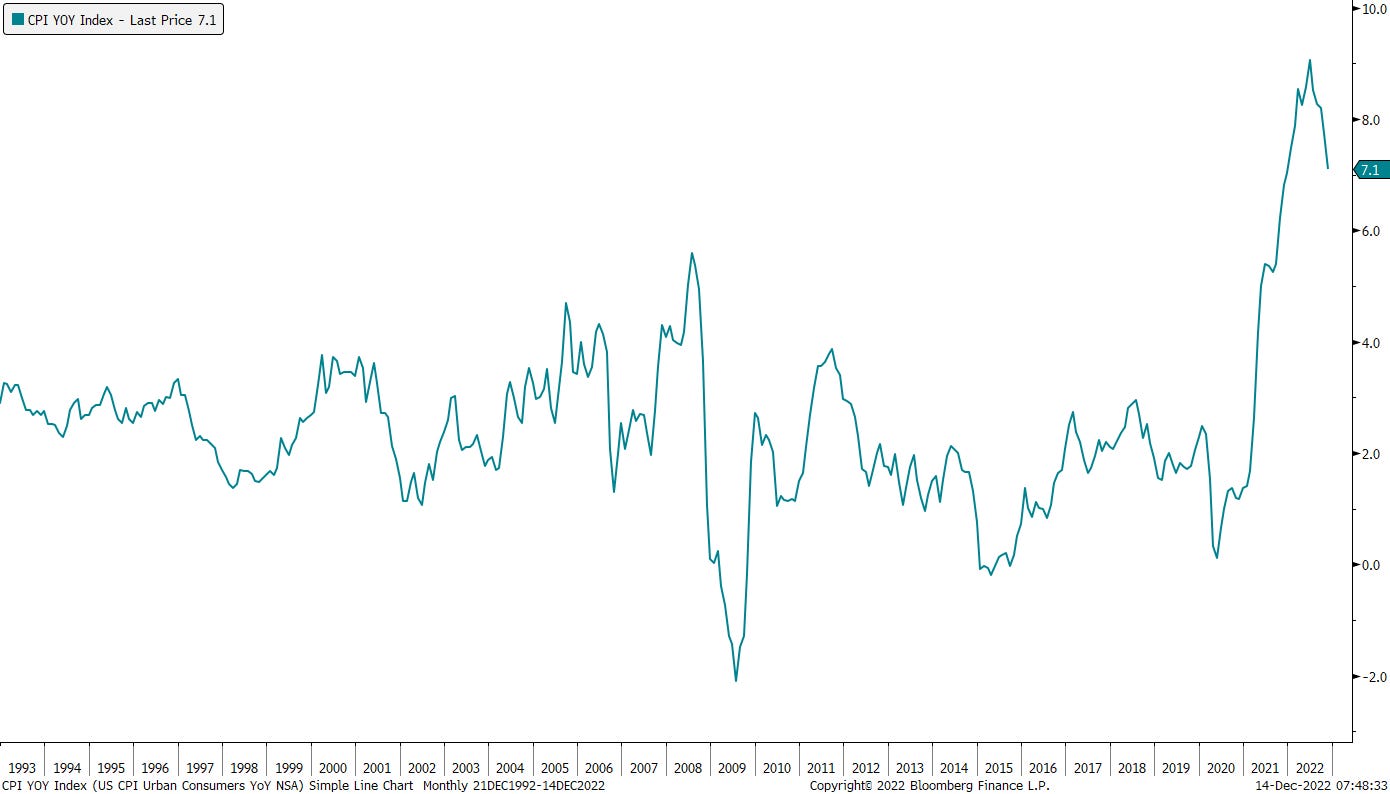

Nevertheless, still a good outcome, given the minuscule improvement in the CPI (0.2% lower than expected), but as we know, it’s not about the magnitude but about the delta (or ROC). Whilst the headline number shows a further decline in year-on-year inflation

we are still at 30-year highs and some segments (e.g. service) still showed higher month-on-month readings.

It is therefore very likely that the Fed will sound more hawkish than dovish during/after this afternoon’s 50 basis point hike.

