Superforecasters

The Quotedian - Vol VI, Issue 87 | Powered by NPB Neue Privat Bank AG

“It is difficult to make predictions, especially about the future."

Niels Bohr or Yogi Berra or both

FOMC today

ECB, BoE & SNB tomorrow

BoJ next week

That’s about all you need to know of the remaining agenda for the year …

It is this time of the year, where we

get too fat

spend too much money

and receive far too money predictions of what’s gonna happen on financial markets in the coming year

All these publications are of course of incalculable value, but especially regarding equity forecasting, let me provide you with a synopsis of all forecasts (without having read one):

“… regarding equities, we are cautiously optimistic …”

So, as today’s title, leitmotif and short introduction would give away, today is all about predictions.

But don’t worry - it is not about my predictions … it is about yours!

Want to know all about the future? Buy a crystal ball … Want sound investment advices? Contact us!

Contact us at ahuwiler@npb-bank.ch

We will run through a series of survey questions today and I thank you in advance for your active participation! After all, “THE MORE, THE MERRIER!”

As this is probably the second last Quotedian of the year …

… I will publish the poll results either next week or in the first week of January - it will be fun, for sure!

For those who cannot vote on their PCs due to firewalls or whatever, I have got two plans:

Plan A - Use your iPad/iPhone

Plan B - Send me your votes manually (ahuwiler@npb-bank.ch). I have numbered the questions for easier reference

With that out of the way, get your pollster pen (finger) ready and let’s dive right in…

By the way, all charts are year-to-date today, i.e. the show what happened to the asset under observation in 2023.

Starting with the S&P 500, we notice that it was a much better than most of us expected as we were finishing 2022 on a very sour note:

So, here’s our first poll:

Continuing with the Nasdaq, we are still in suspense if this index will be able to provide a 50%-performance year (hint: yes):

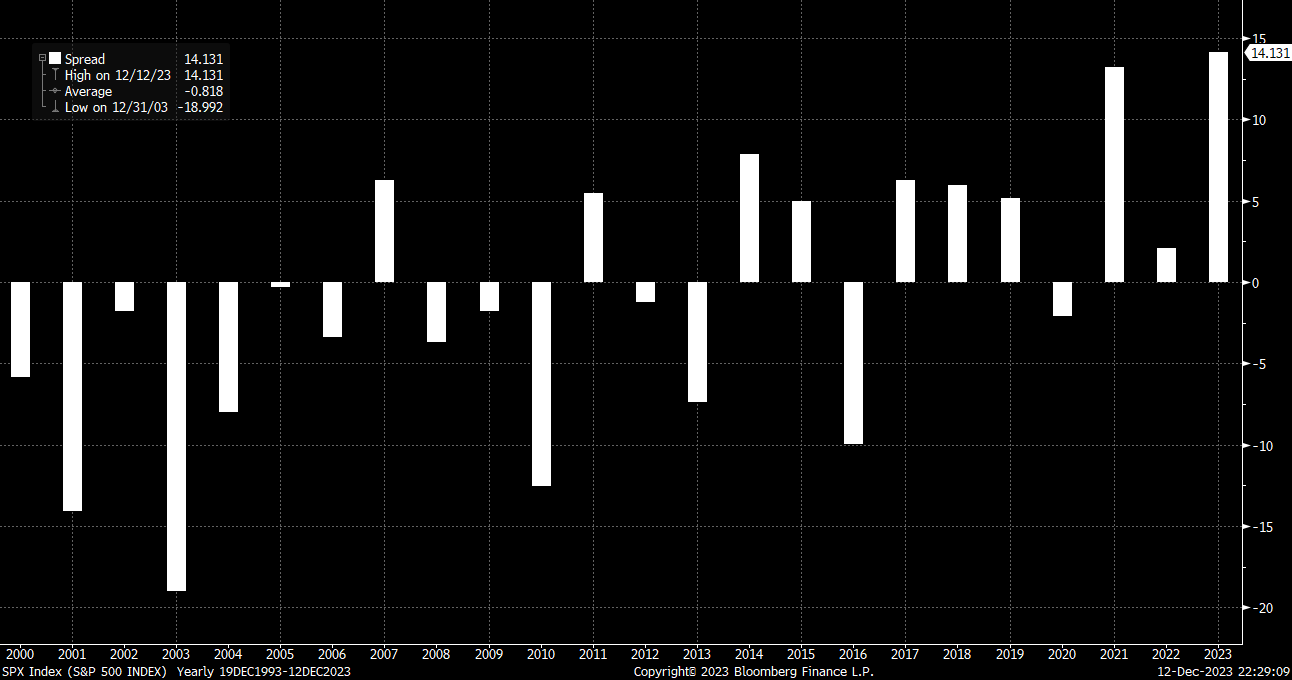

Small Cap stock in the US are prone to deliver their third consecutive year of underperformance, as this chart showing the yearly performance spread between SPX and RTY demonstrates:

Right over to European equities, where the STOXX 600 Europe index leaves us the following impression for the year just wrapping up:

Up a respectable 11% YTD, this index is still lagging the 20% of its US-cousin (SPX).

The chronic underperformance of European stocks versus US peers (it’s xmas time, let’s sound positive) The brilliant outperformance of US stocks versus their US peers has now been nearly uninterrupted for two decades as this longer term of the ratio SXXP/SPX shows:

Similarly, or maybe even related, to the European underperformance, value stocks have gravely underperformed US stocks. Here’s an MSCI World version of the Value versus Growth chart over the past two decades:

Let’s wrap up the equity section with one final question:

To start off in the fixed income section, let’s poll on two economic datapoints first and then use a Fed Fund rate poll as segue into some rate questions.

So, first, the US unemployment rate has been stubbornly low over the past 12-18 months. Here’s a longer-term picture:

And then here’s the big one on everybody’s mind - inflation! Here’s the history of US CPI over the past 100 years as global proxy:

Which brings us the monetary policy rates…

Starting with the US, Fed Fund Futures now discount a full four rate cuts by the end of 2024:

Assuming one rate cut is worth 25 bp, that would bring the Fed Fund rate back to 4.25% (lower boundary).

After its rocket-like ascent, the 10-year yield seems to have finally topped (at least temporarily) out in October of 2023:

For reference, here’s the long-term picture of the US 10-year yield:

Now here’s the USD33.8 Trillion question:

And in Europe? What’s happening in Europe? Here’s the German 10-year Bund as proxy:

Down from 3% intra-year high to 2.20ish as I type. Let’s keep this one simple:

Heading over into the kingdom of currencies, let’s keep it pretty simple, with only three quick questions.

The first regarding the EUR/USD:

Next, here’s the chart of the EUR/CHF rate since roughly two years into my life…

And finally, the 500-pound Currency Gorrilla in the room, the US Dollar to Japanese Yen cross rate, had an epic year:

With the BoJ (Bank of Japan) being rumoured to abandon YCC and NIRP, next year should be another volatile year for the Yen.

And as we are running into 15 (+2) questions already, let’s ask just one for the entire commodity section:

I forgot to throw in the “one question to rule them all” right a the beginning of today’s letter, so let me ask it very elegantly here in form of Bonus Question #1, which will be followed by fun Bonus Question #2.

And there is Bonus Question #2:

Everything in this document is for educational purposes only (FEPO)

Nothing in this document should be considered investment advice

The views expressed in this document may differ from the views published by Neue Private Bank AG

Past performance is hopefully no indication of future performance

Dear André,

Thank you for making our work easer and funnier all year round!

Merry Christmas

Laurent