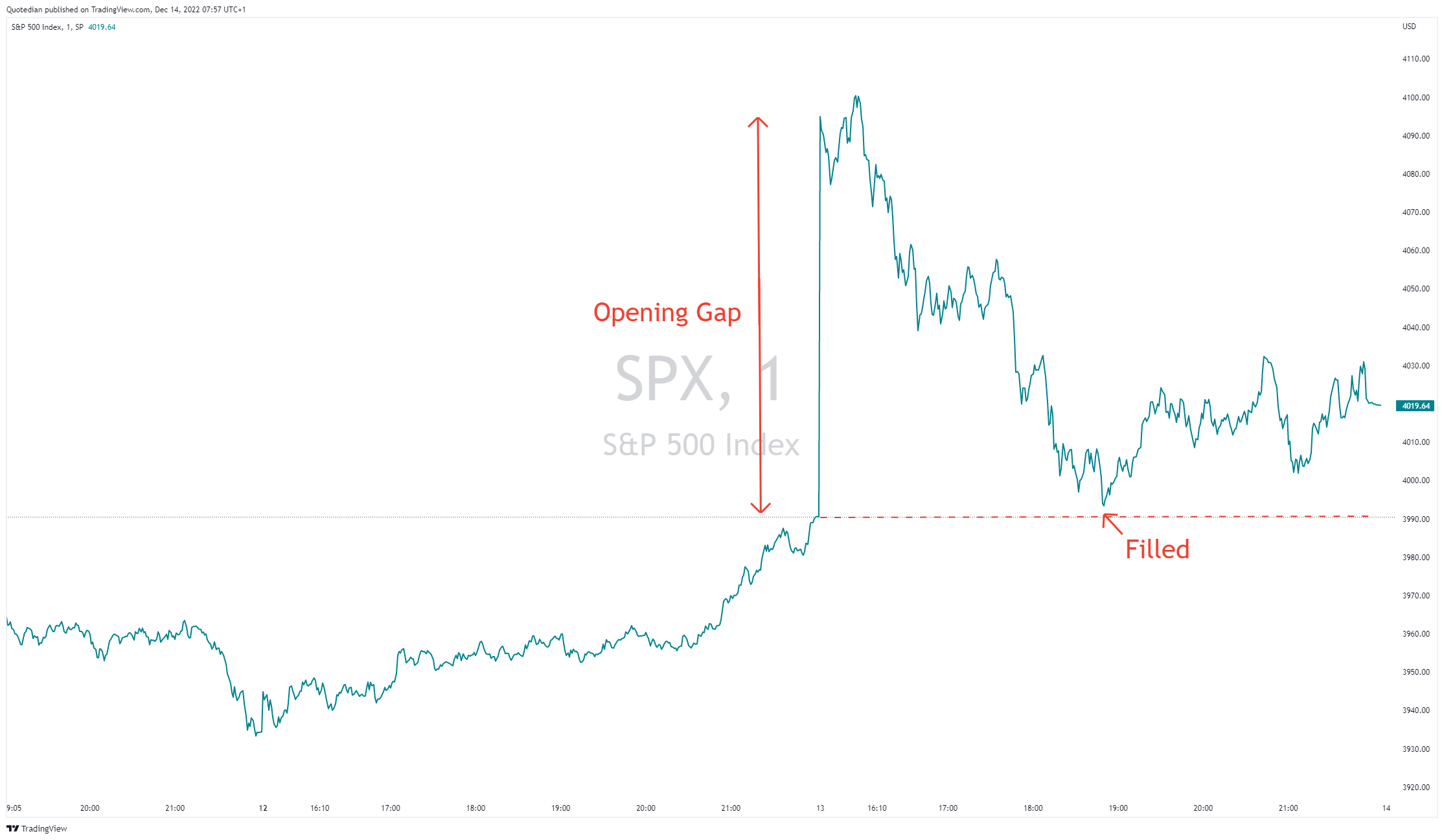

The ‘good’ thing about such fast moving markets is that chart patterns, such as the opening gap on the S&P 500 yesterday, get concluded very quickly:

Overall, participation in yesterday’s rally was not bad, seeing one of the highest volumes in over a month and an advance-decline ratio of roughly 2:1. Only one sector closed down on the day (consumer staples):

On the market heatmap, the sore thumb from yesterday repeats itself:

On the daily chart, the S&P 500 continues to ‘respect’ the cyclical downtrend, having yesterday only briefly broken both, the downward sloping tendline AND the 200-day MA, but closing below both by the end of the session:

The European chart (SXXP) continues to be more constructive, but a firm closing above 444 is also necessary here to confirm resumption of the uptrend:

One market segment I am a bit disappointed about on the equity side is emerging markets (EEM), where I expected more upside given the US Dollar (UUP, inverted) weakness:

EMs (EEM) also failed to break out versus the S&P 500 (SPY):

This early Wednesday, Asian markets are roughly copying Wall Street’s template in terms of direction and magnitude. European and US index futures are flat to shily positive as I type.

Bond yields got hammered upon the release of the CPI numbers and only recovered lightly from the intraday lows reached:

That’s a 20 basis points intraday drop there on the 10-year US yield chart above and that’s massive.

2-year yields dropped even more, provoking a curve steepening,

however, this was not the case on the 10y-3m curve measure:

On the daily chart, the Tens are holding just above uptrend support line:

Credit spreads (high yield shown below) are continuing to contract and seem to be ignoring the most signalled recession ever of next year:

In currency markets it will come to no surprise that the US Dollar saw broad weakness against other major currencies yesterday:

On the US Dollar Index (DXY) chart itself, the TA law of polarity dictates that the previous support zone (grey-shaded) should now be observed as possible area of resistance:

The Euro-hatters are having a difficult month:

Also noteworthy, the inverse panic on Euro volatility (EVZ):

Even the Dollar-Yen cross is challenging its 200-day moving average again (green circled):

Has the SBF arrest yesterday finally ‘liberated’ Bitcoin? 18,000 is suddenly on the radar:

Finally, yesterday’s drop in the US Dollar and push lower in real yields helped Gold rally above the $1,800 handle:

If the yellow metal can hold above this key level, $1,900 should be on the books soon. Silver thinks that is possible:

Time to review the miners once again? Maybe. But definitely, time to hit the SEND button.

Have a great Wednesday, the next football game is only a few hours away.

André

CHART OF THE DAY

This chart from the great Jim Bianco, eponym at Bianco Research, never ceases to surprise me. Or maybe it should not surprise me. Like Pavlov’s dogs, strategists always return to forcasting two percent as future level of inflation:

Like a broken watch, they will be right twice a day.

However, in my books and bedrock scenario, that point may be still quite far away, as in decade(s).

Stay tuned …

Thanks for reading The Quotedian! Subscribe for free to receive new posts and support my work.

DISCLAIMER

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

Past performance is hopefully no indication of future performance